Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

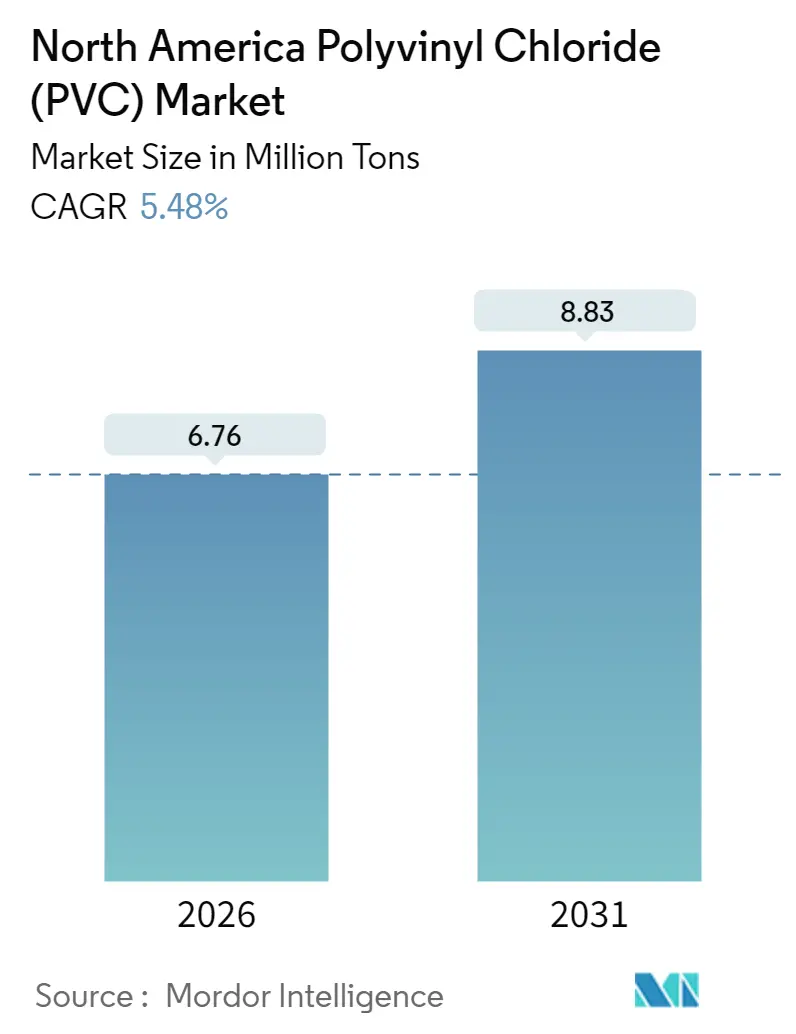

| Market Volume (2026) | 6.76 Million tons |

| Market Volume (2031) | 8.83 Million tons |

| Growth Rate (2026 - 2031) | 5.48% CAGR |

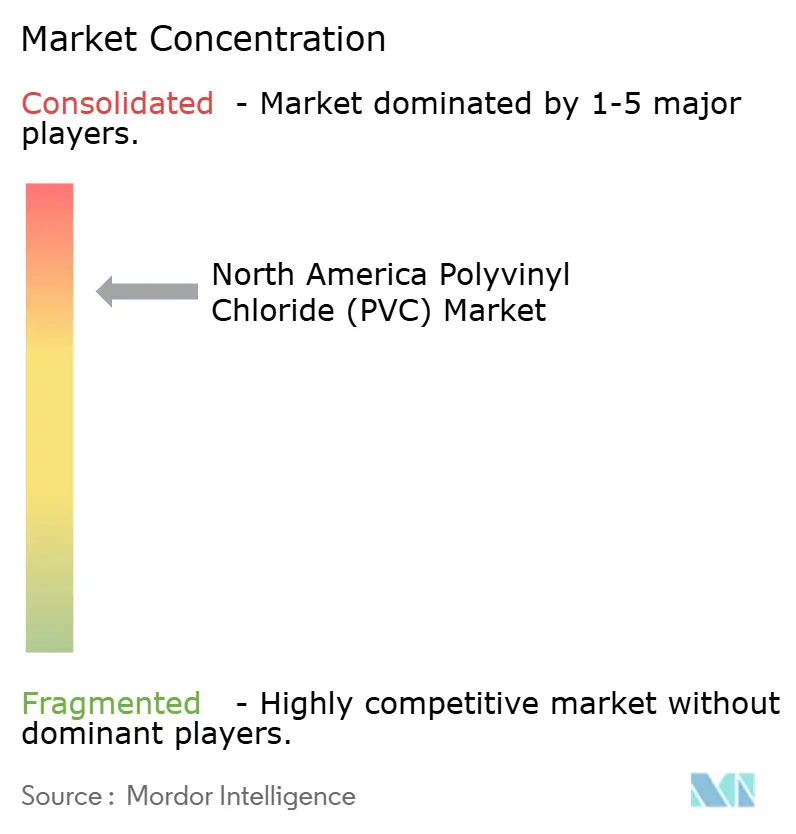

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Polyvinyl Chloride (PVC) Market Analysis by Mordor Intelligence

The North America Polyvinyl Chloride market is expected to grow from 6.41 million tons in 2025 to 6.76 million tons in 2026 and is forecast to reach 8.83 million tons by 2031 at 5.48% CAGR over 2026-2031. Continued infrastructure modernization, especially the federally funded replacement of lead service lines, underpins this expansion even as supply‐chain volatility persists. Demand visibility is strong because municipalities must comply with the ten-year mandate for full lead pipe replacement, insulating pipe purchases from broader economic swings. The United States accounts for the largest regional PVC consumption, supported by advantaged ethane costs that cushion producers from feedstock price shocks. Healthcare is gaining importance as the fastest-growing end user, propelled by demographic trends and the shift to phthalate-free medical devices. Competitive intensity centers on vertical integration, specialty compounding, and sustainability innovations that protect margins in a globally oversupplied resin market.

Key Report Takeaways

- By product type, rigid PVC led with 59.65% North America Polyvinyl Chloride market share in 2025, while flexible PVC is projected to register a 5.82% CAGR through 2031.

- By application, pipes and fittings commanded 45.62% of the North America Polyvinyl Chloride market size in 2025, whereas profiles, hoses, and tubing are forecast to grow at a 5.63% CAGR to 2031.

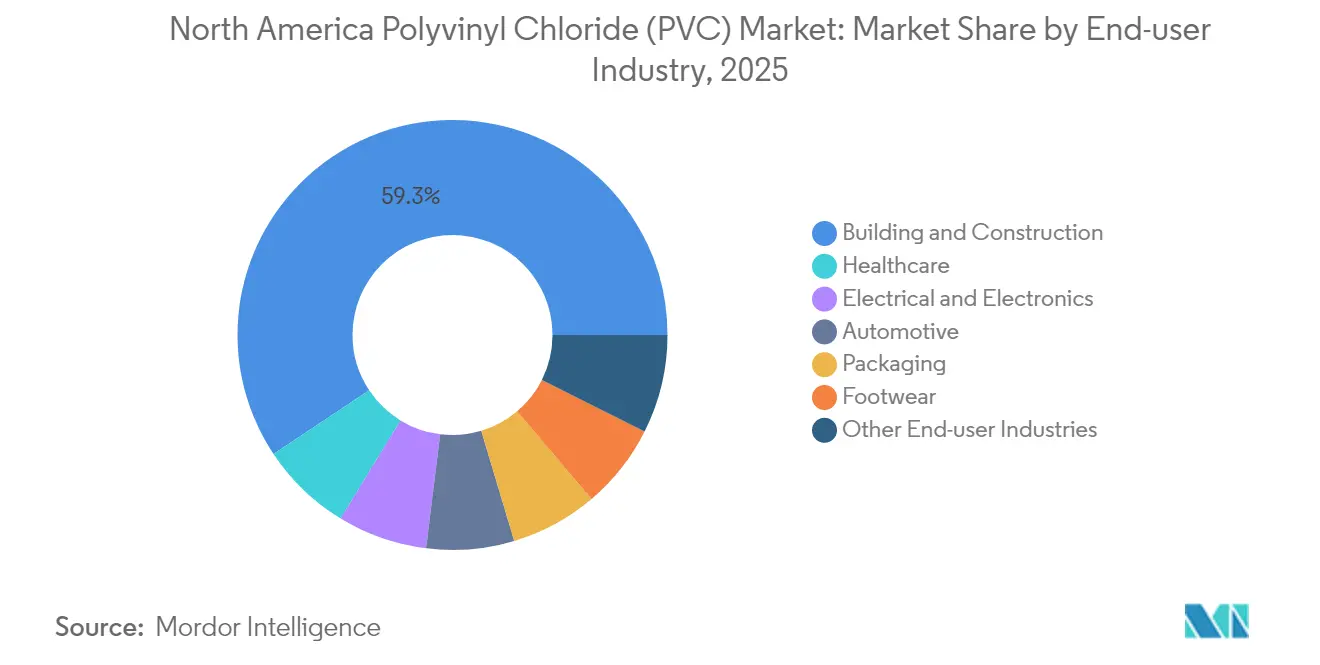

- By end-user industry, building and construction held 59.34% North America Polyvinyl Chloride market share in 2025, while healthcare is poised for the fastest 6.12% CAGR through 2031.

- By geography, the United States accounted for 77.85% regional consumption in 2025 and is anticipated to post a 5.93% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Polyvinyl Chloride (PVC) Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from building and construction | +1.8% | United States, Canada, Mexico | Medium term (2-4 years) |

| Surging use in medical-grade devices and IV bags | +1.2% | United States, Canada | Long term (≥ 4 years) |

| Federal funding for replacement water infrastructure | +1.5% | United States | Short term (≤ 2 years) |

| Regulatory tailwinds for lead-free plumbing | +0.7% | United States, Canada | Medium term (2-4 years) |

| Bio-based plasticizers unlocking premium niches | +0.3% | North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Rising Demand from Building and Construction

PVC consumption in construction tracks the recovery of public works spending, with pipes and fittings representing almost half of all applications. States and provinces are replacing aging distribution networks because federal rules prohibit deferrals. Building codes that cap lead content steer projects toward rigid vinyl systems, while producers leverage integrated ethylene chains to stabilize costs[1]U.S. Environmental Protection Agency, “News Release: EPA Finalizes Rule to Eliminate Lead Pipes,” epa.gov . Long-term infrastructure programs create predictable order books, encouraging capacity upgrades at domestic plants and sustaining resin uptake regardless of private housing cycles.

Surging Use in Medical-Grade Devices and IV Bags

Healthcare demand expands at 6.34% CAGR as hospitals specify non-DEHP compounds for blood bags, tubing, and catheters. Material formulators now offer phthalate-free additives that pass FDA tests without trade-offs in clarity, flexibility, or sterilization resistance. Higher regulatory barriers and validation costs favor established suppliers, enabling premium pricing that offsets commodity margin pressure in the North America Polyvinyl Chloride market. An aging population and the growth of home-based care further extend this demand runway.

Federal Funding for Replacement Water Infrastructure

A USD 15 billion federal allocation obliges utilities to eliminate every lead service line within a decade. The mandate ensures multiyear purchasing schedules for AWWA-compliant PVC pipe, creating a demand floor that lessens the market’s exposure to macroeconomic downturns. Buy America clauses channel much of this spending to domestic mills, fortifying North America's Polyvinyl Chloride market volumes and encouraging backward integration into vinyl chloride monomer production.

Regulatory Tailwinds for Lead-Free Plumbing

Federal law now limits lead content in potable water components to 0.25%, effectively positioning PVC as the default material. The rule applies to new builds and retrofits, expanding addressable demand across commercial and residential properties. Contractors prefer PVC because it combines lead-free compliance with lifetime cost advantages compared with copper or galvanized steel. As more municipalities adopt parallel ordinances, substitution gains widen across the region.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile vinyl chloride monomer and ethylene prices | -0.8% | North America | Short term (≤ 2 years) |

| Intensifying environmental and health scrutiny | -0.5% | United States, Canada | Long term (≥ 4 years) |

| Tightening limits on phthalate plasticizers | -0.3% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Vinyl Chloride Monomer and Ethylene Prices

Feedstock swings erode margins because raw materials represent up to 70% of production cost. Recent rail incidents underscore logistical risk, while planned shutdowns at major crackers tighten regional availability and amplify spot volatility. Integrated firms cushion some of the impact through advantaged ethane, but merchant buyers face sharper price spikes, complicating inventory planning across the North America Polyvinyl Chloride market.

Intensifying Environmental and Health Scrutiny

Policymakers debating a global plastics treaty are testing whether PVC should be labeled problematic, prompting investors to weigh long-term restriction scenarios. EU studies flag additive toxicity, and high-profile incidents intensify public concern about vinyl chloride handling[2]Yale Environment 360, “PVC Under Scrutiny,” yale.edu. Flooring and roofing manufacturers launch PVC-free lines, signaling incremental substitution risk in architect-specified products.

Segment Analysis

By Product Type: Rigid Applications Drive Volume Leadership

Rigid PVC accounted for 59.65% of total volume in 2025, underscoring its strength in underground water infrastructure, where lifespan and cost stability prevail. That share translates to the largest slice of the North America Polyvinyl Chloride market size, anchored by pipes mandated in federally funded projects. Rigid formulations also serve window profiles and siding, adding steady demand outside public works.

The flexible category advances at a 5.82% CAGR as medical devices, hoses, and wire coatings adopt specialized compounds. Manufacturers differentiate through clarity, low-temperature flexibility, and phthalate-free chemistries. Chlorinated PVC retains a niche in hot-water lines, while low-smoke grades address fire-safety codes in transit and high-occupancy buildings. Product mix continues shifting toward specialty grades that command higher margins and reduce exposure to global commodity cycles.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Infrastructure Modernization Sustains Pipe Dominance

Pipes and fittings supplied 45.62% of regional demand in 2025, bolstered by legislated lead replacement that secures multiyear project pipelines. That dominance keeps the North America Polyvinyl Chloride market volumes closely tied to municipal procurement calendars rather than private housing trends. Water and wastewater pipes are typically specified in diameters that optimize balance between tensile strength and hydraulic performance, reinforcing rigid PVC’s entrenched position.

Profiles, hoses, and tubing outpace growth at 5.63% CAGR through 2031. Healthcare tubing, beverage hoses, and precision-profile extrusions require tight dimensional tolerances and customized additive packages. Films and sheets maintain mid-single-digit growth by serving construction membranes and protective packaging, while cables benefit from grid upgrades and data-center expansion across the United States. Bottles are mature and face lightweighting or material-swap pressure in consumer goods.

By End-User Industry: Healthcare Growth Offsets Construction Volatility

Building and construction held a 59.34% share in 2025, reflecting the historical backbone of the North America Polyvinyl Chloride market. Public infrastructure budgets and code updates sustain volumes, but the segment remains exposed to cyclical swings in private non-residential starts.

Healthcare grows fastest at 6.12% CAGR, adding portfolio balance for resin suppliers. Medical device OEMs demand validated raw materials, limiting entry for new competitors. Electrical and electronics absorb steady volumes as utilities harden grids and data centers proliferate. Automotive uptake is mixed; electric vehicles use PVC in battery casings and cable glands but less in trim. Packaging and footwear remain stable but confront sustainability scrutiny from brand owners and consumers.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The United States captured 77.85% of regional consumption in 2025 and is set to expand at a 5.93% CAGR to 2031. Federal water funding and Buy America supply preferences underpin continued growth even as export opportunities narrow due to foreign duties. Abundant shale-based ethane keeps domestic integrated producers cost-competitive.

Canada is a mature market where provincial rules align with U.S. lead limits, maintaining steady refurbishment demand. Pilot programs that collect post-consumer vinyl windows point to a developing circular economy and could influence procurement criteria in future public tenders.

Mexico represents the fastest relative expansion, supported by industrialization and electrical conduit investment. The USMCA rules streamline the cross-border trade of compound and finished pipe. Domestic capacity additions reduce reliance on Asian imports and strengthen regional supply resilience.

Competitive Landscape

The regional market shows moderate concentration: the top five producers combine integrated chlor-alkali assets with downstream extrusion networks, giving a defensible cost and distribution edge. Strategic focus is shifting toward specialty compounding and circularity. Producers collaborate with recyclers to incorporate post-industrial and post-consumer resin, enhancing ESG credentials required by public-sector buyers. Emerging challengers promote PVC-free alternatives in flooring and roofing, but material substitution remains limited in pressurized water infrastructure, where vinyl’s balance of price, strength, and chemical resistance is difficult to replicate. Environmental compliance and product stewardship programs thus become key differentiators as buyers scrutinize suppliers’ lifecycle footprints.

North America Polyvinyl Chloride (PVC) Industry Leaders

Westlake Corporation

Shin-Etsu Chemical Co., Ltd.

Formosa Plastics Corporation

Occidental Petroleum Corporation

Orbia Polymer Solutions (Vestolit)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: Westlake Corporation announced plans to start a new molecular-oriented PVC (PVCO) plant in Wichita Falls, Texas, by 2026. The expansion will add four production lines to support growing demand in the municipal pipe sector. PVCO offers enhanced strength and sustainability by enabling thinner-walled pipes with reduced material usage.

- January 2025: GEON acquired Foster, LLC to strengthen its presence in the high-growth healthcare and medical device sector. The acquisition enhances GEON’s medical offerings, including rigid/flexible PVC and TPE solutions.

North America Polyvinyl Chloride (PVC) Market Report Scope

Polyvinyl chloride is strong and lightweight, durable to weathering, rotting, chemical corrosion, and abrasion, versatile, and easy to use, as it can be cut, shaped, welded, and joined in any style. The North American polyvinyl chloride (PVC) market is segmented by product type (rigid PVC, flexible PVC, low-smoke PVC, and chlorinated PVC), application (pipes and fittings, films and sheets, wires and cables, bottles, profiles, hoses and tubing, and other applications), end-user industry (building and construction, automotive, electrical and electronics, packaging, footwear, healthcare, and other end-user industries), and geography (United States, Canada, and Mexico). The report also offers the size and forecasts of the markets for three countries in the region. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

By Product Type

| Rigid PVC | Clear Rigid PVC |

| Non-clear Rigid PVC | |

| Flexible PVC | Clear Flexible PVC |

| Non-clear Flexible PVC | |

| Low-smoke PVC | |

| Chlorinated PVC |

By Application

| Pipes and Fittings |

| Films and Sheets |

| Wires and Cables |

| Bottles |

| Profiles, Hoses and Tubing |

| Other Applications |

By End-user Industry

| Building and Construction |

| Electrical and Electronics |

| Healthcare |

| Automotive |

| Packaging |

| Footwear |

| Other End-user Industries |

By Country

| United States |

| Canada |

| Mexico |

| By Product Type | Rigid PVC | Clear Rigid PVC |

| Non-clear Rigid PVC | ||

| Flexible PVC | Clear Flexible PVC | |

| Non-clear Flexible PVC | ||

| Low-smoke PVC | ||

| Chlorinated PVC | ||

| By Application | Pipes and Fittings | |

| Films and Sheets | ||

| Wires and Cables | ||

| Bottles | ||

| Profiles, Hoses and Tubing | ||

| Other Applications | ||

| By End-user Industry | Building and Construction | |

| Electrical and Electronics | ||

| Healthcare | ||

| Automotive | ||

| Packaging | ||

| Footwear | ||

| Other End-user Industries | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What volume will PVC demand in North America reach by 2031?

Consumption is projected to rise to 8.83 million tons by 2031 at a 5.48% CAGR from 6.76 million tons in 2026.

Which application holds the largest share of regional PVC use?

Pipes and fittings account for 45.62% of total demand thanks to mandated water infrastructure upgrades.

Which end-user segment is growing fastest?

Healthcare products using medical-grade PVC are expanding at a 6.12% CAGR through 2031.

Why do U.S. producers have a cost edge in PVC?

Access to abundant shale-based ethane keeps ethylene feedstock costs low, improving integrated margins.

How does federal funding influence PVC demand?

A USD 15 billion program requiring lead service line removal guarantees multiyear pipe orders, insulating the market from construction cycles.