Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

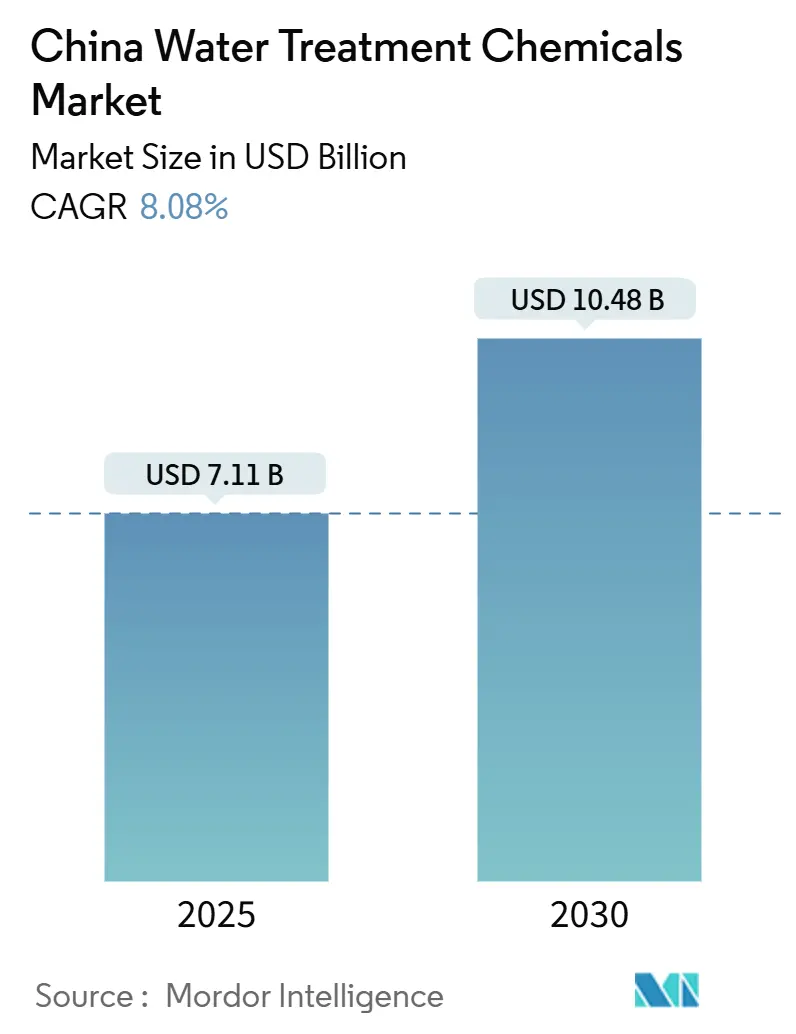

| Market Size (2025) | USD 7.11 Billion |

| Market Size (2030) | USD 10.48 Billion |

| Growth Rate (2025 - 2030) | 8.08% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Water Treatment Chemicals Market Analysis by Mordor Intelligence

The China Water Treatment Chemicals Market size is estimated at USD 7.11 billion in 2025, and is expected to reach USD 10.48 billion by 2030, at a CAGR of 8.08% during the forecast period (2025-2030). Robust funding for water infrastructure, strict GB 8978-2020 discharge limits, and zero-liquid-discharge (ZLD) directives in lithium-battery hubs are reinforcing demand for coagulants, flocculants, and advanced oxidation agents across municipal and industrial sites. Cooling system retrofits at hyperscale data centers and closed-loop upgrades at new coal and nuclear plants are widening the addressable base for corrosion inhibitors, scale preventers, and biocides. Green treatment chemistries that enable resource recovery under circular-economy mandates are evolving from niche to mainstream, while real-time dosing platforms are trimming chemical consumption yet expanding value-added service revenue. Competitive intensity remains moderate: multinationals leverage formulation know-how, whereas regional specialists exploit cost advantages and local market familiarity to serve fragmented end-user needs.

Key Report Takeaways

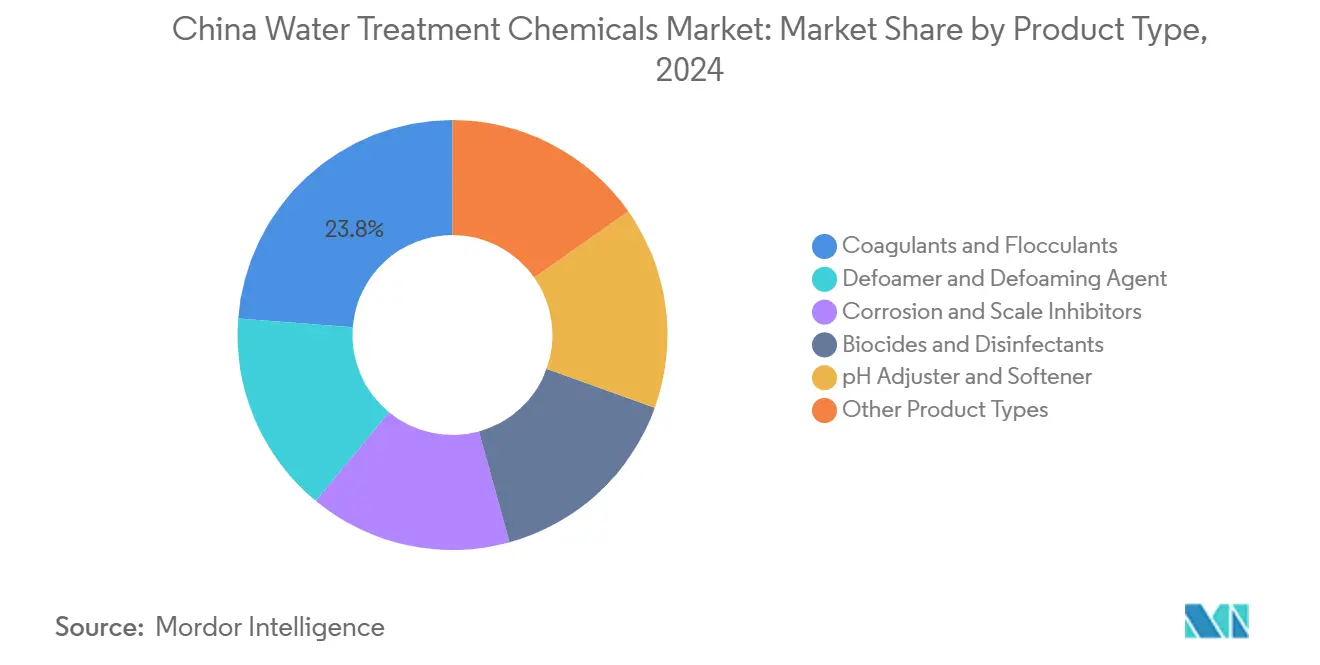

- By product type, coagulants and flocculants held 23.78% of the China water treatment chemicals market share in 2024 and are projected to expand at an 8.90% CAGR through 2030.

- By application, cooling water treatment commanded 32.16% of the China water treatment chemicals market size in 2024, while green water treatment is set to register the fastest 9.12% CAGR from 2025 to 2030.

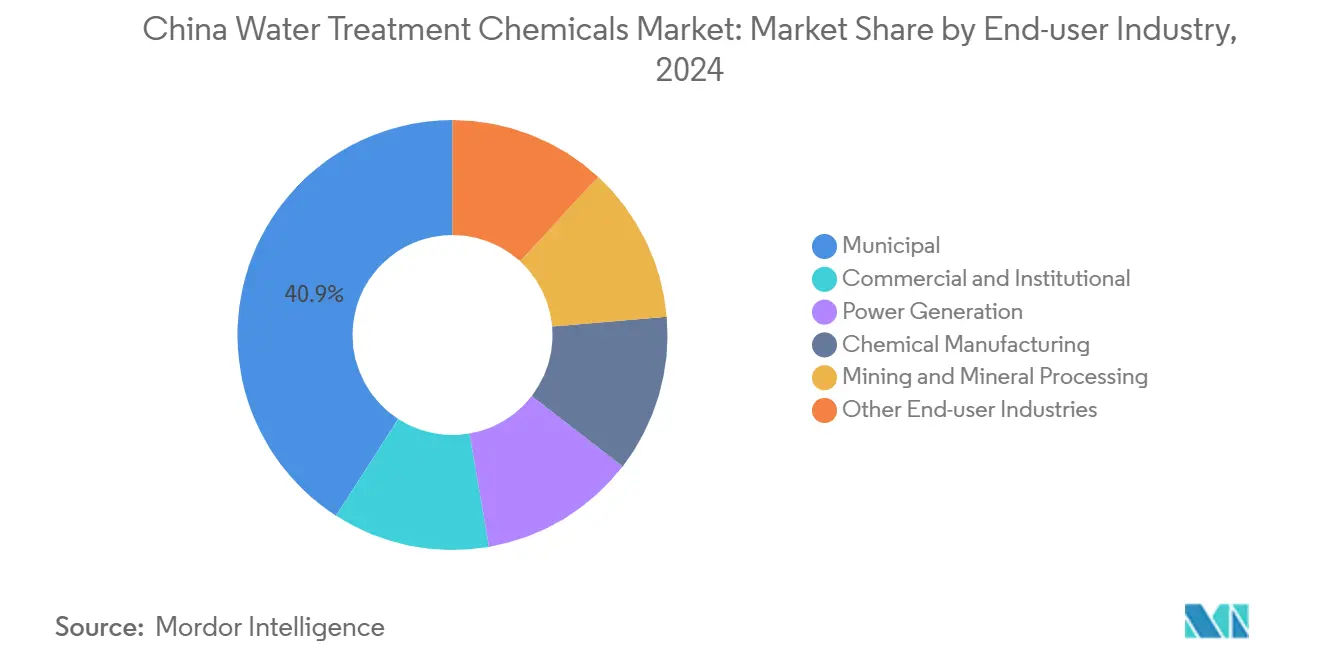

- By end-user industry, the municipal sector captured 40.89% market share in 2024, and also represents the fastest-growing segment, advancing at an 8.94% CAGR through 2030.

China Water Treatment Chemicals Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid capacity additions in coal and nuclear power plants | +1.8% | Northern China, Inner Mongolia, Xinjiang | Medium term (2-4 years) |

| Stricter industrial wastewater discharge standards (GB 8978-2020) | +2.1% | National, concentrated in industrial zones | Short term (≤ 2 years) |

| Municipal WWTP upgrades under the 14th Five-Year Plan | +1.5% | Tier 2-3 cities, western regions | Long term (≥ 4 years) |

| ZLD mandates in lithium-battery manufacturing hubs | +0.9% | Jiangsu, Zhejiang, Guangdong provinces | Medium term (2-4 years) |

| Surge in hyperscale data-centre cooling demand | +1.2% | Beijing-Tianjin-Hebei, Yangtze River Delta | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Capacity Additions in Coal and Nuclear Power Plants

New thermal and nuclear units impose higher water-quality standards, compelling operators to deploy sophisticated boiler-water conditioning packages and flue-gas desulfurization additives. In 2024, China commissioned 47.4 GW of new coal capacity, with each gigawatt consuming 3,000-5,000 tons of treatment chemicals annually[1]Ministry of Ecology and Environment, “Announcement on Air-Pollutant Emission Standards for Coking Chemical Industry,” mee.gov.cn . Ultra-pure systems at coastal reactors now rely on mixed-bed ion-exchange resins and low-fouling antiscalants to meet zero-emission goals. Closed-loop cooling retrofits curb freshwater draw but heighten the need for long-life corrosion inhibitors and microbiological controls. Procurement teams increasingly seek bundled chemical-and-service contracts that guarantee performance and mitigate price volatility over the life of the plant. Suppliers that demonstrate expertise in high-TDS brine crystallization and onsite technical support are increasingly shortlisted for multiyear frameworks.

Stricter Industrial Wastewater Discharge Standards (GB 8978-2020)

GB 8978-2020 reduced chemical-oxygen-demand limits to 50 mg/L and added 21 heavy metals plus 60 organics, forcing industrial parks to adopt advanced oxidation, membrane, and targeted coagulant regimens. Compliance costs run CNY 21-29 per ton of wastewater, with chemicals representing one-third of outlays. Phased rollout through 2027 assures steady demand, yet inconsistent regional enforcement fragments product specifications. Suppliers offering modular chemical portfolios that can be rapidly re-tuned to local discharge permits gain a competitive edge. Centralized treatment facilities unlock bulk-procurement efficiencies, prompting strategic alliances between chemical formulators and park operators.

Municipal WWTP Upgrades Under the 14th Five-Year Plan

Phosphorus caps of 0.2 mg/L in sensitive basins require high-basicity aluminum chloride and ferric sulfate blends. Rural expansion adds thousands of decentralized units where intermittent flows demand chemicals with broad dosage windows and high stability. Smart sensors integrated with supervisory control systems now automate feed rates, cutting chemical consumption up to 20% while maintaining effluent quality. Long-term service agreements, rather than one-off product sales, are becoming the dominant municipal procurement model.

ZLD Mandates in Lithium-Battery Manufacturing Hubs

EV battery plants discharge high-salinity streams rich in lithium and transition metals. Specialized flocculants and pH modulators paired with electrodialysis systems reclaim more than 95% lithium carbonate for reuse. Concentration of capacity in Jiangsu, Zhejiang, and Guangdong creates dense regional demand for antiscalants tailored to high-ionic-strength brines. Export restrictions on lithium-processing technologies introduced in 2025 accelerate domestic innovation in proprietary chemistries that protect national supply chains. Chemical suppliers that integrate resource-recovery value propositions into their offerings gain preferred-vendor status.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight limits on chlorinated organics (Class V water) | -0.8% | National sensitive watersheds | Medium term (2-4 years) |

| Raw-material price volatility amid eco-inspections | -1.3% | Shandong, Jiangsu production hubs | Short term (≤ 2 years) |

| Carbon-pricing costs for chemical-intensive plants | -0.6% | Northern steel and cement clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tight Limits on Chlorinated Organics (Class V Water)

Class V water rules cap total organic halogens at 0.5 mg/L, restricting chlorine-based biocides historically favored for cost and efficacy[2]ScienceDirect, “Cost of Wastewater Treatment in a Chemical Industrial Park,” sciencedirect.com . Facilities near fragile ecosystems are shifting to ozone, UV, or peracetic acid regimes that lack residual kill but meet discharge permits. Transition raises operating costs by 20-30% and shortens the shelf life of on-site chemical stocks. Technology providers capable of marrying alternative disinfectants with real-time monitoring systems are offsetting efficacy gaps through data-driven control.

Raw-Material Price Volatility Amid Eco-Inspections

Spot caustic-soda prices rose in 2024 when eco-inspections shuttered upstream chlor-alkali plants. Chemical formulators face margin compression on long-term supply contracts that lack escalation clauses. Inventory buffers cushion shocks but inflate working-capital needs. Forward contracts and dual-sourcing strategies are gaining traction among risk-averse buyers.

Segment Analysis

By Product Type: Coagulants Extend Leadership

Coagulants and flocculants represented 23.78% of the China water treatment chemicals market share in 2024, a position secured through indispensable use in primary clarification and nutrient removal. Aluminum-based formulations dominate municipal lines for low-turbidity raw water, whereas iron-based variants capture phosphorus in industrial run-off. The China water treatment chemicals market size attributable to coagulants is projected to expand at an 8.90% CAGR, spurred by tighter effluent criteria and microplastic abatement initiatives.

High-charge PAC grades reduce sludge volume, curbing downstream disposal costs and encouraging upgrades in aging plants. Polyacrylamide copolymers customized for high-salinity matrices now command premium pricing in oil-and-gas water flooding and mining tailings. Suppliers coupling laboratory jar-testing with on-site performance validation raise switching barriers and secure multi-cycle replenishment contracts.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Cooling Systems Sustain Prime Demand

Cooling water treatment retained 32.16% of the China water treatment chemicals market in 2024, underpinned by coal-fired power and petrochemical clusters that rely on large evaporative towers. Adoption of closed-loop configurations elevates the need for long-life corrosion inhibitors and bio-dispersion aids that perform at higher cycles of concentration. The China water treatment chemicals market size for cooling treatments is slated to maintain solid momentum as data-center capacity and coastal LNG terminals proliferate. Suppliers that combine digital corrosion monitoring with predictive dosing algorithms are reporting double-digit service revenue growth.

Green water treatment, the fastest-growing application at a 9.12% CAGR, merges chemical oxidation, membrane separation, and nutrient recovery to align with circular-economy metrics. Industrial parks piloting phosphorus and ammonia capture now leverage specialty coagulants, catalysts, and regenerable ion-exchange resins to recover saleable by-products.

By End-User Industry: Municipal Sector Commands Volume

Municipal utilities accounted for 40.89% of the Chinese water treatment chemicals market in 2024, reflecting nationwide WWTP density and continuous upgrade mandates. Nutrient-focused regulations push uptake of biological process accelerators and metal-salt precipitating agents. The China water treatment chemicals market share held by municipalities is expected to rise further as rural wastewater programs scale under equal-access policies. Operators value turnkey supply frameworks that bundle sludge-reduction enzymes, odor control biocides, and cloud-based dosing dashboards.

Power generation is driven by coal retrofits and nuclear build-outs that impose stringent steam-cycle purity criteria. Chemical manufacturing plants are installing advanced oxidation and ion-exchange systems to stay ahead of GB 8978-2020 deadlines, boosting demand for peroxide activators and chelating agents. Mining sites expand application breadth, employing neutralizers to manage acid-mine drainage alongside flocculants for tailings water recovery. Commercial complexes, data campuses, and public institutions adopt Legionella-control packages as building-code revisions spotlight occupant safety, sustaining incremental growth across the non-industrial tier.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Eastern manufacturing corridors are anchored by the Yangtze River Delta’s petrochemical and electronics base. Jiangsu achieved 92.4% Grade III water compliance, necessitating continuous chemical dosing optimization. Northern regions, notably Beijing-Tianjin-Hebei and Inner Mongolia, show accelerated uptake due to data-center clustering and power-plant additions. Severe groundwater depletion on the North China Plain propels industrial water-reuse schemes that intensify chemical demand.

Western provinces welcome migration of compute load under the Eastern Data, Western Compute initiative, yet water scarcity favors hybrid and air-cooling configurations, moderating volume growth. Southern provinces, led by Guangdong and Fujian, maintain steady demand as lithium-battery and electronics manufacturers embrace ZLD mandates. Pearl River Delta municipalities invest in advanced nutrient-removal plants that rely on high-basicity coagulants and denitrifying biochemicals.

Central China benefits from policy-driven industrial relocation, creating fresh opportunities for standardized chemical packages that balance performance, cost, and regulatory certainty. The national water-network build-out, due by 2035, is expected to redistribute supply lines and stimulate chemical uptake in presently underserved basins.

Competitive Landscape

The China water treatment chemicals market features moderate fragmentation. Ecolab, Kemira, and SUEZ retain technology leadership via proprietary polymers, anti-scalants, and real-time monitoring platforms. Domestic specialists such as Shandong Taihe and Jiyuan Qingyuan scale production capacity to leverage cost advantages and provincial incentive policies. Suppliers offering quantifiable greenhouse-gas savings gain a bidding advantage. Service-based revenue models, including subscription dosing with performance guarantees, are gaining traction as buyers seek predictable budgets amid raw-material volatility. Overall, the competitive environment rewards firms that integrate chemical expertise with real-time analytics and holistic water-management consulting.

China Water Treatment Chemicals Industry Leaders

-

Kemira

-

Dow

-

Ecolab

-

SNF

-

Veolia

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2024: Ecolab completed a USD 50 million acquisition of Barclay Water Management, adding the iChlor monochloramine line to its municipal portfolio.

- September 2023: SUEZ signed two contracts in Chongqing to enhance potable-water resilience and waste recovery, supporting China’s 2060 carbon-neutrality goal.

China Water Treatment Chemicals Market Report Scope

Water treatment chemicals are used in the process of treating water and using it for applications such as drinking, cooking, irrigation, and industrial purposes. The process involves both physical and chemical methods. The substances removed during water treatment are suspended solids, viruses, fungi, bacteria, algae, and minerals. The China water treatment chemicals market is segmented by product type, application, and end-user industry. By product type, the market is segmented into biocides & disinfectants, coagulants & flocculants, corrosion & scale inhibitors, defoamers & defoaming agents, pH adjusters & softeners, and other product types. By application, the market is segmented into boiling water treatment, cooling water treatment, membrane treatment, green water treatment, raw water/potable water preparation, and wastewater treatment. By end-user industry, the market is segmented into commercial and institutional, power generation, chemical manufacturing, mining & mineral processing, municipal, and other end-user industries. Each segment's market sizing and forecast are based on revenue (USD million).

By Product Type

| Coagulants and Flocculants |

| Defoamer and Defoaming Agent |

| Corrosion and Scale Inhibitors |

| Biocides and Disinfectants |

| pH Adjuster and Softener |

| Other Product Types |

By Application

| Boiler Water Treatment |

| Cooling Water Treatment |

| Membrane Treatment |

| Green Water Treatment |

| Raw/Potable Water Preparation |

| Wastewater Treatment |

By End-user Industry

| Commercial and Institutional |

| Power Generation |

| Chemical Manufacturing |

| Mining and Mineral Processing |

| Municipal |

| Other End-user Industries |

| By Product Type | Coagulants and Flocculants |

| Defoamer and Defoaming Agent | |

| Corrosion and Scale Inhibitors | |

| Biocides and Disinfectants | |

| pH Adjuster and Softener | |

| Other Product Types | |

| By Application | Boiler Water Treatment |

| Cooling Water Treatment | |

| Membrane Treatment | |

| Green Water Treatment | |

| Raw/Potable Water Preparation | |

| Wastewater Treatment | |

| By End-user Industry | Commercial and Institutional |

| Power Generation | |

| Chemical Manufacturing | |

| Mining and Mineral Processing | |

| Municipal | |

| Other End-user Industries |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the China water treatment chemicals market?

The market is valued at USD 7.11 billion in 2025 and is forecast to reach USD 10.48 billion by 2030.

Which segment holds the largest China water treatment chemicals market share?

Cooling water treatment leads with a 32.16% share in 2024, driven by power and petrochemical demand.

Why are coagulants growing rapidly in China?

GB 8978-2020 discharge limits and microplastic removal goals push utilities and industries toward high-efficacy coagulant and flocculant formulations.

How do zero-liquid-discharge rules affect chemical demand?

ZLD mandates in lithium-battery hubs require specialty antiscalants, pH adjusters, and crystallization aids that lift chemical consumption per unit of wastewater.

What impact does carbon pricing have on end-user budgets?

Inclusion of cement, steel, and aluminum in China's ETS adds 3-5% to treatment-chemical budgets, incentivizing low-carbon chemical solutions.

Page last updated on: