Oxygen Free Copper Market Size

| Study Period | 2019-2029 |

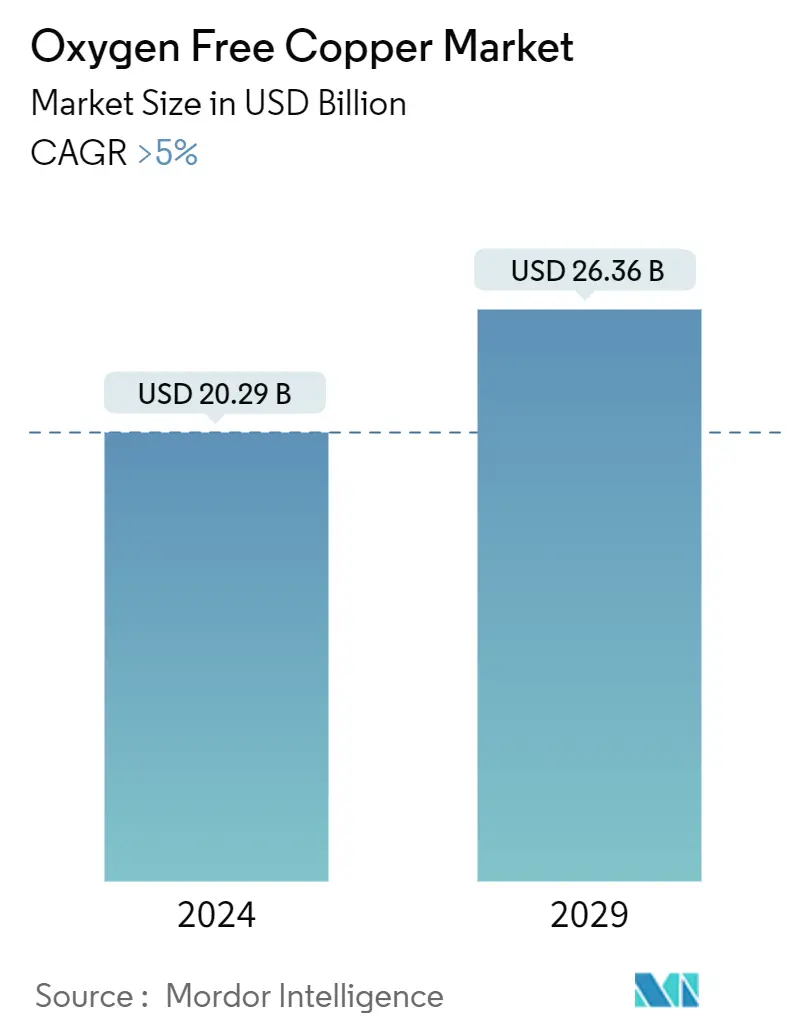

| Market Size (2024) | USD 20.29 Billion |

| Market Size (2029) | USD 26.36 Billion |

| CAGR (2024 - 2029) | > 5.00 % |

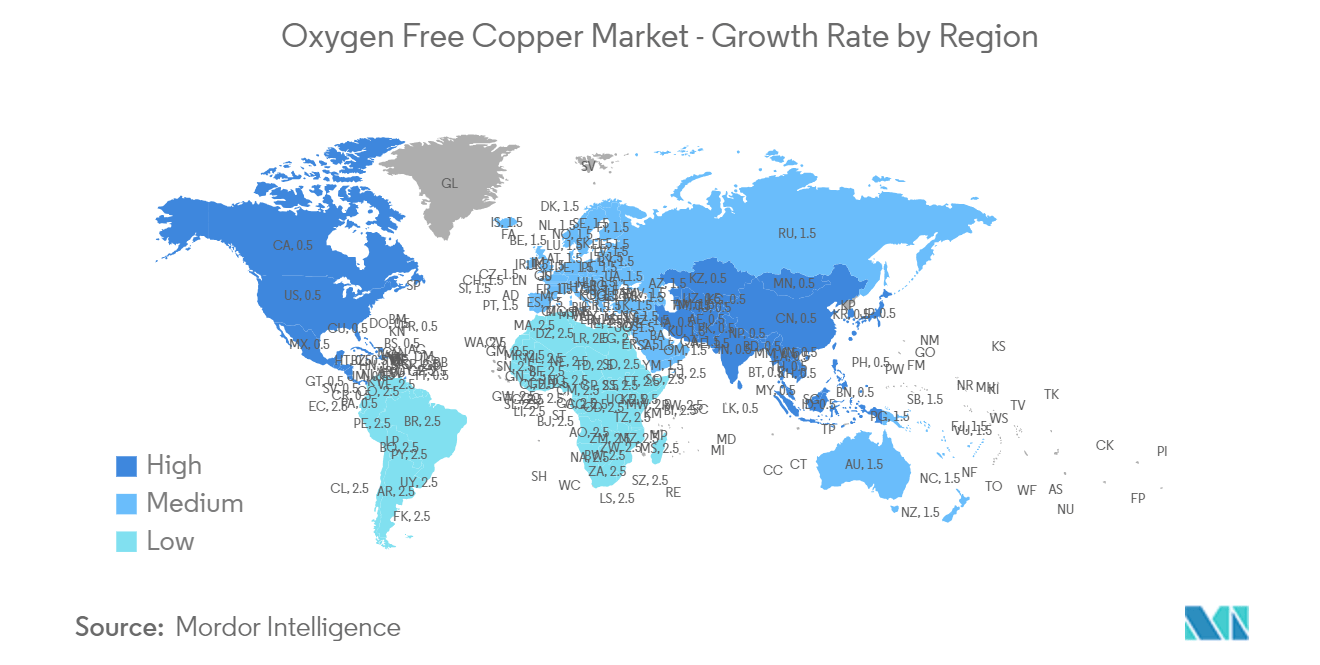

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Oxygen Free Copper Market Analysis

The Oxygen Free Copper Market size is estimated at USD 20.29 billion in 2024, and is expected to reach USD 26.36 billion by 2029, growing at a CAGR of greater than 5% during the forecast period (2024-2029).

The market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility, which caused a shortage of semiconductors, which negatively impacted the market for oxygen-free copper. Also, industries such as electronics, automotive, etc., were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022, and it is expected to grow steadily in the future.

Increasing demand for oxygen-free copper from semiconductors has been driving the market growth during the forecast period.

However, the high cost of copper is anticipated to hinder the growth of the studied market.

Growing oxygen-free copper applications in a wide range of electronics are likely to provide opportunities for the oxygen-free copper market over the next five years.

The Asia-Pacific region is dominated across the world, with increasing consumption from countries like China and India.

Oxygen Free Copper Market Trends

Electrical and Electronics Industry to Dominate the Market

- The electrical and electronics industry stands to be the dominating segment owing to wide consumption in the manufacturing of semiconductors and superconductors.

- Oxygen-free copper is commonly used in manufacturing applications such as the manufacture of semiconductors and superconductors and high-vacuum systems such as particle accelerators requiring plasma deposition.

- The use of oxygen-free materials is critical in these applications, as the presence of oxygen or some other impurity contributes to unwanted chemical reactions with the materials used in the system.

- Oxygen-free copper is witnessing growth in consumption due to its wide application in printed circuit boards, microwave tubes, vacuum capacitors, vacuum interrupters, vacuum seals, waveguides, and vacuum tubes for radio and TV transmitters and magnetrons.

- The exponential growth in the number of electronic gadgets across the globe, such as mobile phones, smart devices, tablets, and TV sets, is expected to drive the demand for oxygen-free copper over the forecast period. Thus, the increasing usage and widening arena of application in the electrical and electronics industry is expected to drive market growth.

- According to the Japan Electronics and Information Technology Industries Association (JEITA), the production by the global electronics and IT industry was estimated at USD 3,436.8 billion in 2022, registering a growth rate of 1% year-on-year, compared to USD 3,415.9 billion in 2021. Moreover, the industry is expected to reach USD 3,526.6 billion, with a growth rate of 3% year-on-year in 2023.

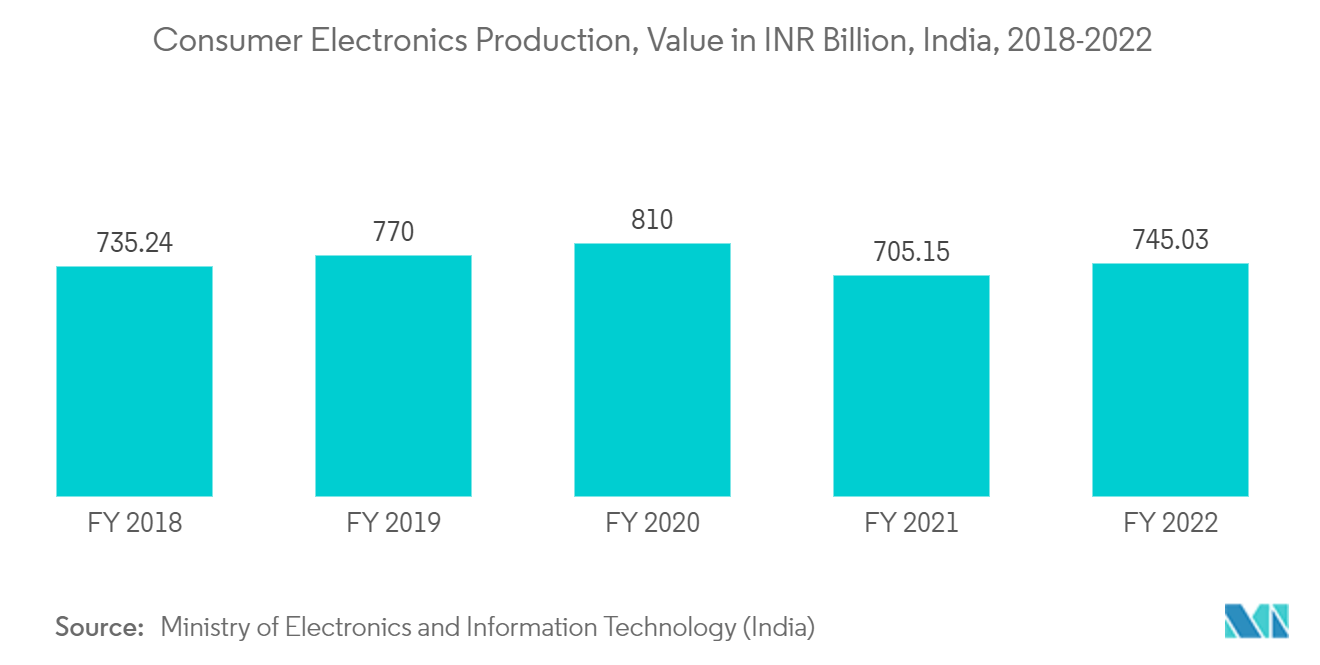

- Moreover, according to the Ministry of Electronics and Information Technology, the production value of consumer electronics (TV, accessories, and audio) across India was above INR 745 billion (USD 9.46 billion) in fiscal year 2022, thus supporting the growth of the market.

- All the aforementioned factors are expected to drive the oxygen-free copper market during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific market is expected to be the largest and fastest-growing market over the forecast period, owing to the increasing demand for electronic semiconductor devices in developing countries of Asia-Pacific, such as China, Japan, and India.

- Demand for consumer devices, such as smartphones, PCs, laptops, and other medical electronics products, is growing rapidly through the Asia-Pacific region, with India, Japan, and China contributing majorly to the market growth.

- According to the Ministry of Industry and Information Technology (MIIT), China is the world’s largest producer of consumer electronics, with a global share of more than 60%.

- Furthermore, Japan is one of the largest producers of electronics; as per the Japan Electronics and Information Technology Industries Association (JEITA), the domestic production by the Japanese electronics industry was estimated at JPY 11,124.3 billion (~USD 85.19 billion) in 2022, witnessing a growth rate of 2% compared to the previous year. The domestic production by the Japanese electronics industry is likely to reach JPY 11,402.9 billion (~USD 87.32 billion) by 2023, registering a growth rate of 3% year-on-year.

- The Asia-Pacific energy sector is also thriving, owing to the high demand for energy. The rapidly growing industrial sector is one of the key factors driving the energy demand in the region, which in turn is supporting the market growth during the forecast period.

- The Asia-Pacific thermal sector is registering growth, with China primarily driving the growth of the sector. China has the most coal-fired power plants of any country or territory in the world. On the Chinese Mainland, as of July 2022, there were 1,118 operational coal power plants. This is approximately four times the number of such power plants in India, which came in second place. China accounts for more than half of the world's coal electricity generation.

- The aforementioned factors are anticipated to contribute to the increasing demand for oxygen-free copper consumption in the region during the forecast period.

Oxygen Free Copper Industry Overview

The oxygen-free copper market is fragmented in nature. The major players in the studied market (not in any particular order) include Copper Braid Products, Mitsubishi Materials Corporation, Aviva Metals, PROTERIAL Ltd, and Sam Dong.

Oxygen Free Copper Market Leaders

Copper Braid Products

Aviva Metals

Mitsubishi Materials Corporation

PROTERIAL, Ltd.

Sam Dong

*Disclaimer: Major Players sorted in no particular order

Oxygen Free Copper Market News

- Jan 2023: Effective January 04, 2023, Hitachi Metals Ltd changed its name to Proterial Ltd.

- Jan 2023: Superior Essex Inc., a manufacturer of wire and cable products, signed an agreement to purchase Lacroix + Kress GmbH, an oxygen-free copper (OFC) drawing manufacturer in Europe, from Mutares SE & Co. KGaA. As OFC is a key component in electric vehicles (EVs), this acquisition aims to enhance the Superior Essex business in the EV market.

Oxygen Free Copper Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Demand from Semiconductor

4.1.2 Increasing Demand from Automotive Sector

4.1.3 Other Drivers

4.2 Restraints

4.2.1 High Cost of Copper

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Value)

5.1 Grade

5.1.1 CU-OF

5.1.2 CU-OFE

5.2 Product

5.2.1 Wires

5.2.2 Strips

5.2.3 Busbars and Rods

5.2.4 Other Products (Tubes and Pipes, Etc.)

5.3 End-user Industry

5.3.1 Electrical and Electronics

5.3.2 Automotive

5.3.3 Industrial

5.3.4 Other End-user Industries (Power Generation, Aerospace, Etc.)

5.4 Geography

5.4.1 Asia-Pacific

5.4.1.1 China

5.4.1.2 India

5.4.1.3 Japan

5.4.1.4 South Korea

5.4.1.5 Malaysia

5.4.1.6 Thailand

5.4.1.7 Indonesia

5.4.1.8 Vietnam

5.4.1.9 Rest of Asia-Pacific

5.4.2 North America

5.4.2.1 United States

5.4.2.2 Canada

5.4.2.3 Mexico

5.4.3 Europe

5.4.3.1 Germany

5.4.3.2 United Kingdom

5.4.3.3 France

5.4.3.4 Italy

5.4.3.5 Spain

5.4.3.6 NORDIC Countries

5.4.3.7 Turkey

5.4.3.8 Russia

5.4.3.9 Rest of Europe

5.4.4 South America

5.4.4.1 Brazil

5.4.4.2 Argentina

5.4.4.3 Colombia

5.4.4.4 Rest of South America

5.4.5 Middle-East and Africa

5.4.5.1 Saudi Arabia

5.4.5.2 South Africa

5.4.5.3 Nigeria

5.4.5.4 Qatar

5.4.5.5 Egypt

5.4.5.6 UAE

5.4.5.7 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share(%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Aviva Metals

6.4.2 Citizen Metalloys Ltd

6.4.3 Copper Braid Products

6.4.4 Cupori

6.4.5 Farmers Copper LTD

6.4.6 FURUKAWA ELECTRIC CO. LTD

6.4.7 KGHM

6.4.8 KME GERMANY GMBH

6.4.9 Metrod Holdings Berhad

6.4.10 Sam Dong

6.4.11 Lacroix + Kress GmbH

6.4.12 Mitsubishi Materials Corporation

6.4.13 PROTERIAL Ltd

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Growing Oxygen-free Copper Application in Wide Range of Electronics

7.2 Other Opportunities

Oxygen Free Copper Industry Segmentation

Oxygen-free copper is a category of highly conductive wrought copper alloys that have been electrolytically optimized to minimize oxygen levels to or below 0.001 percent. Oxygen-free copper is a grade of copper that has a high level of conductivity and is virtually free from oxygen content. Oxygen-free copper is used in several applications, such as in the manufacturing of semiconductors, superconductor components, and others.

The Oxygen Free Copper Market is Segmented by Grade (CU-OF and CU-OFE), Product (Wires, Strips, Busbars and Rods, and Other Products), End-user Industry (Electrical and Electronics, Automotive, Industrial, and Other End-user Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Report Offers Market Size and Forecasts for the Oxygen-Free Copper Market in Value (USD) for all the Above Segments.

| Grade | |

| CU-OF | |

| CU-OFE |

| Product | |

| Wires | |

| Strips | |

| Busbars and Rods | |

| Other Products (Tubes and Pipes, Etc.) |

| End-user Industry | |

| Electrical and Electronics | |

| Automotive | |

| Industrial | |

| Other End-user Industries (Power Generation, Aerospace, Etc.) |

| Geography | |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

|

Oxygen Free Copper Market Research FAQs

How big is the Oxygen Free Copper Market?

The Oxygen Free Copper Market size is expected to reach USD 20.29 billion in 2024 and grow at a CAGR of greater than 5% to reach USD 26.36 billion by 2029.

What is the current Oxygen Free Copper Market size?

In 2024, the Oxygen Free Copper Market size is expected to reach USD 20.29 billion.

Who are the key players in Oxygen Free Copper Market?

Copper Braid Products, Aviva Metals, Mitsubishi Materials Corporation, PROTERIAL, Ltd. and Sam Dong are the major companies operating in the Oxygen Free Copper Market.

Which is the fastest growing region in Oxygen Free Copper Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Oxygen Free Copper Market?

In 2024, the Asia Pacific accounts for the largest market share in Oxygen Free Copper Market.

What years does this Oxygen Free Copper Market cover, and what was the market size in 2023?

In 2023, the Oxygen Free Copper Market size was estimated at USD 19.28 billion. The report covers the Oxygen Free Copper Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Oxygen Free Copper Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Oxygen-Free Copper Industry Report

Statistics for the 2024 Oxygen-Free Copper market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Oxygen-Free Copper analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.