Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

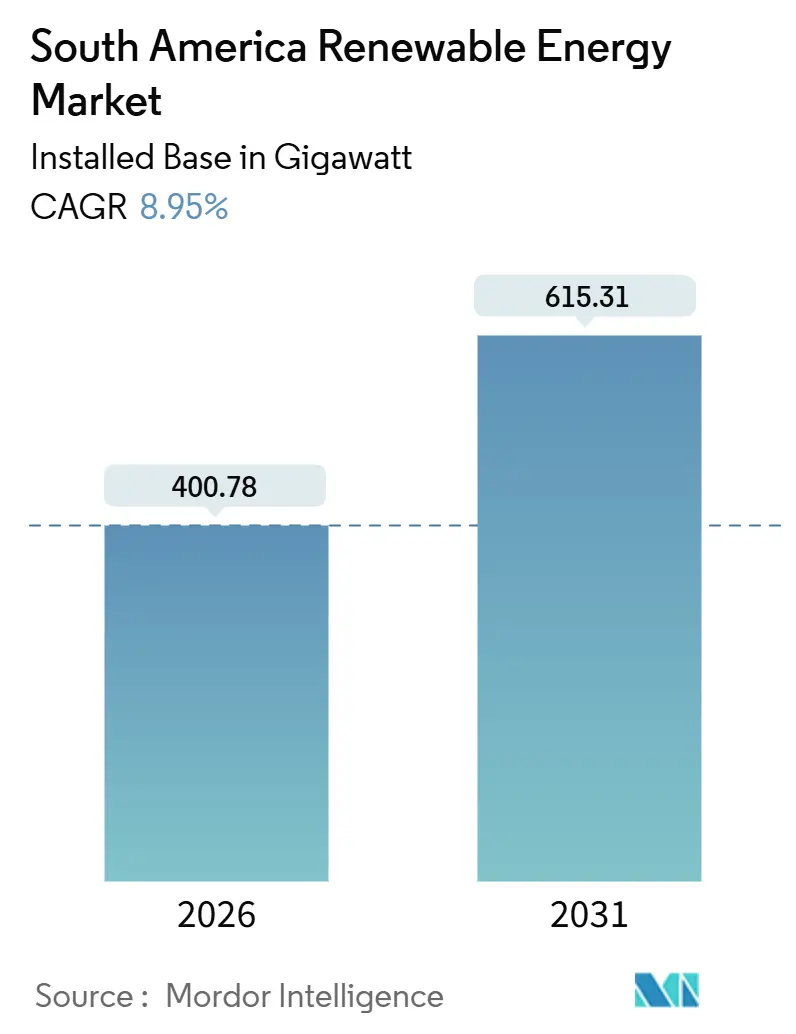

| Market Volume (2026) | 400.78 gigawatt |

| Market Volume (2031) | 615.31 gigawatt |

| Growth Rate (2026 - 2031) | 8.95% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Renewable Energy Market Analysis by Mordor Intelligence

The South America Renewable Energy Market size in terms of installed base is expected to grow from 400.78 gigawatt in 2026 to 615.31 gigawatt by 2031, at a CAGR of 8.95% during the forecast period (2026-2031).

Competitive auctions, lower levelized costs, and long-term corporate power-purchase agreements are aligning to pull fresh capital into utility-scale assets. Falling solar and wind tariffs now undercut thermal generation, while battery storage is easing variability concerns. Mining conglomerates are locking in 20-year fixed-price contracts to decarbonize off-grid operations, and green-hydrogen export plans are reshaping site selection toward coastal and desert regions. Developers that pair generation with storage secure cheaper funding, as lenders view the hybrids as dispatchable resources with stable cash flows.

Key Report Takeaways

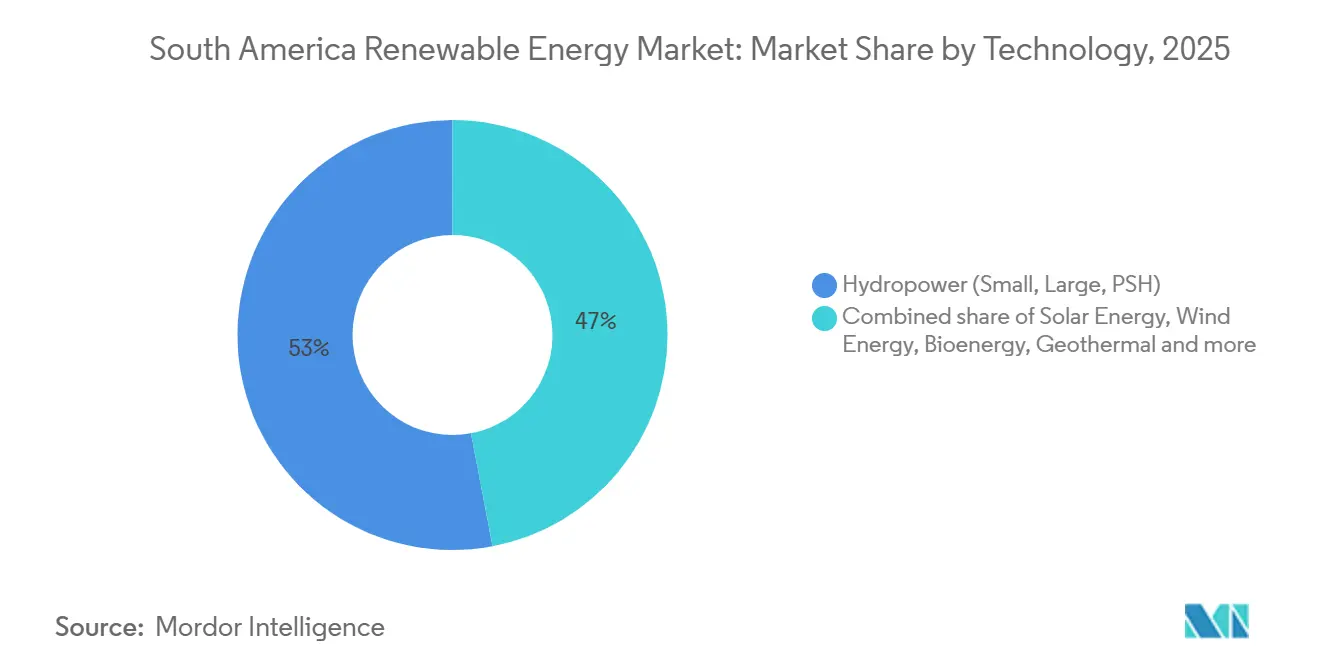

- By technology, hydropower led with 52.98% of the South America renewable energy market share in 2025, while solar is forecast to expand at an 18.30% CAGR through 2031.

- By end-user, utilities held 77.67% of capacity in 2025, but the commercial and industrial segment is projected to grow at a 13.88% CAGR to 2031.

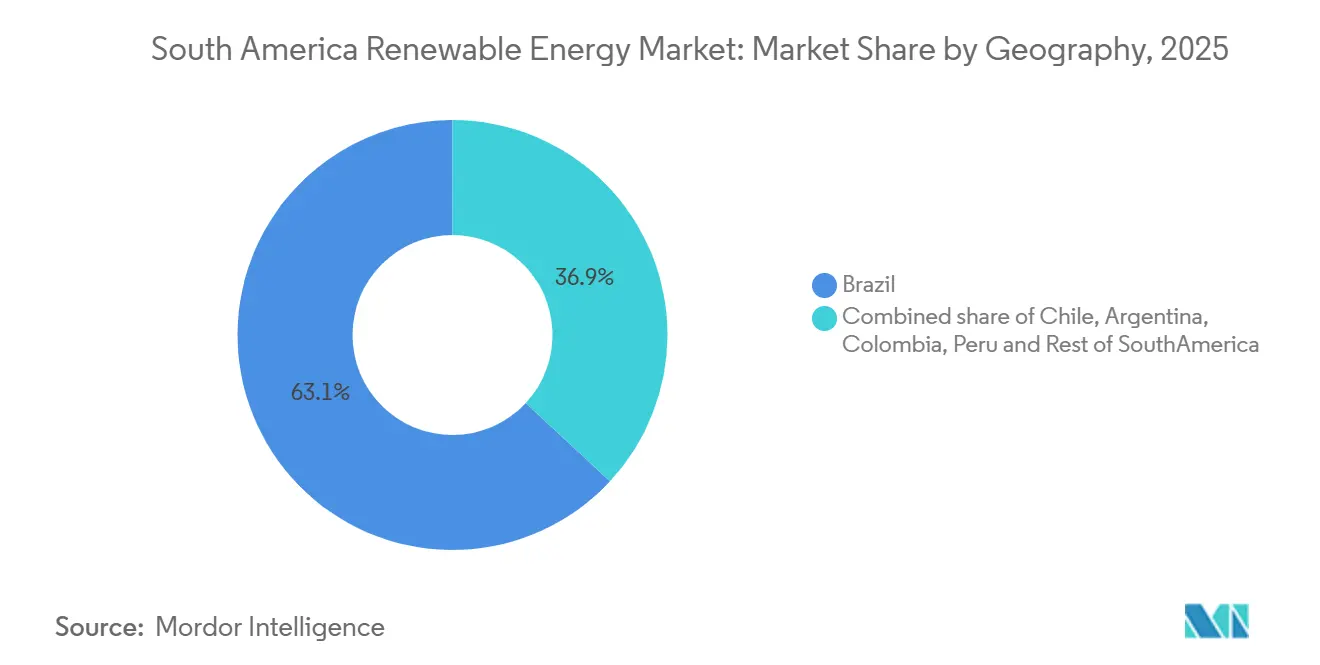

- By geography, Brazil commanded 63.09% of capacity in 2025, and Chile is set to record the fastest 17.19% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Renewable Energy Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Auction programs expanding project pipeline | +2.1% | Brazil, Chile, Colombia, Argentina | Medium term (2-4 years) |

| Declining LCOE for solar PV and onshore wind | +1.8% | Regionwide, strongest in Brazil and Chile | Short term (≤ 2 years) |

| Green-hydrogen export ambitions | +1.5% | Chile, Brazil northeast, Argentina Patagonia | Long term (≥ 4 years) |

| Mining-sector corporate PPAs | +1.3% | Chile, Peru, Brazil Minas Gerais and Pará | Medium term (2-4 years) |

| Grid-connected batteries | +1.0% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Renewable-Energy Auction Programs Accelerating Project Pipeline

Competitive tenders replaced feed-in tariffs after 2023. Brazil, Chile, and Colombia jointly awarded 8.5 GW in 2024-2025, and penalty clauses now force bidders to secure equipment and grid permits before signing, which cuts speculation and speeds build schedules. Brazil’s 2024 reserve auction cleared 3.1 GW at USD 28 per MWh, a record low that showed solar-plus-storage can compete with gas peakers. Chile’s 2025 2.5 GW call mandates four-hour batteries, ensuring a firm evening supply. Colombia’s 2.2 GW award in 2024 reopened its stalled market, while Argentina’s provinces tendered 800 MW of wind to bypass federal budget limits. These rules give investors confidence that contracted assets will connect on time and earn revenue from day one.

Declining LCOE for Solar PV and Onshore Wind

Utility-scale solar averaged USD 29 per MWh in 2024 as bifacial modules and single-axis trackers boosted yields by up to 20%.[1]International Renewable Energy Agency, “Renewable Power Generation Costs in 2023,” irena.org Onshore wind fell to USD 35 per MWh, helped by 120-meter hub heights that catch steadier flows in Brazil’s northeast. Chile’s Atacama solar parks signed sub-USD 20 PPAs in 2024, prompting early retirement of 1.2 GW of coal. Wind farms in Bahia logged more than 50% capacity factors in 2024, shrinking payback periods to under seven years. Cost parity against fossil assets has ended the need for subsidies, letting corporate buyers sign direct PPAs at tariffs 10-15% below retail rates.

Green-Hydrogen Export Ambitions Driving Utility-Scale Additions

Chile targets 25 GW of electrolyzers by 2030, which will need 40 GW of dedicated renewables.[2]International Energy Agency, “Global Hydrogen Review 2024,” iea.org The first 1.5 GW of linked capacity won contracts in 2024, locking in offtake with German and Japanese buyers. Brazil’s northeast coast plans 7 GW of offshore wind to feed hydrogen hubs near Ceará ports, and Uruguay commissioned a 10 MW pilot to produce ammonia for export. Investors accept slightly lower tariffs in exchange for 20-year hydrogen contracts, which cut merchant risk and pull in cheaper debt.

Mining-Sector Corporate PPAs for Off-Grid Decarbonization

Miners signed 4.2 GW of renewable PPAs in 2024-2025 to meet Scope 2 goals. Codelco inked a 1.8 TWh annual supply deal backed by 375 GWh of batteries, guaranteeing round-the-clock power for smelters in the Atacama. Anglo American committed USD 500 million for 300 MW of solar-plus-storage at Brazilian iron-ore sites, while Peru’s Antamina mine secured 120 MW of wind. Take-or-pay clauses and inflation-indexed tariffs turn these contracts into quasi-utility revenue streams, drawing pension funds seeking stable yields.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Transmission bottlenecks and delays | -1.2% | Brazil Bahia, Chile Atacama, Argentina Patagonia | Short term (≤ 2 years) |

| Foreign-exchange volatility | -0.9% | Argentina, Brazil, Colombia | Medium term (2-4 years) |

| Local-content rules raising OEM capex | -0.6% | Brazil, Argentina | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Transmission Bottlenecks and Interconnection Delays

Brazil’s Bahia queue reached 5.4 GW in late 2024, stretching average wait times to 18 months as new substations lag project completion. Chile’s Atacama backlog stranded 3 GW and caused 1.8 TWh of curtailment in 2024. Patagonia wind projects face a 24-month delay because high-voltage links to Buenos Aires remain unfunded. Long queues raise development costs 10-15% and erode tariff margins, pushing sponsors to demand grid-access guarantees before closing debt.

Local-Content Rules Increasing OEM Capex

Brazil requires 60% local content for wind and 50% for solar to tap BNDES loans, adding up to 12% to hardware prices. Vestas opened a nacelle plant in Bahia in 2024 to comply, but ramp-up delays lengthened lead times by four months.[3]Vestas Wind Systems A/S, “Serra do Assuruá Project Fact Sheet 2025,” vestas.com Argentina’s 30% rule inflated turbine prices by 15% because local suppliers cannot reach scale. While the mandates created about 12,000 manufacturing jobs, they cut developer margins by 200-300 basis points and slowed project schedules.

Segment Analysis

By Technology: Solar Surges as Hydro Dominance Wanes

Hydropower held 52.98% of 2025 capacity, yet environmental permitting and variable rainfall slow new builds. Solar will grow at an 18.30% CAGR, the fastest of any technology, propelled by sub-USD 30 per MWh economics and modular designs that skirt transmission bottlenecks. Wind adds about 4.5 GW annually, boosted by 50% capacity factors in Brazil’s northeast. Bioenergy contributes 12 GW through bagasse-fired cogeneration, anchored by Brazil’s RenovaBio targets. Emerging niches include pumped-storage hydropower such as Brazil’s 401 MW Sinop project, which delivers eight-hour discharge capability. Offshore wind development is taking shape with a 16 GW Brazilian pipeline aiming for first turbines in 2027.

Solar’s rapid buildout is shifting the power mix, yet higher variable output requires storage for evening peaks. Concentrated solar power remains marginal beyond Chile’s 110 MW Cerro Dominador plant due to USD 6,000-per-kW costs. Geothermal holds 48 MW at Cerro Pabellón, though Enel is exploring another 200 MW in the Andes. Ocean energy is still confined to pilot projects with capital costs above USD 10,000 per kW. The South America renewable energy market size allocated to solar and wind will therefore expand faster than hydro until 2031, provided that storage and grid upgrades keep pace.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User: C&I Segment Accelerates Behind Utilities

Utilities controlled 77.67% of capacity in 2025 because auction volumes feed directly into their portfolios. The commercial and industrial segment is set to grow at a 13.88% CAGR, powered by behind-the-meter rooftop solar in Brazil and Chile. Distributed solar in Brazil hit 39 GW in 2024, and 28 GW came from C&I rooftops that shave bills 30-40% below grid rates. Chile’s revised net-metering lets businesses sell surplus electricity at 70% of retail rates, adding 1.2 GW of new rooftops in 2024. Mining PPAs form the largest anchor load within C&I, while residential systems reached 8 GW in 2025, mostly in Brazil’s southeast.

Currency instability curbed Argentina’s residential uptake in 2024, but property-tax breaks in Mendoza revived sales in 2025. Colombia’s residential market stayed small at 200 MW as low tariffs lengthen payback periods. As corporate buyers chase price certainty, the South America renewable energy market will see more capacity shift from utilities to C&I rooftops, easing the strain on transmission lines.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Brazil held 63.09% of 2025 capacity with 100 GW of hydro, 45 GW of wind, 39 GW of distributed solar, and 28 GW of utility solar. An August 2024 reserve auction cleared 3.1 GW at USD 28 per MWh and allocated 60% to solar-plus-storage hybrids. A 1.6 GW storage tender the same year underscored a grid-flexibility pivot as variable renewables crossed 30% penetration. Offshore wind is gaining traction through Petrobras’s 7 GW plan and Iberdrola’s 14 GW pipeline, each targeting 2027 installation. ANEEL approved USD 2.1 billion in new lines to ease Bahia and Rio Grande do Norte.

Chile will post the region’s quickest 17.19% CAGR over 2026-2031. Green-hydrogen export contracts secured 1.5 GW of dedicated renewable capacity in 2024, and battery mandates require 20% storage pairing for all large projects from 2025. Transmission upgrades now fast-track 500 kV lines from Atacama to Santiago. Codelco’s 1.8 TWh annual PPA, backed by 375 GWh of batteries, shows how mining demand anchors growth.

Argentina logged 12 GW of capacity in 2025, mainly wind in Patagonia, but currency swings delayed 1.2 GW of new builds. Provincial auctions for 800 MW of wind used multilateral finance to sidestep federal policy gaps. Colombia returned from a five-year pause with 2.2 GW of 2024 auction awards in La Guajira, while Peru advanced 1.5 GW of pipeline projects spearheaded by Enel’s 240 MW Wayra expansion. Uruguay, Paraguay, Ecuador, and Bolivia combined for 8.2 GW in 2025, led by Uruguay’s 10 MW hydrogen pilot.

Note: Segment shares of all individual segments available upon report purchase

Competitive Landscape

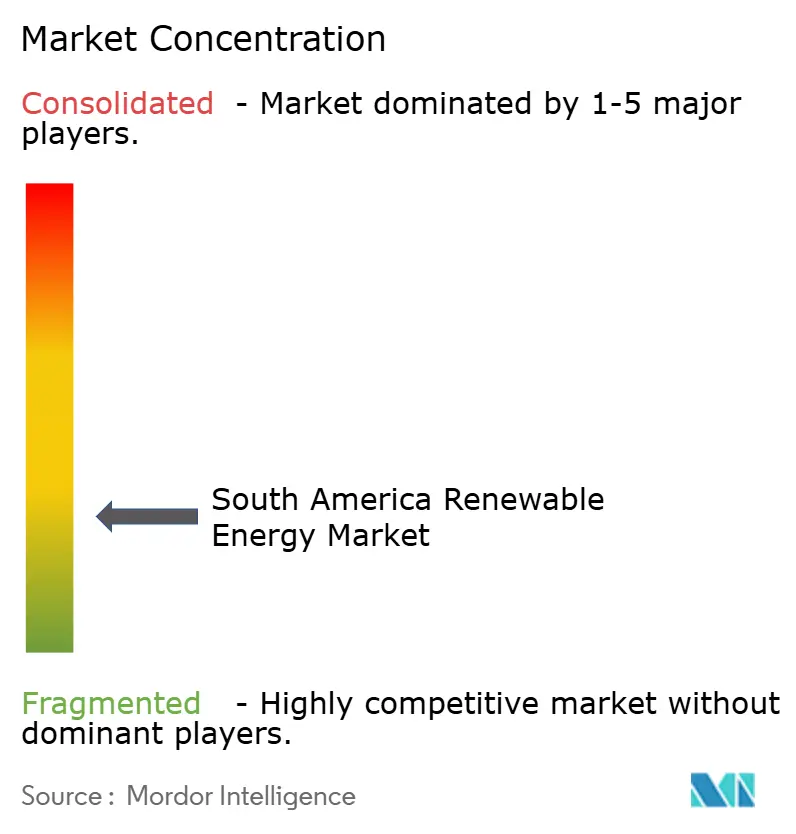

The top ten companies controlled about 45% of installed capacity in 2025, pointing to moderate fragmentation. Enel, Iberdrola, and ENGIE integrate generation, transmission, and retail, giving them bidirectional flexibility to balance portfolios and hedge demand swings. Independent power producers such as Atlas Renewable Energy and Brookfield Renewable Partners focus on long-dated corporate PPAs that secure sub-5% financing. Equipment majors Vestas, Siemens Gamesa, and GE Renewable Energy add digital-twin software that lifts annual output by 3% at installations like the 846 MW Serra do Assuruá wind farm.[4]Vestas Wind Systems A/S, “Serra do Assuruá Project Fact Sheet 2025,” vestas.com

Hybrid solar-wind-battery projects are a white-space niche that rewards developers with storage expertise. ABO Wind and Mainstream Renewable Power chase sub-100 MW assets in Peru and Colombia, where large utilities have limited reach. Chinese OEMs Canadian Solar and Trina Solar are moving upstream into project development, using supply chain control to trim EPC costs 10-15% below Western rivals. Local-content hurdles and ISO 14001 compliance favor incumbents with established manufacturing bases and regulatory teams.

South America Renewable Energy Industry Leaders

Enel Green Power S.p.A.

Iberdrola S.A.

ENGIE Brasil Energia S.A.

Neoenergia S.A.

AES Andes S.A.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: Mercomar is enhancing its logistics services for solar and wind projects across South America, focusing on critical and oversized cargo such as turbines, blades, and transformers. This initiative aims to accelerate project execution, minimize transport risks, and support the scaling of utility-scale renewable installations in Brazil, Chile, and neighboring markets.

- November 2025: Statkraft has inaugurated 340 MW of solar projects in Brazil, expanding its renewable energy portfolio in Latin America. These projects enhance clean energy supply, support Brazil’s growing solar market, and contribute to emissions reductions, reinforcing Statkraft’s role in utility-scale renewable energy development across South America.

- November 2025: According to IRENA, South America’s clean energy transition could generate approximately USD 500 billion annually, fostering job creation, economic growth, and energy security. The report underscores the importance of investments in large-scale solar, wind, grids, and storage, positioning the region as a global renewable energy hub while advancing decarbonization efforts.

- October 2025: A recent roundup highlights the growth of solar PV capacity in Latin America, driven by new project announcements, policy developments, and financing activities. Brazil and Chile remain key markets, supported by declining module prices, corporate PPAs, and grid-scale additions, solidifying South America’s position as a growing solar investment hub.

South America Renewable Energy Market Report Scope

The renewable energy market encompasses the global and regional industry framework engaged in the development, production, installation, operation, financing, and trade of energy derived from naturally replenishing sources. These sources are renewed on a human timescale and generate minimal to no greenhouse gas emissions during operation.

The South American renewable energy market is segmented by technology, end-user, and geography. By technology, the market is segmented into solar energy, wind energy, hydropower, bioenergy, geothermal, and ocean energy. By end-user, the market is divided into utilities, commercial and industrial, residential. The report also covers the market size and forecasts for the South American renewable energy market across the major countries. For each segment, the market sizing and forecasts have been done based on installed capacity (GW).

By Technology

| Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) |

| Hydropower (Small, Large, PSH) |

| Bioenergy |

| Geothermal |

| Ocean Energy (Tidal and Wave) |

By End-User

| Utilities |

| Commercial and Industrial |

| Residential |

By Geography

| Brazil |

| Chile |

| Argentina |

| Colombia |

| Peru |

| Rest of South America |

| By Technology | Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) | |

| Hydropower (Small, Large, PSH) | |

| Bioenergy | |

| Geothermal | |

| Ocean Energy (Tidal and Wave) | |

| By End-User | Utilities |

| Commercial and Industrial | |

| Residential | |

| By Geography | Brazil |

| Chile | |

| Argentina | |

| Colombia | |

| Peru | |

| Rest of South America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the South America renewable energy market in 2026?

Installed capacity stands at 400.78 GW in 2026, on track for 615.31 GW by 2031 at an 8.95% CAGR.

Which country is growing fastest in renewable capacity?

Chile is forecast to expand at roughly 17% annually through 2031 as hydrogen export projects and mining PPAs lift demand.

Why are corporate PPAs popular with miners?

Long-term fixed-price PPAs slash Scope 2 emissions and stabilize energy costs for remote smelters that face diesel price volatility.

What role will battery storage play by 2030?

Four-hour lithium-ion systems will pair with most new solar and wind plants, cutting curtailment and letting grids exceed 40% variable renewables without reliability loss.

How is foreign-exchange risk managed in Brazil?

Developers increasingly use BNDES currency-hedged loans that cap exposure at 30% of project value, though hedging adds up to 120 basis points to borrowing costs.

Which technologies will add the most capacity by 2031?

Solar leads with an 18% CAGR, followed by wind, while hydro additions remain limited due to environmental and social hurdles.