Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

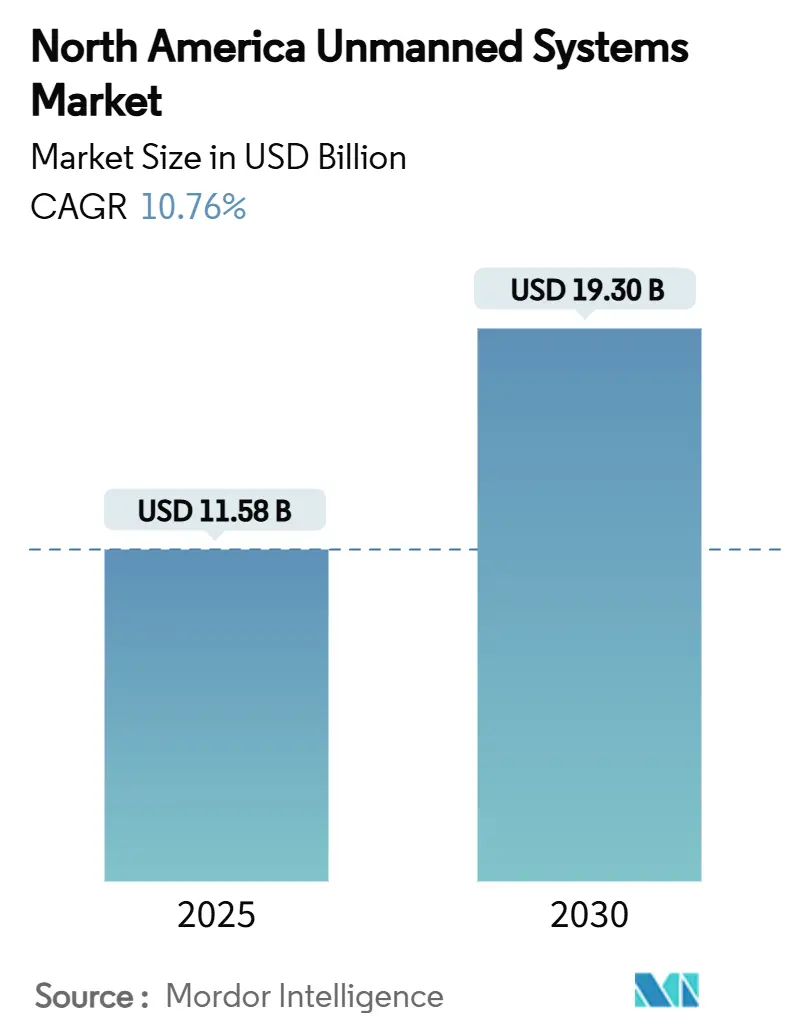

| Market Size (2025) | USD 11.58 Billion |

| Market Size (2030) | USD 19.30 Billion |

| Growth Rate (2025 - 2030) | 10.76% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Unmanned Systems Market Analysis by Mordor Intelligence

The North American unmanned systems market size stands at USD 11.58 billion in 2025 and is projected to advance to USD 19.30 billion by 2030, reflecting a solid 10.76% CAGR. Sustained defense procurement, rapid progress toward beyond-visual-line-of-sight (BVLOS) regulations, and falling autonomy costs continue to shape demand. The US Department of Defense’s USD 10.1 billion FY 2025 request for uncrewed platforms, Transport Canada’s BVLOS rules effective November 2025, and expanding drone-as-a-service offerings collectively increase addressable opportunities across military, civil, and commercial domains. Technology miniaturization and edge-AI integration lower total ownership costs, while supply-chain diversification efforts seek to mitigate chip shortages and foreign component risk. Privacy, data-governance fragmentation, and counter-UAS acquisition delays remain the principal headwinds to market scalability.

Key Report Takeaways

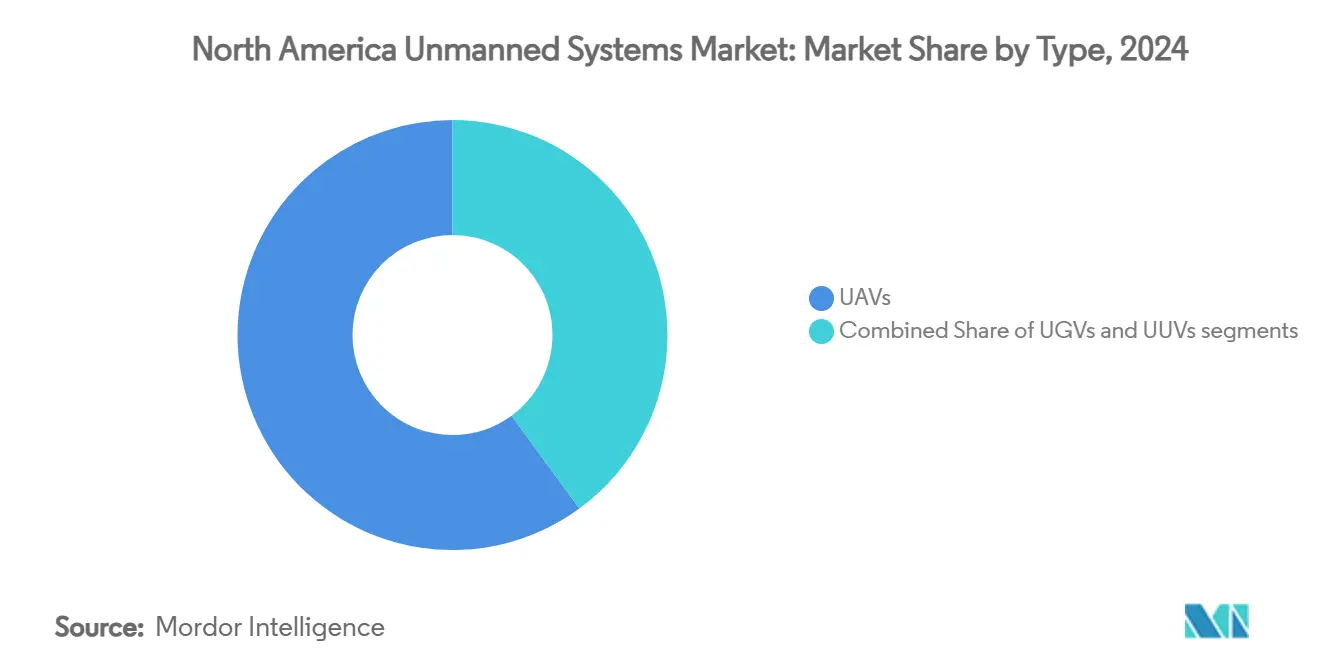

- By platform type, unmanned aerial vehicles led with 60.05% revenue share in 2024; unmanned aerial platforms also post the fastest growth at an 11.56% CAGR through 2030.

- By application, military ISR accounted for 41.28% of the North America unmanned systems market share in 2024, whereas commercial logistics and delivery are expected to climb at a 12.46% CAGR to 2030.

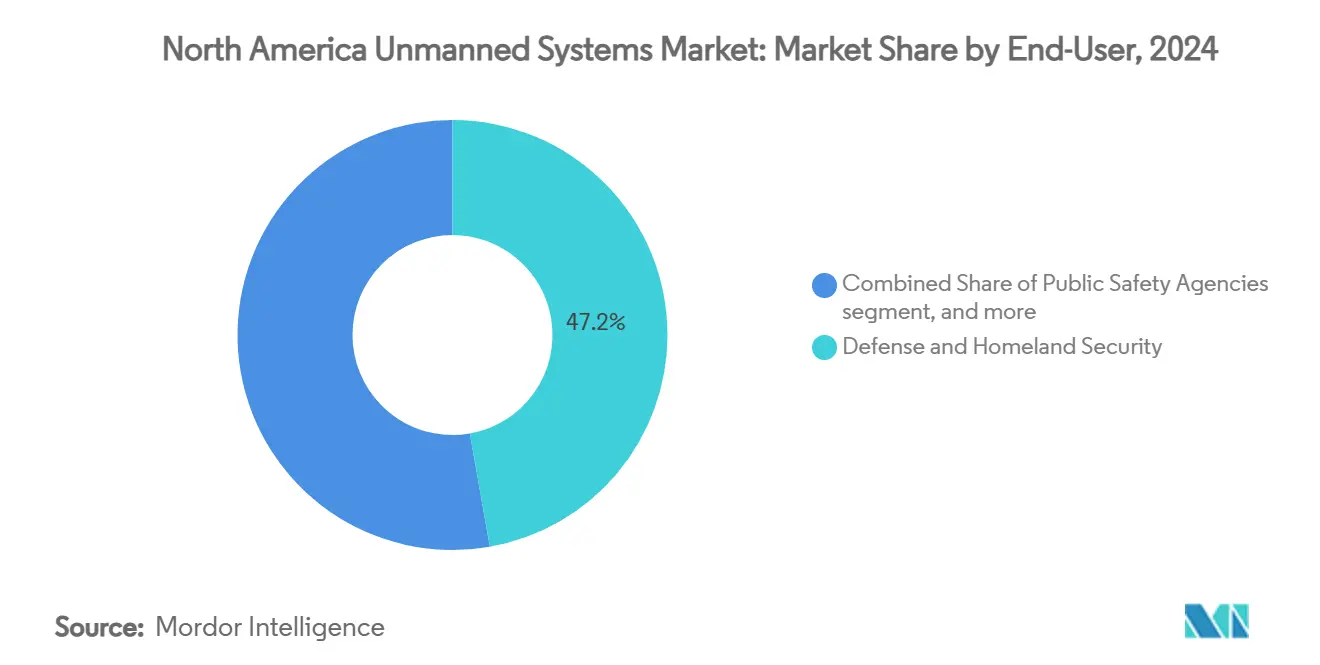

- By end-user, the defense and homeland security segment held 47.22% share of the North America unmanned systems market size in 2024, but service providers register the highest projected CAGR at 12.89% through 2030.

- By geography, the United States dominated with an 87.10% share in 2024, while Canada represents the fastest-growing country, advancing at an 11.12% CAGR to 2030.

North America Unmanned Systems Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-domain defense modernization accelerating unmanned systems procurement | +2.8% | United States defense installations | Medium term (2-4 years) |

| Commercial drone integration expanding across agriculture and logistics sectors | +2.1% | US farm belt, Canadian remote communities | Long term (≥ 4 years) |

| Regulatory progress enabling large-scale beyond-visual-line-of-sight operations | +1.9% | United States and Canada | Short term (≤ 2 years) |

| Cost reductions in AI autonomy and edge processing driving broader adoption | +1.7% | North America technology hubs | Medium term (2-4 years) |

| Rising demand for AUVs in offshore energy and subsea inspection missions | +1.2% | US Gulf Coast, Canadian offshore regions | Long term (≥ 4 years) |

| Public safety and emergency response agencies scaling drone-based operations | +0.9% | Urban centers across North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Multi-domain defense modernization accelerating unmanned systems procurement

Rising multi-domain requirements underpin robust US military spending, as illustrated by the USD 10.1 billion FY 2025 uncrewed-vehicle budget request, which is USD 1 billion higher than the prior year. Consolidated Army programs such as Future Tactical UAS and Launched Effects aim to boost cross-domain interoperability, while the Navy’s purchase of 49 additional unmanned surface vehicles underscores maritime demand growth. Investments exceeding USD 500 million in counter-drone systems reflect an evolving threat environment and reinforce fleet modernization priorities. The DoD’s Replicator program—tasked with fielding thousands of attritable autonomous aircraft—signals an accelerated shift toward large-volume, low-cost systems. These combined initiatives cement defense spending as the chief pillar supporting the North American unmanned systems market.

Commercial drone integration expanding across agriculture and logistics sectors

Registered commercial drones in the United States more than doubled between 2019 and 2024, reaching 842,000 units, and projections indicate a fleet of 1.1 million by 2028.[1]Verisk, “U.S. Commercial Drone Fleet Forecast,” verisk.com FAA approvals for multi-drone swarm operations enable a single pilot to command heavier payload platforms, widening agricultural use cases such as precision spraying and crop analytics. Logistics adoption follows suit—Walmart’s Dallas–Fort Worth operation already covers 1.8 million residents, and industry forecasts anticipate 808 million commercial drone deliveries annually by 2034. The synergy between agriculture and logistics drives producers like MightyFly to develop 100-pound-payload cargo drones capable of 600-mile missions. Together, these milestones validate expanding civilian demand in the North American unmanned systems market.

Regulatory progress enabling large-scale BVLOS operations

Congress has mandated the FAA to issue final BVLOS rules by March 2026, a milestone expected to remove today’s operational waiver bottlenecks. Canada advances even faster; Transport Canada’s regulations, effective November 2025, authorize routine BVLOS flights for aircraft up to 150 kilograms over sparsely populated zones.[2]Shield AI, “AI Pilot Completes Autonomous MQM-178 Flight,” shield.ai The coming FAA Part 108 framework shifts oversight toward corporate rather than individual credentials, streamlining approvals for logistics networks. Early adopters such as the Elk Grove Police Department already report more than 1,000 BVLOS missions, validating efficiency gains. Harmonization talks within ICAO aim to ensure North American rules align with forthcoming international standards, reinforcing regulatory clarity that benefits the North American unmanned systems market.

Cost reductions in AI autonomy and edge processing driving broader adoption

Advances in edge computing allow AI pilots to run locally, as demonstrated by Shield AI’s autonomous flights on the Kratos MQM-178 with onboard processing. Component miniaturization trims size, weight, and power requirements; eliminating a single pound from a drone is estimated to save USD 30,000 over its lifecycle. Deloitte projects parcel-delivery costs to fall from USD 60 to USD 4 per package by 2030, driven by AI navigation improvements and extended battery life. Defense initiatives such as Project Maven illustrate how automated video analytics shorten threat-detection cycles, underscoring the operational benefit of cheaper, smarter autonomy. Falling hardware and software costs expand the addressable user base throughout the North American unmanned systems market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inconsistent privacy and data governance regulations hindering scalability | -1.4% | United States and Canada | Medium term (2-4 years) |

| Sensor and chip supply-chain vulnerabilities impacting production timelines | -1.1% | Entire North America | Short term (≤ 2 years) |

| Delayed counter-UAS acquisitions slowing unmanned system fielding | -0.8% | US military installations, critical infrastructure sites | Short term (≤ 2 years) |

| Acoustic emission restrictions limiting underwater vehicle deployment | -0.3% | US and Canadian coastal waters, marine protected areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inconsistent privacy and data-governance regulations hindering scalability

Fragmented state-level privacy laws in the United States and differing federal-provincial rules in Canada increase compliance costs and constrain multi-jurisdictional operations. Community concerns about sensor-enabled surveillance complicate public safety deployments despite proven emergency-response gains. Unaligned data-retention mandates further restrict cross-border logistics flights and delay nationwide drone-as-first-responder programs. Until uniform standards emerge, governance uncertainty will weigh on expansion plans across the North American unmanned systems market.

Sensor and chip supply-chain vulnerabilities impacting production timelines

Semiconductor shortages, trade restrictions, and dependency on overseas suppliers threaten the timely delivery of high-performance processors and imaging sensors. The potential US ban on Chinese-origin drones illustrates the fragility of existing supply chains and forces manufacturers to re-engineer components. North Dakota’s state agency replacement scheme evidences operational disruption when non-compliant platforms must be retired. Companies are, therefore, investing in domestic fabs and multi-sourcing strategies; however, lead-time volatility is likely to persist into the near term and suppress output across the North American unmanned systems market.

Segment Analysis

By Type: Aerial Platforms Drive Market Leadership

Unmanned aerial vehicles (UAVs) held 60.05% of 2024 revenue and are forecast to expand at an 11.56% CAGR through 2030. Their dominance spans nano-class quadcopters for reconnaissance to large fixed-wing cargo drones such as MightyFly’s Cento, which carries 100 lbs across 600 miles.[3]MightyFly, “Cento Large Autonomous Cargo Drone Specifications,” mightyfly.com The North American unmanned systems market size for UAV applications primarily contributes to overall growth. Unmanned ground vehicles supplement battlefield logistics and explosive-ordnance disposal, while programs retrofitting Black Hawk helicopters for autonomous logistics illustrate how aerial autonomy permeates rotorcraft fleets.

Unmanned underwater vehicles (UUVs) record the smallest unit volumes but benefit from oil-and-gas inspection demand and naval interest in seabed domain awareness. Freedom AUV’s recent US Navy trials and Anduril’s Rhode Island production facility targeting 200 AUVs per year confirm rising subsea investment. Cross-domain technology transfer is increasing; sonar-enabled deep learning in UUVs and GPS-denied navigation in UAVs share AI algorithms, enabling platform convergence and reinforcing the North American unmanned systems market expansion.

Note: Segment shares of all individual segments available upon report purchase

By Application: Military Dominance Gives Way to Commercial Expansion

Military ISR missions generated 41.28% of 2024 revenue, underpinned by sustained federal budgets and border-security operations such as the Texas Department of Public Safety’s 51,674 drone flights. Yet commercial logistics and delivery are projected to outpace all other segments at a 12.46% CAGR to 2030, as BVLOS approvals and edge-AI efficiencies push unit economics toward profitability. The North American unmanned systems market size allocated to logistics platforms is set to rise sharply.

Agricultural and natural-resource management also registers rapid uptake after FAA permissions for swarm operations let one operator supervise multiple heavy-lift sprayers, triggering production scale-ups by US OEMs. Industrial inspection uses thermal, LiDAR, and hyperspectral payloads for infrastructure maintenance, while emergency-response agencies leverage BVLOS fleets to cut incident-arrival times. Across every end-use, onboard AI increasingly handles data fusion, enabling real-time insights that accelerate decision cycles.

By End-User: Service Providers Emerge as Growth Leaders

Defense and homeland-security customers controlled 47.22% of 2024 spending, buttressed by programs such as the Coast Guard’s cutter-based UAS roll-out and the Navy’s enlarged unmanned surface-vehicle fleet. However, drone-as-a-service operators exhibit the fastest growth trajectory at a 12.89% CAGR, indicating a shift toward subscription-based access that minimizes capital outlay for adopters. Their rise redefines the North American unmanned systems market, moving value capture from hardware sales to recurring services.

Public-safety agencies increasingly procure turnkey DFR (drone-as-first-responder) systems; Elk Grove’s citywide BVLOS authorization exemplifies operational maturity. Industrial firms in energy and telecom favor outsourced inspection contracts that bundle platform, pilot, analytics, and compliance support. In parallel, private security, surveying, and environmental-monitoring firms use similar service models, expanding market breadth.

Geography Analysis

The United States accounted for 87.10% of 2024 spending, anchored by the Department of Defense’s USD 10.1 billion budget, mature test-site infrastructure, and a pipeline of more than 200 M&A deals that accelerated domestic capability consolidation. Large-scale deployments span border security, parcel delivery, and emergency response, with one state agency fielding 368 aircraft and 325 pilots for border operations. The forthcoming FAA Part 108 BVLOS framework is expected to unlock commercial use cases further, sustaining the lead of the North America unmanned systems market in the United States.

Canada is projected to grow at an 11.12% CAGR to 2030, catalyzed by progressive BVLOS rules enacted in November 2025 and a CAD 2.5 billion Arctic RPAS procurement that begins production in 2025. The Calgary Police Service’s adoption of drones for traffic reconstruction and vast remote regions that benefit from unmanned logistics creates fertile ground for expansion. Harmonization dialogues with the United States aim to facilitate cross-border flights, integrating Canadian operators more tightly into the broader North America unmanned systems market.

Mexico remains nascent yet strategically important given its border with the United States and diverse terrain suited to precision agriculture, infrastructure inspection, and humanitarian response applications. Domestic regulations continue to evolve, but increasing media coverage of AI-enabled drones suggests rising stakeholder interest. As North American rules converge, Mexico is likely to tap into supply-chain synergies and service-provider models that have proven successful elsewhere in the region.

Competitive Landscape

Competition is fragmented on the civilian side but shows measured consolidation in defense niches, evidenced by more than 200 mergers and acquisitions transactions recorded in 2023. AeroVironment’s USD 4.1 billion acquisition of BlueHalo merged aerial vehicle expertise with electronic warfare assets, signaling a trend toward multi-capability portfolios.[4] AeroVironment, “AeroVironment to Acquire BlueHalo,” avinc.com Larger primes and venture-backed challengers compete to integrate edge AI and autonomy; Shield AI’s flight-proven software stack on Reaper-class aircraft highlights best-in-class performance.

Service-based players such as Ondas-Volatus leverage the Optimus System to provide persistent border-surveillance-as-a-service, illustrating alternative growth vectors beyond manufacturing. Anduril’s Rhode Island AUV plant, targeting 200 annual units, shows how vertical integration and scalable production can disrupt traditional naval suppliers. Supply-chain resilience now differentiates contenders; firms diversifying away from single-source chips gain bidding advantages on defense contracts that mandate domestic content.

Technological convergence, BVLOS compliance expertise, and robust supplier networks determine competitive standing. Companies that blend hardware, software, analytics, and regulatory services are positioned to capture recurring revenue streams and shape the future trajectory of the North America unmanned systems market.

North America Unmanned Systems Industry Leaders

-

Lockheed Martin Corporation

-

Teledyne FLIR LLC (Teledyne Technologies Incorporated)

-

L3Harris Technologies, Inc.

-

General Atomics

-

Northrop Grumman Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: Production commenced on MQ-9B Arctic-configured drones for Canada under a CAD 2.5 billion (USD 1.83 billion) contract, with first delivery slated for 2028.

- January 2025: The Canadian Commercial Corporation (CCC), a government-to-government contracting agency, received a USD 14 million contract from the United States Department of Defense (US DoD) to deliver QinetiQ's Vindicator uncrewed aerial vehicle (UAV) and associated services to the Naval Air Warfare Center Weapons Division (NAWCWD).

- January 2025: The US Air Force awarded Firestorm Labs a USD 100 million contract for its small unmanned aerial systems. Under this contract, the company will deliver its flagship drones, associated support services, and research and development work for multiple applications.

North America Unmanned Systems Market Report Scope

Unmanned systems are autonomous or remotely controlled robots that perform specific tasks. The North American unmanned systems market includes the procurement of unmanned aerial vehicles (UAV or UAS), unmanned ground vehicles (UGV), and unmanned sea systems (surface and underwater) used for commercial, military, and law enforcement applications.

The North American unmanned systems market is segmented by type, application, and geography. By type, the market is segmented into unmanned aerial vehicles, unmanned ground vehicles, and unmanned sea systems. By application, the market is divided into civil and law enforcement, and the military. The report also covers the market sizes and forecasts for the North American unmanned systems market in two countries across the region. For each segment, the market sizing and forecasts were made based on value (USD).

By Type

| Unmanned Aerial Vehicles (UAVs) |

| Unmanned Ground Vehicles (UGVs) |

| Unmanned Underwater Vehicles (UUVs) |

By Application

| Military ISR |

| Civil and Law-Enforcement |

| Commercial Logistics and Delivery |

| Agriculture and Natural-Resources |

| Industrial Inspection and Maintenance |

By End User

| Defense and Homeland Security |

| Public Safety Agencies |

| Enterprise and Industrial Operators |

| Service Providers (Drone-as-a-Service) |

By Geography

| United States |

| Canada |

| Mexico |

| By Type | Unmanned Aerial Vehicles (UAVs) |

| Unmanned Ground Vehicles (UGVs) | |

| Unmanned Underwater Vehicles (UUVs) | |

| By Application | Military ISR |

| Civil and Law-Enforcement | |

| Commercial Logistics and Delivery | |

| Agriculture and Natural-Resources | |

| Industrial Inspection and Maintenance | |

| By End User | Defense and Homeland Security |

| Public Safety Agencies | |

| Enterprise and Industrial Operators | |

| Service Providers (Drone-as-a-Service) | |

| By Geography | United States |

| Canada | |

| Mexico |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the North America unmanned systems market?

The market is valued at USD 11.58 billion in 2025.

How fast is the market expected to grow?

It is forecasted to rise at a 10.76% CAGR, reaching USD 19.30 billion by 2030.

Which platform type dominates revenue?

Unmanned aerial vehicles (UAVs) lead with 60.05% of 2024 revenue and also post the quickest growth.

Why is Canada the fastest-growing country market?

Progressive BVLOS regulations effective November 2025 and Arctic surveillance programs underpin its 11.12% CAGR.

What restraints could slow adoption?

Varied privacy laws and semiconductor supply-chain vulnerabilities are the most significant short-term hurdles.

How are service-provider models reshaping demand?

Drone-as-a-service offerings allow customers to access hardware, pilots, and analytics on subscription terms, driving the highest end user CAGR at 12.89%.

Page last updated on: