Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.75 Billion |

| Market Size (2026) | USD 3.94 Billion |

| Market Size (2031) | USD 5.04 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Oil and Gas Market Analysis by Mordor Intelligence

Vietnam Oil And Gas Market size in 2026 is estimated at USD 3.94 billion, growing from 2025 value of USD 3.75 billion with 2031 projections showing USD 5.04 billion, growing at 5.05% CAGR over 2026-2031.

This trajectory is rooted in Vietnam’s deliberate shift toward energy security as domestic production declines and LNG-to-power investment accelerates under the National Power Development Plan VIII. Substantial upstream commitments—exemplified by the Block B – Ô Môn development with recoverable gas exceeding 170 billion m³—harmonize with rising import alliances that secure fuel flexibility for new gas-fired generation. Offshore exploration success, deeper reservoir targets, and indigenous rig fabrication collectively reinforce capital expenditure momentum. At the same time, downstream digitalization, stricter ESG rules, and a widening industrial gas customer base in foreign direct investment (FDI) parks are expanding mid- and downstream cash flows while nudging operators toward higher-margin maintenance and turnaround services. Together, these forces cultivate a medium-term opportunity set centered on asset optimization rather than pure greenfield capacity.

Key Report Takeaways

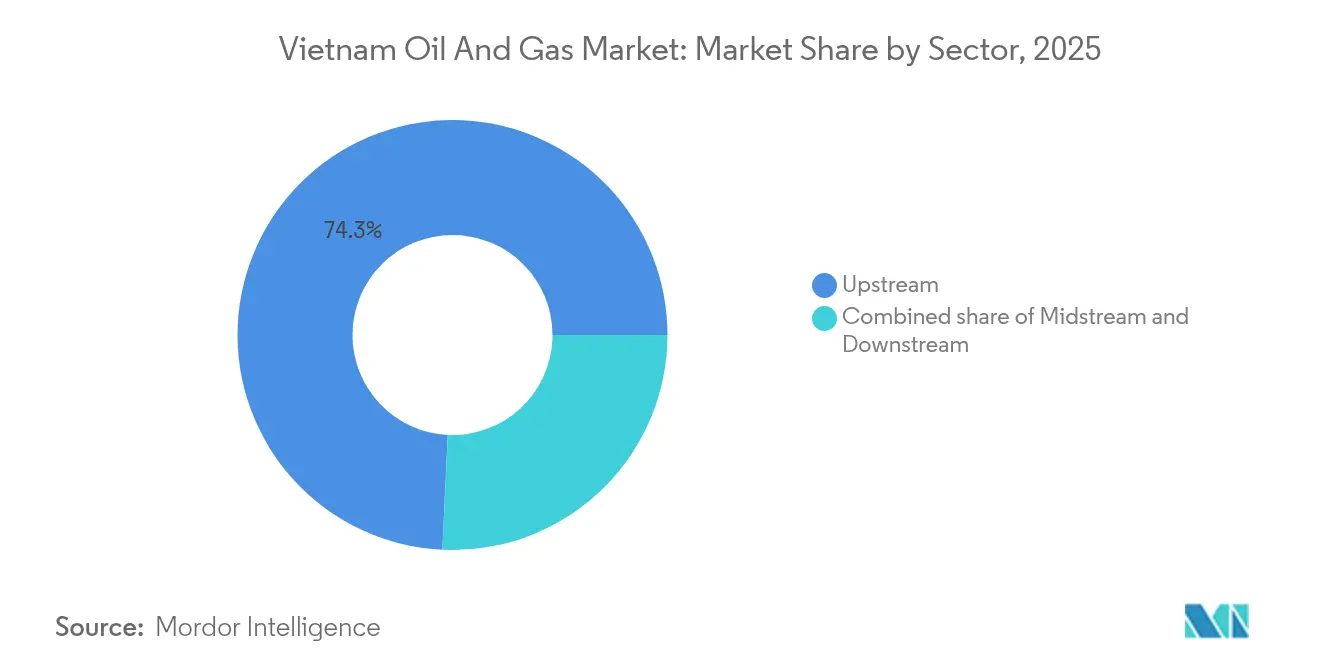

- By sector, upstream operations commanded 74.25% of the Vietnam oil and gas market share in 2025, while registering the fastest growth of 5.38% toward 2031.

- By location, offshore activities held 57.02% of the Vietnam oil and gas market share in 2025, and the segment is projected to expand at a 5.44% CAGR through 2031.

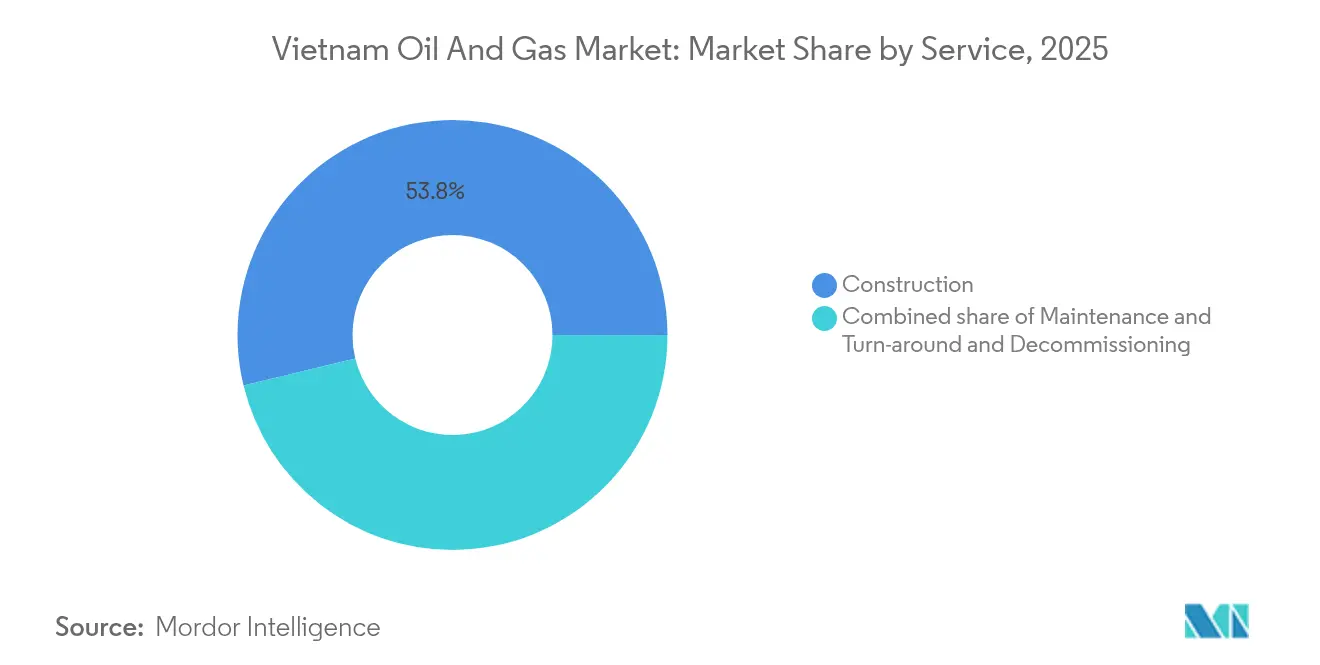

- By service, construction services accounted for 53.78% of the Vietnam oil and gas market share in 2025, whereas maintenance and turnaround services recorded the highest 5.74% CAGR outlook to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Oil and Gas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| LNG-to-Power Push Under PDP-8 | +1.8% | National, concentrated in southern provinces | Medium term (2-4 years) |

| Declining Domestic Output Spurs E&P Spend | +1.2% | Offshore blocks, Cuu Long Basin focus | Short term (≤ 2 years) |

| Gas-Fired Industrial Growth in FDI Parks | +0.9% | Ba Ria-Vung Tau, Dong Nai, Binh Duong | Medium term (2-4 years) |

| Surge in Rigs for Block B & Blue Whale | +0.7% | Southern continental shelf, Malay-Tho Chu Basin | Short term (≤ 2 years) |

| Rapid Fuel-Retail Digitisation (PVOIL Easy) | +0.4% | Urban centers, expanding nationwide | Long term (≥ 4 years) |

| U.S.–Vietnam LNG Supply Alliances | +0.6% | LNG terminals in Ba Ria-Vung Tau, Can Tho | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

LNG-to-Power Push Under PDP-8

Vietnam’s Power Development Plan VIII stipulates 22,524 MW of LNG-fired capacity by 2030, equal to roughly 10% of the national fleet.[1]Thi Bich Ngoc, “PDP-8 Charts Vietnam’s LNG Future,” theinvestor.vnVN. Domestic gas output has been declining at a rate of approximately 5% annually since 2013, yet gas demand is forecast to increase from 13 billion m³ in 2020 to exceed 34 billion m³ by 2030. Capacity additions such as the Thi Vai terminal expansion to 7 million m³ per day in March 2025 underpin that pivot. PV Gas and Excelerate Energy have signed supply memoranda that lock in U.S. cargoes from 2026, bolstering feedstock diversity for Nhon Trach 3 and 4—the country’s first fully integrated LNG-to-power chain. Together, these milestones embed LNG as a cornerstone of power-sector decarbonization.

Declining Domestic Output Spurs E&P Spend

Mature fields, such as Bach Ho and White Tiger, face rising water cuts and falling pressure, prompting operators to explore new reservoirs to stabilize the national supply. Murphy Oil committed USD 110 million for 2025—9% of its global budget—to drill Lac Da Vang and appraise Hai Su Vang, where the 1X well logged 370 ft of net pay over two reservoirs. PetroVietnam delivered Dai Hung Phase 3 twenty days ahead of schedule, demonstrating its domestic capacity to fast-track infill plans that counteract decline. Upcoming farm-outs in Blocks 15-1/05 and 15-2/17 aim to attract more risk capital by pairing production sharing terms with proven service infrastructure. Together, these programs allocate near-term cash flow to high-impact wells while extending field life through enhanced recovery.

Gas-Fired Industrial Growth in FDI Parks

Vietnam disbursed USD 21 billion of FDI in the first 11 months of 2024, much of which was invested in high-tech parks that cluster in Ba Ria-Vung Tau, Dong Nai, and Binh Duong. Clean-fuel mandates and boiler conversions in these zones are increasing pipeline throughput and securing captive gas demand for two-shift manufacturing lines. The Long Son Petrochemicals complex achieved its nameplate 1,350 KTA olefins capacity in 2024, utilizing locally sourced and imported feedgas to stabilize utilization rates for upstream producers. Industrial offtake assures baseload for new regas terminals, reducing seasonal swings tied to power dispatch. This geographic clustering also simplifies last-mile pipeline extensions, reducing capital expenditure per tonne of delivered gas.

Surge in Rigs for Block B & Blue Whale

Engineering, procurement, construction, and installation contracts for Block B – Ô Môn reached 16.7% and 34% completion by February 2025, driving a sharp uptick in jack-up and support-vessel demand. PetroVietnam Services forecasts VND 10,900 billion in revenue for 2025 from three main work packages, representing a 77% year-over-year increase that underscores the project’s service pull-through. Domestic yards have delivered Tam Dao 03, capable of 90 m water depth, and are fabricating Tam Dao 05 for 120 m, lifting local content to roughly 40% and shortening mobilization cycles. Floating production and storage tenders expected in late 2025 will further lengthen the rig queue, tightening day-rates region-wide. Collectively, these developments secure critical wellhead capacity for a resource estimated at 170 billion cubic meters of gas, placing Vietnam firmly on the radar of deepwater contractors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mature Fields & High Water-Cut Costs | -0.8% | Bach Ho, White Tiger, Cuu Long Basin | Short term (≤ 2 years) |

| Price-Capped LNG-Power Tariffs | -0.6% | National power grid, EVN pricing mechanism | Medium term (2-4 years) |

| Slow PSC & LNG Terminal Approvals | -0.5% | Regulatory bottlenecks, Prime Minister approvals | Long term (≥ 4 years) |

| South China Sea Geopolitical Risk | -0.4% | Disputed offshore blocks, exploration activities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mature Fields & High Water-Cut Costs

Historic producers like Bach Ho now record water-cut levels above 80%, inflating separation expenses and squeezing margins.[2]Minh Hai, “Tariff Caps Challenge LNG-Power Economics,” theinvestor.vn Engineering tweaks have trimmed jack-up repair cycles to five days, yet reservoir decline continues to erode volumes and elevate decommissioning liabilities. Capital-intensive enhanced recovery only partially offsets drop-offs, underscoring the need for new exploration.

Price-Capped LNG-Power Tariffs

Vietnam’s regulated tariff ceiling prevents the full pass-through of volatile LNG costs, compressing gross margins for nascent gas-fired plants. With spot cargo prices occasionally doubling long-term averages, plant operators face negative spreads that deter lenders from backing future units. Draft decrees propose indexation tweaks, yet political sensitivity around consumer bills delays implementation, sustaining uncertainty for power-purchase-agreement negotiations. Developers must therefore either lock in long-term supply or seek government guarantees, both of which add transaction complexity and delay final investment decisions. The tariff cap thus tempers LNG demand growth despite strong policy rhetoric.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Upstream Dominance Drives Market Growth

The Vietnam's oil and gas upstream segment accounted for 74.25% of market share in 2025 and is forecast to compound at a 5.38% CAGR to 2031, driven by deepwater spending on projects such as Block B – Ô Môn and Murphy Oil's Lac Da Vang program. This spending surge underwrites appraisal drilling that targets recoverable volumes exceeding 100 million barrels of oil equivalent (boe) and consolidates Vietnam's lead in the oil and gas market for exploration and production. Ongoing reservoir management at White Tiger and Phase 3 of Dai Hung exemplify the shift from primary recovery to secondary techniques, which prolong field life and sustain taxable output.

While midstream subsea pipelines and LNG reception facilities link offshore flows to urban demand centers, downstream refiners at Nghi Son and Dung Quat add capacity headroom from 6.5 million t/y to nearly 7.5 million t/y. Digital twins and AI-driven yield optimization reduce energy intensity and curtail off-spec volumes, thereby increasing profit per barrel despite stricter environmental regulations under the 2020 Environmental Protection Law.

By Location: Offshore Operations Lead Market Expansion

Offshore wells delivered 57.02% of the Vietnam oil and gas market in 2025 while charting a 5.44% CAGR outlook, anchored by the Cuu Long and Malay-Tho Chu basins, plus Blue Whale’s advancement toward. The latest Hai Su Vang-1X encounter totaled 370 ft of net pay and validated high-porosity Miocene sands. Local yards have launched Tam Dao-class jack-ups, rated for 120 m water depth, which are trimming foreign rig imports and lowering capital expenditure per well.

Onshore assets are centered around trunk pipelines that supply Kien Giang power plants and the Ca Mau fertilizer complex. Expansion work along Nam Con Son continues to lift throughput ceilings, while Right-of-Way disputes and Extended Producer Responsibility rules raise compliance workloads for contractors.

By Service: Construction Leads While Maintenance Accelerates

Construction retained 53.78% of the Vietnam oil and gas market in 2025 thanks to mega EPCI packages for Block B – Ô Môn and Long Son Petrochemicals. Localization rates of nearly 40% on Tam Dao-series jack-ups demonstrate a growing domestic fabrication muscle, which translates into cost savings and faster project cycles.

Maintenance and turnaround services, however, are projected to post the fastest 5.74% CAGR to 2031, as operators prioritize uptime. Predictive analytics within PV Gas have reduced unplanned downtime by 15% and extended refinery run lengths, illustrating the segment’s margin-rich prospects.

Geography Analysis

Southern waters continue to anchor the Vietnamese oil and gas market, with the Malay-Tho Chu mega-gas hub and the prolific Cuu Long Basin accounting for more than 80% of the remaining 2P reserves. Rig clusters in Vung Tau underpin rapid mobilization and slash logistics costs. Northern provinces mainly absorb imported LNG for power and industrial boilers, reflecting the consumption-heavy tilt in Hanoi’s manufacturing corridor.

Environmental regulations have nationwide reach. All 2,166 heavy emitters, including refineries and gas plants, must register annual greenhouse inventories and comply with the 2050 net-zero pledge. Central Vietnam’s emerging LNG sites at Da Nang and Nghi Son diversify entry channels and relieve congestion in the south.

Territorial tension in select South China Sea blocks moderates frontier exploration but leaves core producing zones undisturbed, thanks to proximity to undisputed waters and partner diversification involving Murphy Oil, SK Earthon, and PVEP.

Competitive Landscape

PetroVietnam remains the anchor tenant, holding legal pre-emption rights, while foreign majors enter through production-sharing contracts, subject to approval by the Prime Minister. The regulatory construct creates a moderately concentrated arena where technical collaboration, local content pledges, and ESG acumen supersede price as the primary differentiator.

Digital transformation provides a first-mover advantage: AI seismic interpreters now map subsurface faults with 80% certainty, reducing dry-well risk and cumulative spend. Maintenance specialists exploiting predictive analytics gain preferred-supplier status as asset integrity tops operator agendas.

White-space opportunities favor mid-tier service firms adept at turnarounds and decommissioning, a niche growing faster than greenfield construction. Free-trade frameworks under CPTPP and EVFTA safeguard export routes for condensate and petrochemicals but do not override state shareholding ceilings that cap new entrants.

Vietnam Oil and Gas Industry Leaders

Vietnam Oil & Gas Group (PetroVietnam)

Petrolimex Group

PetroVietnam Gas JSC (PV GAS)

PetroVietnam Oil (PVOIL)

Binh Son Refining & Petrochemical (BSR)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Petrolimex signed MOUs with U.S. ethanol suppliers to deepen alternative-fuel trade.

- March 2025: PV Gas raised Thi Vai regas capacity to 7 million m³/day and sealed Excelerate LNG supply from 2026.

- February 2025: Murphy Oil earmarked USD 110 million—9% of its global capital expenditures—for Lac Da Vang and exploration drilling, guiding first oil production by Q4 2026.

- January 2024: Technip Energies achieved final acceptance for Long Son Petrochemicals’ 1,350 KTA steam cracker, confirming Vietnam’s first olefins complex at full tilt.

Vietnam Oil and Gas Market Report Scope

The scope of the Vietnamese oil and gas market includes:

By Sector

| Upstream |

| Midstream |

| Downstream |

By Location

| Onshore |

| Offshore |

By Service

| Construction |

| Maintenance and Turn-around |

| Decommissioning |

| By Sector | Upstream |

| Midstream | |

| Downstream | |

| By Location | Onshore |

| Offshore | |

| By Service | Construction |

| Maintenance and Turn-around | |

| Decommissioning |

Key Questions Answered in the Report

How large is the Vietnam oil and gas market in 2026?

The Vietnam oil and gas market size is USD 3.94 billion in 2026 with a 5.05% CAGR projection to 2031.

Which segment grows the fastest toward 2031?

Maintenance and turnaround services are projected to post the highest 5.74% CAGR through 2031.

What share do offshore projects hold in the national portfolio?

Offshore operations accounted for 57.02% of Vietnam oil and gas market share in 2025 and remain expansion leaders.

How does PDP-8 influence gas demand?

PDP-8 mandates 22,524 MW of LNG-fired capacity by 2030, underpinning demand growth from 13 billion m³ in 2020 to more than 34 billion m³ by 2030.

Which foreign company committed the largest 2025 investment?

Murphy Oil allocated USD 110 million to Vietnamese assets, representing 9% of its global budget.

Page last updated on: