Market Overview

| Study Period | 2019 - 2030 |

|---|---|

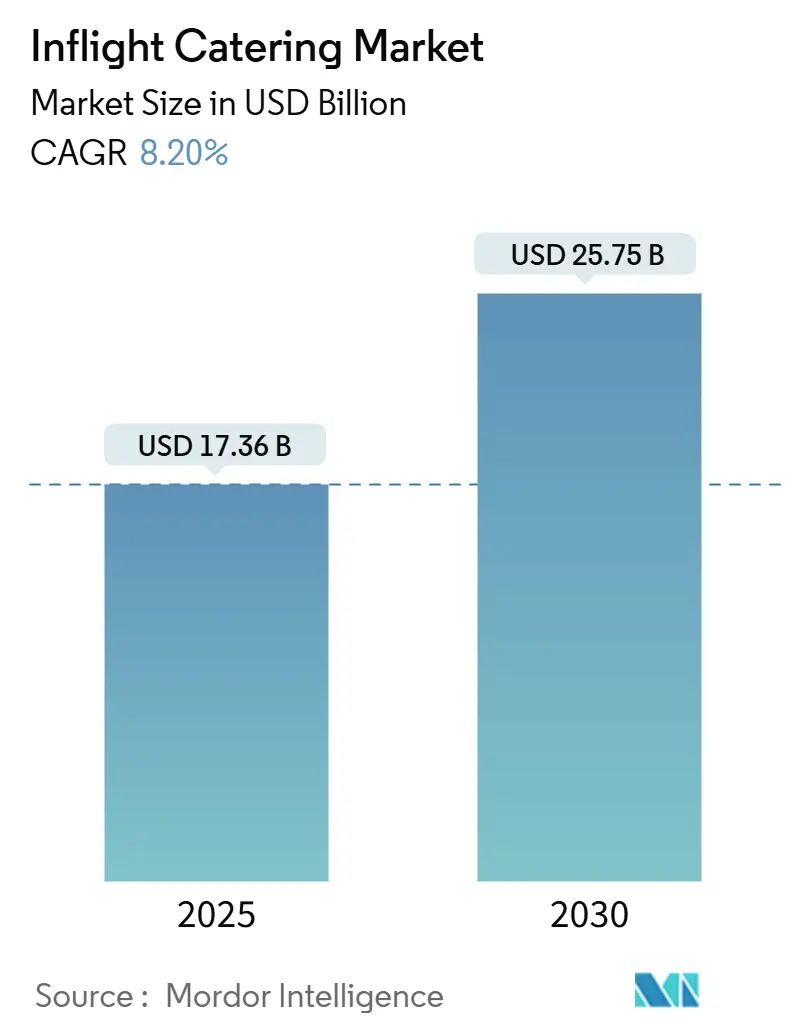

| Market Size (2025) | USD 17.36 Billion |

| Market Size (2030) | USD 25.75 Billion |

| Growth Rate (2025 - 2030) | 8.20% CAGR |

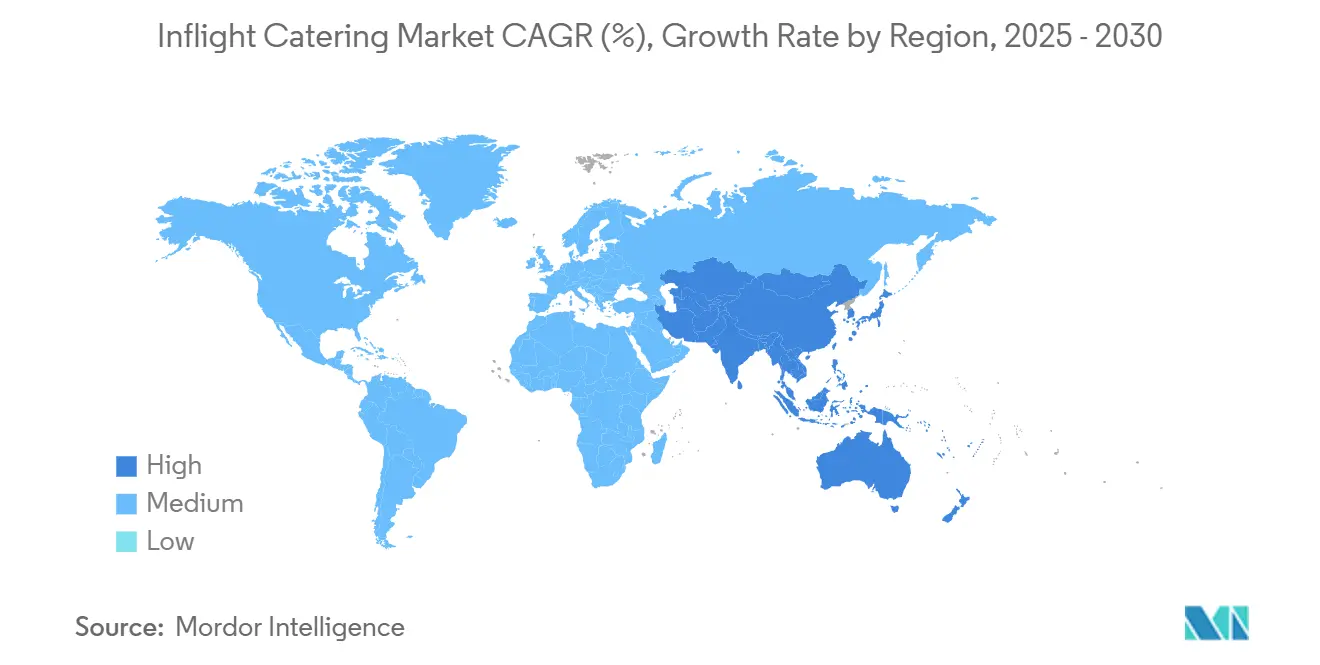

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Inflight Catering Market Analysis by Mordor Intelligence

The inflight catering market size stands at USD 17.36 billion in 2025 and is projected to reach USD 25.75 billion by 2030, advancing at an 8.20% CAGR over the period. Recorded passenger volumes, a premium-cabin refresh cycle, and digital pre-order platforms collectively increase per-passenger spend and sustain pricing power for caterers. Airlines are modernizing galleys, rolling out chef-curated menus, and embedding retail mechanics that monetize ancillary demand. Investments in AI-driven menu planning and cold-chain automation reduce waste, defend margins against food commodity inflation, and shorten the time to introduce new SKUs. Long-haul capacity additions maintain high average meal complexity, while low-cost carriers (LCCs) unlock new revenue through tiered, pay-as-you-go menus. Partnerships that align with halal, kosher, and allergen protocols protect incumbents and open avenues for specialized growth across multi-hub networks.

Key Report Takeaways

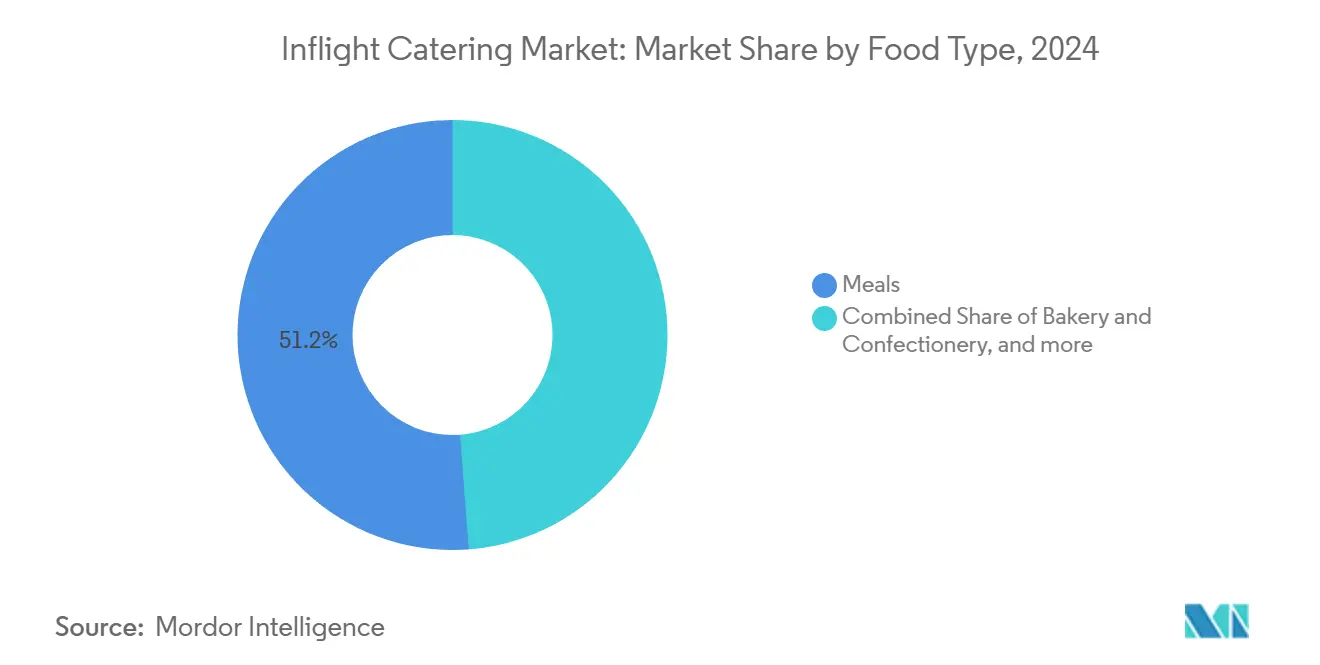

- By food type, meals led with 51.21% of the inflight catering market share in 2024; snacks and savouries are expanding at an 8.64% CAGR through 2030.

- By flight type, FSCs held 57.45% of the inflight catering market share in 2024, whereas LCCs are forecasted to post a 9.28% CAGR to 2030.

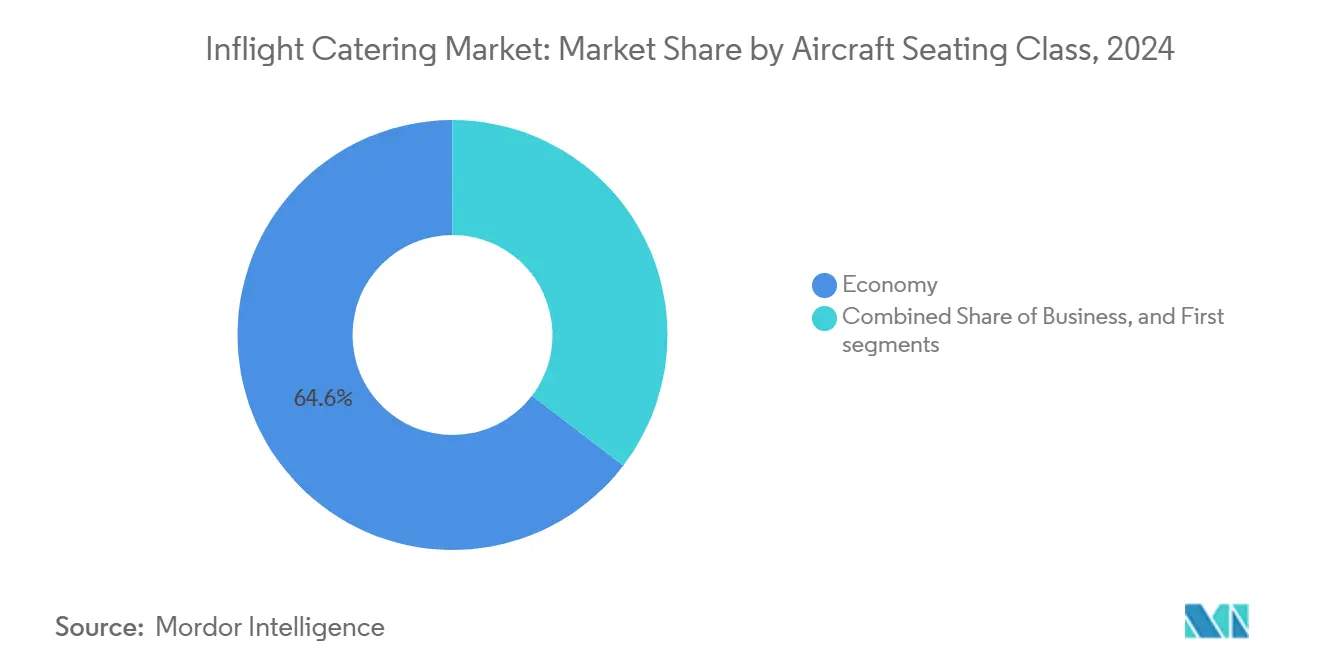

- By aircraft seating class, economy accounted for a 64.10% share of the inflight catering market size in 2024, and first class is projected to grow at a 9.35% CAGR through 2030.

- By catering type, the classic complimentary service commanded 68.50% of the revenue in 2024; retail on-board is advancing at a 9.14% CAGR through 2030.

- By flight duration, long-haul routes accounted for 59.50% of 2024 demand, while short-haul sectors are set to expand at a 9.07% CAGR through 2030.

- By geography, Asia-Pacific generated 32.45% of global revenue in 2024 and is on track for an 8.85% CAGR through 2030.

Global Inflight Catering Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rebound in air passenger traffic and long-haul capacity additions | +1.8% | Global APAC, Middle East strong | Medium term (2-4 years) |

| Premiumization of onboard experience to differentiate airline brands | +1.5% | Global North America, Europe, Middle East | Medium term (2-4 years) |

| Expansion of LCCs and hybrids, scaling buy-on-board and pre-order models | +1.2% | APAC core, spill-over to South America and MEA | Short term (≤ 2 years) |

| Digitalization: pre-order, data-driven menu planning, kitchen automation | +1.0% | Global, early adoption in Middle East and Europe | Long term (≥ 4 years) |

| Fresh-frozen meal networks enabling global SKU standardization | +0.8% | Global, especially multi-hub carriers in North America and Europe | Medium term (2-4 years) |

| Aircraft and engine delivery bottlenecks favor reliable, waste-aware catering | +0.6% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rebound in Air Passenger Traffic and Long-Haul Capacity Additions

Global passenger totals reached 4.7 billion in 2024 and are projected to touch 4.96 billion in 2025, surpassing pre-pandemic peaks as wide-body fleets rejoin service.[1]Source: International Air Transport Association, “Global Passenger Traffic to Reach 4.96 Billion in 2025,” IATA, iata.org Load factors rose to 83.5%, reducing buffer seats and forcing caterers to uplift closer to booked capacity. Although supply-chain delays curb deliveries, airlines continue to add premium-heavy A350 and B787 aircraft, thereby increasing the value of per-flight catering. Transpacific capacity increased 12% year-over-year in 2024, driven by the resumption of Chinese routes and United's securing of new Tokyo-Haneda slots. Because a 12-hour sector typically loads triple the per-flight spend of a 2-hour hop, caterers prioritize wide-body hubs and invest in multi-leg inventory systems that synchronize outbound and return menus.

Premiumization of Onboard Experience to Differentiate Airline Brands

Airlines invested over USD 2 billion in premium-cabin retrofits during 2024 to serve corporate travelers and high-yield leisure traffic.[2]Source: Delta Air Lines, “Investor Update Q3 2024,” Delta, delta.com Delta introduced chef partnerships, Qatar Airways rolled out à la carte dining in Qsuite, and Emirates refreshed Michelin-inspired menus, shifting catering from a cost center to a brand asset. British Airways enhanced its Club World service in 2024 with regional dishes and digital pre-order, boosting satisfaction by eight points within six months. First-class catering now requires small-batch production, dedicated cold-chain logistics, and higher crew engagement. Caterers respond with investment in culinary training, rapid-response quality checks, and premium-ingredient procurement networks that economy-focused rivals cannot match.

Expansion of LCCs and Hybrids, Scaling Buy-On-Board and Pre-Order Models

Expansion of LCCs and hybrids, along with the scaling of buy-on-board and pre-order models, is driving significant growth in ancillary services. Ryanair reported a year-on-year increase in onboard sales, driven by push notifications enabling passengers to place orders before departure. Southwest Airlines tested paid meal boxes on US coast-to-coast routes in late 2024. IndiGo partnered with Taj SATS to reduce waste and to increase ticket-linked catering spend through mobile pre-order options. This growth in retail offerings is expanding the inflight catering market rather than replacing complimentary services. However, it necessitates advancements in payment processing, SKU rationalization, and e-commerce reconciliation, which traditional catering providers are striving to implement.

Digitalization: Pre-Order, Data-Driven Menu Planning, Kitchen Automation

Emirates deployed AI menu planning in 2024 that matches dishes to passenger profiles, cutting refusals by 18% on trial routes. Finnair’s long-haul pre-order platform captures 35% of business-class customers and trims waste on premium ingredients. Cathay Pacific links exclusive dishes to loyalty tiers, creating digital stickiness that rivals cannot mirror. On the production floor, dnata’s semi-automated Dubai kitchen utilizes robotic tray assembly and IoT-enabled cold storage to reduce spoilage by 22%. Digital adoption divides the field into capital-intensive global players and regional specialists that must partner or risk becoming obsolete.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High operating costs and inflation across food, labor, utilities | −1.2% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Stringent multi-jurisdiction food safety plus halal and kosher compliance | −0.7% | Global - Middle East, South Asia, Europe | Long term (≥ 4 years) |

| Short-haul time constraints and bring-your-own-food behavior | −0.5% | North America, Europe, domestic APAC | Medium term (2-4 years) |

| Contract and retail mix shifts lowering meal uplift per flight | −0.4% | Global, concentrated in LCC-heavy markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Operating Costs and Inflation Across Food, Labor, and Utilities

Wheat, dairy, and poultry prices increased by 8-12% in 2024 due to climatic disruptions in key producing regions, such as Australia and Argentina.[3]Source: Food and Agriculture Organization, “Food Price Index 2024,” FAO, fao.org Labor costs for caterers rose by 6-9% across North America and Europe as employers in the hospitality industry faced intensified competition to attract and retain skilled talent. In Europe, utility costs surged by 10-15% following the termination of energy subsidies, adding further pressure on operational expenses. Additionally, dnata staff at major airports, such as Heathrow and Manchester, staged walkouts in November 2024, highlighting vulnerabilities in their cost structures. To mitigate these challenges, operators have turned to automation, implementing tray lines and adopting energy-efficient chillers to recover profit margins. However, smaller players, constrained by limited capital, are increasingly compelled to either merge with larger entities or exit the market entirely.

Stringent Multi-Jurisdiction Food Safety and Halal/Kosher Compliance

Caterers are required to comply with various standards and regulations, including HACCP, ISO 22000, and the US FSMA traceability mandate. These regulations ensure food safety and traceability throughout the supply chain. Halal certification imposes specific requirements, such as the use of segregated utensils and regular audits, which can increase per-meal costs by up to 12%. Similarly, kosher production involves strict guidelines, including rabbinic supervision and the use of sealed packaging to maintain compliance with religious dietary laws. To meet these stringent standards, Emirates Flight Catering operates six dedicated production zones, each tailored to specific requirements. However, the fragmentation of regulatory frameworks across different regions and standards slows down menu innovation. It creates higher entry barriers for new players, thereby reinforcing the competitive advantage of established companies in the market.

Segment Analysis

By Food Type: Snacks Gain as Meal Complexity Plateaus

Meals continue to dominate the inflight catering market, accounting for 51.21% of the revenue in 2024, making it the largest segment. However, snacks and savouries are witnessing significant growth, expanding at a CAGR of 8.64%. This growth reflects changing consumer preferences, with airlines adapting their offerings to meet evolving demands. For instance, Qatar Airways has introduced mezze platters priced between USD 15 and USD 25 for pre-order, catering to travelers seeking lighter meal options. Similarly, Turkish Airlines has increased its onboard sales by 22% by incorporating regional snacks, such as simit and baklava, into its menu. Beverages are also transforming, with the inclusion of craft brews and mocktails that provide higher profit margins without increasing galley workload. These developments highlight the in-flight catering market's efforts to diversify product offerings while addressing operational constraints.

Modularization is emerging as a key trend in the inflight catering market, enabling greater flexibility and efficiency. Caterers are now designing component-level menus that airlines can mix and match based on specific route requirements. This approach not only aligns with retail platforms but also helps in minimizing waste. Airlines that previously faced a binary choice between offering meals or snacks are now deploying mixed stock-keeping units (SKUs), allowing for a more tailored approach to passenger preferences. This flexibility provides caterers with new opportunities to negotiate based on waste reduction and the generation of ancillary revenue. By adopting modularization, airlines can optimize their catering operations, reduce costs, and enhance the overall passenger experience, all while maintaining operational efficiency and sustainability.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Flight Type: LCCs Monetize Ancillaries While FSCs Defend Premium

Full-service carriers (FSCs) accounted for 57.45% of the market share in 2024, making them the largest segment in the inflight catering market. This dominance is attributed to their extensive network coverage and the demand for multi-cabin services, which cater to a wide range of passenger preferences. FSCs offer a variety of meal options and premium services, including chef-curated menus and sommelier-selected wine pairings, which enhance the overall passenger experience. These offerings are particularly appealing to business and first-class travelers, who prioritize quality and customization. The ability of FSCs to provide such high-touch services has solidified their position as the leading segment in the market.

Meanwhile, low-cost carriers (LCCs) are experiencing the fastest growth in the market, with a CAGR of 9.28%. This growth is driven by their ability to innovate and adapt to the preferences of cost-sensitive passengers. For instance, Ryanair generated EUR 400 million in food sales during fiscal 2024, showcasing the potential of retail offerings to rival traditional catering revenues. Similarly, IndiGo doubled its transaction value through app-based meal boxes, demonstrating that passengers are willing to pay for convenience despite being price-conscious. LCCs focus on efficiency and volume-driven strategies, such as SKU rationalization, to meet the demands of their growing customer base. This dual-track evolution, with FSCs focusing on premium services and LCCs on cost-effective solutions, is expanding the overall inflight catering market rather than redistributing market share.

By Aircraft Seating Class: First-Class Complexity Drives Fastest Growth

The economy class continues to dominate the inflight catering market, contributing 64.10% of the total seating-class revenue in 2024, highlighting the consistent demand for affordable travel options, which remains a key driver for the market. Airlines catering to this segment focus on providing cost-effective yet satisfactory meal options to meet the expectations of a large customer base. On the other hand, first class is witnessing the fastest growth, with a CAGR of 9.35%. Premium services offered by airlines such as Emirates, including caviar and Dom Pérignon, necessitate specialized ultra-cold supply chains and chef-prepared meal loading. Similarly, Singapore Airlines has enhanced its premium offerings through its "Book the Cook" platform, which provides passengers with over 50 meal options, resulting in significantly improved customer satisfaction. These high standards compel caterers to adopt small-batch production lines with stringent quality control measures. Providers capable of addressing both the low-volume luxury segment and the high-volume economy class are better positioned to capture a larger share of the inflight catering market.

The increasing complexity of first-class services is driving significant investments in advanced technologies and processes. These include micro-portion blast chilling, premium ingredient procurement, and sophisticated plating stations, all designed to meet the high expectations of first-class passengers. Companies that lack the financial resources to invest in these advanced capabilities are increasingly focusing on business-class contracts, which offer a more manageable level of service complexity. This shift is leading to a consolidation of the premium market share among established players such as SATS, Emirates Flight Catering, and DO & CO. These companies are leveraging their capital and expertise to dominate the premium inflight catering segment, further strengthening their position in the market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Catering Type: Retail On-Board Scales Through Digital Pre-Order

Traditional complimentary services remain the largest segment in the inflight catering market, contributing 68.50% of the total revenue. These services continue to dominate due to their widespread inclusion in ticket pricing and their appeal to a broad range of passengers. However, onboard retail is emerging as a significant growth area, recording a CAGR of 9.14%. This growth is primarily driven by the increasing adoption of mobile applications, which simplify the process of placing orders during flights. Airlines are capitalizing on this trend to diversify their offerings and improve passenger convenience. For instance, United Airlines expanded its product portfolio by introducing 25 new SKUs, resulting in an 18% increase in sales. Similarly, Cathay Pacific has strengthened customer engagement by tying exclusive items to its loyalty tiers, encouraging repeat purchases and fostering brand loyalty.

Onboard retail does not replace traditional complimentary services but complements them by targeting passengers who previously declined meal options. This approach allows airlines to generate additional revenue without undermining the core complimentary service model. The inflight catering market benefits from this strategy by achieving incremental revenue growth without a proportional increase in meal volumes. This dynamic underscores the importance of precise provisioning to minimize waste and optimize inventory. Additionally, the integration of advanced e-commerce analytics has become crucial for understanding passenger preferences and improving the efficiency of onboard retail operations. By combining traditional services with innovative retail strategies, airlines are successfully addressing diverse passenger needs while maximizing revenue potential.

By Flight Duration: Short-Haul Gains as Regional Networks Densify

Long-haul sectors represented the largest share of demand, holding 59.50% in 2024. These sectors continue to dominate due to their extensive flight durations and the associated need for inflight services. On the other hand, short-haul segments are experiencing significant growth, advancing at a CAGR of 9.07%. This growth is primarily driven by the dense networks in the Asia-Pacific and Middle East regions, which facilitate increased connectivity and passenger volumes. Flydubai has successfully increased the average transaction value to USD 15 on flights exceeding three hours by introducing pre-order meal boxes. Similarly, Air India Express achieved a 35% penetration rate with its tiered snack menu, priced between USD 3 and USD 12, catering to diverse passenger preferences.

The compressed service window on short-haul flights necessitates the use of standardized and quickly loaded SKUs, ensuring operational efficiency. This model is particularly attractive to LCCs aiming to streamline their services. At the same time, premium leisure routes continue to support demand for higher-end retail offerings, catering to passengers seeking enhanced inflight experiences. As network density increases, catering companies are strategically positioning centralized kitchens near major hubs. This approach allows them to balance economies of scale with just-in-time delivery, ensuring fresh and timely service to meet the growing demand.

Geography Analysis

The Asia-Pacific region emerged as the largest segment, contributing 32.45% of the global revenue in 2024. China's domestic market recovery drives the region's dominance, India's extensive airport expansion projects, and the rapid growth of LCCs in Southeast Asia. These factors collectively underpin the significant growth in volume in the region. SATS has invested USD 45 million in a Bengaluru kitchen, increasing its daily capacity to 40,000 kg to cater to India's projected 300 million annual passengers. Vietnam Airlines Caterers has also secured the Long Thanh facility tender, with plans to produce 30,000 meals daily by 2026. The region is expected to grow at a CAGR of 8.85% through 2030. Meanwhile, mature markets like Japan and South Korea are consolidating as larger players absorb smaller competitors unable to meet ISO upgrade requirements.

The Middle East and Africa, while smaller in absolute scale, enjoy higher margins compared to other regions. Emirates Flight Catering reported AED 970 million (USD 264.13 million) in external revenue for fiscal 2023-24, reflecting an 11% year-on-year increase. Qatar Aircraft Catering expanded its operations in Doha by adding 15,000 meals daily in 2024. dnata has entered into a joint venture with Saudia, aiming to achieve a daily production capacity of 50,000 meals by 2026. Despite these advancements, infrastructure gaps persist in certain parts of Africa. However, hub carriers in Ethiopia and Kenya are sustaining nascent growth in the region. The Middle East and Africa markets are poised for steady development, supported by these strategic initiatives and partnerships.

North America and Europe represent steady but slower-growing markets. Lufthansa's sale of LSG to Aurelius in 2023 triggered asset rationalization, leaving gategroup, dnata, and Flying Food Group with approximately half of the regional revenue. Delta Airlines renewed a decade-long contract with gategroup across 50 US stations, focusing on sustainability goals such as compostable packaging and waste diversion. These regions are increasingly prioritizing technology, reliability, and sustainability in bid evaluations, which has created significant entry barriers for low-cost challengers. While growth in these markets remains moderate, the emphasis on innovation and environmental responsibility is shaping the competitive landscape and driving operational improvements.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The inflight catering market is moderately consolidated. These established players dominate the market due to their extensive cold-chain infrastructure, global food safety certifications, and exclusive access rights at major airports. Their stronghold is further reinforced by significant investments in advanced technologies, including robotic tray assembly, AI-driven meal planning, and blockchain-based traceability systems. These innovations have enabled them to achieve a reduction of up to 20% in labor costs, thereby enhancing operational efficiency and profitability. Emirates Flight Catering, for example, allocated AED 60 million (USD 16.34 million) in 2024 to upgrade its fleet, ensuring reliability within a critical 45-minute loading window. Such strategic initiatives underline the competitive edge of these incumbents in maintaining their market leadership.

Regional specialists, on the other hand, thrive by catering to specific culinary preferences, such as halal or kosher meal preparation, and by leveraging local sourcing to meet the unique demands of niche markets. This approach allows them to differentiate themselves in a competitive market. For instance, Singapore Airlines reported a 28% increase in requests for vegan meals, reflecting a growing demand for plant-based options. This underserved segment has attracted attention from players like Cathay Pacific Catering and Green Common, who are actively targeting this market. Additionally, opportunities exist in emerging areas such as plant-based proteins and zero-waste packaging, where agile new entrants can carve out a competitive position. These trends highlight the evolving consumer preferences and the potential for innovation in the inflight catering industry.

Regulatory complexities create significant barriers to entry, favoring established players while deterring price-driven new entrants. Airlines are increasingly preferring caterers that comply with stringent standards, such as ISO 22000, HACCP, and multi-cuisine requirements, to ensure food safety and quality. Furthermore, delays in aircraft deliveries exacerbate switching costs, as airlines prioritize proven partners to maintain punctuality and avoid meal-related compensation claims. This dynamic underscores the importance of reliability and operational excellence in securing long-term contracts. Competitive advantage in the market now hinges on a combination of operational efficiency, digital integration, and measurable sustainability metrics. These factors not only enhance the value proposition for airlines but also serve as key differentiators that airlines can showcase to investors, reflecting their commitment to environmental and social governance goals.

Inflight Catering Industry Leaders

-

gategroup

-

LSG Group

-

Newrest Group Services SAS

-

Emirates Group

-

SATS Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: SATS Ltd. announced that its subsidiary, TFK Corporation, secured a three-year inflight catering contract with Turkish Airlines, marking a strategic advancement in SATS Food Solutions' operations in Japan. This development underscores SATS' ability to meet the growing demand for halal-certified inflight meals, leveraging its certified facilities to support Turkish Airlines' extensive global network. By strengthening its partnership with a prominent European carrier, SATS positions itself to enhance its market presence in Asia, aligning with the increasing preference for halal food solutions that reflect broader trends in the aviation and food services industries.

- June 2025: dnata secured a multi-year contract with Aer Lingus to provide inflight catering services for four weekly flights between Nashville International Airport and Dublin Airport. This agreement positions dnata to deliver approximately 40,000 meals annually, reinforcing its footprint in the North American market. The partnership highlights the growing demand for reliable catering solutions in transatlantic routes and underscores dnata's strategic focus on expanding its service portfolio. For Aer Lingus, this collaboration ensures consistent service quality, supporting its operational efficiency and enhancing passenger experience on a key international route.

- January 2025: CATRION Catering Holding Company announced a five-year contract with Riyadh Air, valued at SAR 2.3 billion (USD 613.20 million), to provide catering and support services for domestic and international flights. This agreement is expected to enhance CATRION's financial performance from Q4 2025, driven by Riyadh Air's fleet expansion and passenger growth. Strategically, this positions CATRION to diversify revenue streams and strengthen its role in the aviation supply chain. The partnership aligns with Saudi Vision 2030, supporting Riyadh's development as a global aviation hub and reinforcing the Kingdom's efforts to transform its aviation industry into a key driver of economic growth.

Global Inflight Catering Market Report Scope

Inflight food is the food served to passengers onboard a commercial airliner. Specialist airline catering services prepare these meals and usually serve them to passengers using an airline service trolley.

The inflight catering market is segmented by food type, flight type, aircraft seating class, catering type, flight duration, and geography. By food type, the market is segmented into meals, bakery and confectionery, snacks and savouries, and beverages. By flight type, the market is segmented into full-service carriers (FSCs), low-cost carriers (LCCs), and other types of flights. By seating class, the market is segmented into economy, business, and first class. By catering type, the market is segmented into retail onboard and classic catering. By flight duration, the market is segmented into long-haul and short-haul.

The report also covers the market sizes and forecasts for the inflight catering market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

By Food Type

| Meals |

| Bakery and Confectionery |

| Snacks and Savouries |

| Beverages |

By Flight Type

| Full‑Service Carriers (FSC) |

| Low‑Cost Carriers (LCC) |

| Other Flight Types |

By Aircraft Seating Class

| Economy |

| Business |

| First |

By Catering Type

| Classic (Complimentary and Pre‑ordered) |

| Retail On Board (Buy‑on‑board) |

By Flight Duration

| Short‑Haul |

| Long‑Haul |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Food Type | Meals | ||

| Bakery and Confectionery | |||

| Snacks and Savouries | |||

| Beverages | |||

| By Flight Type | Full‑Service Carriers (FSC) | ||

| Low‑Cost Carriers (LCC) | |||

| Other Flight Types | |||

| By Aircraft Seating Class | Economy | ||

| Business | |||

| First | |||

| By Catering Type | Classic (Complimentary and Pre‑ordered) | ||

| Retail On Board (Buy‑on‑board) | |||

| By Flight Duration | Short‑Haul | ||

| Long‑Haul | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the inflight catering market?

The inflight catering market size is USD 17.36 billion in 2025 and is projected to grow to USD 25.75 billion by 2030.

How fast is inflight catering demand growing?

The market is forecasted to post an 8.20% CAGR between 2025 and 2030, driven by returning passenger traffic and premiumization trends.

Which region leads inflight catering revenue?

Asia-Pacific leads with 32.45% of global revenue in 2024 and is expanding at an 8.85% CAGR to 2030.

Which airline segment shows the fastest catering revenue growth?

First class catering records the quickest growth, advancing at a 9.35% CAGR through 2030 due to ultra-premium service expectations.

How are low-cost carriers impacting catering dynamics?

LCCs boost ancillary revenue with pre-order and buy-on-board programs, growing at a 9.28% CAGR and reshaping provisioning toward exact-demand models.

What technologies are caterers adopting to reduce waste?

Operators deploy AI menu planning, robotic tray assembly, IoT cold storage, and fresh-frozen meal networks to cut waste and enhance reliability.

Page last updated on: