Acetylene Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

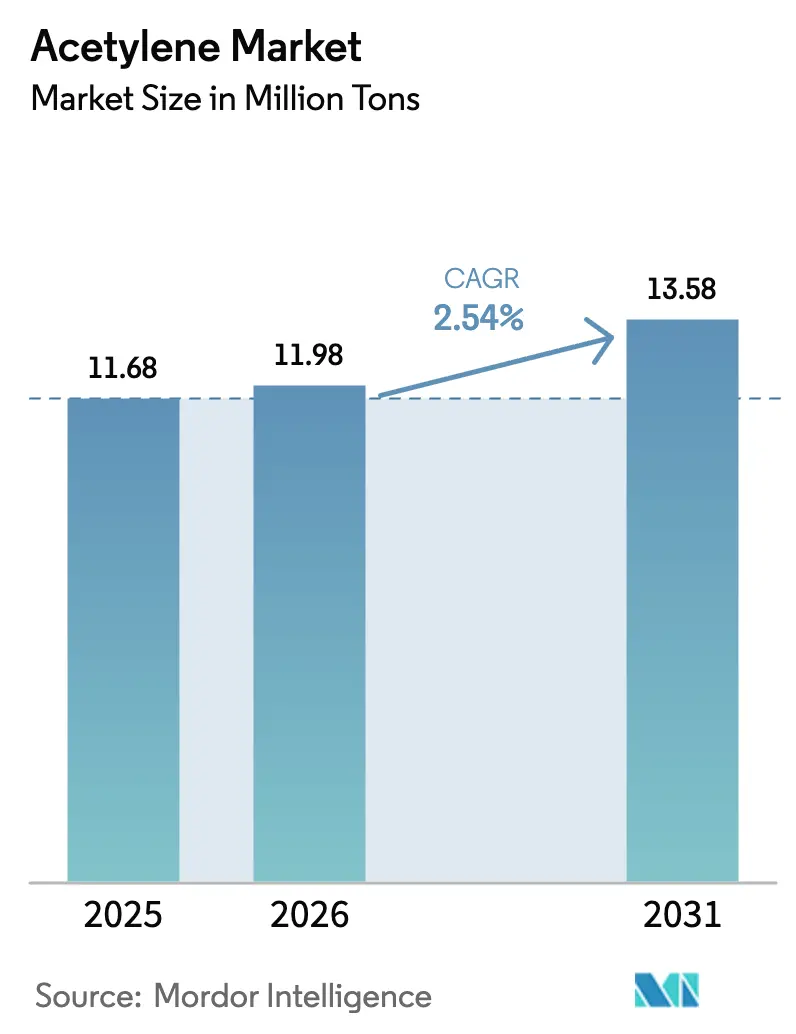

| Market Volume (2026) | 11.98 Million tons |

| Market Volume (2031) | 13.58 Million tons |

| Growth Rate (2026 - 2031) | 2.54% CAGR |

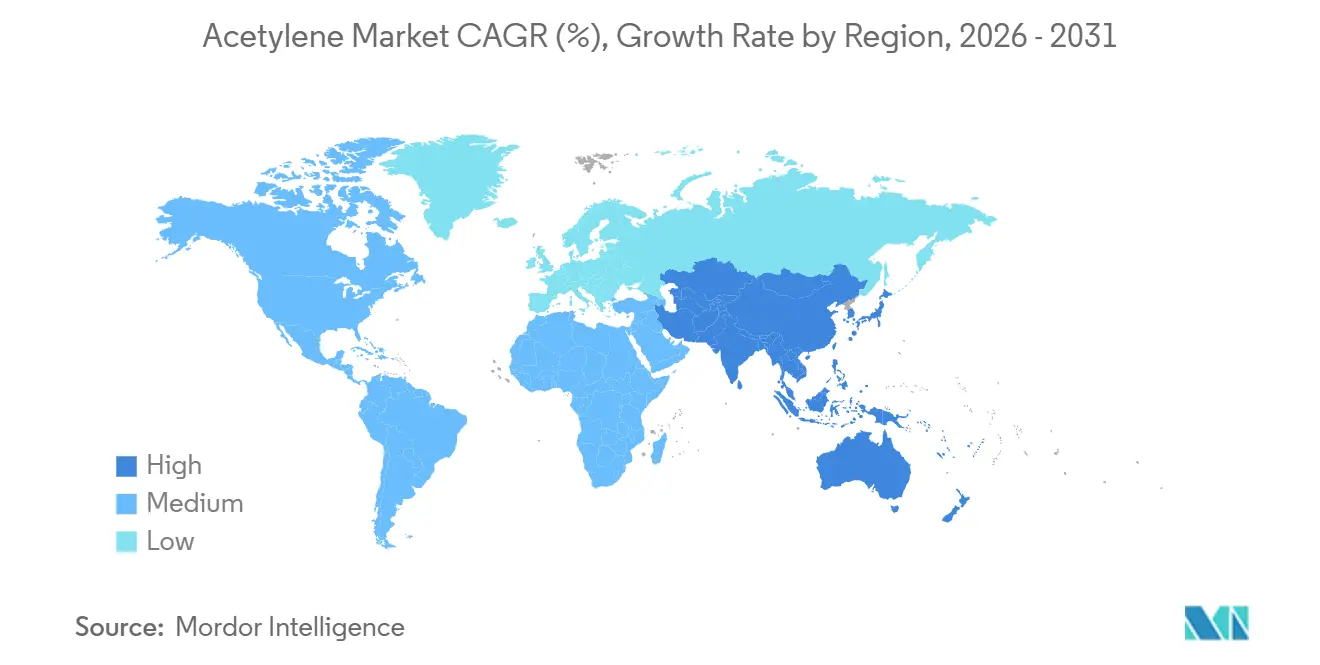

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

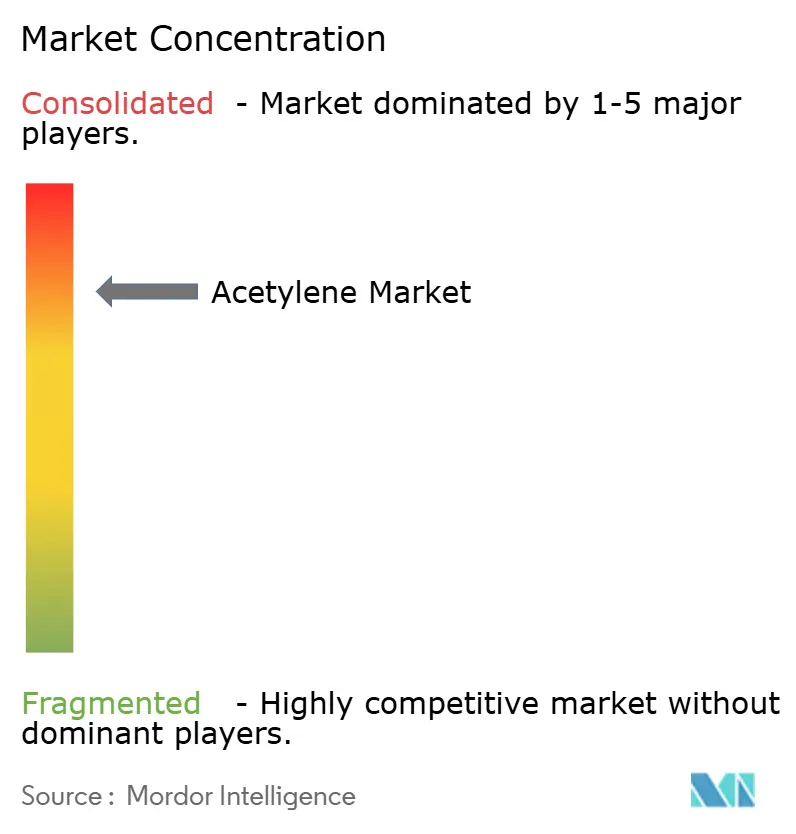

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acetylene Market Analysis by Mordor Intelligence

The Acetylene Market size is expected to increase from 11.68 Million tons in 2025 to 11.98 Million tons in 2026 and reach 13.58 Million tons by 2031, growing at a CAGR of 2.54% over 2026-2031. Rising demand for high-purity grades in battery materials, sustained metal fabrication activity, and a gradual pivot toward greener production routes are shaping volume growth. Chemical raw-material applications, notably specialty solvents and battery-grade acetylene black, are expanding fastest as manufacturers revisit C₂ chemistry to diversify away from traditional ethylene pathways. At the same time, modular on-site generators are shifting supply dynamics by lowering logistics costs for large fabricators. Competitive strategies center on capacity additions in Asia-Pacific, process innovations that lower carbon intensity, and selective acquisitions that enlarge geographic footprints. Safety regulation and fuel-gas substitution pressure temper overall momentum but continue to reward operators with superior compliance records and scale advantages.

Key Report Takeaways

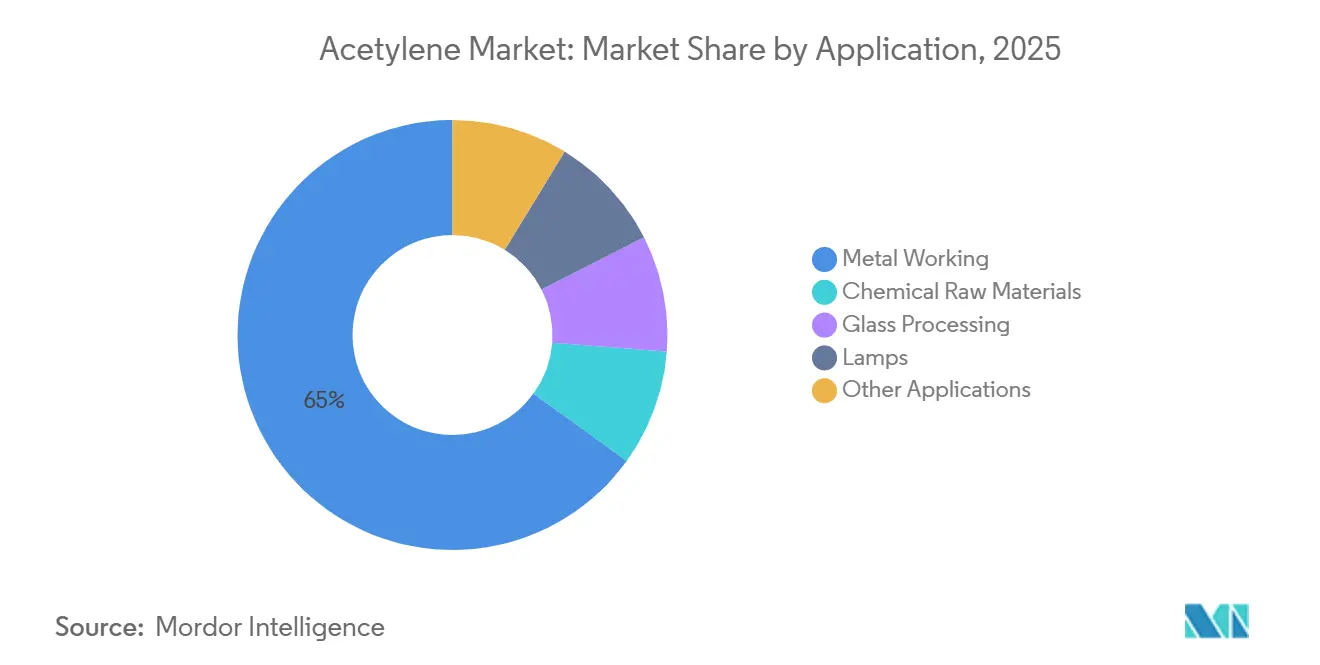

- By application, metal working held 65.04% of the acetylene market share in 2025, while chemical raw materials posted the highest forecast CAGR at 3.27% through 2031.

- By geography, Asia-Pacific commanded 81.91% of global volume in 2025 and is advancing at a 2.71% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Acetylene Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from metalworking and fabrication | +0.8% | Asia-Pacific, North America | Medium term (2-4 years) |

| Rising PVC and downstream vinyl production in Asia | +0.6% | China, ASEAN | Short term (≤ 2 years) |

| Infrastructure-led construction boom in emerging economies | +0.5% | India, Middle East, South America | Medium term (2-4 years) |

| Surge in acetylene-black use for Li-ion batteries | +0.4% | Japan, Thailand, China; spill-over to North America, Europe | Long term (≥ 4 years) |

| Modular on-site acetylene generators gaining traction | +0.3% | North America, Europe, early Asia-Pacific clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand From Metalworking And Fabrication

Legacy oxy-acetylene cutting and welding technologies retain prominence in construction sites, shipyards, and remote maintenance settings where reliable grid power is unavailable. The acetylene market benefits from the gas’s 3,160 °C flame temperature, which cuts steel faster than alternative fuels. However, plasma and laser systems are making inroads in automated workshops, incrementally trimming acetylene volumes in high-precision fabrication. Demand therefore skews toward low-volume, high-mobility tasks and infrastructure builds in emerging economies, keeping growth in line with overall market averages.

Rising PVC And Downstream Vinyl Production In Asia

Cost-advantaged coal-to-calcium-carbide complexes in China underpin the acetylene route to vinyl chloride monomer, sustaining regional dominance even as global producers favor ethylene-based chemistry. Recent capacity additions in Inner Mongolia and Xinjiang leverage amortized assets and local energy subsidies, boosting near-term consumption. Provincial emission caps are tightening, yet ASEAN vinyl producers in Thailand, Vietnam, and Indonesia are scaling downstream PVC output, partially offsetting any decarbonization-driven slowdowns in mainland China.

Infrastructure-Led Construction Boom In Emerging Economies

Large transportation and housing projects across India, Saudi Arabia, and Brazil require on-site metal fabrication that values acetylene’s portability. National safety codes governing storage cylinders and explosive atmospheres raise compliance costs, which entrench established distributors and limit smaller entrants, but project pipelines stretching through 2030 safeguard volume growth. Suppliers are positioning depots close to megaprojects to reduce delivery lead times and secure multi-year contracts.

Surge In Acetylene-Black Use For Li-Ion Batteries

Rayong’s acetylene black facility, a Denka-SCG venture, is ramping up output for high-nickel cathode conductive additives[1]Denka Company Limited, “Denka and SCG Establish Joint Venture for Acetylene Black Production in Thailand,” denka.co.jp. The material’s superior conductivity and morphology compared with conventional carbon blacks position acetylene black as the standard for premium EV battery cells. While its share of total acetylene consumption is modest, the price premium and long-term battery outlook drive a measurable uplift to overall demand, particularly in the Asia-Pacific, where most gigafactories cluster.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent environmental and safety regulations | -0.5% | Europe, North America; tightening in Asia | Short term (≤ 2 years) |

| Substitution by alternative fuel gases (propane, LPG, LNG) | -0.4% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Escalating industrial-insurance premiums after safety incidents | -0.2% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental And Safety Regulations

Global regulations deem acetylene as highly flammable and unstable. To counteract decomposition, they mandate the use of porous-mass cylinders filled with solvent. Compliance with U.S. OSHA PSM, European REACH, and China’s dual-carbon mandates raises production and handling costs. Smaller distributors struggle to absorb audit expenses and frequent cylinder inspections, thereby consolidating supply in the hands of multinational firms that can leverage scale to meet the stricter standards.

Substitution By Alternative Fuel Gases (Propane, LPG, LNG)

Propane delivers more energy per cubic foot compared to acetylene, and its cylinders are easier to handle because they avoid shock-sensitive acetylides. Many North American and European shops now reserve acetylene for piercing while shifting pre-heating and general cutting to oxy-propane, trimming overall acetylene volumes. Urban centers in Asia-Pacific are beginning to follow this cost-centric trend, although remote sites still favor acetylene’s portable high-temperature flame.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Specialty Chemistry Gains Momentum Over Legacy Fabrication

Global metal working accounted for 65.04% of the acetylene market share in 2025. The segment owes its volume lead to decades of entrenched oxy-acetylene infrastructure in construction, shipbuilding, and field maintenance. However, capital-intensive plasma and laser systems are capturing precision jobs inside automated factories, generating a gradual volume shift. Chemical raw materials trail in absolute tonnage yet post the fastest 3.27% CAGR, reflecting renewed interest in acetylene-based 1,4-butanediol, tetrahydrofuran, and vinyl acetate. Environmental regulators encourage this pivot by scrutinizing ethylene-derived routes, prompting specialty-chemical producers to revisit acetylene’s C₂ advantage. Glass processing, lamps, and other niche uses maintain stable but low volumes, collectively offering limited upside to the wider acetylene market size narrative.

The acetylene industry is also witnessing heightened research and development into biochar-to-calcium-carbide routes and plasma-assisted methane cracking. These emerging pathways promise lower carbon footprints and could qualify for green-chemistry incentives in Europe and East Asia. Should technology demonstrations scale successfully, chemical applications may accelerate further, tightening supply in traditional welding markets and intensifying the search for efficiency gains among metal-fabrication end users. Overall, application-mix evolution supports price stability even as volumes shift toward high-margin specialty outlets.

Geography Analysis

Asia-Pacific held 81.91% of global volume in 2025 and is on track for a 2.71% CAGR to 2031, underscoring its dual status as the principal producer and consumer of acetylene. China anchors this dominance through fully amortized coal-to-calcium-carbide complexes in Xinjiang and Inner Mongolia that deliver dissolved acetylene to vinyl chloride, solvent, and battery-carbon value chains. New units—such as Xinjiang Mingli Gas’s facility—represent late-cycle additions ahead of stricter emissions ceilings that will temper future expansions. Japan and South Korea exhibit mature consumption centered on electronics and precision welding, whereas Thailand’s Denka-SCG plant elevates the country to regional hub status for battery-grade acetylene black.

Imports and recovery from petrochemical steam crackers, utilizing dimethylformamide extraction, predominantly meet North America's demand. Integrated chemical companies monetize by-product acetylene internally, leaving metal-fabrication markets to merchant gas firms. Regulatory compliance under OSHA drives consistent but flat growth, and substitution by propane is most pronounced in high-labor-cost regions that optimize total ownership economics over peak flame temperature.

Europe tallies a similar volume share to North America but faces higher compliance costs under REACH and the Industrial Emissions Directive. Germany’s BASF operates an acetylene unit at Ludwigshafen that feeds captive chemical chains rather than merchant outlets, illustrating the trend toward integrated producer-consumer models[2]BASF SE, “Ludwigshafen Site Information – Acetylene Production,” basf.com . The United Kingdom and French markets remain dependent on cylinder distribution for shipbuilding and aerospace maintenance, yet propane displacement limits incremental growth potential.

South America and the Middle East-Africa together represent a small share of the acetylene market. Brazil and Argentina experience project-driven spikes tied to infrastructure megaprojects, though currency volatility and import dependency cap sustained gains. In the Middle East, Saudi Arabia and the UAE show robust demand linked to NEOM and Expo 2030 construction, but logistics constraints necessitate strategic storage hubs to ensure continuity of supply. Nigeria and Egypt remain nascent, characterized by fragmented distribution networks that often operate outside formal regulatory frameworks.

Competitive Landscape

The acetylene market is consolidated. Multinational industrial gas majors dominate high-volume segments by leveraging scale, proprietary cylinder technology, and established safety records. Specialty niches are less consolidated. Process-innovation race is intensifying: plasma-assisted methane cracking and biochar-derived calcium carbide are key research and development frontiers as producers aim to decarbonize portfolios and secure future carbon-credit revenues. Modular generator manufacturers target large fabricators willing to assume on-site production risk, but regulatory permitting remains a barrier. Concurrently, integrated chemical companies with captive acetylene units will continue internalizing consumption, limiting merchant-market growth in mature economies. The competitive arena is therefore bifurcated between high-volume integrated chains and high-margin specialty segments that reward technological differentiation.

Acetylene Industry Leaders

Linde plc

Gulf Cryo

Air Liquide

China Petrochemical Corporation.

Koatsu Gas Kogyo Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: HydroGraph Clean Power Inc. signed a strategic agreement with a North American gas supplier and announced plans for a Texas facility that will rely on high-purity acetylene to scale detonation-synthesized pristine graphene.

- April 2025: Denka Company Limited terminated its microwave-plasma low-carbon acetylene project following the dissolution of partner Transform Materials but reaffirmed its commitment to develop alternative low-CO₂ acetylene technologies and meet 2050 carbon-neutral targets.

Global Acetylene Market Report Scope

Acetylene, or ethyne, is a colorless and highly flammable gas known for its distinct, unpleasant odor. With the chemical formula C₂H₂, it stands as the simplest form of alkyne, a category of hydrocarbons. Due to its high reactivity, acetylene serves crucial roles in diverse industrial and commercial sectors. It's prominently used as a fuel in oxyacetylene welding and metal cutting, and it acts as a primary raw material in producing a wide range of organic chemicals and plastics.

The acetylene market is segmented by application and geography. By application, the market is segmented into metal working, chemical raw materials, glass processing, lamps, and other applications. The report also covers the market sizes and forecasts for the global acetylene market in 22 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (Tons).

| Metal Working |

| Chemical Raw Materials |

| Glass Processing |

| Lamps |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Nigeria | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Metal Working | |

| Chemical Raw Materials | ||

| Glass Processing | ||

| Lamps | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Nigeria | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current global volume of the acetylene market?

It stands at 11.98 million tons in 2026 and is forecast to reach 13.58 million tons by 2031.

Which region dominates acetylene consumption?

Asia-Pacific holds about 81.91% of global volume, anchored by China’s coal-to-carbide infrastructure.

Why is acetylene black important for electric-vehicle batteries?

Its superior conductivity and particle morphology enhance high-nickel cathode performance, making it the preferred conductive additive for premium EV cells.

How are environmental regulations affecting acetylene producers?

Stricter safety and emissions rules raise compliance costs, favor large integrated suppliers, and encourage research and development into low-carbon production routes.

What trends are shaping supply models for large fabricators?

Modular on-site acetylene generators are gaining traction, reducing cylinder logistics and offering cost advantages where daily demand is high.

Which application segment is growing fastest?

Chemical raw materials, including specialty solvents and battery-grade carbons, are forecast to expand at a 3.27% CAGR through 2031.

Page last updated on: