Energy & Power

30th JulyUnlocking Market Potential for Solid-State Transformers

3 Min Read

The Portable Filtration System Market Report is Segmented by Product Type (Cart-Mounted Systems, Skid-Mounted Systems, Suction/Vacuum Portable Units, Drum-Top Filtration Kits, and Compact Mobile Trolley), End-User (Oil and Gas, Power Generation, Pulp and Paper, Metal and Mining, Food and Beverage, Marine and Shipbuilding, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

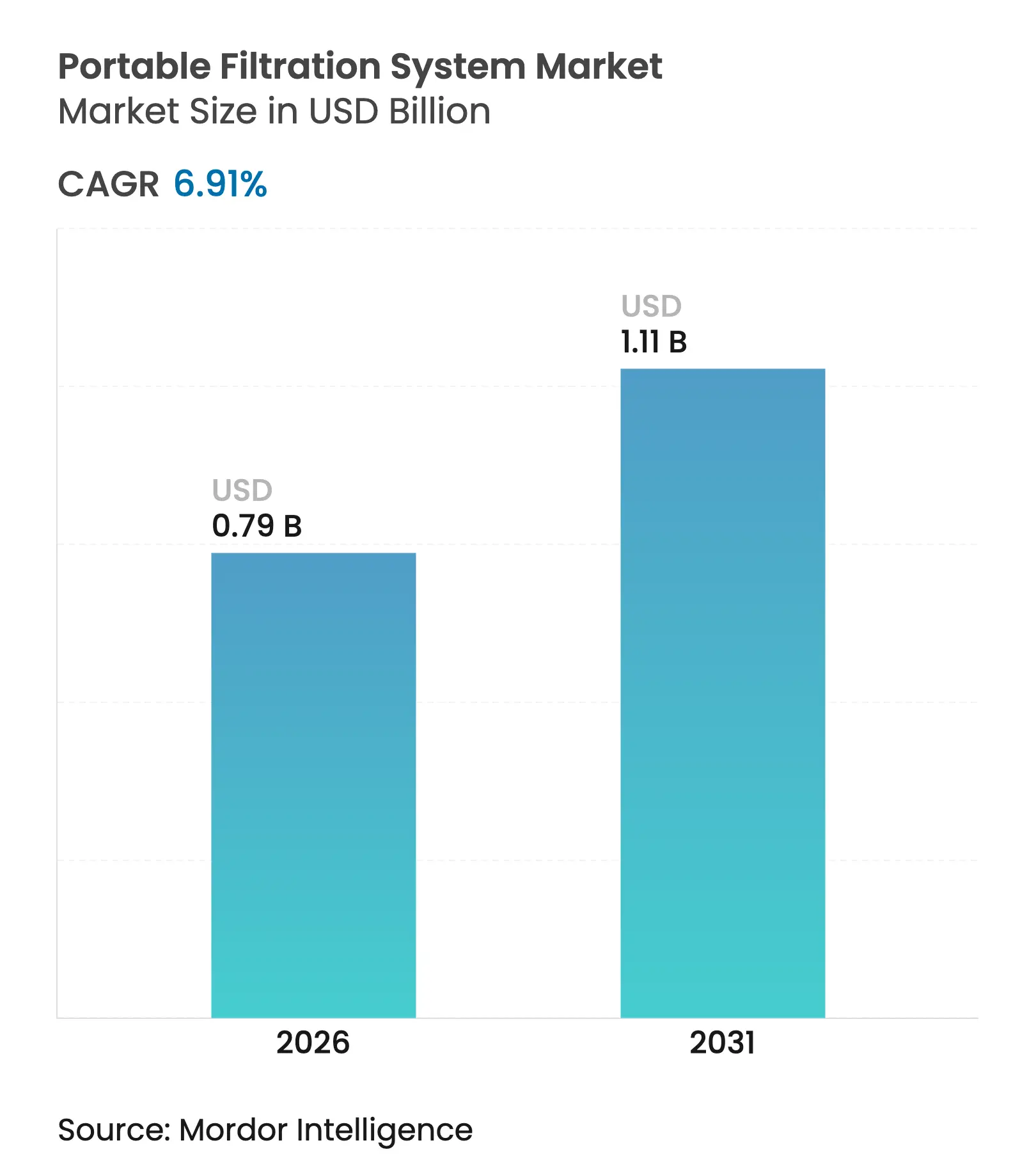

| Market Size (2026) | USD 0.79 Billion |

| Market Size (2031) | USD 1.11 Billion |

| Growth Rate (2026 - 2031) | 6.91 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Strong growth reflects a shift from reactive fluid maintenance to proactive contamination control strategies, which extend equipment life and reduce downtime. Industrial brownfield upgrades, tougher ISO 4406 cleanliness codes, and a growing preference for rental-based services acceleratethe adoption of mobile solutions across oil and gas, aerospace, marine, and power generation applications.[1]International Organization for Standardization, “ISO 4406: Hydraulic Fluid Cleanliness Codes,” iso.org Rising investment in predictive maintenance technologies further supports steady demand as operators align portable systems with data-driven service schedules.[2]Power & Motion, “AI-Driven Filtration Schedules,” powermotiontech.com

Key Report Takeaways

*Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising demand for contamination-free hydraulic & lube fluids in brownfield assets Rising demand for contamination-free hydraulic & lube fluids in brownfield assets | 1.20% | Global, North America & Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:1.20% | Geographic Relevance:Global, North America & Europe | Impact Timeline:Medium term (2-4 years) |

Increasing adoption of diesel & biodiesel fuels with higher particulate load Increasing adoption of diesel & biodiesel fuels with higher particulate load | 0.80% | APAC & Sub-Saharan Africa | Short term (≤ 2 years) | |||

Stricter ISO 4406 cleanliness codes in aerospace and defence MRO Stricter ISO 4406 cleanliness codes in aerospace and defence MRO | 1.10% | North America, Europe, APAC | Long term (≥ 4 years) | |||

Predictive-maintenance programmes boosting offline filtration retrofits Predictive-maintenance programmes boosting offline filtration retrofits | 0.90% | Global industrial hubs | Medium term (2-4 years) | |||

Growth of rental fleets for emergency fluid polishing services Growth of rental fleets for emergency fluid polishing services | 0.60% | North America, Europe, Gulf states | Short term (≤ 2 years) | |||

Surging mini-grid installations in Sub-Saharan Africa requiring mobile fuel filtration Surging mini-grid installations in Sub-Saharan Africa requiring mobile fuel filtration | 0.70% | Sub-Saharan Africa, rural APAC | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Demand for Contamination-Free Fluids in Brownfield Assets

Aging factories operate equipment beyond its original design limits, producing elevated particulate matter and water ingress that threaten hydraulic reliability. Operators deploy portable filtration carts to achieve ISO 18/16/13 targets without the need for costly plant overhauls.[3]Y2K Filtration, “Portable Filtration for Brownfield Plants,” y2kfiltration.com Single units can sequentially service multiple machines, maximizing capital use and trimming maintenance budgets. Brownfield sites also prefer portable solutions because they minimize production outages during fluid conditioning. High-efficiency elements now remove ≥99% of 4 µm particles, protecting pumps and valves from premature wear and tear. As a result, the portable filtration system market gains steady replacement demand each maintenance cycle.

Increasing Adoption of Diesel and Biodiesel Fuels with Higher Particulate Load

Tier IV engines operate at injection pressures exceeding 30,000 PSI, which forces fuel cleanliness toward the ISO 12/9/6 standards recommended by injector OEMs.[4]Bell Performance, “Fuel Cleanliness for Tier IV Engines,” bellperformance.com Biodiesel blends exacerbate the challenge by absorbing more water and promoting microbial growth, thereby accelerating filter blockage. Portable fuel polishers integrate coalescers and high-beta elements, achieving single-pass water removal above 99% while maintaining flow rates suitable for bunkering and bulk transfer. Renewable diesel adoption magnifies demand because biofuel stability varies under tropical storage conditions. This fuels an 8.3% regional CAGR in the Asia-Pacific portable filtration system market.

Stricter ISO 4406 Cleanliness Codes in Aerospace and Defence MRO

Modern aircraft hydraulics require ISO 15/13/10 or cleaner fluids to maintain servo-valve accuracy and ensure flight safety. Portable purifiers provide MRO facilities with the flexibility to treat fluids for multiple aircraft platforms without the need for permanent installations. Integrated particle counters verify cleanliness in real-time, reducing laboratory wait times and enabling same-shift sign-off. Military depots also deploy mobile units to austere field locations, sustaining mission readiness in remote theaters. These factors are expected to expand the portable filtration system market across defense corridors in North America, Europe, and Asia.

Predictive-Maintenance Programmes Boosting Offline Filtration Retrofits

Condition-monitoring sensors, combined with AI models, trigger filtration only when contamination trends exceed thresholds, reducing energy use by up to 96% compared to continuous-run systems. Portable skids fitted with telemetry send real-time data to maintenance hubs, supporting just-in-time service calls that minimize operator intervention. The approach transforms carts from reactive tools into intelligent assets that extend oil life and lower the total cost of ownership. Increased digitalization keeps the portable filtration system industry aligned with broader smart-factory investments.

*Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Slower CAPEX cycles in pulp & paper and mining sectors Slower CAPEX cycles in pulp & paper and mining sectors | -0.50% | Resource-dependent regions globally | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-0.50% | Geographic Relevance:Resource-dependent regions globally | Impact Timeline:Medium term (2-4 years) |

Emergence of self-cleaning inline filter skids Emergence of self-cleaning inline filter skids | -0.40% | North America, Europe, advanced hubs | Long term (≥ 4 years) | |||

High differential pressure losses in high-viscosity applications High differential pressure losses in high-viscosity applications | -0.30% | Global industrial sites | Short term (≤ 2 years) | |||

Import tariffs on filter media in South America Import tariffs on filter media in South America | -0.20% | Brazil & Argentina | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Slower CAPEX Cycles in Pulp & Paper and Mining Sectors

Commodity price swings prompt mills and mines to delay non-essential spending, which in turn limits orders for new filtration carts. Instead, plants extend filter life through ultrasonic cleaning or chemical regeneration, which cuts replacement frequency by up to 300% and reduces the immediate need for new equipment. Service-based offerings partly offset this drag, yet sluggish project pipelines shave 0.5 percentage points off the forecast CAGR for the portable filtration system market.

Emergence of Self-Cleaning Inline Filter Skids

Automated back-flush systems promise continuous operation with minimal labor, tempting sectors such as food processing to shift away from mobile carts. Although upfront investment is higher, reduced manual handling appeals to plants that run 24/7 lines. Portable solutions keep an edge in intermittent or multi-asset environments, but the growing installed base of self-cleaning units deducts 0.4 percentage points from long-term growth expectations.

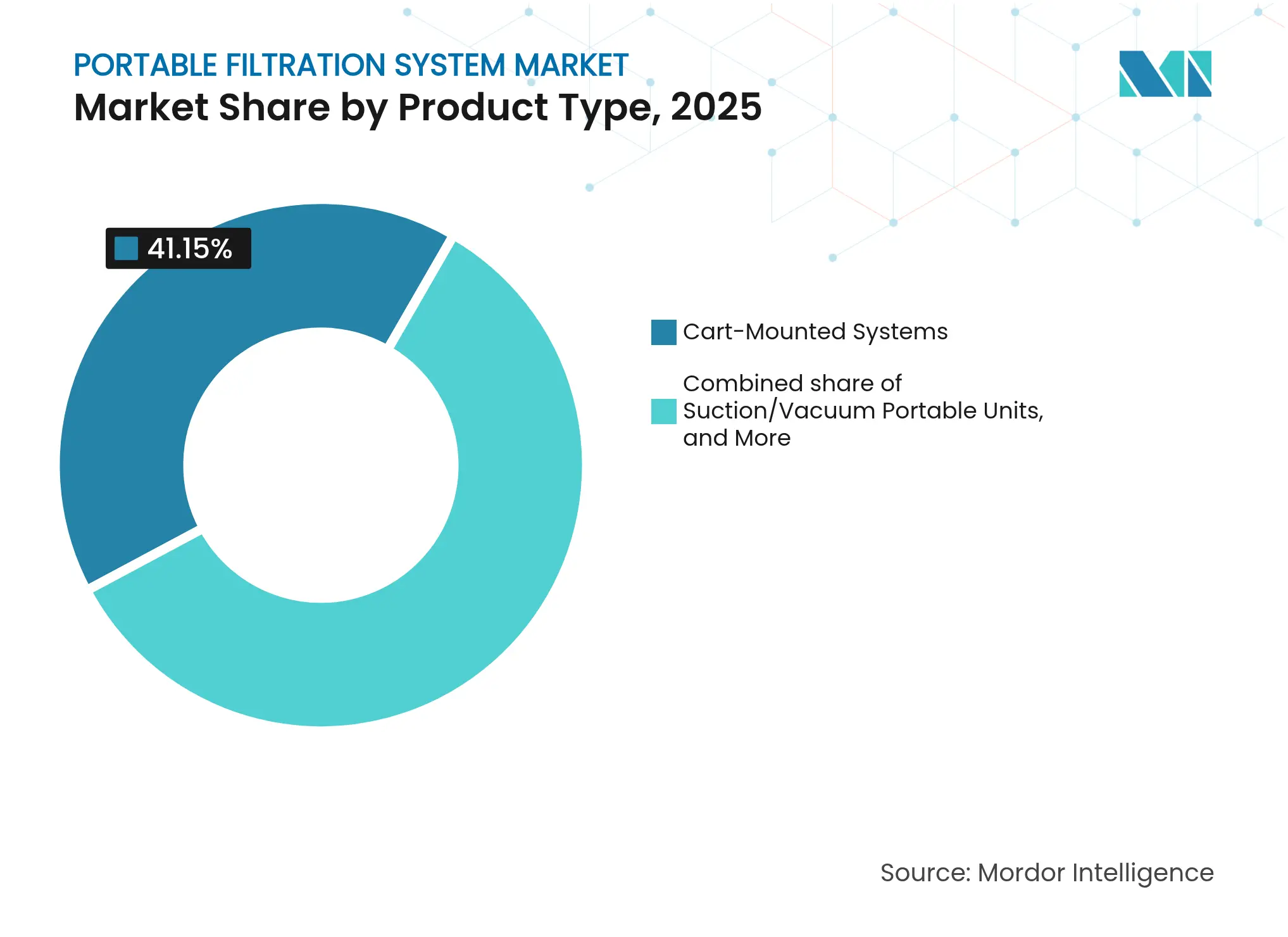

By Product Type: Cart-Mounted Systems Lead Despite Vacuum Innovation

Cart-mounted units held 41.15% of the portable filtration system market in 2025, driven by their proven versatility, ease of service, and extensive distributor networks. Suction/vacuum models, although smaller in installed base, are forecasted for a 8.72% CAGR, as their ability to handle high-viscosity oils without excessive differential pressure aligns with the needs of heavy-equipment maintenance. Integrated sensors and touchscreen controls transform newer carts into smart skids that log ISO codes during operation, enhancing traceability for aerospace and marine clients. The shift toward real-time data has raised average selling prices, while also enhancing value perception, cementing cart dominance even as vacuum technology gains traction.

Skid-mounted frames meet flow-rate demands of up to 400 L/min in refinery and power-plant settings where semi-permanent placement is feasible, while drum-top kits appeal to cost-sensitive workshops seeking quick oil recirculation during drum filling. Portable trolley units with narrow wheelbases serve space-constrained aircraft hangars and semiconductor fabs. Such diversification enables suppliers to address niche markets without straying far from core design principles, thereby supporting long-term stability in the portable filtration system market.

Note: Segment shares of all individual segments available upon report purchase

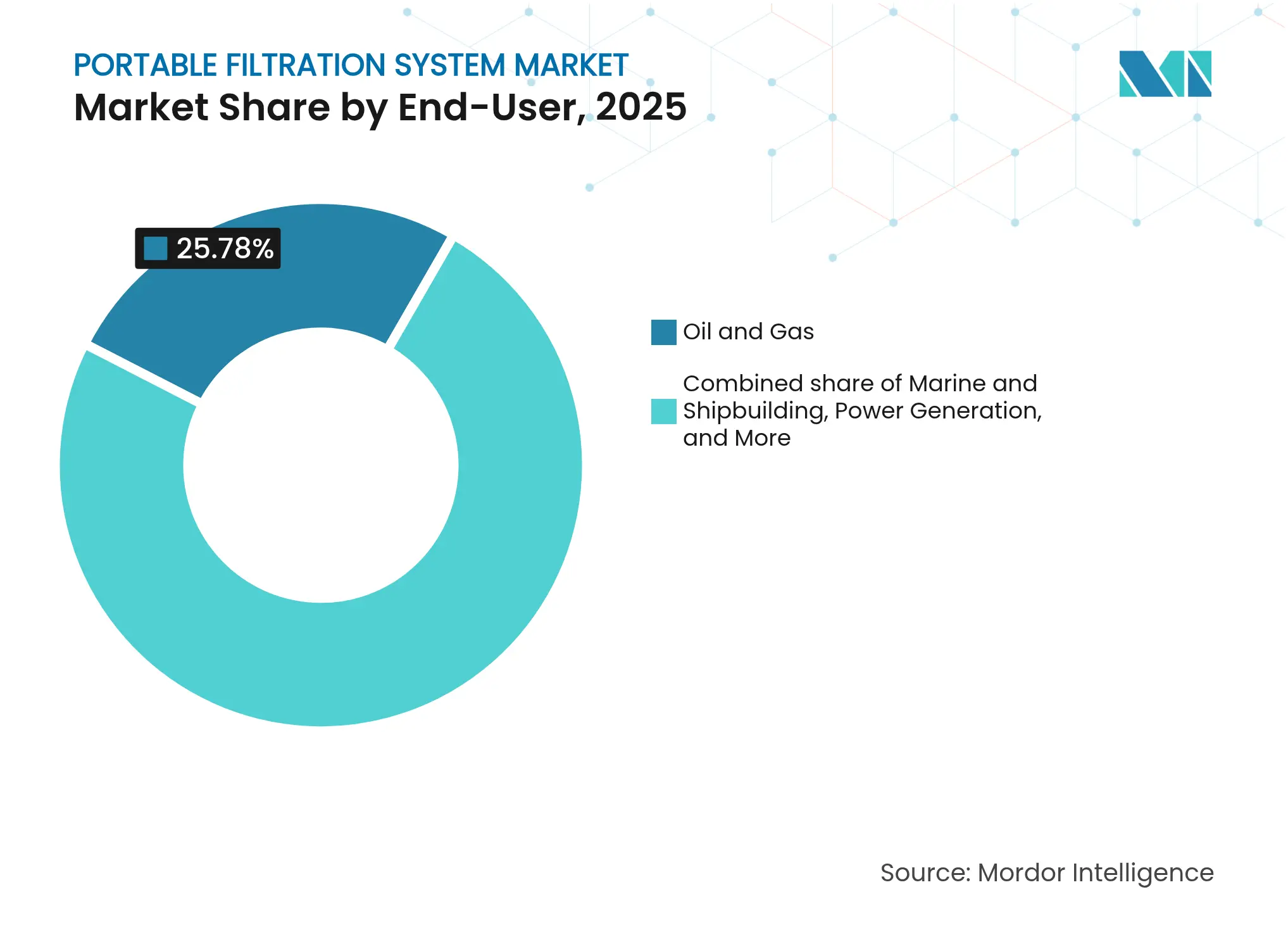

By End-User: Oil & Gas Dominance Challenged by Marine Growth

Oil and gas remained the top adopter, with a 25.78% share of the portable filtration system market size in 2025, driven by offshore completion-fluid conditioning and produced-water polishing, which together filter more than 20 billion gallons daily. High-pressure, high-temperature service environments favor rugged stainless housings and β >1000 media, ensuring long replacement intervals. Power-generation turbine operators follow closely, sidelining portable skids during major outages to clean reservoir fluids and meet warranty thresholds.

Marine and shipbuilding follow an 8.09% CAGR as IMO rules cap bilge-water discharge to 15 ppm and tighten bunker-fuel sulfur limits, prompting yards and fleets to add deck-mounted purifiers for fuel and lube oils [IMO.ORG]. Hybrid electric ferries and offshore support vessels also adopt portable gear to service multiple tanks without permanent retrofits. Chemicals and petrochemicals purchase specialty systems with acid-resistant internals, while pulp and paper plants hold off on demand until commodity prices strengthen. Food and beverage processors incorporate portable filtration when batch lines switch between frequent recipes, requiring sanitary requalification, although the volume remains modest relative to industrial sectors.

Note: Segment shares of all individual segments available upon report purchase

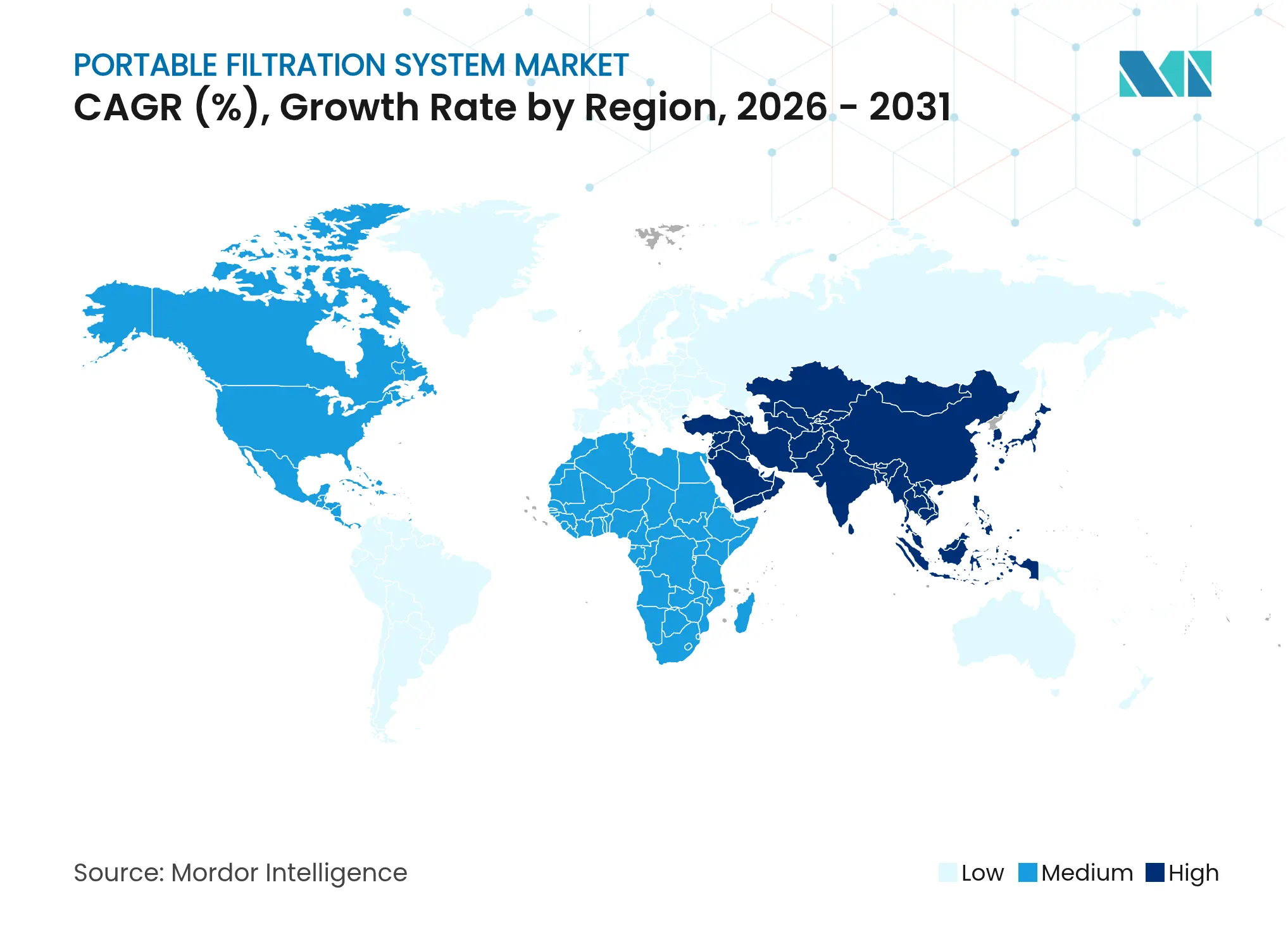

North America retained 33.02% of the portable filtration system market in 2025, driven by stringent environmental oversight and a mature service ecosystem that streamlines rental logistics and on-site support. Gulf of Mexico platforms require portable purifiers rated for 10,000 psi to process completion fluids in real-time. Aerospace hubs in Washington, Texas, and Quebec adhere to ISO 15/13/10 hydraulic standards, maintaining steady demand. Regulatory momentum, including evolving marine discharge rules, will keep regional growth close to the global trend, despite occasional CAPEX pauses triggered by energy price fluctuations.

The Asia-Pacific region is the fastest-growing region, with an 7.98% CAGR through 2031. China intensifies its focus on product quality in the automotive and electronics sectors, prompting factories to invest in predictive filtration as part of Industry 4.0 rollouts. India expands refining and petrochemical capacity, channeling orders for portable fuel-oil skids. Semiconductor investments in Singapore and Taiwan require ultra-clean fluids for CMP and lithography tools, giving premium suppliers an entry point. Governments across ASEAN raise wastewater-discharge thresholds, indirectly stimulating mobile polishing services during plant turnarounds.

Europe sustains a technology-driven stance; aerospace centers in France and Germany demand portable purifiers with onboard particle counting and IoT connectivity. EU circular-economy directives favor solutions that extend oil life and cut filter waste, aligning with portable carts equipped for β > 2000 elements. South America faces tariff-driven media price hikes that limit near-term adoption, although Brazilian offshore rigs continue to procure high-capacity units for FPSO topsides. The Middle East and Africa rely on energy-sector spending, with Gulf states integrating portable filtration into maintenance contracts for new petrochemical complexes. Mini-grid electrification in Sub-Saharan Africa also adds incremental volume as rural operators prioritize the reliability of generators.

Market Concentration

The portable filtration system market remains moderately fragmented. Pall Corporation, Parker Hannifin, and Donaldson leverage broad product catalogs, global service reach, and continued R&D outlays to hold leadership positions. Pall extended semiconductor coverage by opening a USD 150 million Singapore plant in 2024, demonstrating a commitment to regional supply security. Parker integrates cloud dashboards into the latest carts, bundling subscription analytics that deepen customer stickiness. Donaldson’s minority investment in Medica S.p.A. brings hollow-fiber expertise that could translate to high-purity industrial skids.

Midsize specialists—Schroeder Industries, MP Filtri, and Y2K Filtration—win share in niche segments such as high-viscosity suction carts or ATEX-rated units. Rental providers build fleets capable of 4,000 L/min flow to capitalize on emergency decontamination events, offering turnkey services that include root-cause analysis. Technology convergence promotes partnerships: filter OEMs collaborate with sensor start-ups to embed real-time ISO code feedback, raising system ASPs but improving ROI for end-users.

Acquisition appetite stays high. Thermo Fisher’s USD 4.1 billion acquisition of Solventum’s purification unit demonstrates that life sciences players are eyeing cross-sector synergies. United Flow Technologies and Aqua-Aerobic Systems expand their geographic reach through strategic tuck-ins, strengthening their municipal water positions. Competitive intensity thus centers on technology integration, service contracts, and solution breadth rather than pure price rivalry, supporting healthy margins across the portable filtration system industry.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts

6. Competitive Landscape

7. Market Opportunities & Future Outlook

The portable filtration system market report include:

Unlocking Market Potential for Solid-State Transformers

3 Min Read

Wealth Management Intelligence for the Middle East

4 Min Read

Driving Growth in the Embedded Insurance Market

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.