The US government’s decision to raise the fee for sponsoring an H-1B visa from roughly $4,000–$6,000 to $100,000 per application marks one of the most significant shifts in skilled immigration policy in decades.

What had been a predictable administrative process, became an immediate strategic variable, altering hiring math, project planning, and even family decisions for thousands of professionals. For companies that rely on cross-border expertise, the calculus of where and how to build teams changed overnight, with ripple effects certain to extend from Silicon Valley and Bengaluru to Toronto, Dublin, and Singapore.

For multinational firms, particularly in technology and consulting, this is not merely an immigration update. It is a strategic inflection point forcing leaders to rethink delivery models, workforce design, and geographic allocation of innovation capacity.

Why the US Government May Have Raised the Fee

Several strategic considerations appear to underpin the $100K surcharge.

- Protect Domestic Wages and Opportunities: By lifting the cost of each H-1B hire to six figures, the government is effectively discouraging mass recruitment of foreign mid-skill workers and nudging employers toward US graduates and re-skilling initiatives.

- Prioritize Exceptional Talent: The fee makes it economical only for top-tier specialist roles, aligning with a policy of prioritizing exceptional talent rather than large outsourcing cohorts.

- Generate Fiscal Revenue: Even at modest application volumes, a $100K surcharge yields billions in federal receipts helping fund workforce programs or offsetting immigration-related administration costs.

- Political Signaling: With an election cycle approaching, the move plays to constituencies concerned about job competition, while signaling toughness on immigration.

The American Immigration Council has long argued that H-1B holders complement rather than displace domestic workers, fueling innovation and consumption spillovers. The new surcharge risks unsettling that balance.

The key question is whether the innovation engine, domestic talent development, and policy calibration can absorb the shock or whether America will reduce its edge in the global war for high-skill labor.

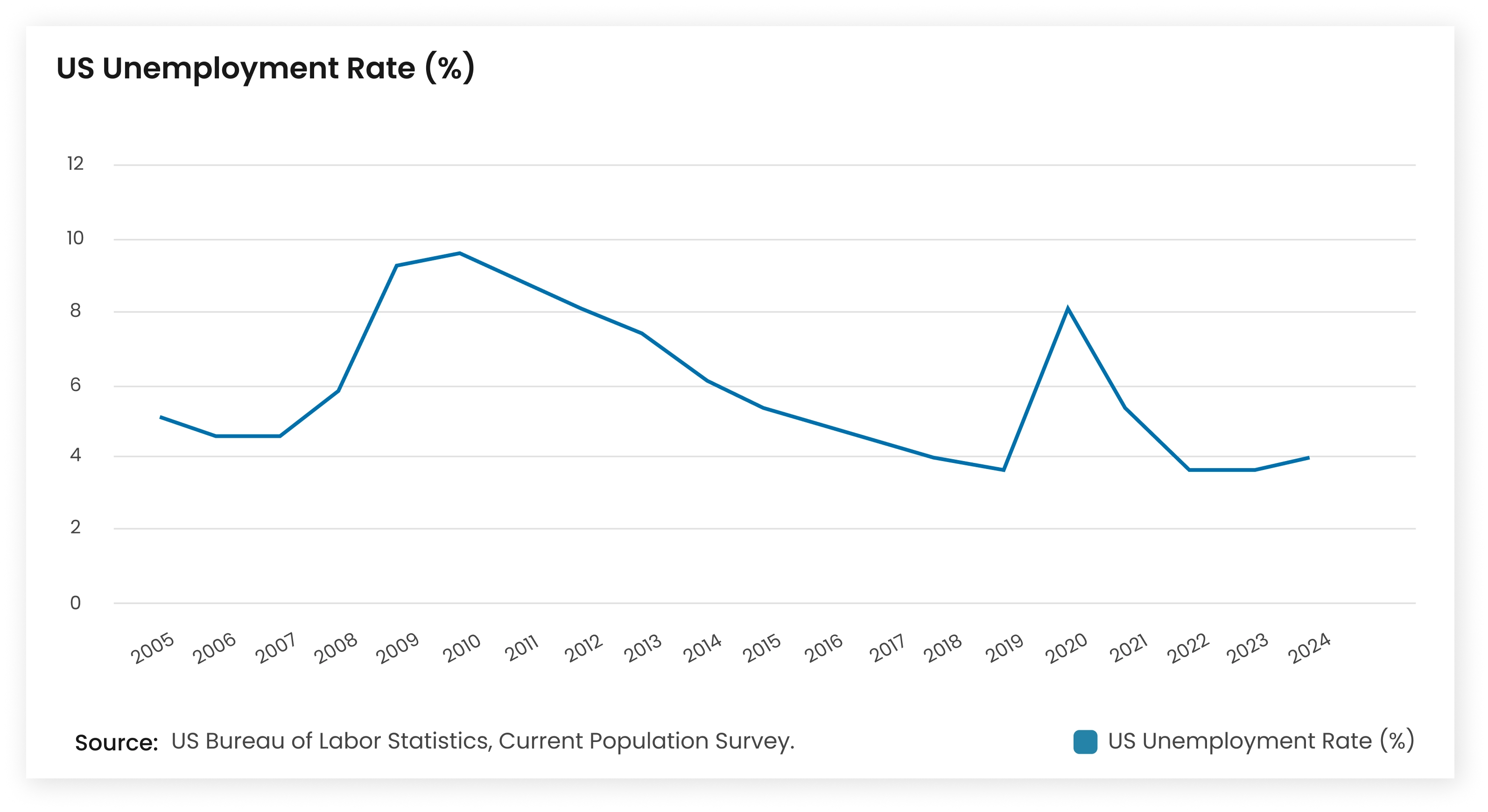

The US Labor Market Context

The US unemployment rate remains relatively low by historical standards, hovering around 4 percent in recent months. But this figure masks the employment shortages in high-skill domains.

In technology and STEM-heavy states, wage pressures, talent shortages, and competition for expertise have coexisted with moderate unemployment rates. The administration’s move reflects a belief that some skilled roles occupied by foreign workers can be brought back into domestic labor pools or at least made more expensive to outsource.

Raising visa costs may discourage outsourcing of mid-tier roles, but in domains where domestic pipelines are thin, the risk is that innovation slows just as global competition intensifies.

India’s Talent Pipeline at a Crossroads

India is at the center of this policy shift. Over two-thirds of all H-1B visa holders are Indian nationals in FY2024, far ahead of any other country. China was a distant second at 11.7%, and no other country exceeded 2%.

Country-Wise Share of H-1B Approvals in FY2024

| Country | Approved H-1B Beneficiaries (FY2024) | Share of Total |

| India | 283,397 | 71% |

| China | 46,680 | 11.7% |

| Philippines | 5,248 | 1.3% |

| Canada | 4,222 | 1.1% |

| South Korea | 3,983 | 1.0% |

| Mexico | 3,333 | <1% |

| All others | 41,470 | 10.4% |

| Total | 399,395 | 100% |

Source: U.S. Citizenship and Immigration Services (USCIS)

The Indian IT talent pipeline to the US is massive. For decades, Indian engineers and developers have been the invisible scaffolding of US technology growth from coding banking cores in New York to scaling AI models in Seattle. The $100K price tag rewrites that calculus overnight.

- Acceleration of Offshore Delivery: Indian IT majors have already cut US visa dependence to 3–5% of their global headcount. Now they might accelerate offshore delivery, keeping more projects in Bengaluru or Hyderabad where costs are lower and visas irrelevant.

- Growth of Global Capability Centers (GCCs): Multinationals may expand GCCs, the R&D and product hubs, in India rather than importing talent at six-figure costs.

- Potential Reverse Brain Drains and New Destinations: Skilled Indians who once queued for Silicon Valley may stay home or come back, strengthening India’s startup and AI ecosystems. Others may increasingly look to Southeast Asia and the Gulf, where growing tech hubs in Singapore, Dubai, and Riyadh are competing aggressively for talent with incentives and easier visa regimes.

H-1B Policy Reshapes IT in US and India

The $100,000 H-1B surcharge isn’t just a macro policy shift, it strikes at the heart of how global IT firms structure teams, parcel work across geographies, and leverage human capital arbitrage.

H-1B Visa Cost Surge: Strategic Impact on Indian IT and US Tech Firms

| India: Stress Test of Offshore Models | United States: Strategic Scarcity and Cost Inflation |

| Operational Model Shock: Indian IT majors have long relied on cross-border staffing, rotating engineers into US client sites under H-1B or L-1 visas. The $100k surcharge makes these rotations prohibitively expensive. | Dependence on Global Talent: US technology firms accustomed to drawing from overseas pipelines will adjust to both higher visa costs and reduced inflows of talent. |

| Shift to Offshore Delivery: Firms will accelerate domestic delivery arms and GCC expansion, keeping more work in major IT cities (Bengaluru, Hyderabad, and Pune). | Scarcity in Key Roles: Data science, AI, DevOps, and cybersecurity positions, already facing limited domestic supply, will see even fiercer competition. |

| Hybrid Engagement Models Rethought: Client projects once structured around US rotations will increasingly rely on remote or offshore-led engagement, reducing client-site presence. | Corporate Responses: Some firms might invest in internal training and local pipelines, others may explore alternative visa categories, while a subset may reduce headcount or delay projects. |

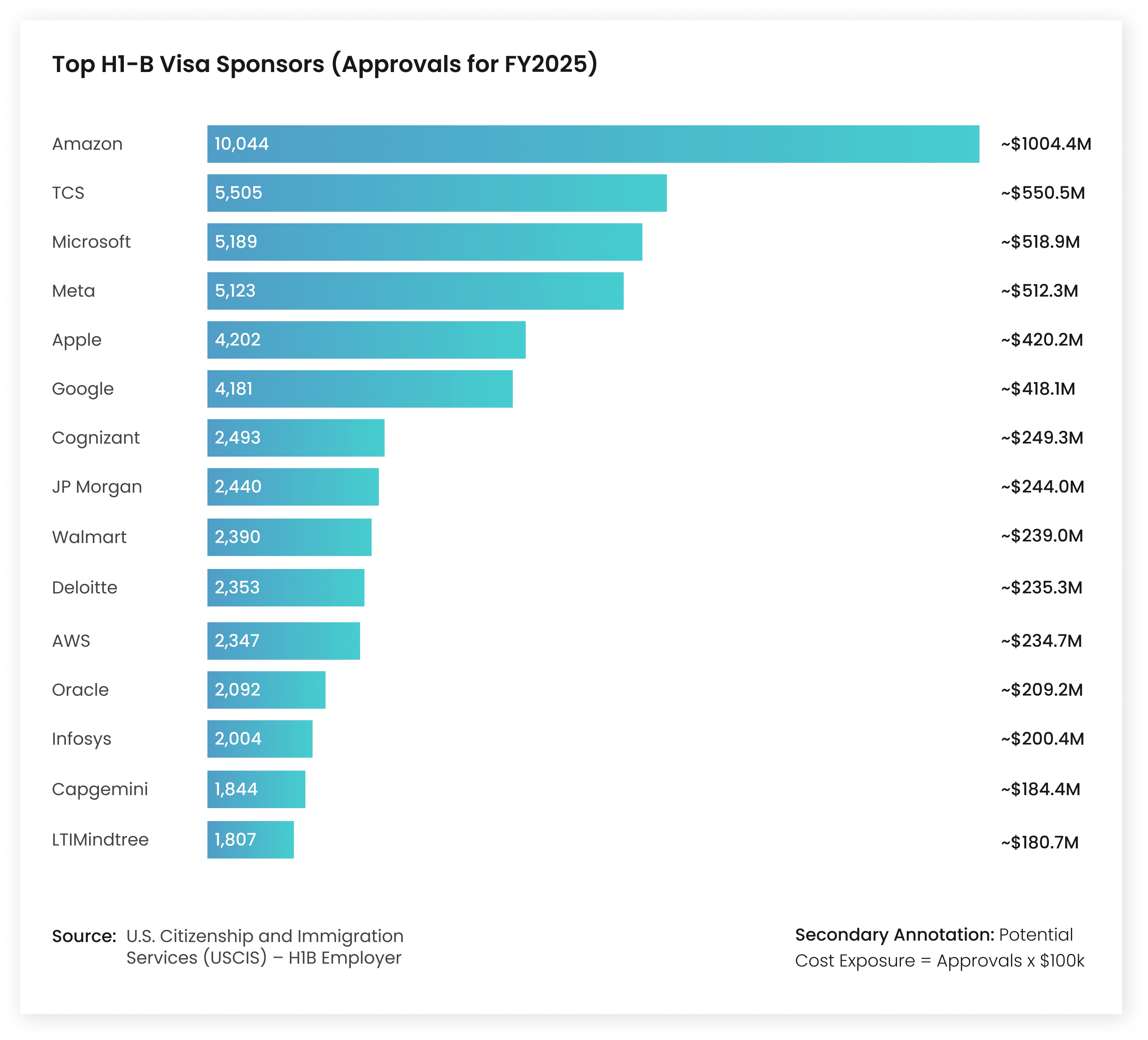

| Key Exposure (FY2025): TCS (5,505 approvals), Infosys (2,004), LTIMindtree (1,807), each now facing a six-figure cost per visa. | Key Exposure (FY2025): Amazon (10,044 approvals), Microsoft (5,189), Google (4,181), Deloitte (2,353), all directly exposed to doubled visa costs. |

| Strategic Implication: Indian firms will prioritize leaner offshore execution and specialized use of visas only for critical architecture and client leadership roles. | Strategic Implication: US firms may reprice project economics, reassess which roles are visa-worthy, and potentially scale back innovation capacity if domestic pipelines cannot fill gaps. |

Source: Mordor Intelligence

Impact on Global Technology Firms

The surcharge reshapes how leading employers manage talent. In FY2025, firms like Amazon (10,044 visas), Microsoft (5,189), and Google (4,181) were among the largest H-1B sponsors. Their margins, project pipelines, and innovation timelines now face direct exposure.

Corporate Playbook: Reinventing Global Delivery

The corporate response to this H-1B disruption is not mere retrenchment, it’s reinvention. Leading firms will transform their delivery architecture, decompose work, build toward automation, and reinvent the boundary between onshore and offshore operations. Those that cling to legacy rotation-heavy models may find themselves outpaced by more adaptive, leaner competitors.

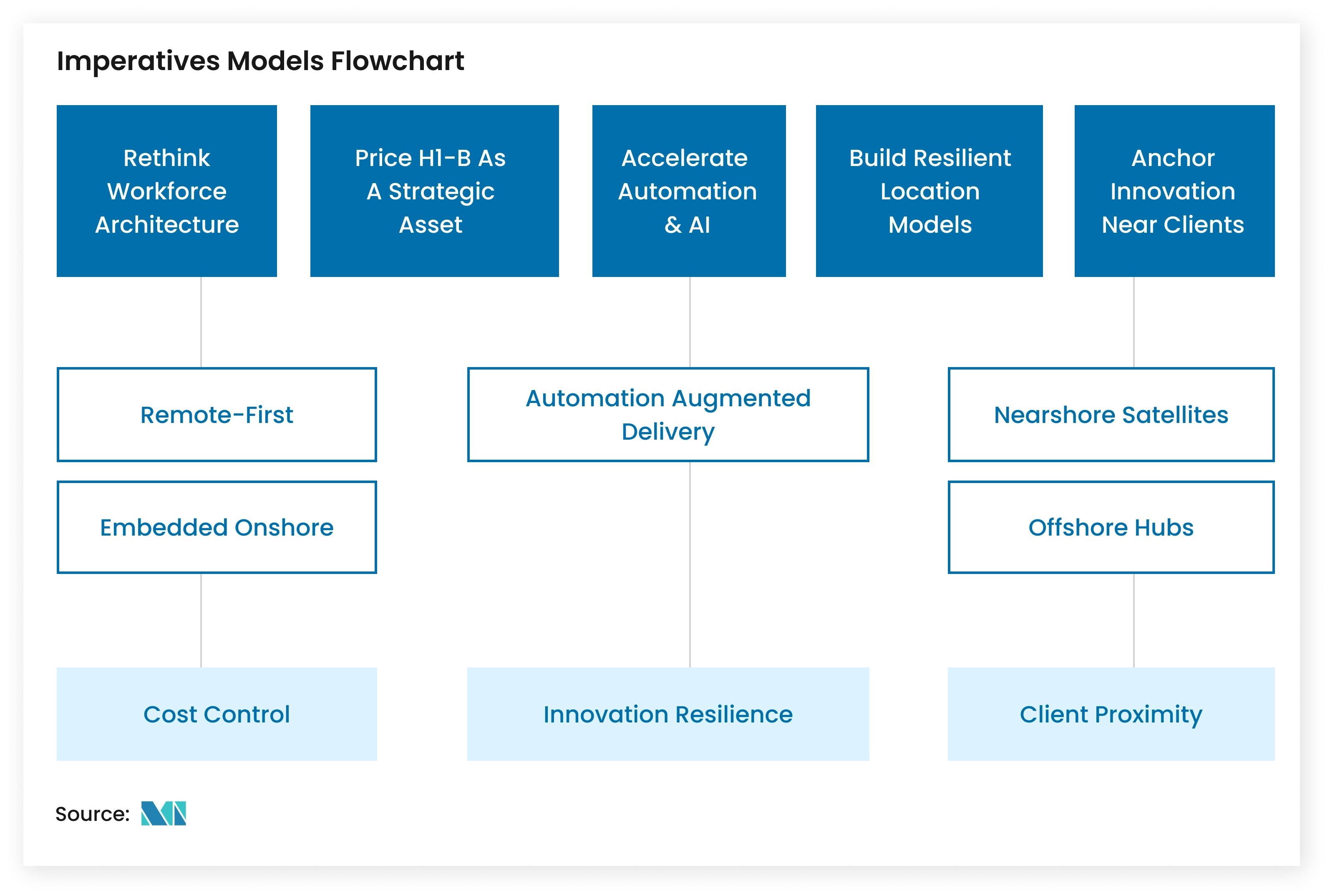

A. Five Strategic Imperatives

Future-Ready Workforce Strategies: Imperatives, Insights, and Actions

| Strategic Imperative | What It Means | Priority Actions |

| 1. Rethink Workforce Architecture | Redefine which roles truly require a US presence (client leaders, regulatory functions, frontier R&D) versus those that can be delivered offshore or nearshore. | • Classify all roles by visa sensitivity • Modularize projects to reduce reliance on onshore rotations • Strengthen Global Capability Centers (GCCs) for scale delivery |

| 2. Price H-1B as a Strategic Asset | Treat every visa sponsorship as a six-figure capital allocation decision with measurable ROI. | • Establish internal “visa ROI” dashboards • Reserve visas for high-impact, high-margin roles only • Escalate sponsorship decisions to the leadership level |

| 3. Accelerate Automation and AI Adoption | Reduce dependency on mid-tier roles most exposed to visa costs by embedding automation across delivery. | • Scale adoption of generative AI, low-code, and DevOps tools • Launch automation centers of excellence in offshore hubs • Incentivize engineers to embed productivity tools into delivery |

| 4. Build Resilient Location Models | Diversify geographic exposure to reduce over-reliance on a single visa regime or delivery hub. | • Expand nearshore hubs in Canada, Mexico, and Eastern Europe • Grow India-based GCCs with mandates beyond cost-saving, including R&D • Partner with boutique firms in client markets for flexibility |

| 5. Anchor Innovation Close to Clients | Retain client intimacy and IP control by maintaining a selective onshore innovation presence. | • Create micro-labs or satellite pods near major clients • Acquire or partner with niche firms in North America and Europe • Deploy hybrid teams that blend onshore leadership with offshore execution |

Source: Mordor Intelligence

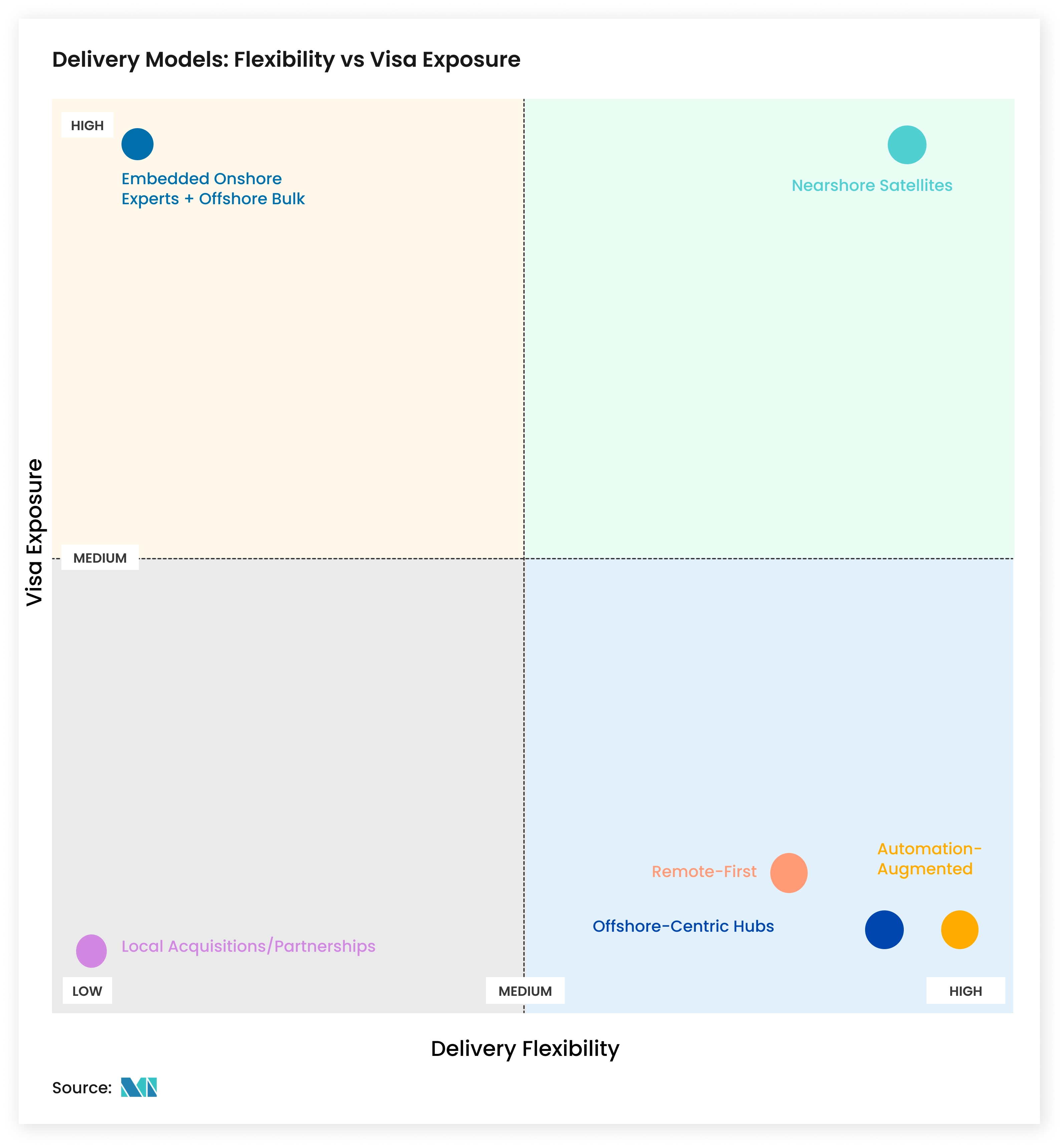

B. Delivery Models in Practice

Global Workforce Models: Strategic Options at a Glance

| Model | Essence | Key Upside | Main Risk |

| Offshore-Centric Hubs | Concentrate development and product engineering in India/Eastern Europe with minimal US rotation. | Lowest cost, no visa exposure, scale leverage. | Client proximity, regulatory compliance, time-zone management. |

| Remote-First Global Teams | Make virtual, distributed work the default. | Full geographic flexibility; bypasses visas entirely. | Culture cohesion, quality control, security compliance. |

| Embedded Onshore Experts + Offshore Bulk | Keep critical architecture/client roles in the US; shift bulk coding and support offshore. | Balances cost with on-site needs; uses visas sparingly. | Complex coordination; risk of delivery gaps if interfaces fail. |

| Satellite Nearshore Offices | Build small hubs in visa-friendly countries (e.g., Canada, Mexico, Poland) for quick client access. | Lower visa friction; near-time-zone advantage. | Setup cost, local legal hurdles, higher wages than India. |

| Micro-Delivery / Modular Projects | Break large projects into independent, offshore-executable modules. | Reduces on-site dependency; faster parallel delivery. | Requires strong architecture discipline and tight quality oversight. |

| Automation-Augmented Delivery | Use AI/low-code tools to cut human hours and team size. | Offsets labor cost; speeds execution. | Upfront investment; not all tasks are automatable; oversight risk. |

| Acquire or Partner with Local Boutiques | Buy or ally with US/Canada engineering shops to gain onshore talent. | Instant local presence and client trust. | Integration complexity; acquisition cost premium. |

Source: Mordor Intelligence

Conclusion: A $100K Inflection Point

The $100K H-1B surcharge is more than a cost hike, it is a strategic re-pricing of global talent flows. If the US successfully balances domestic workforce development with selective, high-value immigration, it may secure a stronger innovation base at home. If mismanaged, the move could cede ground to Canada, Europe, and a fast-strengthening Southeast Asia.

Either way, the visa that once powered decades of US tech leadership has entered a new era, one defined not by open pipelines but by precision hiring and borderless digital delivery. The next 24 months will reveal whether this bold experiment strengthens America’s innovation engine or becomes the most expensive self-imposed goal in the global war for talent.

Want deeper insights on how the $100K H-1B fee is reshaping global tech talent flows? Explore our latest IT Outsourcing Market Report.