Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

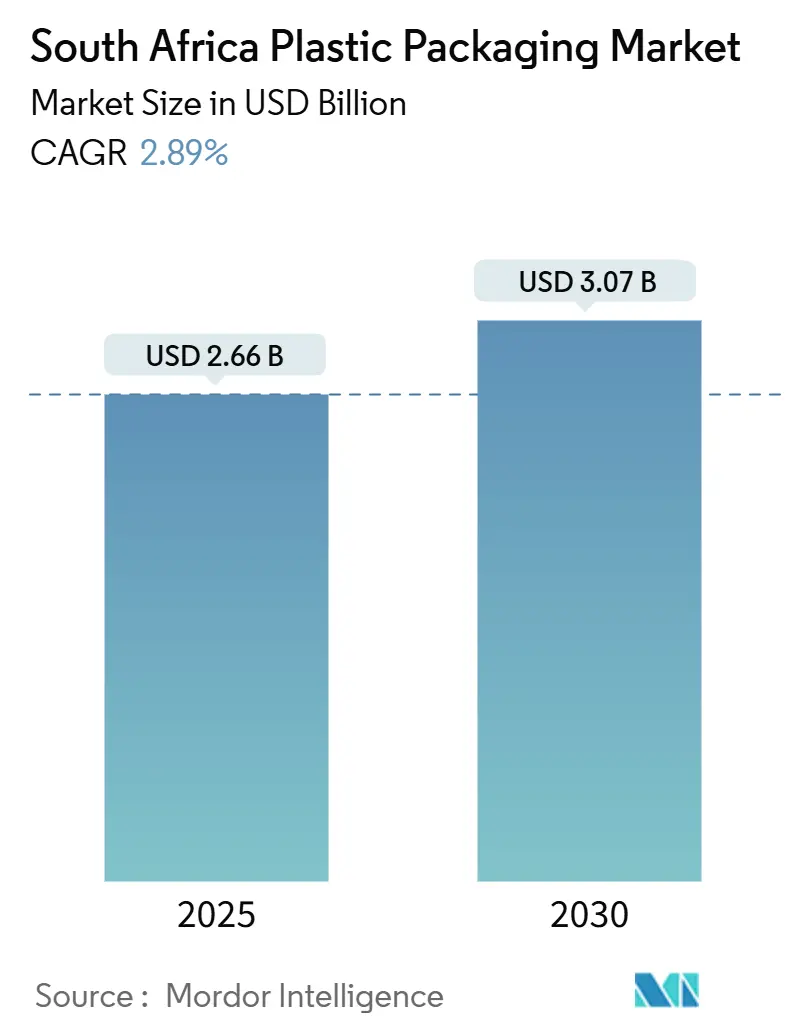

| Market Size (2025) | USD 2.66 Billion |

| Market Size (2030) | USD 3.07 Billion |

| Growth Rate (2025 - 2030) | 2.89% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Africa Plastic Packaging Market Analysis by Mordor Intelligence

The South Africa plastic packaging market size stands at USD 2.66 billion in 2025 and is projected to reach USD 3.07 billion by 2030, translating into a steady 2.89% CAGR during the forecast period. Demand holds firm as e-commerce fulfillment, food processing expansion, and localization incentives offset electricity supply volatility and resin price swings. Material substitution toward mono-material films accelerates the shift from rigid to flexible formats, while recycling investments anchor circular-economy value chains across beverages and personal care. Converter margins remain under pressure from rand depreciation and feedstock costs, yet off-grid power solutions and digitalized operations bolster productivity. Intensifying regulatory scrutiny of single-use plastics simultaneously sparks innovation in biodegradable resins and premium recycled content, positioning the South Africa plastic packaging market to capture both domestic and export opportunities into the Southern African Customs Union.

Key Report Takeaways

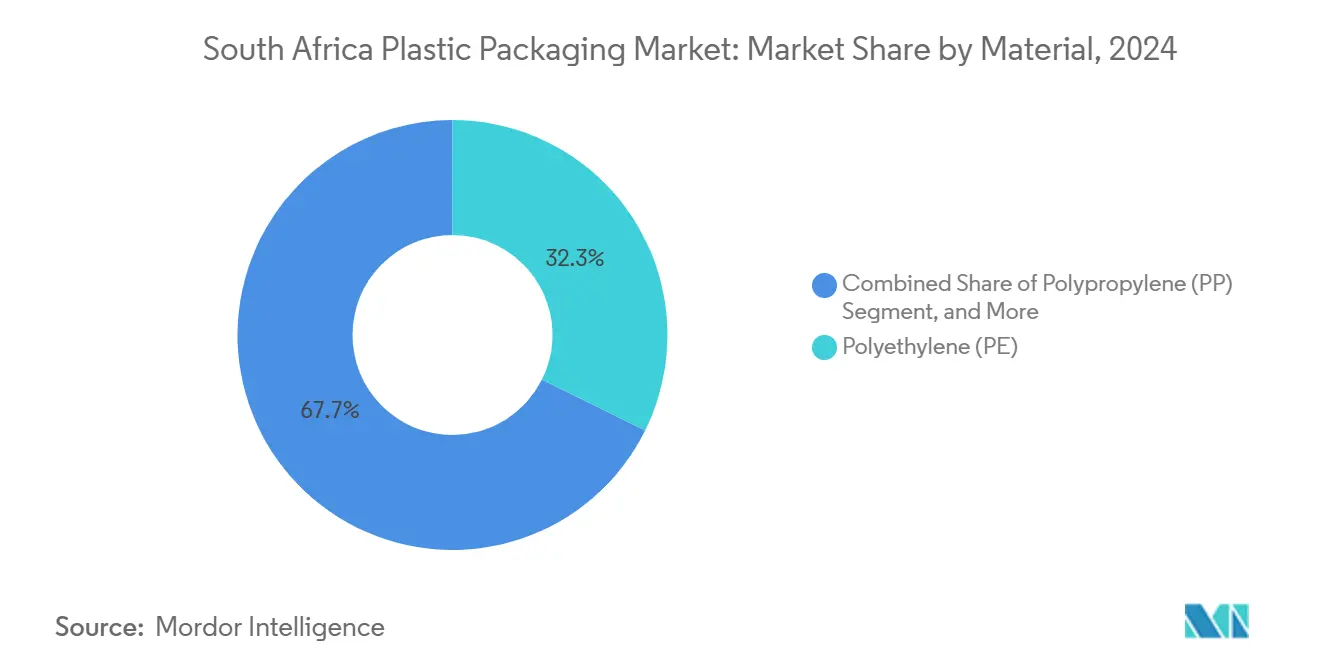

- By material, polyethylene led with 32.32% of the South Africa plastic packaging market share in 2024, whereas polyethylene terephthalate is forecast to expand at a 3.78% CAGR through 2030.

- By product type, pouches commanded 28.42% share of the South Africa plastic packaging market size in 2024, while films and wraps are projected to grow at 3.64% CAGR between 2025 and 2030.

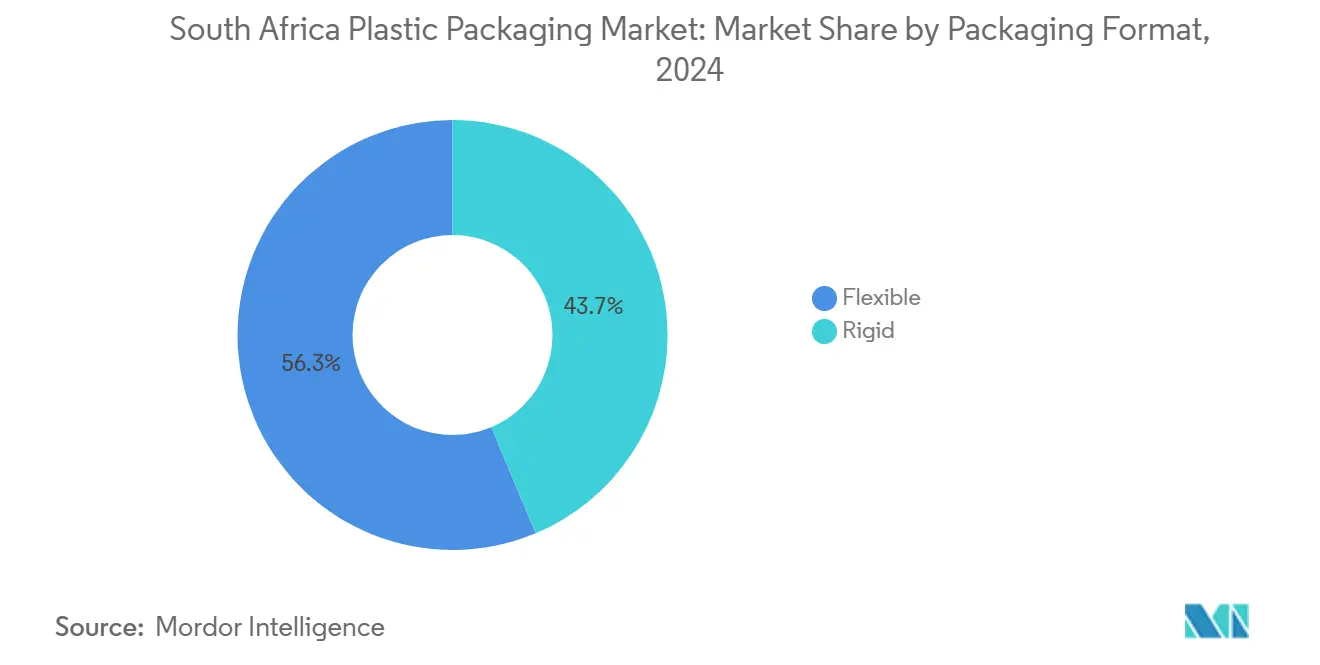

- By packaging format, flexible solutions captured 56.32% of 2024 revenue and also represent the fastest-growing format at 4.01% CAGR to 2030.

- By end-user industry, food applications accounted for 30.12% of the 2024 South Africa plastic packaging market size, whereas personal and home care products are set to advance at a 4.23% CAGR to 2030.

South Africa Plastic Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for consumer goods | +0.80% | Gauteng and Western Cape | Medium term (2-4 years) |

| Favorable material properties of plastics | +0.60% | National | Long term (≥ 4 years) |

| Expansion of e-commerce logistics and last-mile delivery | +0.70% | Urban centers | Short term (≤ 2 years) |

| Localization incentives under South Africa’s industrial policy | +0.50% | National | Medium term (2-4 years) |

| Surge in cannabis-derived food and pharma packaging | +0.30% | Western Cape | Short term (≤ 2 years) |

| Rising adoption of mono-material flexible packs | +0.40% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Consumer Goods

Household final-consumption expenditure rebounded 1.4% quarter-on-quarter in Q2 2024, restoring packaging volumes across food, beverages, and personal care. [1]South African Reserve Bank, “Quarterly Bulletin No 312,” resbank.co.za Flexible pouches absorbed much of this lift, capturing 28.42% market share in 2024 owing to portion control, portability, and value positioning. Township retail expansion fuels demand for small pack sizes that match disposable-income realities, while the Small Enterprise Manufacturing Support Programme helps converters tap these micro-market niches. Food producers extend shelf life via oxygen-barrier films that also curb food waste in rural distribution corridors. As brand owners prioritize on-shelf differentiation, the South Africa plastic packaging market gains further impetus from graphics-rich laminates and lightweight rigid options.

Expansion of E-commerce Logistics and Last-mile Delivery

Online retail penetration surpasses 5% of total commerce in 2025, triggering sizeable secondary-pack demand for shippers and cushioning inserts. Reusable corrugated-plastic hybrids lower return-trip damages, whereas lightweight mailers cut fulfillment freight costs by up to 20%. Tamper-evident and moisture-barrier pouches dominate pharmaceutical and beauty shipments that require product integrity assurance. Packaging equipped with QR-enabled track-and-trace boosts consumer confidence and reduces reverse-logistics friction. Collectively, these dynamics reinforce volume upside for the South Africa plastic packaging market in dense urban nodes and emerging secondary cities.

Localization Incentives under South Africa’s Industrial Policy

The Department of Trade, Industry and Competition links investment rebates to domestic content thresholds for consumer goods, catalyzing extrusion and thermoforming capacity upgrades among packaging converters. Black Industrialists Programme beneficiaries secure preferential procurement from state-owned enterprises, anchoring order books and encouraging skills transfer. Industrial Development Zones in Eastern Cape and KwaZulu-Natal channel tax holidays toward export-oriented flexible-pack plants that serve agricultural exporters. Such initiatives replace imports of high-barrier pouches with locally converted alternatives, nudging the South Africa plastic packaging market toward deeper manufacturing integration and job creation.

Rising Adoption of Mono-material Flexible Packs for Recyclability

Extended Producer Responsibility regulations stipulate design-for-recycling criteria that elevate polyethylene-based mono-material films. Polymer-modification and coating advances now replicate multilayer oxygen and moisture barriers without complicating recycling streams. The Department of Forestry, Fisheries and Environment’s USD 16.4 million PET recycling facility underscores government commitment to circular infrastructure. Extrupet processes more than 2 billion bottles per year into food-grade rPET, shrinking virgin demand and reducing carbon footprints. Consumer brands inserting mono-material mandates into briefs propel further scale, consolidating the sustainability thesis underpinning growth in the South Africa plastic packaging market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile resin prices and environmental concerns | -0.90% | National | Short term (≤ 2 years) |

| Stricter regulations on single-use plastics | -0.60% | National | Medium term (2-4 years) |

| Electricity load-shedding disrupting production lines | -1.20% | Manufacturing hubs | Medium term (2-4 years) |

| Recycled-resin supply constraints from informal collection | -0.40% | Urban-rural mix | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Resin Prices and Environmental Concerns

Rand depreciation magnifies global crude-linked resin swings, compressing converter margins and complicating contract pricing. Brand owners adopting plastic-reduction targets stall volume growth in legacy rigid formats. Import reliance on specialty additives exposes local plants to shipping delays, while limited domestic petrochemical capacity restricts hedging options. Heightened consumer eco-awareness channels demand toward bio-based or recycled inputs, forcing converters to retool lines and qualify new suppliers. These factors collectively temper upside for the South Africa plastic packaging market despite underlying consumption gains.

Electricity “Load-shedding” Disrupting Production Lines

Intermittent power curtailments lower extrusion uptime and elevate scrap rates that can exceed 7% during peak outages. Generators and battery systems shield critical processes but inflate operating costs by up to 15%. Production scheduling around load-shedding blocks elongates lead times, thereby raising working capital tied up in safety stock. Independent-power-producer collaborations unlock renewable-energy purchase agreements, yet capital payback horizons challenge cash-constrained small converters. Until grid stability improves, power insecurity remains the single most material bottleneck facing the South Africa plastic packaging market.

Segment Analysis

By Material: Polyethylene Dominance Amid PET Innovation

Polyethylene retained 32.32% of the South Africa plastic packaging market share in 2024, thanks to unrivaled versatility across carrier bags, shrink films, and pharmaceutical vials. Metallocene-catalyst grades permit thinner gauges without sacrificing seal integrity, lowering resin use per SKU and helping brand owners meet plastic-reduction pledges. Polypropylene follows, leveraging heat resistance critical for microwave-able ready meals.

Polyethylene terephthalate is projected to post the highest 3.78% CAGR, buoyed by bottle-to-bottle recycling that tightens closed-loop supply and enhances food-grade credentials. [2]Extrupet, “Bottle-to-Bottle Recycling Expansion,” extrupet.com Capital injections at Extrupet’s Germiston plant coupled with PETCO’s collection network elevate rPET content in beverage bottles well beyond the statutory 30% threshold. Polyvinyl chloride applications persist in IV-fluid bags and blister packs where chemical resistance trumps substitution efforts, while niche biodegradable polymers gain modest traction under premium organic-food labels.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Product Type: Flexible Solutions Drive Innovation

Pouches captured 28.42% of the South Africa plastic packaging market size in 2024, underpinned by urban consumer preference for portability, tear-open convenience, and resealability. Coffee, pet food, and cosmetics increasingly migrate into stand-up pouches with laser-scored easy-open spouts.

Films and wraps will accelerate at a 3.64% CAGR through 2030 as produce exporters adopt high-oxygen-transmission films that delay ripening and slash wastage in cross-border supply chains. Bottles and jars retain beverage and personal-care footholds due to merchandising familiarity, yet lightweight PET iterations shave gram weight by 9% on 500 ml formats without compromising top-load. Technical consultations with the University of Pretoria spotlight changeover optimization that trims downtime on multi-format lines.

By Packaging Format: Flexible Packaging Transformation

Flexible formats accounted for 56.32% of 2024 revenue and will outpace the overall South Africa plastic packaging market at a 4.01% CAGR. [3]Department of Forestry, Fisheries and Environment, “PET Recycling Facility Announcement,” environment.gov.za Typically using 70% less material than equivalent rigid packs, they also slash freight emissions and optimize warehouse cube utilization. Advances in vacuum-deposited barrier coatings now deliver 18-month shelf life suitable for ambient retort soups, broadening end-use horizons.

Rigid packaging continues to dominate carbonated beverages, agrochemicals, and industrial lubricants where drop testing and tamper evidence are paramount. Lightweighting and design for recyclability remain the focus, with tethered-cap directives prompting neck-finish redesigns. Biodegradable rigid trays sourced from cassava starch, as outlined in MDPI Foods research, present early-stage avenues for eco-minded retailers.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-user Industry: Food Sector Leadership and Personal Care Growth

Food applications held 30.12% of 2024 demand, reflecting South Africa’s status as the region’s agri-processing hub. Modified-atmosphere bags double shelf life for strawberries on export runs to the Middle East, while meat processors deploy high-barrier shrink films that cut freezer burn. Sachetization of cooking oil and fortified staples improves affordability for low-income households, sustaining baseline volumes.

Personal and home care is slated for the quickest 4.23% CAGR, propelled by premium cosmetics, men’s grooming, and eco-friendly cleaning concentrates. Multi-layer pump bottles equipped with 50% rPET exemplify brand strategies that fuse sustainability with shelf presence. Beverage converters balance PET lightweighting with carbonation integrity, and pharmaceutical firms preserve growth via serial-numbered blister packs satisfying track-and-trace mandates.

Geography Analysis

South Africa anchors regional plastic-pack production, leveraging mature logistics, skilled labor, and robust downstream consumer-goods clusters concentrated around Gauteng. The province hosts more than half of national converting capacity, enabling just-in-time deliveries to Johannesburg distribution centers. Western Cape benefits from agricultural exports and the Cape Town port, channeling fresh-produce film demand and wine-bottle label volumes. KwaZulu-Natal’s Richards Bay Industrial Development Zone incentivizes thermoformed fruit-tray plants serving both domestic retailers and Mozambican wholesalers.

Real GDP dipped 0.3% quarter-on-quarter in Q3 2024, yet year-on-year growth remained positive at 0.3%, signaling macro resilience amid load-shedding and logistics congestion. Currency appreciation through 2025 improves imported resin affordability but compresses margins on export packs shipped to Botswana and Namibia. Nevertheless, Southern African Development Community trade facilitation reduces border dwell times by 12%, sustaining outbound flows of flexible sacks for maize meal and detergent.

Risk diversification drives converters to establish satellite warehouses in Windhoek and Gaborone, mitigating lead-time volatility. Political turmoil in Mozambique tempers long-haul investments, although short-run pouch exports for canned tuna persist via Beira port corridors. Overall, regional integration augments baseline growth for the South Africa plastic packaging market while reinforcing its role as the supply node for sub-Saharan fast-moving consumer goods.

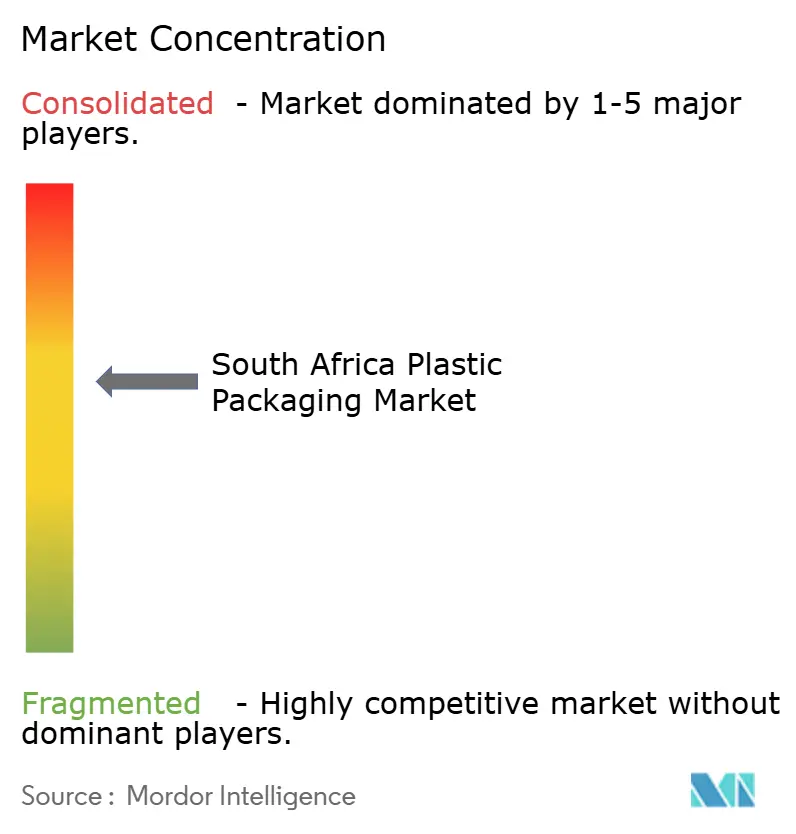

Competitive Landscape

The South Africa plastic packaging market remains moderately Concentrated. Mpact leverages vertical integration across paper and plastics, translating recovered polyethylene and PET into value-added films and trays that resonate with retailer sustainability goals. [4]Mpact Limited, “Integrated Report 2025,” mpact.co.za Nampak’s divestiture of its liquid-cartons unit in September 2024 freed capital for high-speed PET preform lines and tethered-cap adoption. Constantia Afripack amplifies its share in barrier laminates, servicing multinational confectionery and dairy brands through region-wide contracts.

Technology spending differentiates leaders: digital inkjet presses print SKUs-on-demand, slashing inventory of obsolete labels, while automated optical inspection boosts line yield on complex spouted pouches. Smaller challengers such as Dank Pack specialize in odor-barrier cannabis packaging, capturing emerging medical-marijuana channels legalized nationally in 2024. BioPack Africa pilots compostable cassava-starch trays for ready meals, illustrating how niche innovators exploit regulation-driven white spaces.

Strategic collaborations multiply; Mpact partners with Extrupet to secure food-grade rPET feedstock, reducing virgin resin exposure and meeting beverage-client recycled-content quotas. Nampak collaborates with Sasol Polymers on metallocene LLDPE supply that underpins downgauged stretch film ranges. Constantia inks R&D agreements with the Council for Scientific and Industrial Research to certify mono-material barrier structures. Such maneuvers intensify competitive jockeying yet collectively expand technical capability across the South Africa plastic packaging market.

South Africa Plastic Packaging Industry Leaders

-

Amcor plc

-

Nampak Ltd

-

Mpact Ltd

-

Constantia Flexibles GmbH

-

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Mpact reported full-year headline earnings per share growth and emphasized the contribution of integrated paper-and-plastics recycling platforms.

- February 2025: Propak Africa 2025 showcased smart-packaging and energy-efficient extrusion equipment to South African converters.

- January 2025: AcePak, Opack Africa, and USS Pactech broadened field-service capabilities, expediting technology transfer to local SMEs.

- December 2024: MDPI Foods published research on starch-based biodegradable packaging, offering scalable process parameters for developing-country factories.

South Africa Plastic Packaging Market Report Scope

The scope of the study characterizes the plastic packaging industry based on the raw materials of the product, including PP, PE, PET, and other raw materials used across various end-user industries, such as food and beverage, across the country. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The plastic packaging industry in South Africa is segmented by product type (bottles and jars, pouches, bags, films and wraps, and other product types), type of plastic (rigid plastic and flexible plastic), material (polyethylene (PE), polypropylene (PP), polyvinyl chloride (PVC), polyethylene terephthalate (PET), and other materials), and end-user industry (food, beverages, healthcare and pharmaceuticals, personal and home care, and other end-user industries). The market sizes and forecasts are provided in terms of value (USD) for the above segments.

By Material

| Polyethylene (PE) |

| Polypropylene (PP) |

| Polyvinyl Chloride (PVC) |

| Polyethylene Terephthalate (PET) |

| Other Materials |

By Product Type

| Bottles and Jars |

| Pouches |

| Bags |

| Films and Wraps |

| Other Product Types |

By Packaging Format

| Rigid |

| Flexible |

By End-user Industry

| Food |

| Beverages |

| Healthcare and Pharmaceuticals |

| Personal and Home Care |

| Other End-user Industries |

| By Material | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyvinyl Chloride (PVC) | |

| Polyethylene Terephthalate (PET) | |

| Other Materials | |

| By Product Type | Bottles and Jars |

| Pouches | |

| Bags | |

| Films and Wraps | |

| Other Product Types | |

| By Packaging Format | Rigid |

| Flexible | |

| By End-user Industry | Food |

| Beverages | |

| Healthcare and Pharmaceuticals | |

| Personal and Home Care | |

| Other End-user Industries |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the South Africa plastic packaging market in 2025?

The market is valued at USD 2.66 billion in 2025 and is forecast to grow at 2.89% CAGR to 2030.

Which material leads demand?

Polyethylene holds the highest 32.32% share due to versatility across rigid and flexible applications.

What is the fastest-growing packaging format?

Flexible formats such as pouches and wraps are projected to expand at 4.01% CAGR through 2030.

How is load-shedding affecting converters?

Power interruptions raise scrap rates, extend lead times, and inflate operating costs by up to 15%, prompting off-grid energy investments.

Which end-user segment offers the quickest growth?

Personal and home care packaging is forecast to post a 4.23% CAGR, buoyed by premium beauty and eco-cleaning products.

What regulatory trend shapes design choices?

Extended Producer Responsibility rules push adoption of mono-material packs that improve mechanical recyclability and secure recycled-content supply.

Page last updated on: