Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 13.88 Billion |

| Market Size (2030) | USD 18.09 Billion |

| Growth Rate (2025 - 2030) | 5.44% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Indonesia Oil And Gas Market Analysis by Mordor Intelligence

The Indonesia Oil And Gas Market size is estimated at USD 13.88 billion in 2025, and is expected to reach USD 18.09 billion by 2030, at a CAGR of 5.44% during the forecast period (2025-2030).

This trajectory highlights how the Indonesian oil and gas market is shifting from long-mature onshore basins toward offshore growth, carbon capture integration, and digital transformation. Rising domestic demand, favorable production-sharing terms, and deep-water discoveries are widening capital flows into exploration while sustaining service revenues from maintenance and turnaround activities that keep aging infrastructure online. Competitive intensity is shaped by Pertamina’s 60% share of national output, the return of international oil companies that leverage advanced recovery techniques, and escalating investment in CCUS hubs, which extend field life and lower lifecycle emissions. Offshore fields in the Natuna Sea, Abadi Masela, and Mahakam Delta are redefining project economics, with FPSOs and subsea tiebacks significantly shortening the time to first gas. Meanwhile, small-scale LNG solutions are broadening the market reach to remote islands and mining enclaves.

Key Report Takeaways

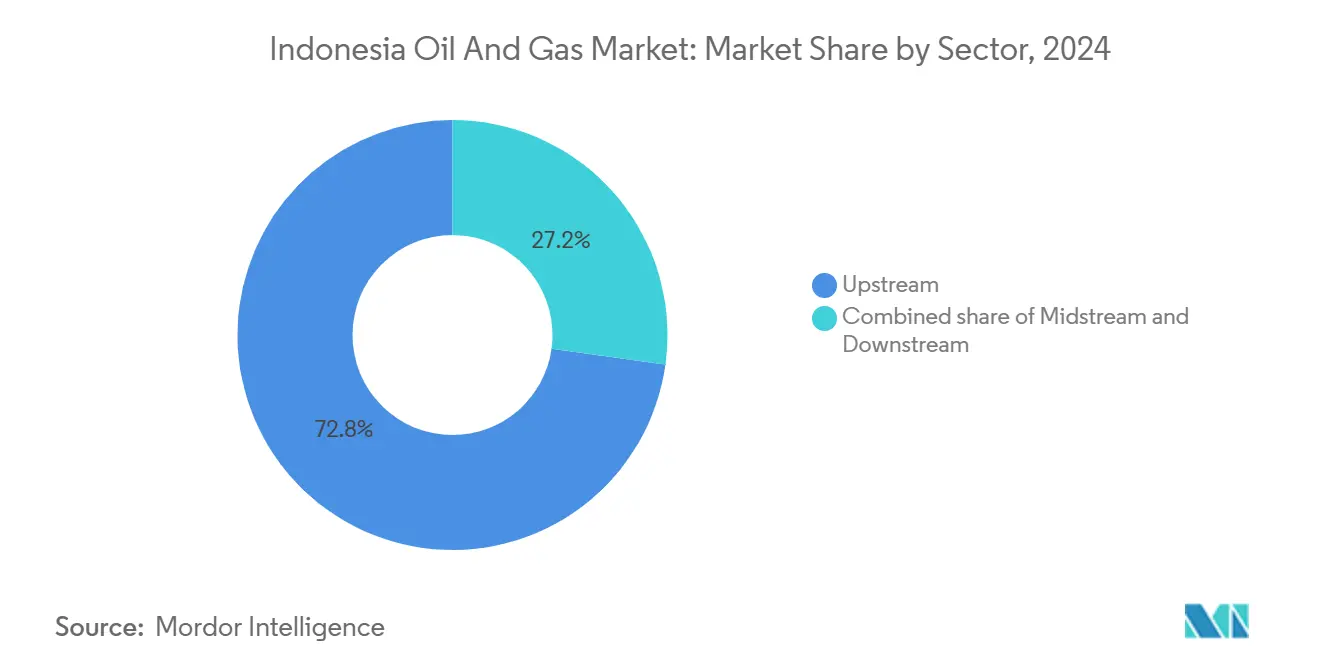

- By sector, upstream activities held a 72.8% Indonesia oil and gas market share in 2024, while midstream and downstream segments are projected to grow at 4.9% and 4.4% CAGRs, respectively, through 2030.

- By location, offshore developments are advancing at a 6.1% CAGR through 2030, outpacing the mature onshore segment that still commanded 58.5% of the Indonesian oil and gas market size in 2024.

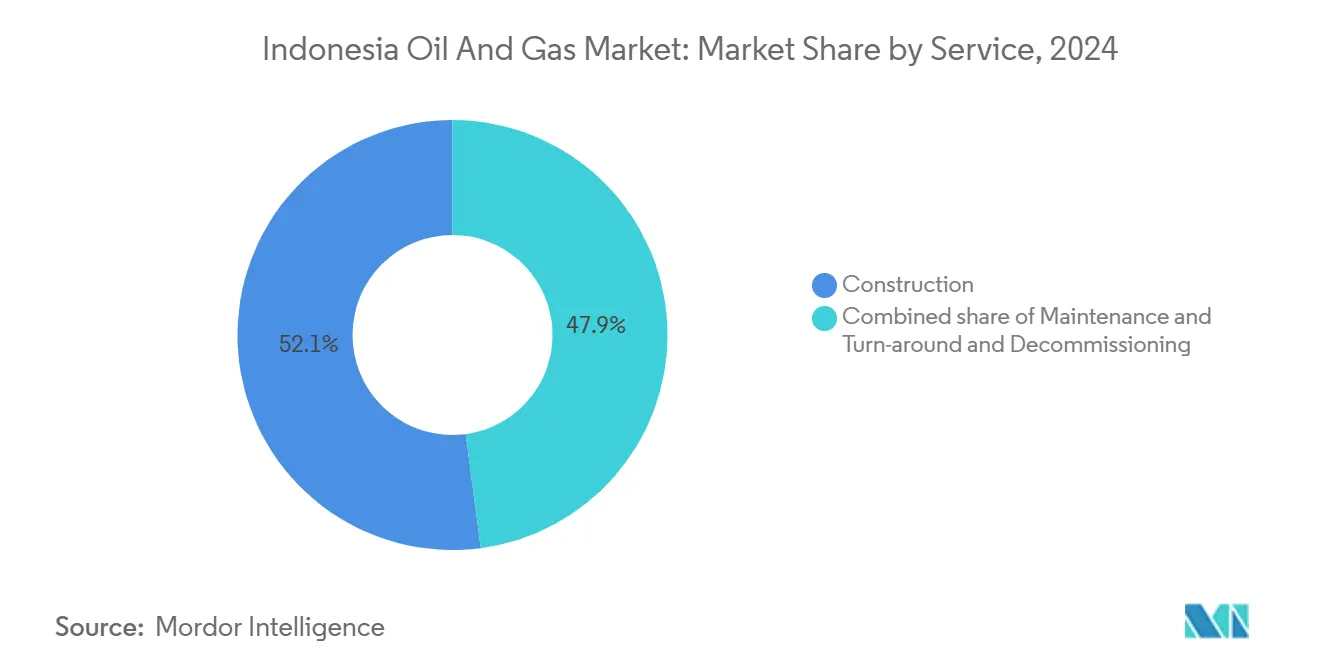

- By service, maintenance, and turn-around offerings are forecast to expand at a 6.3% CAGR, yet construction services retained a 52.1% share of the Indonesian oil and gas market size in 2024.

Indonesia Oil And Gas Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust domestic demand from rising middle class | +0.8% | National, with concentration in Java, Sumatra, and Kalimantan urban centers | Medium term (2-4 years) |

| Government push for 1 mb/d crude & 12 Bcf/d gas by 2030 | +1.1% | National, with focus on Natuna, Mahakam, and East Java basins | Long term (≥ 4 years) |

| LNG export arbitrage to North-East Asia | +1.0% | Coastal regions, particularly Bontang, Tangguh, and planned Jawa-1 facilities | Medium term (2-4 years) |

| PSC gross-split incentives attracting IOCs | +0.7% | National, with early gains in frontier basins and deep-water blocks | Short term (≤ 2 years) |

| Carbon-capture hubs boosting mature-field economics | +0.4% | Mature basins in South Sumatra, Central Java, and East Kalimantan | Long term (≥ 4 years) |

| AI-enabled digital oilfields cutting lifting cost | +0.5% | National, with pilot implementations in Pertamina and IOC operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Robust Domestic Demand from Rising Middle Class

Indonesia’s growing middle class is driving up gasoline, diesel, and petrochemical consumption, with daily crude demand projected to reach 1.8 million barrels by 2030, up from roughly 1.6 million barrels in 2025.[1]Ministry of Energy and Mineral Resources, “Energy Outlook 2025–2035,” esdm.go.id Java’s urbanization rate above 60% intensifies transport fuel use, despite efficiency drives, while rising personal incomes underpin higher demand for plastics and packaging. Natural gas demand is expected to reach 12 Bcf/d by 2030, as combined-cycle power plants supplement renewable energy intermittency and meet the needs of industrial boilers. Fuel-subsidy reforms redirect savings into roads, ports, and mass transit projects, which further spur energy needs, reinforcing the long-term pull for domestic hydrocarbons.

Government Push for 1 Million bbl/d Crude and 12 Bcf/d Gas by 2030

SKK Migas targets 1 million barrels per day (bbl/d) of oil and 12 billion cubic feet per day (Bcf/d) of gas to curb import dependence, which already covers 60% of refined-product demand. Priority accelerators include 127 blocks slated for fast-track approval, fiscal sweeteners for enhanced recovery, and digital field surveillance that lifts output from marginal reservoirs. Projects such as Abadi LNG and the Tangguh expansion underpin gas deliverability, whereas steamflood and chemical EOR initiatives at Minas and Duri slow base decline. The regulatory path features gross-split PSCs that streamline audits and guarantee earlier cash flow, attracting Chevron, Harbour Energy, and Medco into frontier acreage.

LNG Export Arbitrage to North-East Asia

Indonesia’s 34 MTPA of operating LNG capacity from Bontang and Tangguh traditionally feeds Japan, South Korea, and China, where spot premiums can rise USD 2–3/MMBtu above domestic. While Abadi LNG will inject another 9.5 MTPA, policymakers warn that swelling domestic offtake could see Indonesia pivot from a net exporter to an importer late this decade. Pertamina’s USD 1.5 billion program for modular regas units enables diesel displacement on outer islands, expanding local gas penetration and partially cushioning export erosion. Producers thus navigate a dual market, capturing arbitrage when available, while prioritizing long-term Indonesian contracts that hedge policy risk.

PSC Gross-Split Incentives Attracting IOCs

Introduced in 2017, gross-split PSCs grant contractors a fixed production percentage upfront, thereby eliminating the need for exhaustive cost-recovery audits.[2]Upstream Online, “Gross-Split PSCs Lure IOCs Back,” upstreamonline.com Subsequent amendments enhance splits for deep-water, high-CO₂, or CCUS-integrated projects, resulting in after-tax IRRs that are up to 4 percentage points higher than those under legacy terms. Faster cash visibility has lured TotalEnergies back into Mahakam infill drilling and enticed Shell to re-enter the Corridor Block after setbacks from its divestment. Early-mover benefits include carbon-credit eligibility for verified sequestration associated with producing assets, thereby increasing the blended project NPV.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewable-energy build-out & EV adoption | -0.4% | National, with accelerated impact in Java and urban centers | Medium term (2-4 years) |

| Declining output from ageing basins | -0.7% | Legacy producing regions: South Sumatra, Central Java, East Kalimantan | Short term (≤ 2 years) |

| Land-right & indigenous community disputes | -0.3% | Papua, Kalimantan, and remote Sumatra regions | Long term (≥ 4 years) |

| ESG-linked financing constraints | -0.4% | Global, with spillover effects on Indonesian upstream projects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Renewable-Energy Build-Out and EV Adoption

Indonesia aims for 23% renewable energy penetration by 2025 and net-zero emissions by 2060, ambitions that redirect capital from fossil fuel projects into solar, wind, and geothermal units totaling 10 GW under construction. Fiscal incentives for EV assembly plants draw global OEMs to West Java, in line with a national goal of 2 million battery electric vehicles on the roads by 2030. While gas still balances intermittency, long-run gasoline demand faces attrition as charging networks densify across toll-road corridors. Yet infrastructure gaps and price sensitivity moderate short-term displacement, allowing the Indonesian oil and gas market to retain core transport and industrial segments.

Declining Output from Ageing Basins

Production falls 5–8% annually at Minas, Duri, and Mahakam, despite the implementation of waterflood and steam cycles, and lifting unit costs increase by 15–20% per year.[3]Pertamina, “Enhanced Recovery at Minas and Duri,” pertamina.com The Mahakam Delta, once Indonesia’s largest gas hub, now yields 600 MMcf/d, down from peaks above 1 Bcf/d. AI-driven well diagnostics reduced optimization time by 66% at Attaka, yet base decline still erodes national volumes faster than new projects can ramp up. Sustaining 1 million barrels per day (mb/d) thus hinges on continuous infill drilling, EOR pilots, and accelerated tie-backs from satellite fields.

Segment Analysis

By Sector: Upstream Dominance Drives Market Growth

Indonesia's oil and gas market size for the upstream segment was USD 10.1 billion in 2025, accounting for 72.8% of the overall revenue and projected to grow at a 5.7% CAGR through 2030. Major capital commitments include BP's USD 7 billion Tangguh UCC and Inpex's USD 20 billion Abadi LNG project, signaling durable corporate confidence in long-cycle gas projects. Production-sharing reforms, digital subsurface imaging, and reservoir robotics enhance recovery rates from legacy wells, reinforcing upstream cash flow even as basins mature.

Gross-split PSCs heighten transparency, with cost certainty spurring Chevron's return to the Rapak Block and Harbour Energy's infill campaign at Tuna. Digital asset integrity systems deployed by Pertamina and FPT Software reduced unplanned shutdowns by 15%, demonstrating the operational advantage that AI integration provides. Midstream expansions—new pipelines linking Central Sulawesi to Java—protect evacuation economics, while downstream petrochemical integration at Tuban refinery monetizes heavier crudes into high-margin olefins.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Location: Offshore Growth Outpaces Onshore Maturity

Onshore operations still accounted for 58.5% of the Indonesian oil and gas market share in 2024; however, offshore CAGRs of 6.1% underscore where incremental barrels are expected to arise. Deep-water wells in the Natuna Sea achieve initial flow rates exceeding 10,000 bbl/d, supported by FPSO units that bypass costly fixed platforms. Abadi FLNG’s subsea-to-shore design reduces surface footprint, complying with stringent maritime spatial directives while reducing project time.

Onshore producers face higher lifting costs and community permitting, prompting Pertamina to ramp up steamflood operations at Duri and pilot polymer floods at Rokan. In contrast, offshore contractors deploy wired drill-pipe telemetry to optimize steerable drilling, thereby reducing the number of days on the well. Environmental stewardship remains stringent, with marine-mammal monitoring and zero-discharge mandates preceding SKK Migas approvals for any subsea tie-back.

By Service: Maintenance Complexity Drives Service Growth

Construction retained 52.1% of the Indonesian oil and gas market share in 2024, as pipeline builds, LNG tanks, and gas-fired power plants required extensive heavy civil works. Yet, maintenance and turn-around services are tipped to grow at a 6.3% CAGR, beating overall output because 70% of wells are classified as mature and demand condition-based servicing. Predictive analytics cut pump failure at Mahakam by 18%, while drones and crawler robots inspect flare stacks without shutdown.

Decommissioning emerges as a niche, with 12 offshore platforms scheduled for retirement by 2030, unlocking USD 300 million in plug-and-abandon contracts. Service providers that couple digital twins with modular well-plugging equipment secure a competitive advantage under strict local-content rules. Real-time collaboration centers in Jakarta liaise with Kalimantan work sites, enabling expert oversight with minimal travel cost and greenhouse emissions.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

South Sumatra supplies roughly 25% of the nation's crude, leveraging steam-assisted gravity drainage to extend fields that began production in the 1960s. Enhanced recovery boosts recovery factors to 40%, cushioning the natural decline and keeping the Cilacap refinery well-stocked to meet Java’s motor-fuel demand. East Kalimantan’s Mahakam Delta, now a brownfield, still anchors LNG feed-gas volumes for Bontang, though output slipped to 600 MMcf/d in 2025.

The Natuna basin is estimated to hold 200 Tcf of high-CO₂ gas; TCF-level reservoirs, such as East Natuna, remain dormant pending declines in carbon-capture costs and a rise in gas prices. Central Java balances waning onshore liquids with refinery throughput gains, importing sweet crudes and blending with local Naphthenic streams to maximize middle-distillate yield. Papua’s offshore Arafura Sea prospects remain under-tested, hindered by sparse infrastructure and unresolved land tenure. Yet, the government’s new “Ring-Fence” fiscal model offers accelerated depreciation to entice drilling.

Deep-water clusters form Indonesia’s frontier, requiring 2,500-m water-depth capability, dynamic positioning rigs, and subsea trees rated to 15,000 psi. Government marine zoning ensures coexistence with tuna fisheries and coral reef conservation; exploration plans must pass environmental impact assessments that detail oil-spill modeling, waste management, and decommissioning escrow arrangements.

Competitive Landscape

The Indonesian oil and gas market is moderately concentrated, with Pertamina accounting for approximately 60% of crude and gas output. Chevron, Shell, and ExxonMobil collectively share another 20%, while the remaining balance is split among Medco, Harbour Energy, Jadestone, and independent companies.[4]Indonesia Business Post, “Pertamina Market Share,” indonesiabusinesspost.com Gross-split PSCs reduce bureaucracy, enabling nimble operators to fast-track wildcats and monetization. International majors leverage deep-water expertise and CCUS capabilities for complex reservoirs, co-venturing with local players to meet domestic-content mandates.

Technological race shapes rivalry: Schlumberger's digital-rock study at Abadi accelerates reservoir modeling, Halliburton's smart completions in Natuna raise uptime, and Baker Hughes supplies carbon-capture compressors rated at 250 bar. Pertamina invests heavily in AI, partnering with FPT Software to create a 30,000-sensor IoT mesh that has boosted recovery and reduced downtime by 12% by 2024. The small-scale LNG value chain presents growth opportunities—PGN, a Pertamina affiliate, is rolling out mini-FSRUs, while Chart Industries supplies ISO tanks for trucked LNG to Sumba's mining districts.

Fiscal policy builds protective moats: local-content thresholds of 35% for equipment, in-country fabrication yards for topsides, and mandatory knowledge transfer secure differentiators for incumbents. Environmental credentials are now considered in tender evaluations, with CCS participation, methane-intensity targets, and ESG disclosure influencing license awards.

Indonesia Oil And Gas Industry Leaders

-

PT Pertamina

-

Chevron Corporation

-

Petroliam Nasional Berhad

-

Exxon Mobil Corporation

-

PT Medco Energi Internasional Tbk

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: Conrad Asia Energy, a natural gas company based in Singapore, has shared operational and resource updates for its two production sharing contracts (PSCs) in Indonesia.

- July 2025: ACWA Power, Danantara, and Pertamina pledged USD 10 billion for 5 GW of hybrid renewable-gas projects across Indonesia.

- April 2025: Jadestone Energy inaugurated the USD 130 million Akatara Gas Project offshore East Java, commencing at 15 MMcf/d with plans to reach a plateau of 25 MMcf/d.

- November 2024: BP green-lit the USD 7 billion Tangguh UCC, blending 11.4 MTPA liquefaction expansion with Southeast Asia’s largest CCUS hub capable of injecting 2.5 million t/y CO₂.

Indonesia Oil And Gas Market Report Scope

Oil and natural gas markets are major industries in the energy market and play an influential role in the global economy as the world's primary fuel source. The processes and systems involved in producing and distributing oil and gas are highly complex, capital-intensive, and require state-of-the-art technology.

The Indonesian oil and gas market is segmented by sector into upstream, midstream, and downstream. The market sizing and forecasts have been done based on volume for all above segments.

By Sector

| Upstream |

| Midstream |

| Downstream |

By Location

| Onshore |

| Offshore |

By Service

| Construction |

| Maintenance and Turn-around |

| Decommissioning |

| By Sector | Upstream |

| Midstream | |

| Downstream | |

| By Location | Onshore |

| Offshore | |

| By Service | Construction |

| Maintenance and Turn-around | |

| Decommissioning |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Indonesia oil and gas market in 2025?

The Indonesia oil and gas market size is valued at USD 13.88 billion in 2025 and is projected to grow 5.44% CAGR to 2030.

Which segment leads sector-wise revenue?

Upstream activities dominate with 72.8% share in 2024, supported by new field developments and enhanced recovery projects.

What is driving offshore investment in Indonesia?

Deep-water discoveries, favorable gross-split PSC terms, and FPSO adoption push offshore growth at a 6.1% CAGR through 2030.

Why is Pertamina central to Indonesia’s energy sector?

Pertamina holds about 60% of national oil and gas output, operates refineries, and spearheads digital and CCUS initiatives to extend field life.

How is Indonesia balancing LNG exports with domestic demand?

While legacy plants feed North-East Asia, small-scale LNG infrastructure backed by USD 1.5 billion in funding is diverting gas to remote domestic markets.

What role does CCUS play in Indonesia’s future production?

Projects like BP’s Tangguh UCC integrate 2.5 million t/y CO₂ storage, enhancing mature-field economics and aligning with net-zero commitments.

Page last updated on: