Acute Intermittent Porphyria Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

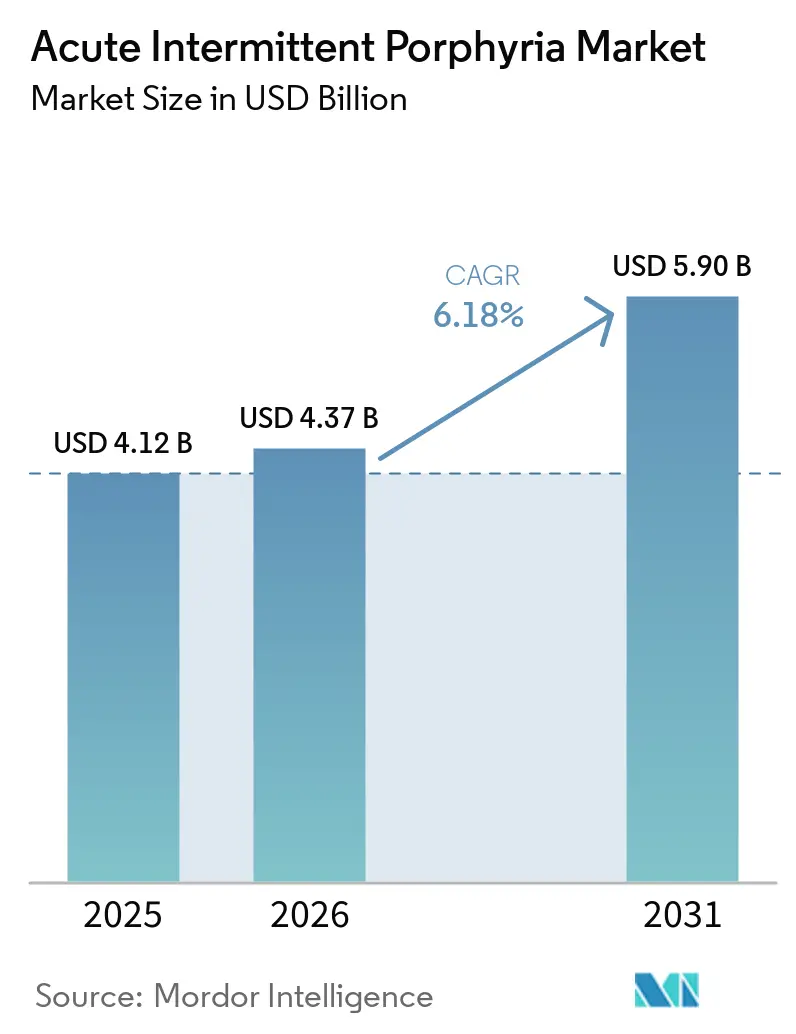

| Market Size (2026) | USD 4.37 Billion |

| Market Size (2031) | USD 5.90 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

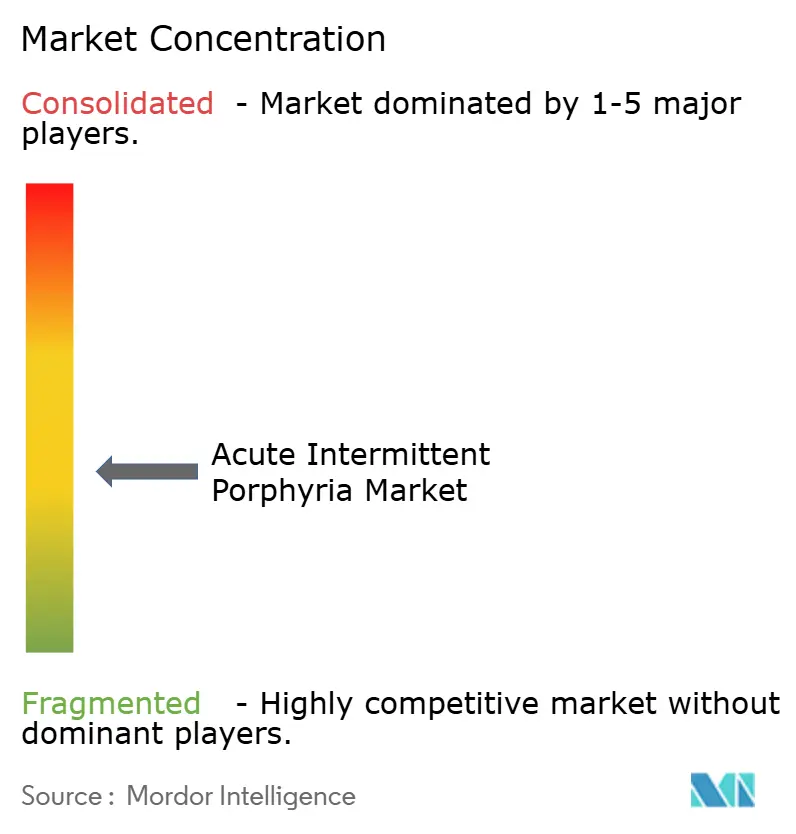

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acute Intermittent Porphyria Market Analysis by Mordor Intelligence

The Acute Intermittent Porphyria Market size is expected to increase from USD 4.12 billion in 2025 to USD 4.37 billion in 2026 and reach USD 5.90 billion by 2031, growing at a CAGR of 6.18% over 2026-2031.

The 2026 revenue run rate reflects steady uptake of RNA interference prophylaxis and a wider diagnostic base shaped by sponsored genetic testing programs, which are bringing more symptomatic patients and at-risk families into formal care pathways. For many years, the acute intermittent porphyria market depended on episodic revenue from IV hemin use and fragmented laboratory testing, which limited treatment duration and kept spending closely tied to acute attacks. The launch of monthly subcutaneous givosiran changed that structure by moving the acute intermittent porphyria market toward chronic disease management, which lifted average revenue per treated patient and extended the treatment horizon beyond crisis care. Referral-network expansion, broader reimbursement for rare disease therapies, and surveillance for liver and kidney complications are now adding recurring demand that persists after diagnosis and even outside acute treatment windows. Growth remains moderated by the very small recurrent-attack pool and by increasing payer pressure for tighter documentation and outcomes-based access terms, which means the acute intermittent porphyria market is expanding on a firmer base but not without reimbursement friction.

Key Report Takeaways

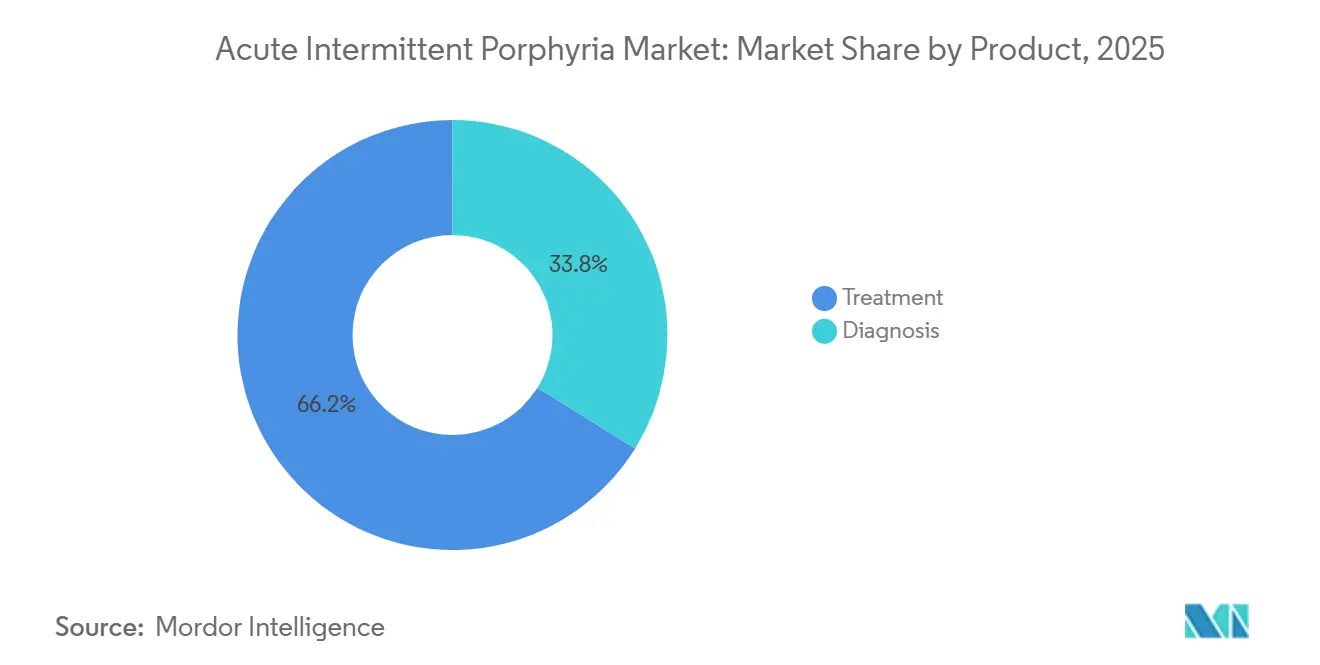

- By product, treatment led with a 66.15% revenue share in 2025, while diagnosis is forecast to expand at a 7.98% CAGR through 2031.

- By end user, hospitals held 48.19% of revenue in 2025, while specialty clinics recorded the highest projected CAGR at 9.52% through 2031.

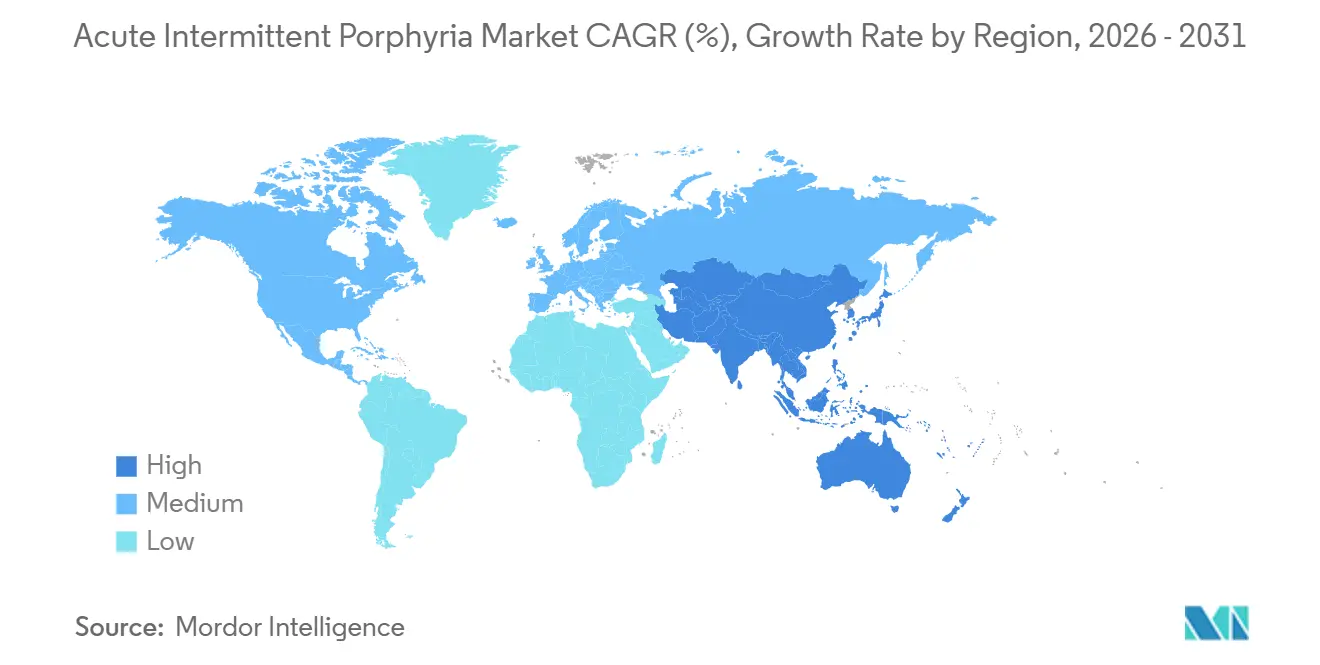

- By geography, North America accounted for 47.16% of revenue in 2025, while Asia-Pacific is advancing at the fastest projected CAGR of 7.33% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Acute Intermittent Porphyria Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Earlier Urine PBG And Genetic Confirmation | +1.2% | Global, highest impact in North America and EU | Short term (≤ 2 years) |

| RNAi Prophylaxis Shifting Care Model | +1.5% | Global, North America and EU leading adoption, APAC accelerating | Medium term (2-4 years) |

| Orphan-Drug Incentives And Reimbursement Expansion | +0.8% | North America and EU core, spillover to Japan and selected APAC markets | Medium term (2-4 years) |

| Expansion Of Referral Networks And Expert Centers | +0.6% | North America and EU, early-stage in APAC and MEA | Medium term (2-4 years) |

| Sponsored Family Cascade Testing | +0.7% | North America and EU primary, Canada reimbursement catalyzing wider interest | Short term (≤ 2 years) |

| HCC And CKD Surveillance Demand | +0.5% | Global, highest in countries with aging AIP cohorts including EU and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Earlier Urine PBG and Genetic Confirmation Compressing the Diagnostic Gap

The diagnostic pathway for acute hepatic porphyrias has remained long, with Canadian guidance published in October 2024 still documenting an average delay of 15 years from symptom onset to confirmation, a lag that continues to limit timely treatment initiation in the acute intermittent porphyria market. Practical recommendations published in Liver International showed that combining biochemical testing with HMBS sequencing lifted confirmed-case detection from 56% with urine ALA and PBG testing alone to 74%, while also identifying asymptomatic carriers who could enter family screening pathways. A 2024 PubMed-indexed study using UCSF and UCLA health record data reported F-scores of 86%-92% for referral identification models and suggested that these tools could shorten diagnosis by 1.2 years, which gives the acute intermittent porphyria market a practical route to improve case finding without relying only on physician memory. The value of that shift extends beyond therapy starts because newly identified patients can remain inside ongoing surveillance programs for liver and kidney complications even when recurrent attacks are not frequent, which broadens longitudinal demand in the acute intermittent porphyria market.

Mayo Clinic Laboratories reinforced this direction in May 2024 when it updated its acute porphyria testing algorithm and placed HMBS panel testing directly within the diagnostic cascade, helping standardize biochemical-to-genetic workups across referral settings. As more laboratories and specialist centers adopt this structure, the acute intermittent porphyria market gains a steadier flow of earlier diagnoses, stronger family tracing, and fewer false-negative exits from the care pathway.

RNAi Prophylaxis Redefining the Treatment Standard

The 48-month open-label extension study for givosiran reported a 97% reduction in annualized attack rates and a 96% reduction in hemin use, confirming that durable prevention is reshaping the treatment profile of the acute intermittent porphyria market. The same study found that all participants became attack-free and hemin-free during months 33-36 onward, which sharply contrasts with the historical crisis-driven treatment model that had long defined revenue in the acute intermittent porphyria market. German real-world evidence published in late 2024 supported that pattern, with annualized attack rates falling from 2.9 to 0.45 in a cohort of 28 patients and 75% of patients reporting clinical improvement under givosiran. This depth of attack suppression materially reduces demand for repeated hemin infusions, which can create institutional friction in settings where acute infusion activity had previously anchored care economics in the acute intermittent porphyria market.

Monthly subcutaneous dosing also pushes routine management toward specialty pharmacy and outpatient settings, which means the acute intermittent porphyria market is no longer centered only on inpatient crisis management. Alnylam’s first quarter 2026 results showed that global patients on GIVLAARI therapy increased by 16% year over year, even while gross-to-net factors moderated reported revenue growth, which signals continued uptake of prophylaxis across the acute intermittent porphyria market.

Orphan-Drug Incentives and Rare-Disease Reimbursement Strengthening Market Access

The reimbursement backdrop for the acute intermittent porphyria market improved in 2025 when broader orphan drug exemptions from Medicare price negotiation were incorporated into U.S. policy changes, extending protection for certain rare disease therapies and improving the planning environment for developers. That shift matters because commercial interest in the acute intermittent porphyria market depends not only on clinical outcomes, but also on whether rare disease products can preserve pricing stability long enough to justify continued investment in very small patient populations.

In Japan, givosiran benefits from National Health Insurance reimbursement and from a 2025 Japanese Dermatological Association guideline that gave the therapy a Grade A, Level II recommendation for recurrent attack prevention, which supports wide clinical acceptance once patients are identified[1]“Porphyria Treatment Guidelines 2025,” Japanese Dermatological Association, dermatol.or.jp. Across Europe, access remains shaped by country-level health technology assessment and managed-entry structures, which reward products that bring real-world evidence packages strong enough to support orphan reimbursement decisions. That means evidence generation now sits close to reimbursement strategy, and companies active in the acute intermittent porphyria market cannot depend on orphan designation alone to drive uptake across major markets. The practical result is a market access environment that is more supportive than it was several years ago, but still selective in favor of well-documented therapies and clearly defined recurrent-attack populations.

Expansion of Porphyria Referral Networks Systematising Patient Identification

The acute intermittent porphyria market is benefiting from formal referral structures because the American Porphyrias Expert Collaborative, which succeeded the earlier consortium model in July 2025, now operates 13 referral centers across the United States and gives clinicians a recognized specialist route for diagnosis, follow-up, and study enrollment. NORD expanded its Rare Disease Centers of Excellence network to 46 institutions across 28 states and Washington, D.C. in December 2025, adding more institutional capacity through which patients with suspected porphyria can be referred, worked up, and retained in specialist care. In Germany, the PoReGer registry linked major academic centers through a REDCap-based infrastructure and IPNET affiliation, which created a structured environment for longitudinal data capture, registry follow-up, and coordinated case handling. These networks help standardize diagnostic thresholds, reduce the number of ambiguous cases that are dismissed without confirmatory testing, and push more borderline presentations toward specialist laboratories rather than back into general practice.

The same structure also supports the acute intermittent porphyria market by making it easier to recruit patients into registries and trials, which strengthens real-world evidence at the same time that it improves case identification. As referral systems mature, the acute intermittent porphyria market gains not only more diagnosed patients, but also a more predictable framework for ongoing surveillance, specialist management, and therapy selection.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Orphan-Therapy Cost And Payer Controls | -1.5% | Global, most acute in price-sensitive APAC markets and multi-indication EU payers | Medium term (2-4 years) |

| Persistent Symptom Overlap And Diagnostic Delay | -1.0% | Global, disproportionately affects non-specialist settings in emerging markets and rural areas | Short term (≤ 2 years) |

| Givosiran And Chronic Hemin Monitoring Burden | -0.6% | Global, highest in low-resource settings and markets with limited hepatology and nephrology infrastructure | Medium term (2-4 years) |

| Tiny Recurrent-Attack Pool Limiting Pipeline ROI | -0.5% | Global, most restrictive for pipeline entrants targeting North American and EU launches | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Orphan-Therapy Cost and Payer Controls Compressing Access

The acute intermittent porphyria market still faces a meaningful access ceiling because payers continue to evaluate rare disease therapies through budget impact, contracting structure, and documentation standards rather than through efficacy data alone. Alnylam’s 2024 rare disease payer report noted that 5 of the top 10 payer access decision drivers focused on cost and contracting, and it also showed that prior authorization tied to laboratory evidence remained a standard gatekeeping tool for high-cost orphan therapies[2]“2024 Rare Disease Trend Report,” Alnylam Pharmaceuticals, alnylam.com. European access is also uneven because national reimbursement systems apply different standards for clinical value and pricing, which can preserve formal availability but still slow commercial uptake between countries.

The Congressional Budget Office estimated in October 2025 that broader orphan exemptions from Medicare price negotiation would carry a USD 8.8 billion fiscal effect over 10 years, which shows how central price policy has become to the long-term shape of the acute intermittent porphyria market. Those pressures intensify when payers are reviewing chronic prophylaxis for patients whose attack burden may be intermittent, because outcomes-based contracts and tighter documentation can become the compromise route to preserve access. The acute intermittent porphyria market therefore supports high-need use, but still encounters reimbursement resistance when sponsors seek broader use beyond clearly defined recurrent-attack populations.

Persistent Symptom Overlap and Diagnostic Delay Limiting Market Penetration

Severe abdominal pain remains the most common symptom in acute attacks and was reported in 85%-95% of cases in the revised Panhematin prescribing information, but that presentation still overlaps with many more common gastrointestinal and gynecologic conditions. Canadian guidance published in 2024 continued to document an average diagnostic delay of 15 years, which shows how often the acute intermittent porphyria market loses patients before confirmatory testing is even considered. Recommendations focused on atypical patient populations also showed that porphyria can present outside classic attack patterns, which makes specialist referral less consistent in emergency medicine, psychiatry, gastroenterology, and primary care.

That overlap means a large share of the clinically addressable population remains outside the treated funnel, which holds back therapy uptake in the acute intermittent porphyria market even when effective options are available. Closing the gap requires sustained education and repeat testing discipline across several specialties, and that burden is too broad for any single commercial sponsor to solve quickly at global scale. The acute intermittent porphyria market therefore continues to expand under the weight of real clinical need, but it still grows more slowly than treatment efficacy results alone would suggest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Treatment Revenue Anchors the Market as Diagnostics Accelerate

Treatment accounted for 66.15% of acute intermittent porphyria market share in 2025, reflecting the therapy-heavy spending structure created by high-value biologics, IV hemin use, and the continuing cost of managing acute episodes and follow-up care. Within the acute intermittent porphyria industry, IV hematin and heme arginate remain central to acute attack therapy, while supportive symptom management for pain, nausea, and seizure control provides steadier but lower-value revenue across both hospital and outpatient pathways. Preventive pharmacotherapy is expanding faster within treatment because GIVLAARI moved care into a recurring monthly model, and company-reported financial results showed FY2025 GIVLAARI net revenues of nearly USD 308 million, followed by USD 74.4 million in the first quarter of 2026 with 11% year-over-year growth. Definitive interventions remain small in current revenue terms, but the category is still important to watch because gene editing and related liver-directed approaches could eventually change how the acute intermittent porphyria market values one-time or infrequent treatment options.

The acute intermittent porphyria market size for diagnosis is projected to expand at a 7.98% CAGR between 2026 and 2031, making it the fastest-growing product area as testing pathways become broader, more structured, and more proactive. That growth is being driven by sponsored no-cost testing programs, greater use of HMBS gene panels inside porphyria algorithms, EHR-based referral tools, and family cascade testing after each newly confirmed case, all of which expand the diagnosed base that feeds the acute intermittent porphyria market. Practical recommendations in Liver International noted that HMBS sequencing identifies pathogenic variants in 96%-98% of probands, which explains why DNA testing is outgrowing traditional urine testing as clinical practice increasingly seeks genetic confirmation after biochemical suspicion. Diagnostic spending is also widening because plasma-based assessment is gaining importance in patients with chronic kidney disease and because nationally commissioned genomic pathways are making DNA confirmation a more routine part of the acute intermittent porphyria market rather than an exceptional add-on.

By End User: Hospitals Underpin Volume While Specialty Clinics Gain Ground

Hospitals held 48.19% of end-user revenue in 2025 and remained the largest setting in the acute intermittent porphyria market because acute attacks still require urgent assessment, inpatient stabilization, and pharmacy control over IV hemin distribution. Data from Germany’s PoReGer network showed that more than 75% of attack patients required hospitalization, which supports the continued central role of tertiary centers in the acute intermittent porphyria market even as prophylaxis use rises. Hospital demand is further supported by the monitoring burden attached to long-term givosiran use, where liver function, renal function, and metabolic parameters still need coordinated specialist oversight. Reference laboratories and genetic testing centers remain a structurally important end-user layer because a large share of quantitative ALA and PBG testing, porphyrin workups, and HMBS analysis continues to move through specialized external testing platforms rather than only through local hospital laboratories.

The acute intermittent porphyria market size for specialty clinics is projected to expand at a 9.52% CAGR through 2031, making this the fastest-growing end-user category as chronic care increasingly shifts away from inpatient settings. Monthly subcutaneous dosing, rising patient preference for planned outpatient management, and the spread of dedicated porphyria services within hepatology, hematology, and metabolic medicine are all moving the acute intermittent porphyria market toward specialist ambulatory care. The Massachusetts General Hospital Porphyria Center, which follows more than 150 porphyria patients through monthly specialist clinics, illustrates the outpatient model that referral networks are helping replicate across major centers. Research centers and clinical trial sites remain smaller in revenue terms, but they matter strategically because the APEX longitudinal study was active at 13 U.S. sites in January 2026 and because pipeline programs such as CTX450 keep academic porphyria centers engaged in trial infrastructure.

Geography Analysis

North America held 47.16% of acute intermittent porphyria market share in 2025, which kept the region in the leading position on the strength of high per-patient therapy spending, dense referral capacity, and wider access to prophylaxis. The region benefits from the deepest concentration of APEX centers and from the wider NORD Centers of Excellence network, both of which improve patient routing, long-term follow-up, and enrollment into specialist care pathways. Canada expanded access in December 2024 when GIVLAARI achieved broad reimbursement across public and private plans, reducing a prior treatment gap for patients who had been limited mainly to IV hemin. Manufacturer-sponsored identification programs also strengthened the regional funnel after the Alnylam Act testing program moved to PreventionGenetics in March 2025, creating a no-cost genetic testing route for eligible patients in the United States and Canada.

Europe retains a meaningful share of the acute intermittent porphyria market because the region combines orphan-drug infrastructure, specialist referral systems, and established use of hemin and prophylaxis in recurrent-attack populations. Germany is a leading European setting because its early-access environment and registry-based evidence generation through PoReGer support adoption and strengthen reimbursement dialogue over time. France and Spain apply tighter health technology assessment and pricing review, which can moderate per-unit revenue while still preserving access for patients who meet prophylaxis criteria. Across the region, launch planning in the acute intermittent porphyria market increasingly depends on real-world evidence, managed-entry design, and country-specific negotiation strategy rather than on regulatory approval alone.

Asia-Pacific is the fastest-growing geography, and acute intermittent porphyria market size in the region is projected to expand at a 7.33% CAGR through 2031. Japan anchors regional growth because National Health Insurance reimburses givosiran and because the 2025 Japanese Dermatological Association guideline gave the drug its strongest clinical endorsement for recurrent acute hepatic porphyria attack prevention. An expanded-access study in 10 Japanese patients published in Scientific Reports found urinary ALA and PBG normalization in all participants and reported only non-serious adverse events, which supports continued uptake in the Japanese acute intermittent porphyria market. China, India, South Korea, and Australia represent the larger structural opportunity because underdiagnosis is still considerable, molecular testing pathways are less mature, and referral depth remains uneven outside top centers. South America contributes a modest but growing base where authorizations are in place, while the Middle East and Africa remain early-stage settings where genomics investment is improving diagnostic capacity more quickly than therapy penetration.

Competitive Landscape

The acute intermittent porphyria market has a split competitive structure in which treatment is concentrated, while diagnostics remains broadly fragmented across reference laboratories, genetic testing centers, and hospital-based testing platforms. On the treatment side, Alnylam Pharmaceuticals leads prophylaxis through GIVLAARI and Recordati Rare Diseases holds the hemin franchise through Panhematin in North America and Normosang in Europe, which gives the acute intermittent porphyria market a near-duopoly in core therapy categories. Alnylam’s first quarter 2026 results showed continued patient growth and USD 74.4 million in quarterly GIVLAARI net revenue, confirming that the product is a durable commercial asset rather than a short-lived orphan launch. Recordati’s position remains durable because IV hemin is still required in acute attack care, and continued label maintenance for Panhematin shows that the company is still supporting this part of the acute intermittent porphyria market[3]“PANHEMATIN, Hemin Powder, for Solution,” DailyMed, dailymed.nlm.nih.gov.

The most open competitive white space in the acute intermittent porphyria market sits in 3 areas, potential one-time intervention platforms, diagnostic consolidation, and structured surveillance services. CRISPR Therapeutics kept attention on that first area by highlighting CTX450 as an anticipated 2025 milestone, which shows that curative or near-curative strategies are still being positioned as future challenges to chronic prophylaxis. Diagnostics is still highly fragmented because testing volume is spread across many vendors, which means a platform that combines porphyria expertise, rapid turnaround, and EHR connectivity could gradually take referral share in the acute intermittent porphyria market. Surveillance is also commercially underdeveloped because annual liver and biomarker follow-up for older patients with AIP is recommended by both the MSD Manual and Japanese guidance, yet this demand is still captured through general care pathways rather than through dedicated disease management programs. Machine-learning referral tools add another layer to competition because they can widen the diagnosed base faster than traditional awareness campaigns, and the UCSF and UCLA study showing F-scores above 86% suggests that this route could materially shape future growth in the acute intermittent porphyria market.

Strategic moves in the acute intermittent porphyria market have centered more on access, evidence, and referral generation than on broad product-line expansion. Alnylam strengthened its commercial position by supporting no-cost genetic testing through the Alnylam Act program and then transferring program management to PreventionGenetics in 2025, which turned patient identification into a structured franchise-support tool. The company also used long-term extension data and reimbursement expansion in Canada to reinforce the chronic-care positioning of GIVLAARI across the acute intermittent porphyria market. Recordati, by contrast, has remained relevant through its entrenched acute-care role, while specialist laboratories continue to compete on speed, menu depth, and referral relationships rather than on scale alone, leaving the acute intermittent porphyria market moderately concentrated in treatment and widely dispersed in diagnostics.

Acute Intermittent Porphyria Industry Leaders

Alnylam Pharmaceuticals, Inc.

Recordati Rare Diseases

Labcorp

Quest Diagnostics

Mayo Clinic Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Global Porphyria Advocacy Coalition announced the official Spanish-language launch of the NAPOS Safe Drugs Database for the acute hepatic porphyrias, an internationally recognized clinical reference developed by the Norwegian Porphyria Centre to support medication safety assessment in porphyria patients.

- December 2025: The National Organization for Rare Disorders expanded its Rare Disease Centers of Excellence network to 46 institutions across 28 US states and Washington, D.C., adding seven academic medical centers. The network aims to reduce rare-disease diagnostic timelines, which average 5 to 7 years, and increases the infrastructure through which AIP patients can be identified, referred, and enrolled in longitudinal studies.

Global Acute Intermittent Porphyria Market Report Scope

As per the scope of the report, acute intermittent porphyria is a rare genetic disorder characterized by a deficiency of the enzyme hydroxymethylbilane synthase (also known as porphobilinogen deaminase) in the heme biosynthesis pathway. This deficiency leads to the accumulation and increased excretion of porphyrin precursors, particularly delta-aminolevulinic acid (ALA) and porphobilinogen (PBG), which can cause a range of acute neurological and gastrointestinal symptoms.

The segmentation of the acute intermittent porphyria market is categorized by product, diagnosis, treatment, end user, and geography. By diagnosis, the market includes urine testing, blood/erythrocyte testing, serum/plasma testing, and DNA testing. By treatment, it is segmented into acute attack therapy, preventive pharmacotherapy, supportive symptom management, and definitive/advanced interventions. Acute attack therapy comprises IV hematin/hemin, heme arginate, and carbohydrate loading. Preventive pharmacotherapy includes RNAi therapy and GnRH analogues. Supportive symptom management focuses on pain control, antiemetics and autonomic symptom control, and seizure and electrolyte management. Definitive/advanced interventions cover liver transplantation and gene therapy/mRNA/enzyme replacement pipeline. By end user, the market is divided into hospitals, specialty clinics, reference laboratories and genetic testing centers, and research centers and clinical trial sites. By geography, the market spans North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| By Diagnosis | Urine Testing | |

| Blood / Erythrocyte Testing | ||

| Serum / Plasma Testing | ||

| DNA Testing | ||

| By Treatment | Acute Attack Therapy | IV hematin / hemin |

| Heme arginate | ||

| Carbohydrate loading | ||

| Preventive Pharmacotherapy | RNAi therapy | |

| GnRH analogues | ||

| Supportive Symptom Management | Pain control | |

| Antiemetics and autonomic symptom control | ||

| Seizure and electrolyte management | ||

| Definitive / Advanced Interventions | Liver transplantation | |

| Gene therapy / mRNA / enzyme replacement pipeline | ||

| Hospitals |

| Specialty clinics |

| Reference laboratories and genetic testing centers |

| Research centers and clinical trial sites |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | By Diagnosis | Urine Testing | |

| Blood / Erythrocyte Testing | |||

| Serum / Plasma Testing | |||

| DNA Testing | |||

| By Treatment | Acute Attack Therapy | IV hematin / hemin | |

| Heme arginate | |||

| Carbohydrate loading | |||

| Preventive Pharmacotherapy | RNAi therapy | ||

| GnRH analogues | |||

| Supportive Symptom Management | Pain control | ||

| Antiemetics and autonomic symptom control | |||

| Seizure and electrolyte management | |||

| Definitive / Advanced Interventions | Liver transplantation | ||

| Gene therapy / mRNA / enzyme replacement pipeline | |||

| By End User | Hospitals | ||

| Specialty clinics | |||

| Reference laboratories and genetic testing centers | |||

| Research centers and clinical trial sites | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is driving growth in acute intermittent porphyria treatment demand?

Growth is being supported by wider use of givosiran, which moved care from attack treatment toward prevention, and by broader diagnosis through genetic testing and referral networks. The market is forecast to reach USD 5.90 billion by 2031 from USD 4.37 billion in 2026.

Why is diagnosis becoming a larger revenue contributor in AIP care?

Diagnosis is the fastest-growing product area, with a 7.98% CAGR through 2031, because combined biochemical and genetic testing confirms more cases and brings more families into cascade screening.

Which care setting leads AIP management today?

Hospitals remained the largest end-user segment in 2025 with 48.19% share because acute attacks still require inpatient care, IV hemin use, and close monitoring for complex patients.

Why are specialty clinics gaining importance in porphyria care?

Specialty clinics are projected to grow at a 9.52% CAGR through 2031 as monthly subcutaneous prophylaxis and planned follow-up shift more chronic management away from inpatient settings.

Which region is growing fastest for AIP-related products and services?

Asia-Pacific is the fastest-growing region at a 7.33% CAGR through 2031, helped by Japans reimbursement and guideline support, along with a large underdiagnosed patient pool across major regional markets.

How concentrated is competition in this space?

Treatment competition is relatively concentrated around Alnylam and Recordati, but diagnostics is fragmented across many laboratories and hospital platforms, which keeps the overall structure less concentrated than the therapy segment alone suggests.

Page last updated on: