A-Si X-ray Flat Panel Detectors Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

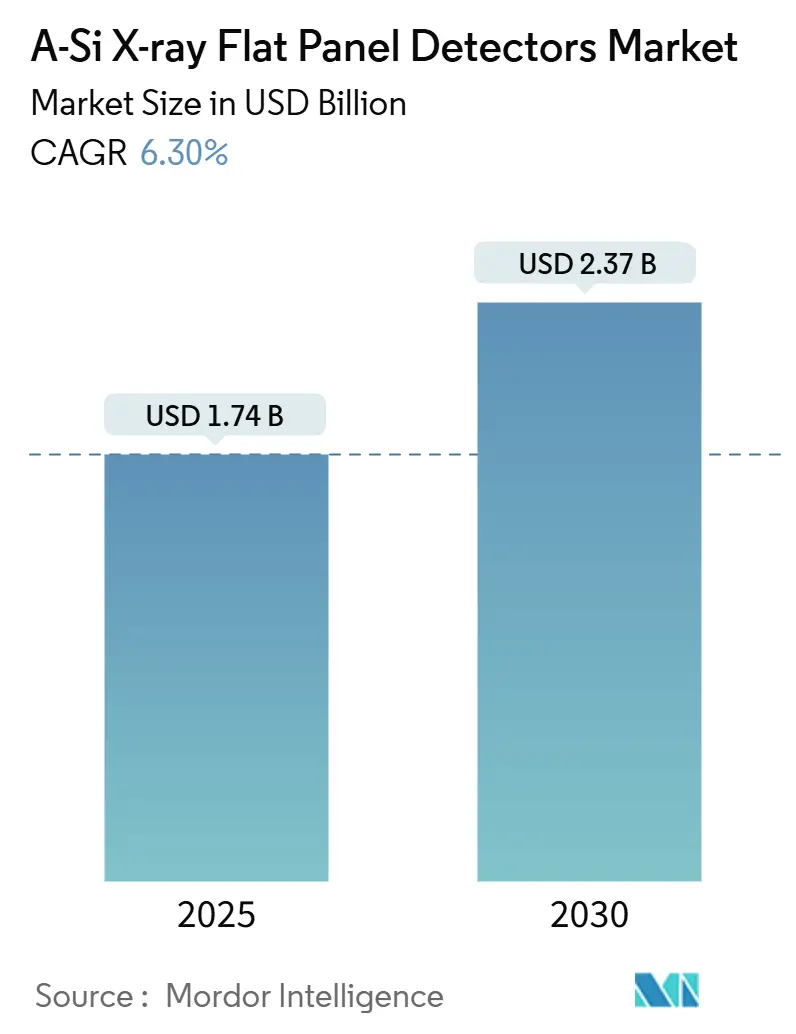

| Market Size (2025) | USD 1.74 Billion |

| Market Size (2030) | USD 2.37 Billion |

| Growth Rate (2025 - 2030) | 6.30% CAGR |

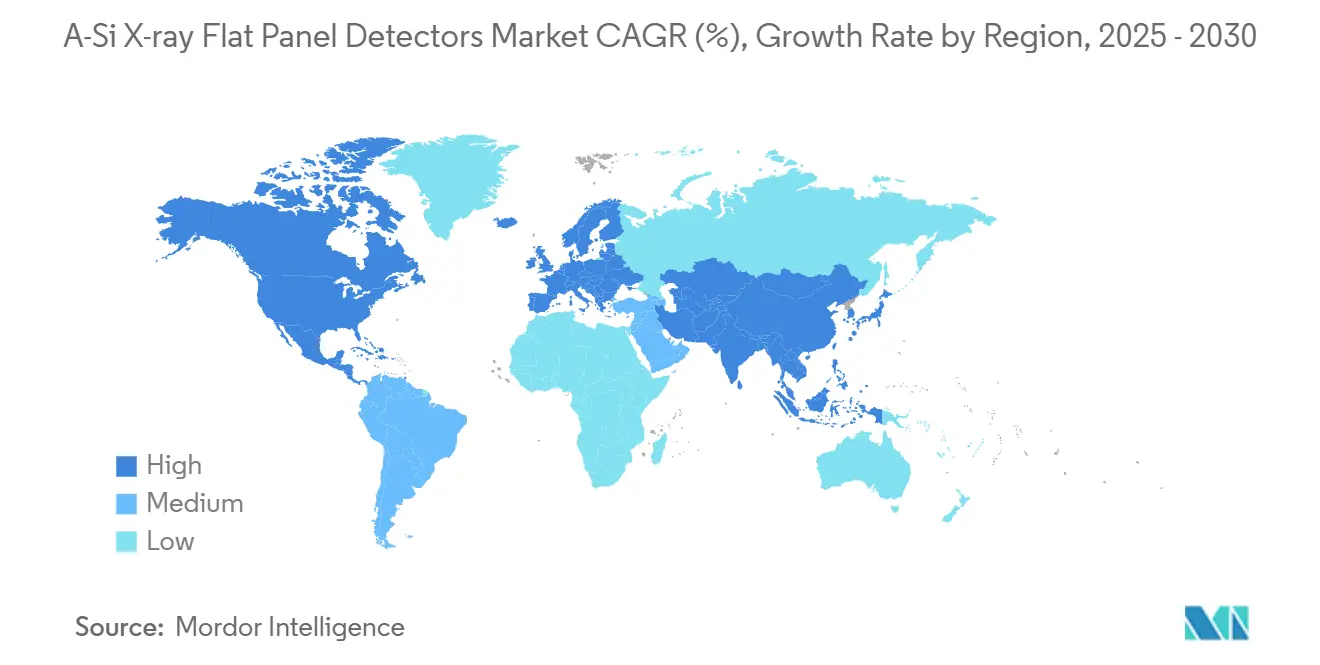

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

A-Si X-ray Flat Panel Detectors Market Analysis by Mordor Intelligence

The a-Si X-ray Flat Panel Detectors market size touched USD 1.74 billion in 2025 and is projected to climb to USD 2.37 billion by 2030, reflecting a 6.30% CAGR. Advancing detector design, artificial-intelligence calibration, and the push toward mobile point-of-care imaging underpin this steady expansion even as substrate shortages and regulatory hurdles introduce cost and timing risk. Hospitals in high-income nations replace computed-radiography bays to avoid reimbursement penalties, while facilities in emerging economies leapfrog directly to wireless panels, accelerating installation cycles. Low-dose pediatric protocols, wider industrial inspection use, and dental CBCT integration diversify revenue streams. These trends collectively keep the a-Si X-ray Flat Panel Detectors market on a resilient mid-term growth path despite episodic supply disruptions.

Key Report Takeaways

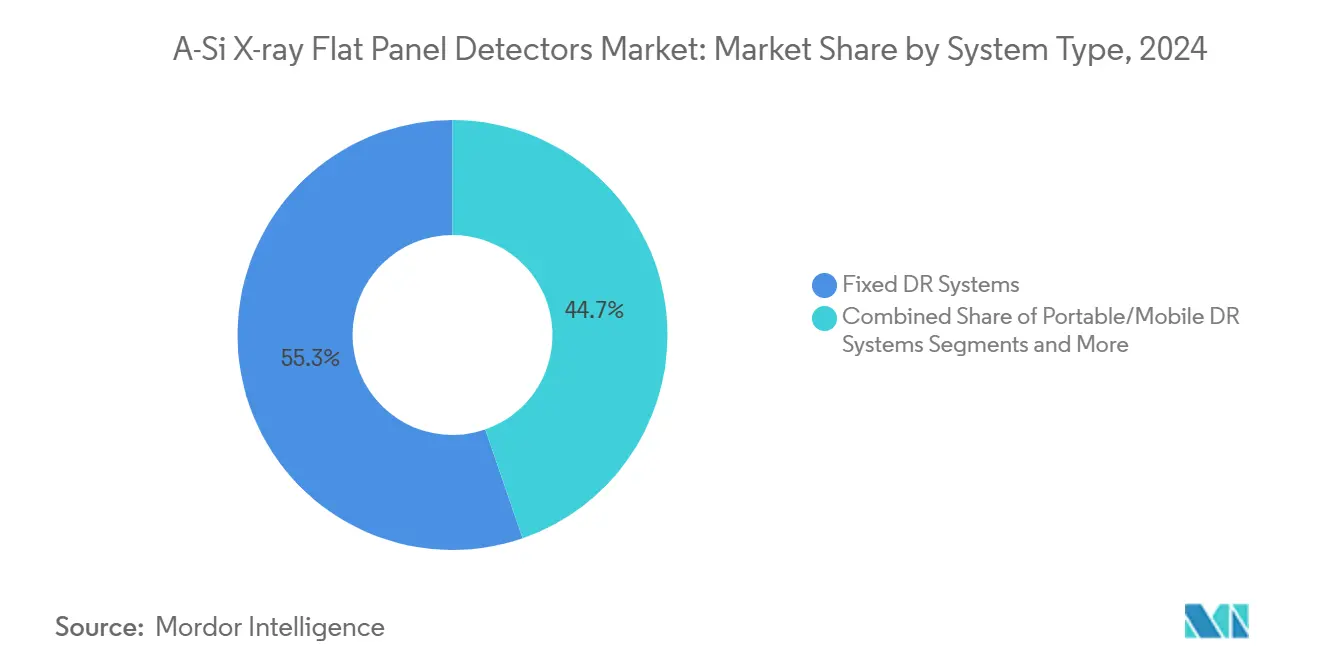

- By system type, fixed detectors held 55.3% of the a-Si X-ray Flat Panel Detectors market share in 2024; portable and mobile units are forecast to deliver an 11% CAGR through 2030, outpacing every other modality.

- By application, medical imaging represented 60.1% of the a-Si X-ray Flat Panel Detectors market size in 2024, while security and border-protection installations are advancing at a 12.5% CAGR to 2030.

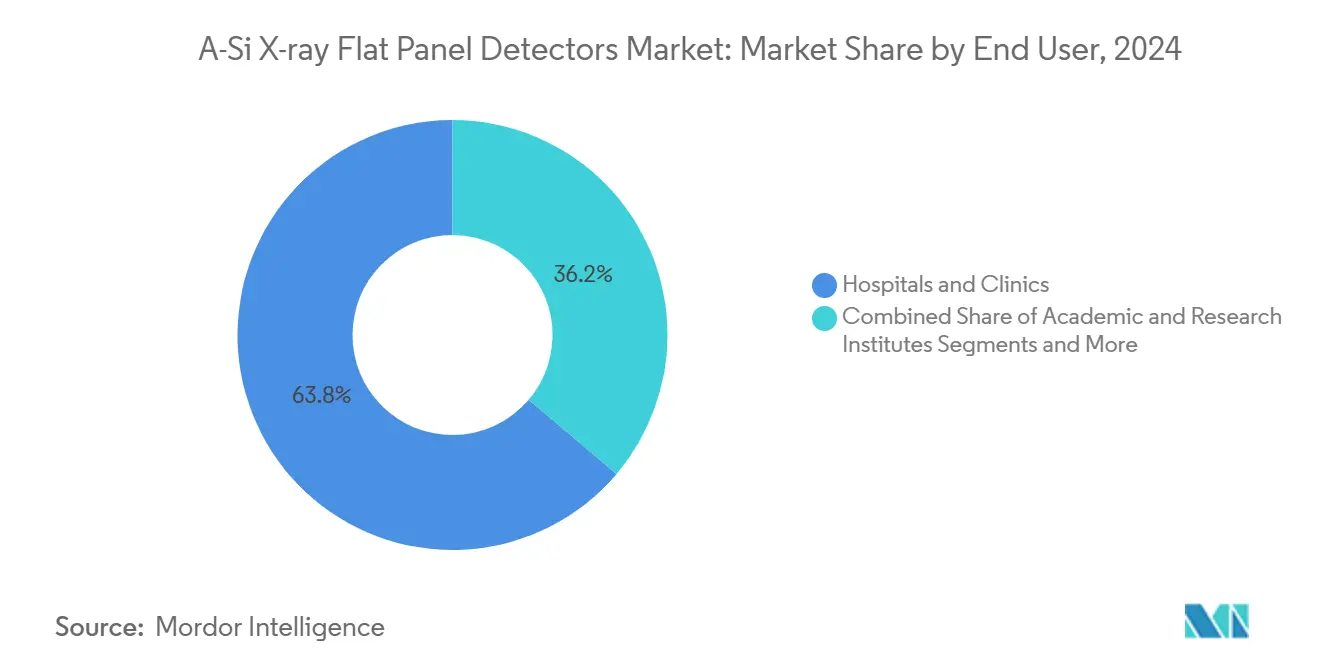

- By end user, hospitals and clinics commanded 63.8% revenue share in 2024; original equipment manufacturers (OEMs) record the fastest 10.5% CAGR as turnkey platform demand rises.

- By geography, North America retained 34.7% of 2024 revenues, whereas Asia Pacific is set to post a 6.8% CAGR through 2030, the highest regional rate.

Global A-Si X-ray Flat Panel Detectors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Shift From CR/CCD To Flat-Panel DR Systems | +1.80% | Global, with North America leading adoption | Medium term (2-4 years) |

| Accelerated Demand For Low-Dose Imaging In Pediatrics & Neonatal Care | +0.90% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Growth Of Mobile X-Ray Systems For POC & Field Triage | +1.20% | Global, with rural and emergency care focus | Short term (≤ 2 years) |

| Rapid Expansion Of Dental CBCT And Panoramic Imaging | +0.70% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Large-Area Detector Adoption In Industrial NDT & Security Screening | +0.50% | Global, with security applications in high-risk regions | Long term (≥ 4 years) |

| AI-Augmented Detector Calibration Boosting Image Quality & Workflow | +0.60% | North America & EU initially, global expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Shift From CR/CCD To Flat-Panel Detectors

Medicare’s reimbursement cuts for computed-radiography rooms trigger accelerated hospital replacement programs, with flat-panel detectors shortening study acquisition by 60-70% compared with cassette workflows.[1]Keith Loria, “A New Frontier,” Radiology Today, radiologytoday.net Wireless penetration grew from 53% in 2020 to an estimated 61% in 2025 as infection-control benefits, fewer retakes, and seamless PACS connectivity become decisive procurement criteria. ISO 4090 standards unify detector sizes, giving purchasing teams predictable lifecycle specifications. Emerging-market hospitals bypass CR entirely, adopting low-cost Chinese flat panels, a pattern that lifts annual global unit shipments even when capital budgets tighten elsewhere.

Accelerated Demand for Low-Dose Imaging in Pediatrics & Neonatal Care

Cesium-iodide scintillators incorporated into current a-Si backplanes cut entrance dose by 30–50% versus gadolinium equivalents while maintaining high detective-quantum efficiency, safeguarding radiation-sensitive populations.[2]Ysenmed, “How X-ray Flat Panel Detectors Are Revolutionizing Medical Imaging,” ysenmed.comChildren’s hospitals integrate age-based exposure presets, automating technique selection and widening technologist adoption. Updated U.S. and EU guidelines reinforce dose-limit awareness, prompting tender requirements that favor systems with embedded dose-monitoring dashboards. Vendors demonstrating peer-reviewed dose-saving outcomes now win a larger share of pediatric tenders, a trend expected to persist beyond the forecast window.

Growth Of Mobile X-Ray Systems for POC & Field Triage

Portable detectors weighing under 4 kg drive real-time bedside imaging in pandemic-era isolation wards and battlefront trauma units. The Amadeo M-DR mini offers 200 exposures on a single 8-hour battery, proving suitable for remote deployments without reliable mains power. Ultralight units integrate 5G encryption modules to enable instant cloud upload to radiologist worklists. As a result, governments allocate emergency-preparedness budgets for mobile fleets, elevating shipment growth of portable panels well above the overall a-Si X-ray Flat Panel Detectors market trend.

Rapid Expansion of Dental CBCT And Panoramic Imaging

Dental clinics adopt cone-beam CT because it provides 3-D anatomic detail at lower radiation than multi-detector CT. Detector makers leverage a-Si fabrication know-how to mass-produce compact CBCT sensors, enabling market entry for mid-sized practices. AI-assisted caries-detection software layers on top of the hardware stack, demonstrating improved diagnostic accuracy that underpins higher patient throughput and justifies investment. Market growth concentrates in North America and Western Europe but spills over to urban APAC dental chains in line with rising discretionary spending.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Volatility Of Amorphous Silicon & TFT Substrates | -1.1% | Global, with Asia manufacturing concentration | Short term (≤ 2 years) |

| Price Erosion Due To Rising Chinese ODM/IDM Competition | -0.8% | Global, with price-sensitive markets most affected | Medium term (2-4 years) |

| Slow Retrofit Cycles In Radiography Rooms > 10 Years Old | -0.4% | North America & EU legacy infrastructure | Long term (≥ 4 years) |

| Regulatory Delays For Veterinary & Security Detectors In EU | -0.3% | EU primarily, with spillover to aligned markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Volatility Of a-Si & TFT Substrates

Electric-vehicle demand consumes silicon-carbide wafer output, indirectly constraining detector backplane availability and stretching lead times beyond 16 weeks for high-resolution panels. Gallium- and indium-dependent IGZO fabrication faces raw-material price spikes exceeding 25% quarter-to-quarter, adding cost pressure on detector makers.[3]Yan Yan, “Reliability Issues of Amorphous Oxide TFTs,” Royal Society of Chemistry, rsc.org Vendors diversify sourcing through Japanese specialty foundries and evaluate glass-free architectures to reduce supply shock exposure.

Price Erosion Due To Rising Chinese ODM/IDM Competition

Chinese firms bundle generators and detectors at discounts reaching 40%, winning public-hospital tenders across Latin America, Africa, and Southeast Asia. Incumbent brands counter with extended warranty, AI add-ons, and cybersecurity guarantees, yet cost-driven customers often accept lower-priced alternatives. Sustained margin compression could deter smaller innovators from entering the a-Si X-ray Flat Panel Detectors industry and may spur consolidation among established Western suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Fixed Detectors Anchor Install Base While Mobile Units Surge

Fixed detector suites commanded 55.3% revenue in 2024 as high-volume imaging centers rely on ceiling-mount auto-positioning systems for rapid chest and skeletal studies. Retrofit kits extend life to older bays, cutting capital outlay by up to 50% and appealing to mid-sized hospitals. Portable panels are forecast for 11% CAGR driven by isolation-room protocols and emergency-response mandates. Canon’s Adora DRFi illustrates hybrid convergence, combining static radiography and fluoroscopy functionalities within a single footprint to optimize space and budget. Battery innovations enable 8-hour shift coverage, elevating workflow efficiency. Consequently, mobile detectors gain incremental share each year, though fixed rooms continue to underpin revenue stability for the a-Si X-ray Flat Panel Detectors market.

By Application: Healthcare Leads While Security Adoption Accelerates

Healthcare imaging generated 60.1% of 2024 shipments due to continual demand for chest, orthopedic, and perioperative exams. Industrial non-destructive testing uses large-area panels to inspect welded joints and aircraft components under stringent safety regulations. Security and border-protection installations grow fastest at 12.5% CAGR as customs agencies install dual-energy systems for cargo inspection and contraband detection. Veterinary practices deploy compact detectors for small-animal diagnostics, while dental CBCT uptake broadens flat-panel utility beyond 2-D X-ray imaging. Each end-market reinforces a diversified revenue base that reduces cyclicality for manufacturers.

By End User: Hospitals Dominate Yet OEM Expansion Signals Integration Trend

Hospitals and clinics retained 63.8% of shipments in 2024, driven by replacement urgency and infection-control standards. Independent imaging centers invest in single-detector U-arms to deliver cost-effective studies and meet insurer site-of-service directives. OEMs achieve a 10.5% CAGR as detector makers pursue vertical integration, illustrated by Varex Imaging’s USD 15 million stake in Micro-X that secures multi-beam tube exclusivity. Academic research labs and biomechanics units add incremental demand for high-frame-rate prototypes.

Geography Analysis

North America captured 34.7% of 2024 sales as Medicare penalties hastened analog-room retirement and integrated delivery networks refreshed radiology suites ahead of dose-monitoring deadlines. Cloud-based AI services gain early traction, aligning with domestic cybersecurity regulation.

Europe grows moderately. Germany and France stipulate mandatory Pediatric Dose Reference Levels, driving detector upgrades. Yet veterinary and security applications face CE-mark delays under evolving EU Medical Device Regulation, stalling some SKUs. Eastern Europe opts for retrofits due to constrained public budgets, cushioning but not eliminating demand.

Asia Pacific is the primary growth engine with a 6.8% CAGR through 2030. China’s “Healthy China 2030” campaign subsidizes rural imaging trucks equipped with wireless panels, while local ODMs capture domestic share through aggressive pricing. Japan confronts the “device-lag problem” that delays new-equipment approvals, yet an aging population keeps baseline procedure volume high. India’s Ayushman Bharat initiative issues tenders for economically configured detector rooms, and ASEAN island nations adopt backpack units to bridge geographic gaps. Middle East humanitarian programs and Latin American public–private partnerships further broaden geographic revenue distribution for the a-Si X-ray Flat Panel Detectors market.

Competitive Landscape

Five global suppliers account for an estimated 60–65% of detector revenue, yielding moderate concentration yet leaving room for regional entrants. Canon, FUJIFILM, and Varex Imaging rely on proprietary scintillator chemistry, ASIC design, and end-to-end manufacturing to maintain competitive advantage. Chinese brands such as Wandong leverage vertically integrated plants and state subsidies to undercut price, seizing share in cost-sensitive tenders.

Strategic alliances shape technology leadership. Varex’s collaboration with Micro-X secures Nano Electronic X-ray multi-beam tubes for lightweight CT, broadening its portfolio beyond flat panels. Siemens Healthineers’ Varian acquisition integrates oncology-imaging planning, while Agfa promotes glass-free detectors for durability in mobile trauma carts. Carestream Health expands Latin American presence through distribution pacts that bundle printers and detectors, illustrating service-based differentiation.

Competition centers on battery runtime, waterproof rating, and AI-workflow integration rather than pixel pitch alone. Vendors release cloud dashboards that monitor panel health, predict maintenance, and automate cybersecurity patches. Price competition will remain intense, but end-to-end service reliability and AI readiness now tilt tender outcomes, shaping long-term positioning within the a-Si X-ray Flat Panel Detectors market.

A-Si X-ray Flat Panel Detectors Industry Leaders

Varex Imaging Corporation

Thales Group

Canon Inc.

FUJIFILM Holdings Corporation

Konica Minolta Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Canon Medical Systems USA obtained FDA clearance for Adora DRFi, an automated hybrid platform pairing radiography and fluoroscopy with inMotion auto-positioning.

- December 2024: Varex Imaging introduced Lumen HD and Lumen HD Pro detectors tailored for high-performance DR suites.

- November 2024: Agfa unveiled glass-free Dura-line XF+ detectors with 99-micron pitch for ultra-high-resolution imaging.

Global A-Si X-ray Flat Panel Detectors Market Report Scope

| Fixed DR Systems |

| Portable/Mobile DR Systems |

| Retrofit DR Kits |

| Fluoroscopy/DDR Systems |

| R&D/Prototype Platforms |

| Medical Imaging |

| Dental Imaging |

| Veterinary Imaging |

| Non-Destructive Testing (NDT) |

| Security & Border Protection |

| Hospitals & Clinics |

| Diagnostic Imaging Centers |

| Original Equipment Manufacturers (OEMs) |

| Academic & Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By System Type | Fixed DR Systems | |

| Portable/Mobile DR Systems | ||

| Retrofit DR Kits | ||

| Fluoroscopy/DDR Systems | ||

| R&D/Prototype Platforms | ||

| By Application | Medical Imaging | |

| Dental Imaging | ||

| Veterinary Imaging | ||

| Non-Destructive Testing (NDT) | ||

| Security & Border Protection | ||

| By End User | Hospitals & Clinics | |

| Diagnostic Imaging Centers | ||

| Original Equipment Manufacturers (OEMs) | ||

| Academic & Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the a-Si X-ray Flat Panel Detectors market today?

It generated USD 1.74 billion in 2025 and is forecast to reach USD 2.37 billion by 2030.

Which region is expanding fastest for a-Si panels?

Asia Pacific is projected to log a 6.8% CAGR through 2030 due to healthcare digitization programs.

Why are mobile flat-panel detectors gaining traction?

Lightweight designs, all-day battery life, and pandemic-driven bedside imaging needs are accelerating hospital adoption.

How does AI enhance detector performance?

AI automates calibration, optimizes exposure, and flags fractures, cutting retake rates by up to 25% and speeding radiologist interpretation.

What is the primary supply-chain risk for detector manufacturers?

Volatile availability and pricing of amorphous-silicon and IGZO TFT substrates can prolong lead times and inflate costs.

Which end-user segment is growing quickest?

OEMs show the highest 10.5% CAGR as detector makers integrate full systems and AI software into turnkey offerings.

Page last updated on: