Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

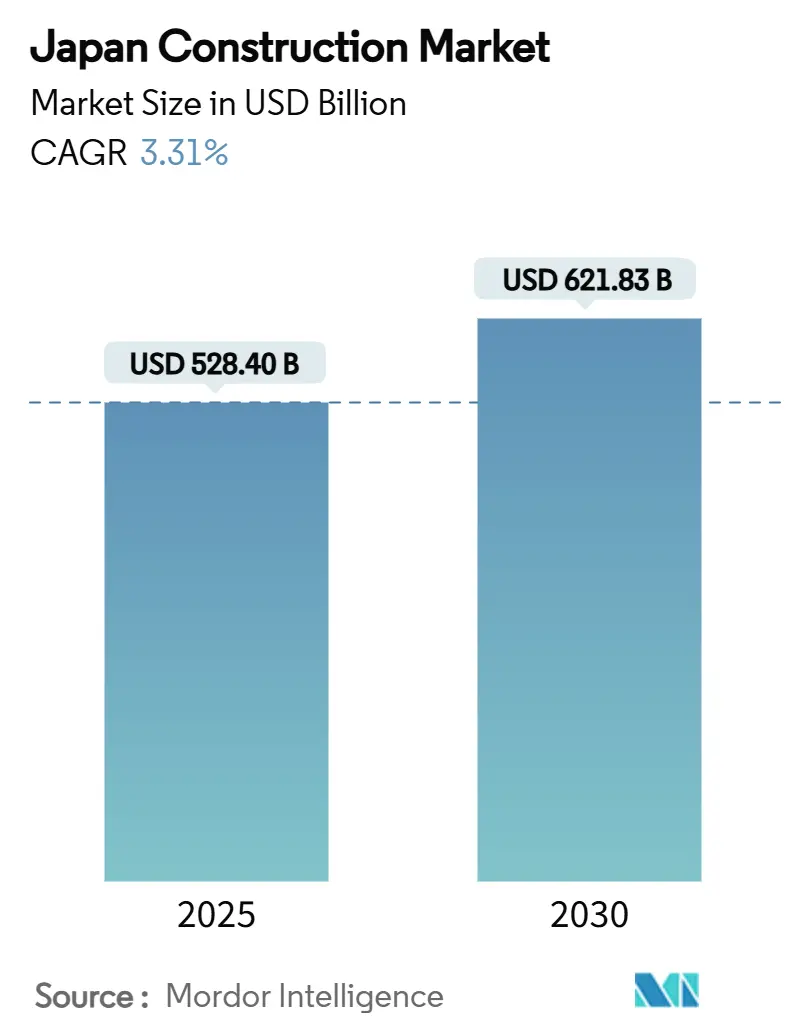

| Market Size (2025) | USD 528.40 Billion |

| Market Size (2030) | USD 621.83 Billion |

| Growth Rate (2025 - 2030) | 3.31% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Japan Construction Market Analysis by Mordor Intelligence

The Japan Construction Market size stands at USD 528.4 billion in 2025 and is forecast to reach USD 621.83 billion by 2030, translating into a 3.31% CAGR over the period. The outlook reflects a stable demand base anchored in public-works spending, stringent seismic regulations, and sustained housing requirements in the Tokyo metropolitan area. Government commitment to long-range resilience, illustrated by the National Resilience Plan’s JPY 20 trillion (USD 137.9 billion) allocation,n assures contractors of a predictable pipeline that spans water, sewage, and disaster-mitigation assets. Momentum is reinforced by a 10 GW offshore-wind target for 2030, a digital-twin procurement mandate due in 2026, and a fast-growing prefabrication ecosystem that alleviates labor constraints. Simultaneously, higher material costs arising from yen weakness and aging craft labor pools intensify the need for technology-enabled productivity gains.

Key Report Takeaways

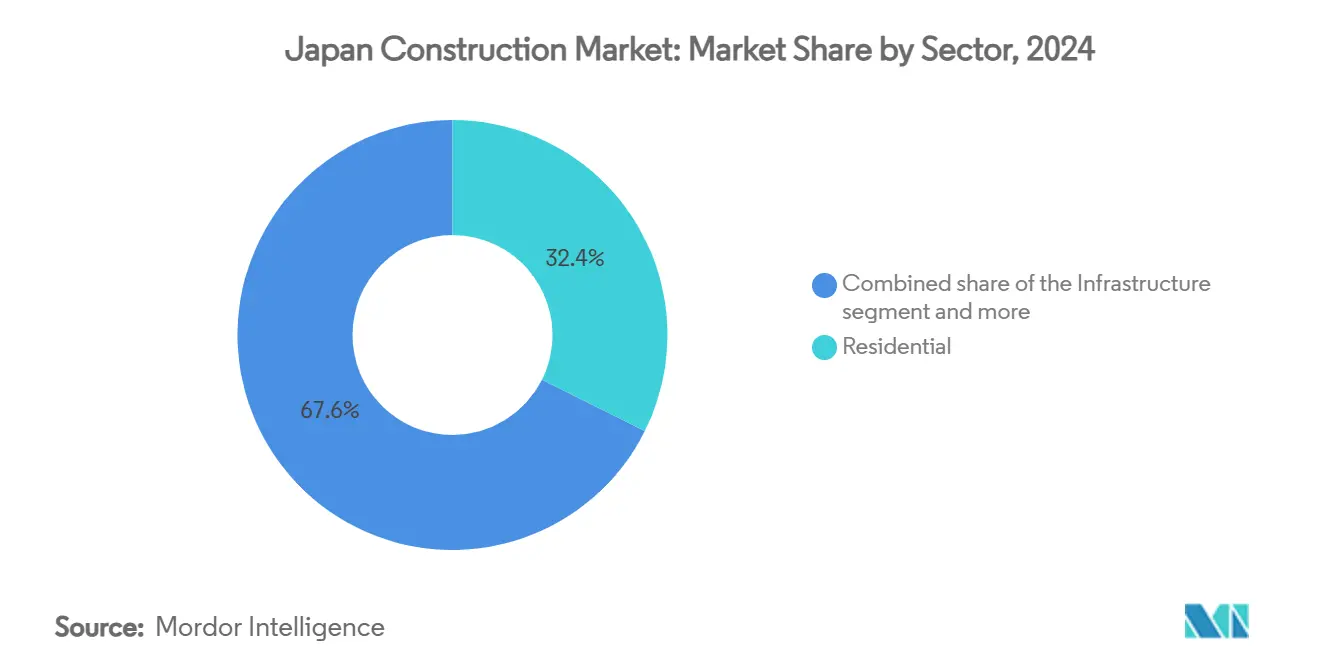

- By sector, residential construction led with 32.37% of Japan's construction market share in 2024, and it is expanding at a 4.60% CAGR through 2030.

- By construction type, new builds commanded 72.40% share of the Japan construction market size in 2024, while renovation is growing at a 3.89% CAGR to 2030.

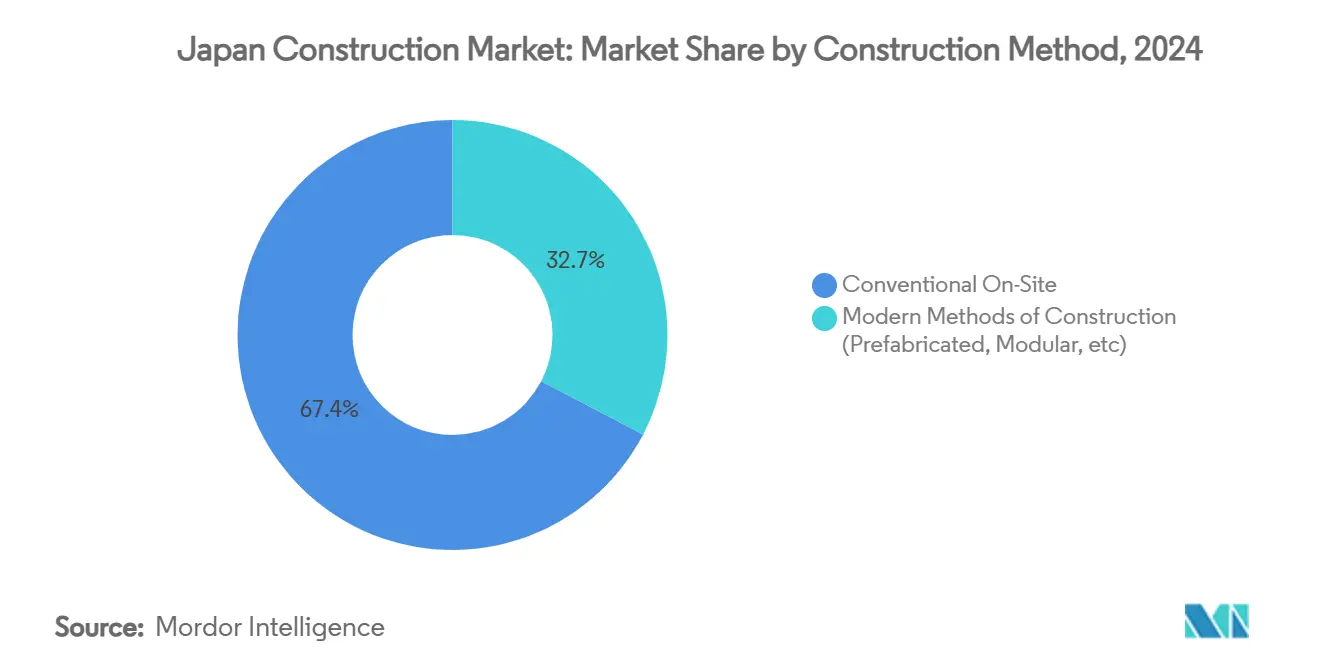

- By construction method, conventional on-site techniques held a 67.35% share in 2024, whereas modern methods are advancing at a 6.32% CAGR to 2030.

- By investment source, Public entities controlled 78.20% of project funding in 2024, yet private investment is growing briskly at a 5.88% CAGR to 2030.

- By geography, Kanto accounted for 41.28% revenue in 2024; the Rest of Japan is projected to accelerate at a 5.15% CAGR over the forecast horizon.

Japan Construction Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government stimulus & public-works spending | +0.8% | National, concentration in disaster-prone prefectures | Medium term (2-4 years) |

| Seismic retrofitting & urban redevelopment wave | +0.6% | National, priority in Tokyo, Osaka, Kansai | Long term (≥ 4 years) |

| Tokyo metropolitan housing demand pressure | +0.4% | Kanto; spillover to adjacent prefectures | Short term (≤ 2 years) |

| Renewable-energy project pipeline (offshore wind, solar) | +0.3% | Coastal prefectures—Aomori, Yamagata, Kyushu | Medium term (2-4 years) |

| Wood-based high-rise subsidies | +0.2% | Major urban centers | Long term (≥ 4 years) |

| BIM & digital-twin procurement mandate (MLIT 2026) | +0.2% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Stimulus & Public-Works Spending

Japan’s shift from reactive repairs to proactive infrastructure resilience provides a structural floor for the Japan construction market. The National Resilience Plan channels multi-year outlays into flood-control tunnels, bridge renewals, and quake-proof water pipelines, ensuring steady project flow across all prefectures. Contractors with expertise in advanced materials and seismic design benefit from specification-heavy tenders that favor specialized know-how. Smaller firms also gain entry points in niche applications such as pipe-lining and vibration-dampening devices. Overall, elevated public budgets cushion cyclical swings and support technology investments that lift sector productivity[1]Ministry of Land, Infrastructure, Transport and Tourism, “National Resilience Plan 2023–2030,” MLIT, mlit.go.jp.

Seismic Retrofitting & Urban Redevelopment Wave

Compulsory bridge and building assessments have identified 92,000 structures requiring urgent reinforcement, stimulating a multiyear retrofitting wave. Unlike earlier quake repair cycles, projects now integrate energy efficiency, smart monitoring, and demographic adaptation elements, transforming single-purpose jobs into integrated urban renewal programs. Contractors must therefore pair structural engineering skills with sensor integration and data analytics capabilities. The emphasis on community-wide resilience fosters collaboration among builders, planners, and ICT providers, creating bundled service opportunities that expand revenue per project[2]Ministry of Land, Infrastructure, Transport and Tourism, “Urgent Bridge Repair Assessment 2024,” MLIT, mlit.go.jp.

Tokyo Metropolitan Housing Demand Pressure

Persistent economic gravitation toward Tokyo keeps residential demand high despite decentralization initiatives. Limited developable land pushes developers toward vertical and modular solutions that maximize floor-area ratios. Builders equipped for high-rise timber, 2x4 wall systems, and factory-finished modules shorten project cycles and mitigate labor limits. Affordability concerns spur creative financing and standardized components, while municipal zoning revisions encourage mixed-use towers with integrated mobility hubs. Together, these dynamics sustain the Japan construction market even as population growth stagnates.

Renewable-Energy Project Pipeline (Offshore Wind, Solar)

Offshore wind auctions awarding 1.1 GW combined capacity illustrate Japan’s accelerated clean-energy trajectory. Marine foundation work, transmission upgrades, and port facility expansions present sizeable civil-works scopes that traditional contractors can secure through joint ventures with marine specialists. Onshore, building-integrated photovoltaics expand rooftop retrofits and new commercial roofs alike. Feed-in premium frameworks extend revenue visibility, enabling EPC firms to lock in multiyear backlogs while honing green-construction credentials.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labor shortage & aging workforce | -0.7% | Nationwide; acute in rural prefectures | Long term (≥ 4 years) |

| Imported material inflation & weak yen | -0.4% | Nationwide; higher in import-dependent regions | Short term (≤ 2 years) |

| Carbon-footprint approval bottlenecks | -0.3% | Major metros | Medium term (2-4 years) |

| Zoning reforms favor renovation over new builds | -0.2% | Tokyo, Osaka, Kansai | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled-Labor Shortage & Aging Workforce

More than one-third of craft workers are over 55, and retirements outpace new entrants, constraining project capacity. April 2024 overtime curbs further reduce available man-hours, compelling general contractors to deploy autonomous earth-moving fleets, remote-controlled cranes, and AI-driven scheduling. Leading firms have demonstrated multi-machine robotic control that keeps sites active during off-peak hours, preserving output with fewer tradespeople. Concurrently, digital training modules and exoskeletons extend veteran workers’ careers, but labor scarcity remains the single biggest drag on the Japan construction market[3]Ministry of Health, Labor and Welfare, “Construction Workforce Statistical Yearbook 2024,” MHLW, mhlw.go.jp.

Imported Material Inflation & Weak Yen

An 18% spike in the producer price index for construction inputs, amplified by currency depreciation, erodes contractor margins. Builders increasingly secure hedged contracts with domestic steel mills and experiment with engineered wood, recycled aggregates, and high-strength lightweight concrete to cut import dependence. Prefabrication also improves price predictability by relocating value-added processes to controlled factories. Nonetheless, tender prices lag cost surges, forcing firms to prioritize value-engineering and collaborative procurement to remain competitive.

Segment Analysis

By Sector: Residential Dominance Drives Market Evolution

The residential arena captured the largest slice of Japan construction market share at 32.37% in 2024. Demand is concentrated in greater Tokyo, where vertical expansion and space-efficient floor plans sustain new-build activity. Prefabricated apartments shorten cycle times while meeting energy-code requirements slated for universal enforcement in 2025. In contrast, commercial construction rides e-commerce growth through logistics hubs, while infrastructure spending flows to rail capacity upgrades and coastal defenses.

The sector remains the fastest riser, charting a 4.60% CAGR. Modular high-rise systems, wood-based CLT towers, and integrated smart-home packages improve affordability and appeal to aging households seeking barrier-free environments. Commercial builders pivot toward flexible offices that combine retail and coworking zones, responding to hybrid work patterns. Infrastructure contractors integrate digital twins into bridges and tunnels, enabling predictive maintenance that lowers long-term ownership costs. Collectively, these shifts underpin a sustained expansion of the Japan construction market size for sector participants.

Note: Segment shares of all individual segments available upon report purchase

By Construction Type: Renovation Gains Strategic Importance

New construction dominated with 72.40% of Japan construction market size in 2024, yet renovation’s 3.89% CAGR signals growing strategic weight. Adaptive reuse of office blocks into residential units trims carbon footprints and sidesteps land scarcity in dense cores. Municipal incentives for seismic upgrades unlock grants that make overhauls financially viable.

Renovation specialists excel in structural diagnostics, asbestos abatement, and integration of energy-conserving HVAC systems. Meanwhile, new-build projects advance through design-for-manufacture approaches that modularize pipelines, wall panels, and façade elements. The interplay between renovation and new construction diversifies revenue streams and cushions cyclical swings across the Japan construction market.

By Construction Method: Modern Methods Transform Industry Practices

Conventional on-site work retained a 67.35% share in 2024, but modern methods are accelerating at a 6.32% CAGR as firms confront labor shortages and schedule compression. Factory-built modules ensure tighter tolerances and waste reductions that cut embodied carbon, aligning with city-level emission caps.

Large contractors invest in automated rebar manufacturing and robotic welding lines, while SMEs access shared prefabrication hubs to climb the learning curve. Digital field-tracking platforms link fabrication plants with job sites, shrinking rework rates and raising profitability. The shift to modern methods elevates productivity, bolsters quality, and reinforces the competitiveness of the Japan construction market.

By Investment Source: Private Sector Momentum Builds

Public agencies supplied 78.20% of project capital in 2024, anchoring the Japan construction market against macro shocks. National resilience works, urban drainage tunnels, and renewable-energy installations dominate the tender roster.

Private investment, however, is rising at 5.88% CAGR as investors seek stable, inflation-hedged assets. Public–private partnerships streamline risk allocation, while green bonds finance zero-carbon buildings and data centers. Technology-oriented funds favor projects that employ building information modeling and prefabrication, reinforcing innovation across the value chain.

Geography Analysis

Kanto maintained its commanding 41.28% foothold in 2024, fueled by megaprojects such as rail extensions, high-rise condominiums, and data corridors. Early adoption of BIM and net-zero building codes positions the region as a national trendsetter. Government outlays for seismic retrofits of expressways and municipal shelters further extend the Japan construction market size within Kanto.

Chubu, Kansai, and Kyushu contribute mid-tier volumes through airport expansions, smart logistics parks, and hydrogen demonstration plants. Regional authorities bundle smaller projects into multiyear packages, offering predictable backlogs to medium-sized contractors. Local universities partner with builders on timber-tower prototypes, reflecting wood-subsidy uptake.

The Rest of Japan is the growth pacesetter at a 5.15% CAGR. Hokkaido’s onshore wind farms, Tohoku’s recovery infrastructure, and Shikoku’s tourism-linked resorts diversify opportunity sets. Rural prefectures pilot drone-based surveying and remote inspection under MLIT grants, lowering entry costs for SMEs. This geographic diffusion stabilizes workloads and broadens the reach of the Japan construction market.

Competitive Landscape

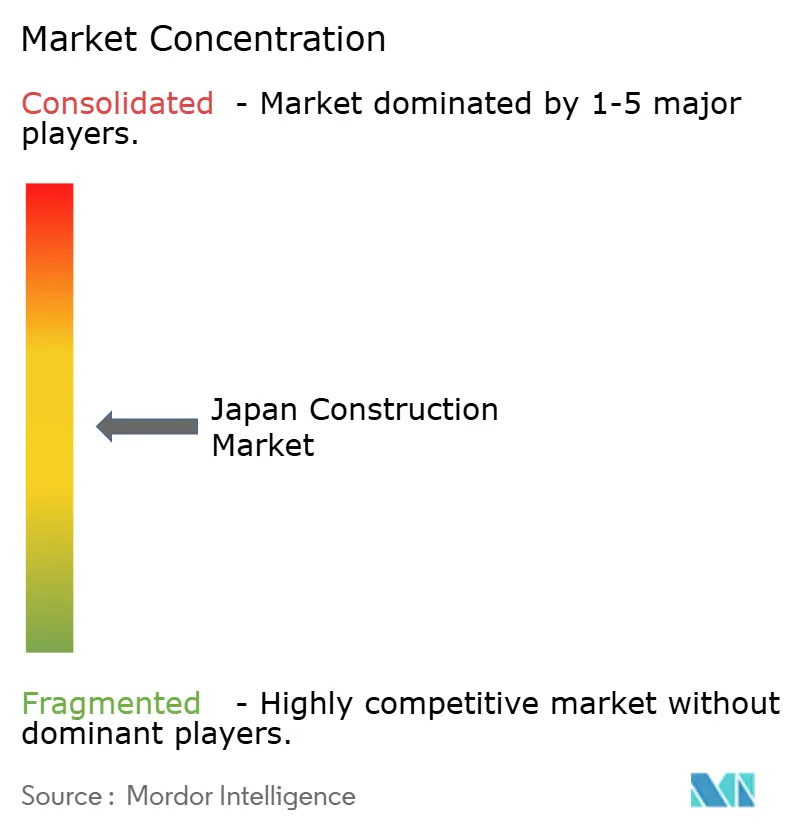

The market displays moderate concentration, with Obayashi, Kajima, Shimizu, and Taisei forming a technology-intensive oligopoly. These firms command integrated design-build services, proprietary prefabrication yards, and AI-driven site-control platforms that differentiate them beyond pure scale. Mid-tier players cluster in regional infrastructure, tapping local relationships and niche capabilities.

Strategic themes revolve around digital twins, autonomous equipment fleets, and low-carbon construction materials. Obayashi’s battery-powered excavators cut site emissions; Kajima’s multi-machine control system maintains productivity with lean crews; and Shimizu’s timber-skyscraper prototypes position it for wood-subsidy projects. International diversification also features, as majors pursue Southeast Asian rail and Middle Eastern smart-city contracts to offset domestic growth limits.

Emergent competitors include technology firms offering robotics-as-a-service and prefab startups leveraging vertically integrated supply chains. Joint ventures such as INFRONEER Strategy & Innovation pair consulting analytics with field execution, widening the innovation funnel.

Japan Construction Industry Leaders

-

Obayashi Corporation

-

Kajima Corporation

-

Shimizu Corporation

-

Taisei Corporation

-

Takenaka Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Taisei and Toyo completed a strategic merger to reinforce earnings resilience and broaden project portfolios.

- April 2025: The revised 2x4 building code came into force, tightening energy-efficiency and structural criteria.

- February 2025: INFRONEER Holdings and Accenture launched INFRONEER Strategy & Innovation to digitize asset management and tackle labor shortages.

- April 2024: Obayashi began deploying battery-powered backhoes, targeting a 46.2% CO2 reduction against 2019 levels.

Japan Construction Market Report Scope

Construction refers to building commercial, institutional, or residential infrastructures like bridges, buildings, roads, and other structures. The different materials used in modern-day construction include clay, stone, timber, brick, concrete, metals, and plastics, among others.

Japan's construction market is segmented by sector (residential, commercial, industrial, infrastructure (transportation), and energy and utilities).

The report offers the market sizes and forecasts in value (USD) for all the above segments. The report also covers the impact of COVID-19 on the market.

By Sector

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By Geography

| Hokkaido |

| Tohoku |

| Kanto (Tokyo) |

| Chubu (Nagoya) |

| Kansai (Osaka) |

| Rest Of Japan |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | Hokkaido | |

| Tohoku | ||

| Kanto (Tokyo) | ||

| Chubu (Nagoya) | ||

| Kansai (Osaka) | ||

| Rest Of Japan | ||

Key Questions Answered in the Report

How large is the Japan construction market in 2025?

It is valued at USD 528.4 billion and is forecast to reach USD 621.83 billion by 2030.

What is the expected CAGR for Japan’s construction sector to 2030?

A steady 3.31% CAGR is projected over the 2025-2030 period.

Which segment is growing the fastest across Japanese construction?

Residential building shows the highest growth, advancing at a 4.60% CAGR through 2030.

Why are modern construction methods gaining traction?

Prefabrication and modular systems reduce labor needs, improve quality, and shorten schedules, making them attractive amid workforce shortages.

How does public works spending affect contractors?

The National Resilience Plan supplies multi-year, specification-rich projects that stabilize order books and reward firms with advanced engineering capabilities.

What regions outside Kanto present notable growth?

Hokkaido, Tohoku, and Kyushu collectively post a 5.15% CAGR thanks to renewable-energy builds, disaster-recovery works, and tourism facilities.

Page last updated on: