Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

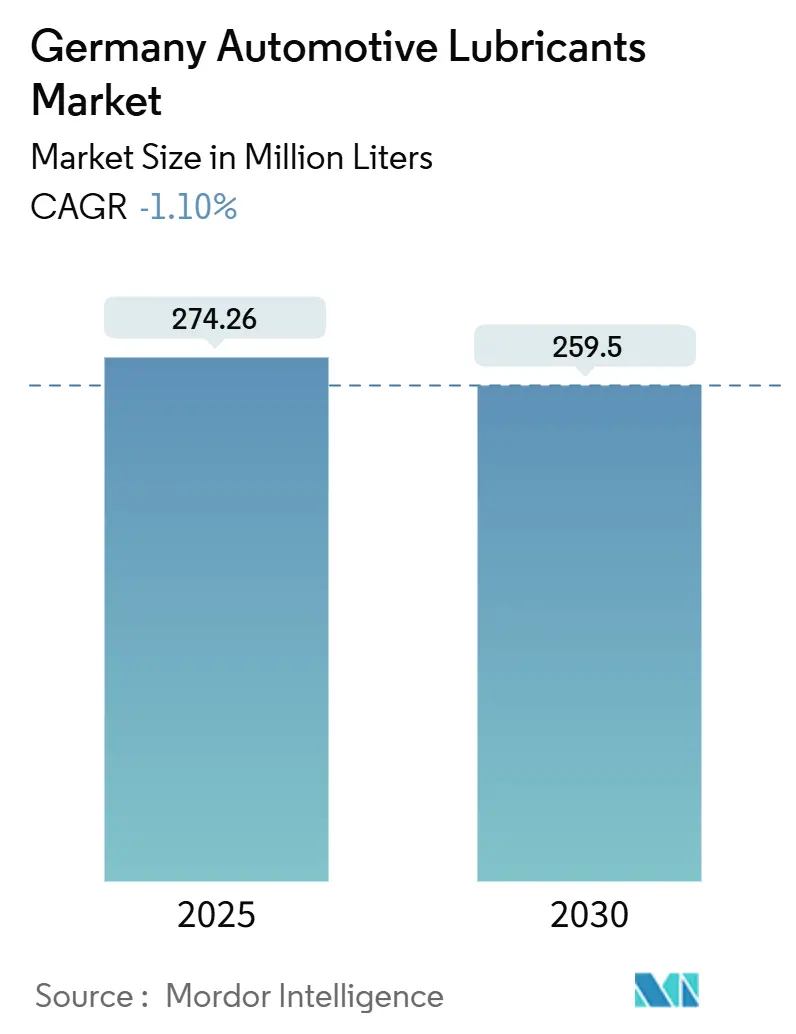

| Market Volume (2025) | 274.26 Million liters |

| Market Volume (2030) | 259.5 Million liters |

| Growth Rate (2025 - 2030) | -1.10% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Automotive Lubricants Market Analysis by Mordor Intelligence

The Germany Automotive Lubricants Market size is estimated at 274.26 million liters in 2025, and is expected to decline to 259.5 million liters by 2030, at a CAGR of -1.10% during the forecast period (2025-2030). This contraction stems from rapid electrification, which lowers the intensity of engine oil per vehicle. Even so, the industry continues to benefit from a modest rebound in domestic vehicle production, an aging car parc that lifts aftermarket volumes, and rising use of premium synthetic formulations that support value retention. Competitive pressure intensifies as suppliers pivot toward e-drive fluids, while shifts in base-oil supply, such as Shell’s Wesseling conversion, heighten input-cost volatility. Regulatory attention on packaging waste and Scope 3 emissions further reshapes product development priorities, prompting companies to invest in circular packaging and lower-carbon formulations.

Key Report Takeaways

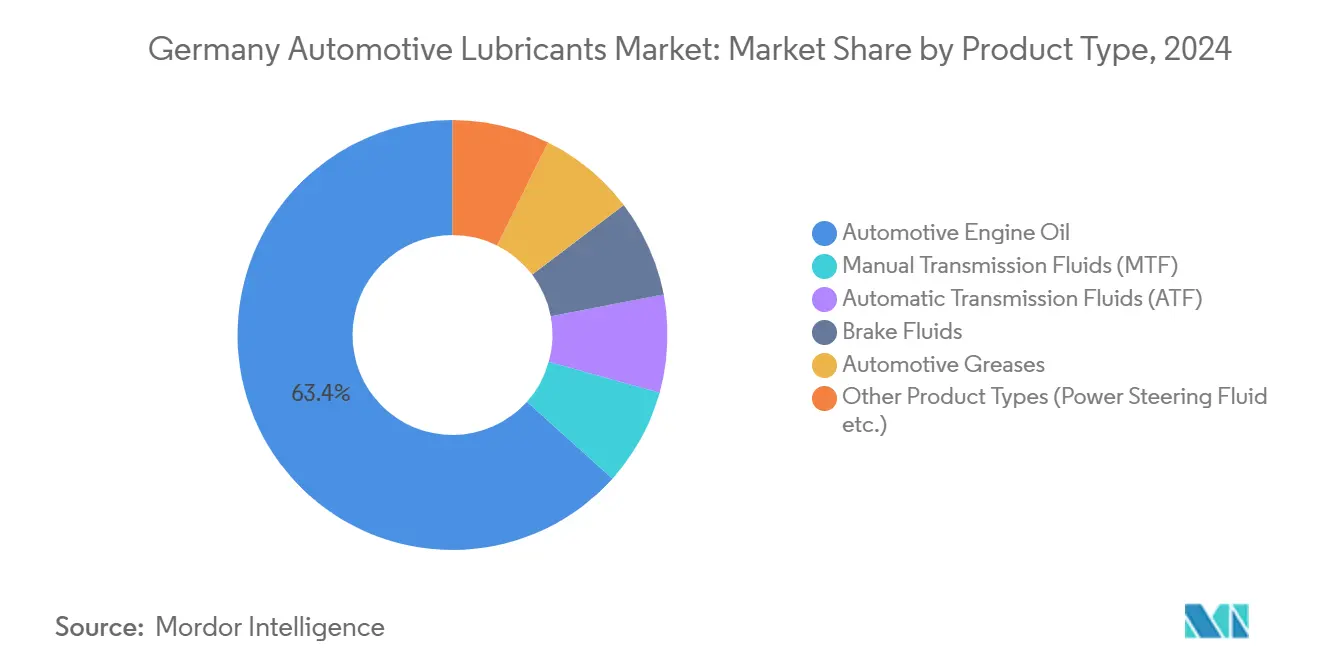

- By product type, automotive engine oil led with 63.35% of Germany's automotive lubricants market share in 2024, while automatic transmission fluids posted the sharpest drop at a –0.93% CAGR through 2030.

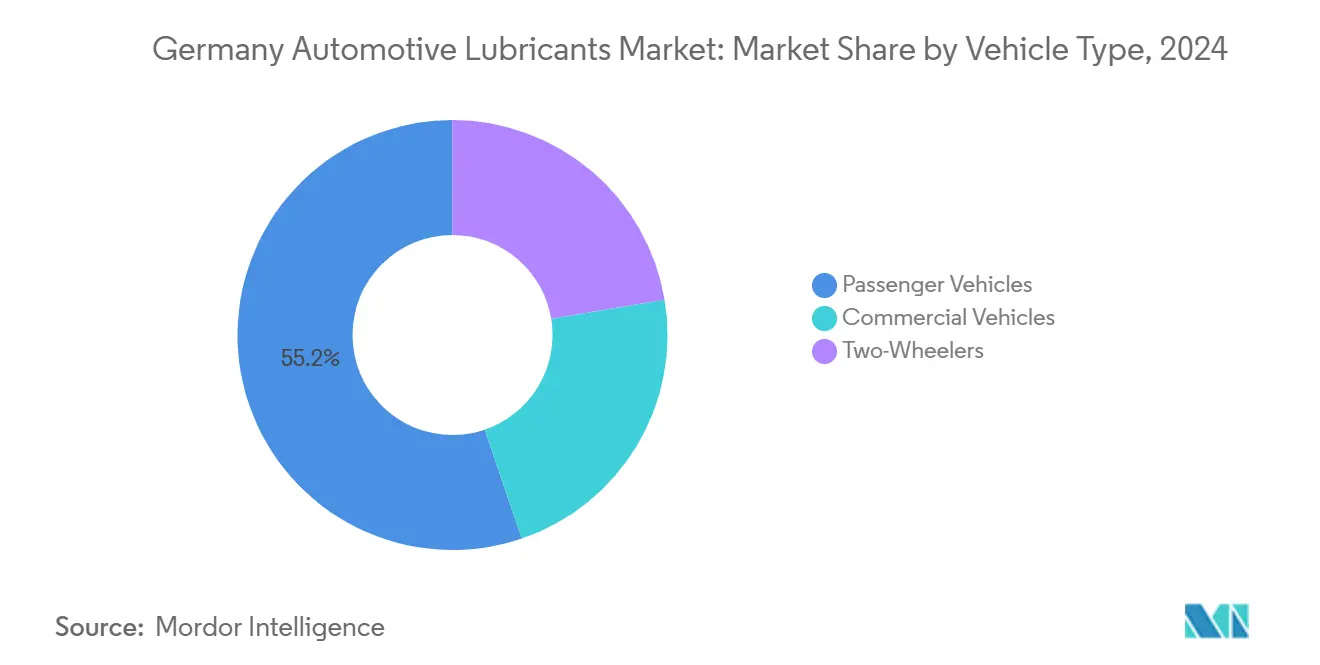

- By vehicle type, passenger vehicles accounted for 55.23% of the German automotive lubricants market size in 2024; commercial vehicles, however, recorded the most resilient outlook, with a CAGR of –0.78% to 2030.

Germany Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Revival of German light-vehicle production | +0.5% | Bavaria and Baden-Württemberg | Short term (≤ 2 years) |

| Rising penetration of synthetic low-viscosity oils | +0.3% | Nationwide premium segments | Medium term (2-4 years) |

| Aging car parc above 10 years | +0.2% | Rural and eastern regions | Medium term (2-4 years) |

| Demand for e-motor and reduction-gearbox fluids | +0.1% | Clusters near OEM plants | Long term (≥ 4 years) |

| OEM Scope-3 targets for CO₂-neutral fluids | +0.1% | Areas around major OEM headquarters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Revival of German Light-Vehicle Production Post-2024

Domestic passenger-car output rebounded in September 2025, stabilizing factory fill and early-service demand. Although volumes remain below 2019 levels, committed investments of EUR 320 billion between 2025 and 2029 indicate sustained manufacturing activity. Electrified models already command a growing share of this output, trimming lubricant litres per vehicle yet opening new opportunities in e-drive coolants. Engine-plant utilization remains below historical norms; however, improved parts availability and reorganized supply chains are expected to support a near-term increase in industrial lubricants used within assembly facilities. The revival, therefore, offers a modest buffer that slows the overall decline of the German automotive lubricants market.

Rising Penetration of Synthetic Low-Viscosity Engine Oils

OEM specifications for 0W-XX and 5W-XX grades accelerate nationwide as automakers chase fuel economy and extended-drain benefits. Synthetics provide better volatility control and sludge resistance under turbocharged, high-thermal-load conditions. ACEA approvals governed by the ATIEL Code of Practice set rigorous bench and engine tests that few small blenders can meet, limiting competitive entry. Shell’s shift to Group III output tightens Group I availability, raising feedstock premiums yet improving access to high-performance base oils required for synthetics. Premium suppliers consequently leverage brand equity and accredited labs to capture wallet share, cementing the German automotive lubricants market as a value-over-volume play.

Aging Car Parc Boosting After-Market Demand

The average vehicle age reached 10.1 years in 2024, marking the first time it had surpassed the double-digit mark on record[1]TÜV SÜD Editorial Team, “TÜV-Report 2023 Vehicles Are Getting Older,” TÜV SÜD, tuvsud.com. Older cars are more prone to oil leaks and gasket wear, prompting more frequent service intervals and a demand for seal-friendly additives. Economic uncertainty and hesitation over EV resale values lengthen ownership cycles, especially in rural and eastern states where public charging remains sparse. These factors collectively underpin a steady aftermarket that cushions the German automotive lubricants market against the faster declines on the OEM side.

Demand for E-Motor and Reduction-Gearbox Fluids

Battery electric vehicle registrations rose in the first nine months of 2025. Each BEV substitutes roughly 4-6 litres of engine oil with 2-4 litres of high-value e-drive coolant or reduction-gearbox fluid, reducing volume but improving revenue per litre. OEM specifications remain fragmented, granting early movers room to secure proprietary approvals that lock in future factory-fill contracts. Although current volumes are modest, the long-term upside aligns with electrification commitments that will reshape the German automotive lubricants market during the next decade.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing BEV fleet reducing engine-oil volume | –0.8% | Urban centers with advanced charging | Medium term (2-4 years) |

| Base-oil price volatility | –0.4% | Nationwide | Short term (≤ 2 years) |

| Stricter German packaging-waste rules | –0.2% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing BEV Fleet Reducing Engine-Oil Volume

BEV registrations increased, resulting in a reduction in annual engine oil demand. Urban areas with dense charging hubs already show double-digit declines in quick-lube traffic. OEM spending commitments favor battery assembly and electric drivetrains, ensuring that engine manufacturing will continue to shrink. Lubricant marketers must therefore retool portfolios toward e-drive fluids, greases for thermal gap fillers, and coolant blends compatible with silicone-free materials. Failing to adapt will expose them to lasting volume loss in the German automotive lubricants market.

Base-Oil Price Volatility

Shell’s EUR 200 million conversion of Wesseling to Group III output removed significant Group I and II supply, pushing blend-cost indices up by double digits in early 2025[2]Shell Communications, “Shell Converts Wesseling Refinery to Group III Output,” Shell, shell.com. Crude swings are transmitted into base-oil prices with a time lag, complicating inventory valuation and pricing strategies. Small blenders lacking long-term supply agreements face the heaviest margin compression, accelerating calls for industry consolidation. The volatility also prompts reformulation to reduce reliance on virgin oil, but such changes require fresh OEM approvals, which take time and capital.

Segment Analysis

By Product Type Engine Oil Dominance Faces Gradual Erosion

Automotive engine oil accounted for 63.35% of Germany's automotive lubricants market. The segment benefits from the still-dominant internal-combustion fleet and gains further support from older vehicles that require shorter drain intervals. Synthetic 0W-20 and 0W-30 formulations capture premium shelf space due to OEM fuel-economy directives and the availability of Group III base oils. Yet the decline in passenger-car engine builds and the replacement of automatic transmissions with single-speed gearboxes in BEVs undercut long-term volume. Manual transmission fluids and brake fluids account for a modest slice of demand, showing relatively stable trends tied to routine service schedules. Automotive greases serve wheel bearings and chassis points, with a limited impact on electrification, while niche products, such as hydraulic and steering fluids, decline in tandem with the adoption of electronic braking and steering systems. Altogether, the mix shift merely slows rather than stops the decline in volume in the German automotive lubricants market.

Automatic transmission fluids are expected to represent the steepest contraction, -0.93% CAGR, mirroring the rapid decline in the use of multi-gear boxes. Other product categories see uneven trajectories: brake fluids track the size of the rolling fleet, greases follow component counts in heavy-duty sectors, and emergent e-drive coolants acquire incremental litres that partially offset traditional losses. Over the forecast horizon, synthetic share rises faster than total litres decline, allowing value retention even as Germany's automotive lubricants market size contracts in absolute terms.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Vehicle Type Passenger Dominance with Commercial Resilience

Passenger vehicles accounted for 55.23% of Germany's automotive lubricants market size in 2024. Urban driving cycles, higher annual mileage, and older vehicle profiles continue to sustain service frequencies despite the adoption of electric vehicles. Synthetic adoption skews heavily toward premium passenger brands, boosting average revenue per litre. Nevertheless, BEV penetration already hits 27% of new passenger registrations, signaling a faster erosion of engine oil volumes in this segment than elsewhere. Two-wheeler demand remains niche and relatively stable, anchored by leisure motorcycling culture and limited electric uptake.

Commercial vehicles exhibit greater resilience, contracting at a rate of just –0.78% CAGR through 2030. Diesel trucks still dominate freight corridors, each needing 15-25 litres of heavy-duty engine oil at every change. Extended drain intervals partly counteract litre growth, yet absolute volume remains meaningful. Electrification proceeds cautiously in this class because battery weight impinges on payload economics, so lubricant suppliers maintain a dependable base here. Fleet operators also gravitate to telematics-driven maintenance scheduling, fostering partnerships for predictive oil-analysis services that support competitive differentiation within the German automotive lubricants market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Germany’s automotive hubs shape regional lubricant demand profiles. Bavaria and Baden-Württemberg house premium OEM headquarters and most final-assembly plants, driving high volumes of first-fill synthetics and creating sizable offtake for adjacent component manufacturers. North Rhine-Westphalia is feeling the immediate impact of Shell’s refinery switch, which is tightening traditional base-oil availability but improving access to Group III stocks for high-tier blends. Northern ports in Hamburg and Bremen facilitate imports that mitigate local shortages, but also incur additional logistical costs.

Urban centers such as Berlin, Hamburg, and Munich are registering the fastest BEV uptake, owing to their dense charging infrastructure and environmental zone policies. These cities, therefore, see the steepest declines in quick-lube visits and retail oil sales. Rural and eastern Länder retain older internal-combustion fleets, sustaining aftermarket volumes and supporting independent service shops. Workshop density correlates with fleet age, reinforcing the aftermarket importance of the eastern regions within the German automotive lubricants market.

Component manufacturing footprints also matter. Transmission and axle plants clustered in the south demand specialty greases and process oils, while battery gigafactories emerging in Brandenburg and Lower Saxony spur interest in dielectric coolants and fire-safe fluids. Uniform DIN standards ensure nationwide product quality; however, procurement preferences differ. Southern OEMs tend to rely on long-term tier-one contracts, whereas northern independent workshops prioritize price and accessibility.

Competitive Landscape

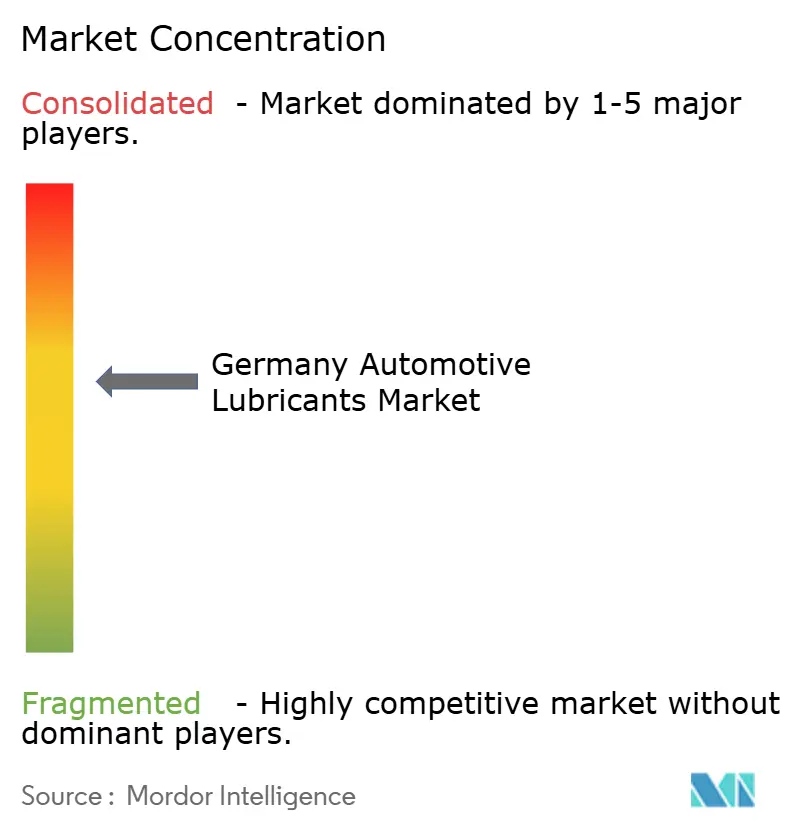

Market concentration is moderately consolidated, with a core group of multinationals and national champions accounting for the bulk of the litres sold. FUCHS, LIQUI MOLY, Shell, and TotalEnergies leverage multi-channel distribution networks and long-standing OEM approvals. Their embedded laboratory infrastructure enables rapid compliance with evolving ACEA and OEM requirements, while smaller firms struggle to fund equivalent validation cycles. Rivalry now centers less on volume and more on securing proprietary fill approvals, offering predictive maintenance analytics, and demonstrating life-cycle CO₂ reductions. Emerging additive suppliers with strong e-drive expertise challenge incumbents by targeting white-space formulations that lack entrenched specifications. Compliance with ATIEL’s Code of Practice raises barriers to entry, protecting established players that can document rigorous quality-management processes. Over the forecast period, these dynamics reinforce premiumization, even as the German automotive lubricants market volume trends downward.

Germany Automotive Lubricants Industry Leaders

-

Shell plc

-

BP Plc

-

FUCHS

-

TotalEnergies

-

Exxon Mobil Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: BP Plc initiated the sale of its Castrol lubricants division, valued at up to USD 10 billion, as part of a broader divestment strategy targeted for completion by 2027.

- September 2024: Chevron has announced Finke Mineralölwerk GmbH as the sole distributor of Texaco-branded lubricants in Germany. Finke, a member of the Hoyer Group, will utilize its 70 regional sales offices to distribute the entire Texaco portfolio, which includes Havoline, Delo, HDAX, and Techron.

Germany Automotive Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

By Vehicle Type

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What volume decline is expected for Germany's automotive lubricants by 2030?

Consumption is projected to fall from 274.26 million litres in 2025 to 259.50 million litres in 2030, equal to a –1.10% CAGR.

Which product type currently dominates lubricant demand in Germany?

Automotive engine oil leads with 63.35% share of the total 2024 volume, thanks to the large internal-combustion fleet.

How is electrification affecting lubricant suppliers?

Battery electric vehicles remove 4-6 litres of engine oil per car yet create demand for 2-4 litres of high-value e-drive fluids, shifting the product mix toward specialty formulations.

Why are synthetic low-viscosity oils growing in Germany?

OEMs specify 0W-XX and 5W-XX grades to improve fuel economy and extend drain intervals, while the availability of Group III base oil supports formulation quality.

Which vehicle segment shows the least contraction in lubricant volumes?

Commercial vehicles shrink at a rate of only –0.78% CAGR because freight applications continue to favor diesel powertrains that require large amounts of oil per service.

How are packaging-waste regulations influencing lubricant packaging?

New rules demand higher recycled content and deposit schemes, prompting suppliers to adopt reusable drums and recyclable plastics to remain compliant.

Page last updated on: