GCC Fruit And Vegetable Market Analysis by Mordor Intelligence

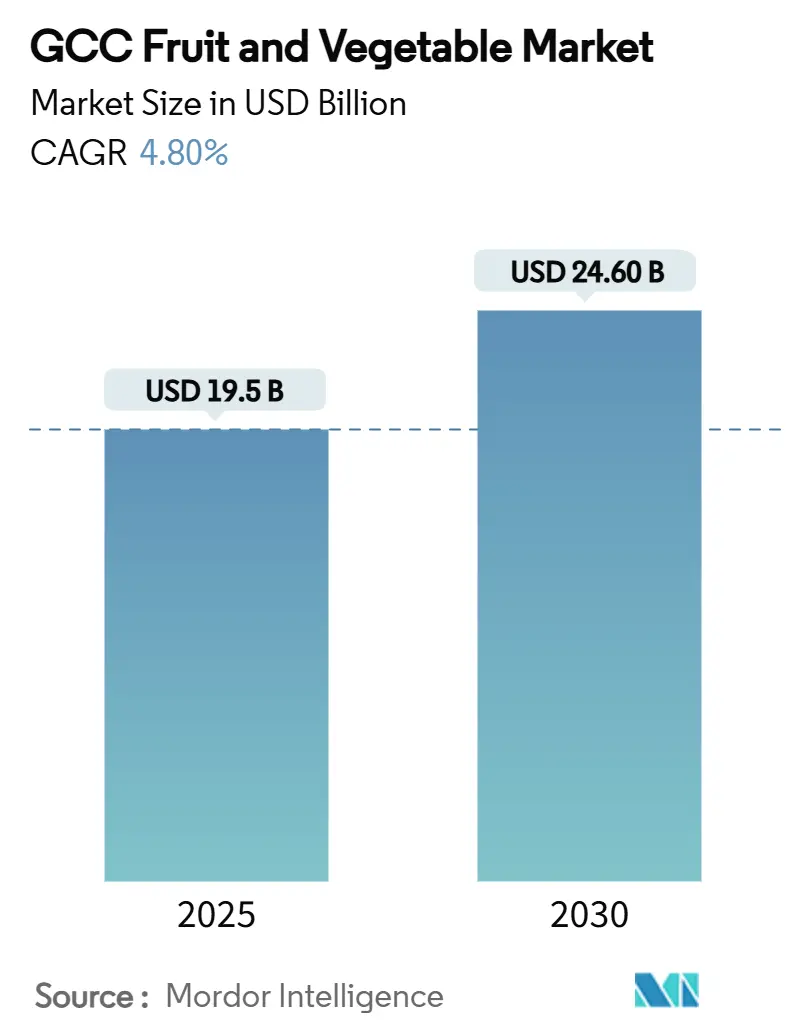

The GCC fruit and vegetable market size reached USD 19.5 billion in 2025 and is anticipated to grow to USD 24.6 billion by 2030, registering a CAGR of 4.8% during the forecast period. Gulf governments are shifting their food policies toward domestic production technologies to reduce import dependence and strengthen their balance of payments. Saudi Arabia's USD 2 billion agriculture fund and the United Arab Emirates's Food Tech Valley are investing in controlled-environment farming facilities that produce pesticide-free crops while optimizing water usage. The implementation of hydroponic and drip irrigation systems has decreased water consumption per unit and enabled year-round production, reducing reliance on imports. Cold-chain infrastructure developments, such as RSA Cold Chain's 40,000-pallet facility in Dubai, are reducing post-harvest losses and creating new re-export opportunities to Asian and European markets. The market is fragmented, with major stakeholders such as Pure Harvest Smart Farms integrating agricultural technology to achieve market consolidation, vertical integration, and technological differentiation.

Key Report Takeaways

- By geography, Saudi Arabia led with 53.8% of the GCC fruit and vegetable market size in 2024, while the United Arab Emirates is forecast to expand at a 5.1% CAGR through 2030.

GCC Fruit And Vegetable Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Widespread adoption of drip and hydroponic systems across GCC farms | +1.1% | United Arab Emirates and Saudi Arabia lead regional uptake | Medium term (2-4 years) |

| Government-backed agri-parks and food-security funds | +0.9% | Saudi Arabia, United Arab Emirates, and Qatar | Long term (≥ 4 years) |

| Expansion of cold-chain logistics reducing post-harvest losses | +0.7% | Distribution hubs in the United Arab Emirates and Saudi Arabia | Short term (≤ 2 years) |

| Rapid growth of Controlled-Environment Agriculture (CEA) greenhouses | +0.8% | United Arab Emirates, Saudi Arabia, and Oman | Medium term (2-4 years) |

| Surge in institutional buyers sourcing locally | +0.5% | GCC-wide | Short term (≤ 2 years) |

| Carbon-border-adjustment pressures favoring regional produce | +0.3% | Exporters with Europe exposure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Widespread Adoption of Drip and Hydroponic Systems Across GCC Farms

Hydroponic adoption at scale is transforming resource efficiency in the GCC fruit and vegetable market. Bustanica's 30,658 m² vertical farming facility produces 1 million kg of leafy greens annually while saving 250 million liters of water, reducing water usage by 95% compared to conventional farming[1]Source: Gulfood Green, “World’s Largest Vertical Farm Opens in Dubai,” gulfoodgreen.com. Saudi Arabia's Dava Agricultural Co. demonstrates similar progress through its 107-hectare greenhouse complex, which exports tomatoes to Europe, establishing the commercial feasibility of desert-grown fresh produce exports. The integration of AI-driven nutrient dosing, automated climate control, and cloud analytics helps reduce production costs to compete with imports. Government policies support this transition through water conservation subsidies and, integration of hydroponics into national food security strategies.

Government-Backed Agri-Parks and Food-Security Funds

Saudi Arabia allocated USD 2 billion for agriculture in 2025, representing a 67% budget increase focused on precision greenhouses, variable-rate irrigation, and agricultural robotics. The United Arab Emirates's Food Tech Valley has generated over 300 products through its integrated framework of startups, investors, and research institutes. Oman aims to improve food self-sufficiency by implementing AI-based crop planning and satellite imagery to transform individual farms into connected agricultural clusters. These integrated approaches minimize investment risks and facilitate technology adoption among medium-sized farms, supporting growth in the GCC fruit and vegetable market.

Expansion of Cold-Chain Logistics Reducing Post-Harvest Losses

Post-harvest losses have historically reduced fruit and vegetable value along Gulf trade corridors. RSA Cold Chain's distribution center in Jebel Ali provides 40,000 pallet positions with temperature control capabilities down to -25 °C, enabling same-day cross-docking operations to the Middle East and North Africa (MENA) and South Asia. The facility's predictive maintenance systems identify compressor issues before temperature variations occur, while its routing software coordinates truck arrivals with warehouse dock availability. These operational improvements reduce product spoilage, decrease cash cycles, and strengthen the GCC fruit and vegetable market value chain by channeling cost savings into competitive pricing and expanded product selection.

Rapid Growth of Controlled-Environment Agriculture (CEA) Greenhouses

Vertical and net-house farms are establishing regional supply networks in climate-challenging regions. The United Arab Emirates aims to increase vertical farming operations within five years to achieve water-neutral production in the GCC fresh produce market. Plenty Unlimited has allocated USD 680 million for strawberry vertical farming facilities in Abu Dhabi, targeting an annual production of 2 million kg, with Mawarid Holding as co-financier. Field trials demonstrate that cucumber production in Omani net houses exceeds traditional United Arab Emirates greenhouse yields while reducing energy consumption through solar-powered climate control systems. The economic benefits include higher margins from premium produce varieties, reduced transportation costs, and consistent supply management.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Saline-ground-water and limited arable land | -0.8% | Highest in Bahrain and Kuwait | Long term (≥ 4 years) |

| High energy cost of desalinated irrigation water | -0.6% | Saudi Arabia, United Arab Emirates, and Oman | Medium term (2-4 years) |

| Price volatility in global spot markets | -0.5% | GCC-wide | Short term (≤ 2 years) |

| Fragmented smallholder farm structure limiting economies of scale and bargaining power | -0.4% | Rural pockets across the GCC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Saline-Ground-Water and Limited Arable Land

The Gulf region's renewable water resources primarily support agriculture, limiting the capacity to mitigate increasing salinity levels. Bahrain's limited land mass and brackish aquifers necessitate substantial food imports[2]Source: Middle East Institute, “Building a More Resilient Bahrain,” mei.edu. Kuwait's agricultural studies demonstrate that salinity constrains crop selection, even though certain varieties achieve efficient water usage. While moisture-retention technologies such as stearic-acid-coated sand show promise, they have not reached commercial viability. The GCC fruit and vegetable market growth remains constrained by saline intrusion into farmland, a challenge that will persist unless desalination becomes more cost-effective.

Price Volatility in Global Spot Markets

Despite the expansion of Gulf farms, the region continues to rely heavily on imported fruits and vegetables, linking retail prices to global market fluctuations. Weather-related disruptions in supplier countries result in rapid price increases across the Gulf Cooperation Council (GCC) supermarkets. While vertical farming provides some protection against supply volatility, its higher operational costs cannot be fully absorbed, creating margin risks for retailers. Exchange rate fluctuations against the euro and Indian rupee further complicate pricing, making risk management expensive for small-scale distributors.

Geography Analysis

Saudi Arabia accounts for 53.8% of the GCC fruit and vegetable market share in 2024, primarily driven by its date production. The Ministry of Environment, Water, and Agriculture reports that Saudi dates are essential to the Kingdom's food security, with domestic production surpassing 1.9 million metric tons in 2024. The country's market position is strengthened by extensive land availability and subsidized water access, which reduces barriers for greenhouse investments. The agriculture fund provides financial support for precision pollination equipment, reducing labor costs and increasing fruit and vegetable production. The country's greenhouse tomato exports to Europe demonstrate compliance with stringent phytosanitary standards, enhancing its presence in premium retail markets. The nation's selective self-sufficiency approach prioritizes crops suited to its climate and technological capabilities, while importing wheat and rice and developing export channels for high-margin fruits.

The United Arab Emirates is anticipated to achieve the highest growth rate at 5.1% CAGR through 2030, driven by vertical farming operations, including Bustanica, which produces 1 million kg of leafy greens annually. The National Food Security Strategy 2051 encompasses 38 initiatives, including energy recovery ventilation systems and advanced light-emitting diode (LED) technology, reducing production costs[3]Source: United Arab Emirates Government, “National Food Security Strategy 2051,” u.ae. The Plant the Emirates program aims to increase productive farms by 20% by 2030 and expand certified organic acreage by 25%. The country addresses its limited rainfall by combining solar photovoltaic systems with hydroponic facilities to reduce energy costs. This strategy, along with efficient port logistics, enables the United Arab Emirates to deliver fresh berries and herbs to European markets within 48 hours of harvest.

Oman's Vision 2040 focuses on implementing data analytics and IoT sensors to improve cucumber yields in net houses, exceeding the Gulf Cooperation Council (GCC) averages. The Million Date Trees Plantation program utilizes drone technology for canopy monitoring, enabling precise fertilization that reduces resource usage and supports climate goals. As economic feasibility improves, private investors are pursuing long-term land leases in interior regions where night temperatures are favorable for energy-efficient production. This strategy complements greenhouse operations near Sohar Port, where refrigerated shipments to India and East Africa help expand the GCC fruit and vegetable market by connecting major growth markets.

Recent Industry Developments

- October 2024: The Food Tech Valley, a government initiative in the United Arab Emirates, has established a 27-year agreement with Badia Farms, a hydroponic farming company backed by Gulf Islamic Investments (GII). Through this partnership, Badia Farms implements hybrid farming methods to grow high-quality fruits and vegetables throughout the year.

- July 2024: Plenty Unlimited partnered with Mawarid Holding to channel USD 680 million over five years into vertical strawberry farms across the GCC, starting with Abu Dhabi’s flagship site designed for 2 million kg annual output.

- July 2024: Ghitha Holding’s Al Ain Farms acquired Arabian Farms Investments for AED 240 million (USD 65.3 million), securing hydroponic assets in the United Arab Emirates and Saudi Arabia and extending the buyer’s downstream distribution reach.

- February 2024: Emirates Flight Catering finalized the full takeover of Bustanica, positioning the United Arab Emirates entity to supply more than 1 million kg of pesticide-free greens annually and secure ingredient pipelines for 225 million passenger meals.

GCC Fruit And Vegetable Market Report Scope

Fruits and vegetables are necessary supplements to the human diet as they provide essential nutrients for maintaining health.

The GCC fruits and vegetables market is segmented by Geography into the United Arab Emirates, Bahrain, Kuwait, Oman, Qatar, and Saudi Arabia. The report provides a detailed analysis of fruit and vegetable production (volume), consumption (value and volume), import (value and volume), export (value and volume), and price. It also offers market estimation and forecasts in value (USD) and volume (metric tons).

By Geography (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis)

| United Arab Emirates | Fruits |

| Vegetables | |

| Bahrain | Fruits |

| Vegetables | |

| Kuwait | Fruits |

| Vegetables | |

| Oman | Fruits |

| Vegetables | |

| Qatar | Fruits |

| Vegetables | |

| Saudi Arabia | Fruits |

| Vegetables |

| By Geography (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis) | United Arab Emirates | Fruits |

| Vegetables | ||

| Bahrain | Fruits | |

| Vegetables | ||

| Kuwait | Fruits | |

| Vegetables | ||

| Oman | Fruits | |

| Vegetables | ||

| Qatar | Fruits | |

| Vegetables | ||

| Saudi Arabia | Fruits | |

| Vegetables | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the GCC fruit and vegetable market by 2030?

The market is forecast to reach USD 24.6 billion by 2030, rising at a 4.8% CAGR.

Which country currently holds the largest share of the GCC fruit and vegetable market?

Saudi Arabia led with a 53.8% share in 2024, supported by strong greenhouse output and date production.

Why is vertical farming gaining traction across the Gulf?

Vertical farms, including Bustanica, deliver pesticide-free produce using 95% less water, aligning with national water conservation and food security goals.

How do cold-chain investments affect fruit and vegetable profitability?

Facilities such as RSA Cold Chain's 40,000-pallet hub cut post-harvest losses and enable rapid re-export, boosting margins for growers and distributors.

What is the main challenge slowing farm expansion in Bahrain and Kuwait?

High salinity levels in groundwater and limited arable land restrict large-scale cultivation, making these markets reliant on imports.

Page last updated on: