Video Conferencing Hardware Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

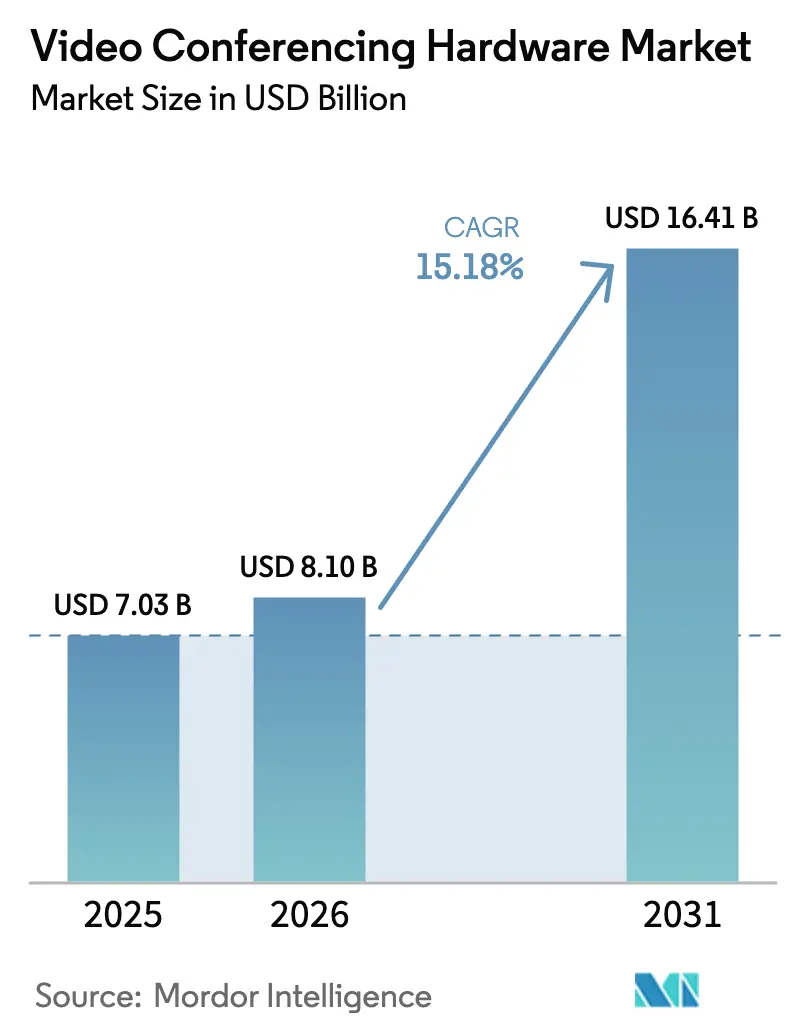

| Market Size (2026) | USD 8.1 Billion |

| Market Size (2031) | USD 16.41 Billion |

| Growth Rate (2026 - 2031) | 15.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Video Conferencing Hardware Market Analysis by Mordor Intelligence

The video conferencing hardware market size was valued at USD 7.03 billion in 2025 and estimated to grow from USD 8.1 billion in 2026 to reach USD 16.41 billion by 2031, at a CAGR of 15.18% during the forecast period (2026-2031). Robust growth is fueled by permanent hybrid-work policies, rapid AI feature commoditization, and expanding enterprise security mandates that keep on-premise codecs relevant alongside cloud-first solutions. Integrated collaboration bars, AI-enabled USB endpoints, and energy-efficient designs are rewriting procurement criteria as organizations prioritize interoperability, total cost of ownership, and ESG compliance. Strategic consolidation exemplified by HP’s purchase of Poly has sharpened competitive intensity, while semiconductor volatility and BYOD-centric cultures inject measured risk into the otherwise upbeat demand outlook.[1]Source: HP Inc., “HP Inc. Completes Acquisition of Poly,” HP.com

Key Report Takeaways

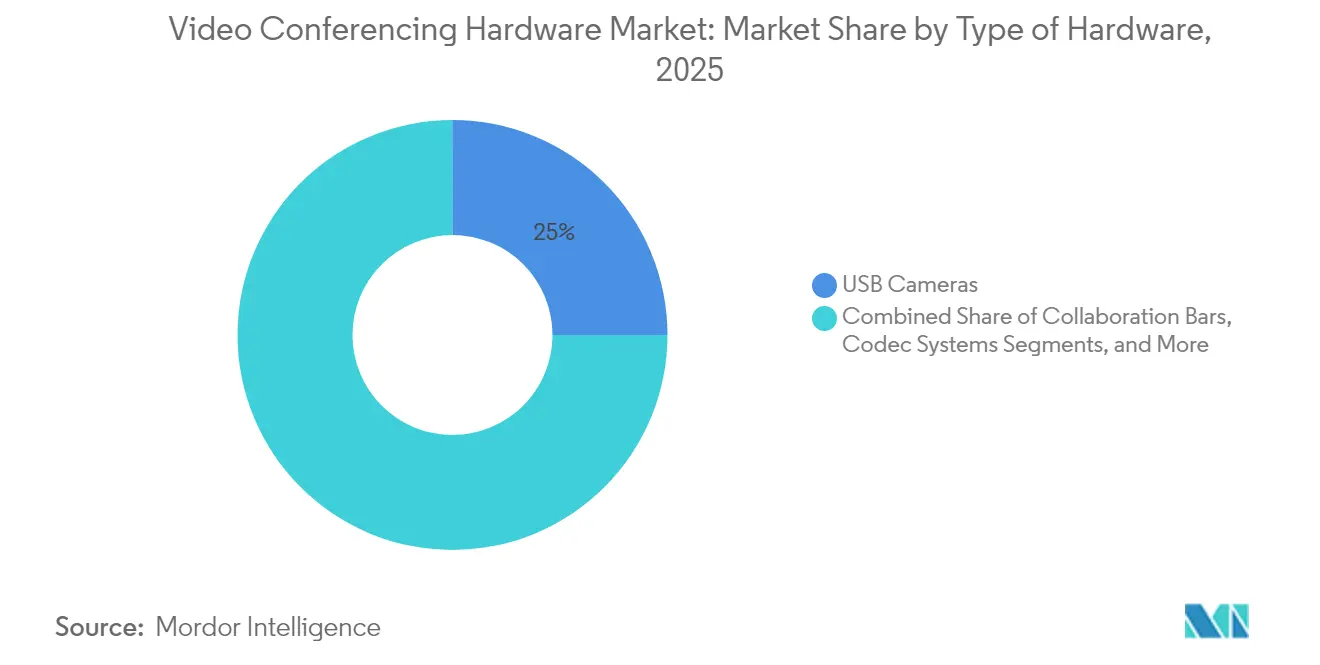

- By hardware type, USB cameras led with a 25.02% share of the video conferencing hardware market in 2025, and collaboration bars recorded the highest projected CAGR of 16.21% through 2031.

- By end user, commercial spaces held a 39.52% share of the video conferencing hardware market size in 2025, and healthcare facilities are expected to advance at a 16.74% CAGR through 2031.

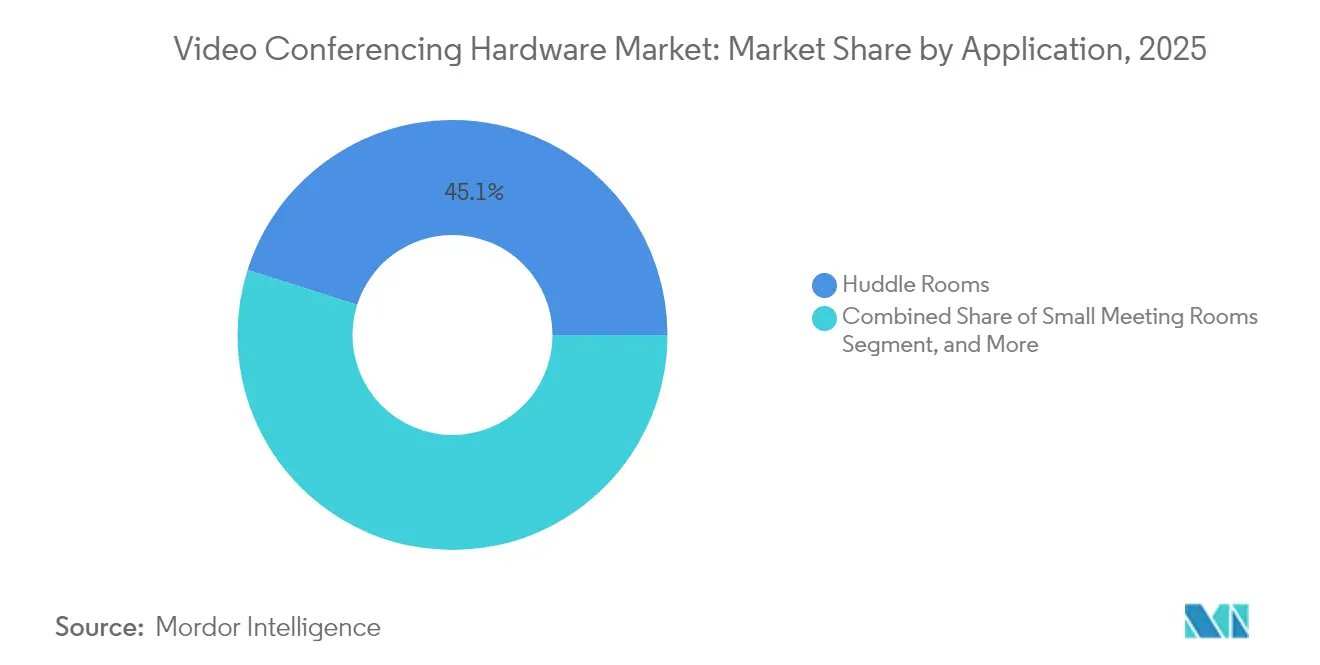

- By application, huddle rooms are forecasted to command a 45.12% share of the video conferencing hardware market size in 2025 and are expected to expand at a 16.48% CAGR between 2026 and 2031.

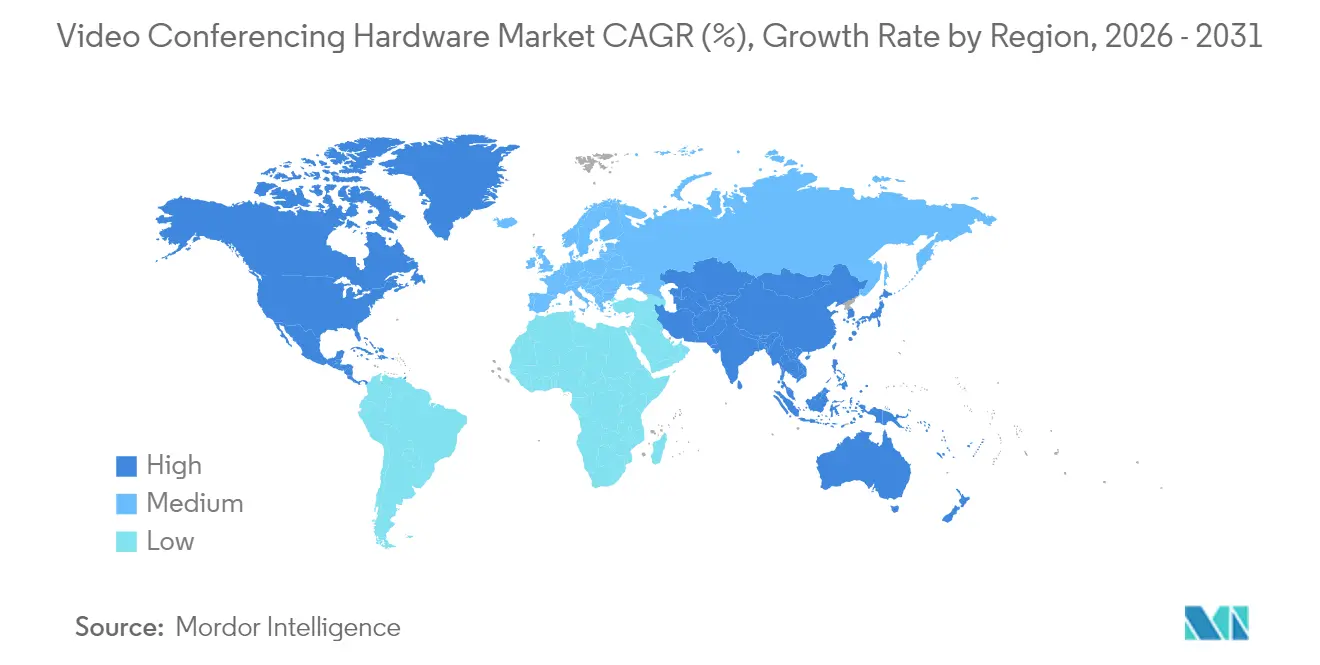

- By geography, North America captured 35.12% of the video conferencing hardware market share in 2025, and Asia-Pacific is forecast to post a 16.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Video Conferencing Hardware Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Proliferation of hybrid-work policies | +4.2% | Global – strong in North America and Europe | Medium term (2-4 years) |

| Cost-effective USB-based endpoints | +3.1% | Global – particularly strong in Asia-Pacific emerging markets | Short term (≤ 2 years) |

| Rising huddle-room deployments | +2.8% | North America and Europe corporate sectors | Medium term (2-4 years) |

| AI-enabled auto-framing and transcription | +2.4% | Global – led by technology-forward enterprises | Long term (≥ 4 years) |

| ESG-driven upgrade cycles | +1.7% | Europe and North America regulatory markets | Long term (≥ 4 years) |

| Government zero-trust mandates | +1.3% | North America and Europe government sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Hybrid-Work Policies

Permanent hybrid work arrangements prompt enterprises to standardize collaboration experiences across offices, homes, and satellite sites, thereby increasing the baseline demand for consistent video endpoints. Seventy-nine percent of surveyed employees now expect flexible schedules that require frictionless transitions between locations, compelling IT teams to budget for device parity and remote manageability.[2]Source: AVIXA, “4 Biggest Challenges Linked to Video Conferencing in Enterprises Today,” AVIXA.orgProcurement cycles lengthen because decision makers weigh ecosystem fit, security certifications, and analytics capabilities before issuing multi-year contracts. Mid-tier solutions that strike a balance between feature richness and affordability find particular traction among small to medium-sized enterprises, a cohort that has historically been underserved by dedicated codecs. Vendors that demonstrate cross-platform compatibility, zero-touch provisioning, and firmware uniformity gain preference as buyers treat hardware as mission-critical infrastructure, not discretionary peripherals.

Cost-Effective USB-Based Endpoints

Plug-and-play USB cameras and bars are redefining affordability thresholds by eliminating the need for specialized controllers and proprietary cabling. Enterprises embracing BYOD unlock rapid room conversion with minimal installation labor. Volume economics favor manufacturers that can bundle AI features, such as auto-framing and background noise suppression, without inflating price points. Because USB devices natively integrate with dominant software platforms, they serve as gateway SKUs for broader subscription services that bolster lifetime customer value. For emerging Asia-Pacific markets, USB offerings satisfy both capex sensitivity and feature expectations, accelerating greenfield adoption across small businesses and branch offices.

Rising Huddle-Room Deployments

Open-plan offices prioritize smaller, tech-ready spaces that support spontaneous collaboration for the huddle-room segment. Purpose-built collaboration bars optimize audio pickup for rooms seating four to six people, while integrated occupancy sensors provide facility teams with utilization analytics that inform real estate decisions.[3]Source: Logitech, “Optimizing Small Rooms for Video Collaboration,” Logitech.com With a significant application share already secured, huddle-room hardware serves as a lever for workplace redesign strategies seeking a productivity boost without extensive floorplate expansion. Vendors combine sleek industrial design and native cloud management to simplify multi-room rollouts, reducing IT truck rolls and improving uptime through proactive diagnostics.

AI-Enabled Auto-Framing and Transcription Demand

Artificial intelligence is migrating from software layers to hardware edges, embedding compute directly inside cameras and bars. HP’s DirectorAI suite delivers group, person, and presenter framing powered by proprietary models that execute locally for lower latency and enhanced privacy.[4]Source: HP Inc., “HP Poly DirectorAI – AI-Powered Meeting Solutions,” HP.comEnterprises welcome endpoint-level transcription and gesture recognition because it frees cloud cores for bandwidth-intensive content sharing. As AI becomes a table stake, vendors differentiate themselves through dataset breadth, algorithm transparency, and integration depth with productivity suites. The resulting arms race accelerates feature democratization, lowering switching barriers and inviting specialized entrants that target vertical-specific AI use cases, such as clinical documentation or courtroom captioning.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High upfront capex for enterprise-grade systems | -2.8% | Global – pronounced among SMEs | Short term (≤ 2 years) |

| Inter-vendor interoperability issues | -2.1% | Global – acute in mixed-vendor environments | Medium term (2-4 years) |

| Semiconductor supply-chain volatility | -1.9% | Global – concentrated in Asia-Pacific production | Short term (≤ 2 years) |

| Growing preference for software-only BYOD | -1.4% | North America and Europe tech-forward organizations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex for Enterprise-Grade Systems

Codec-based room kits and multi-control units often carry price tags that dissuade cash-constrained organizations from upgrading legacy conference spaces. Capital fear extends to ancillary costs covering installation, user training, and multi-year maintenance contracts. Leasing and hardware-as-a-service programs partially solve cash-flow hurdles, yet aggregate spend over device lifecycles can surpass outright purchase values, prolonging ROI horizons. Vendors have responded with modular architectures and consumption-based licenses, but uncertainty around refresh timing keeps some buyers in deferral mode particularly when economies signal softness.

Inter-Vendor Interoperability Issues

Enterprises that juggle disparate camera, microphone, and control brands often face audio sync glitches, feature downgrades, and onerous firmware coordination. Sixty-nine percent of surveyed IT leaders flagged platform integration as their top deployment pain point. Proprietary extensions, while useful for brand differentiation, can perpetuate lock-in and increase the load on support desks’ ticket volumes. Standards bodies shepherding USB-C, SIP, and emerging IPMX protocols aim to harmonize connectivity layers, yet adoption lags because incumbent vendors guard premium features behind closed APIs. Buyers consequently favor suppliers that publish SDKs, certify against leading UC platforms, and provide back compatibility with service-level agreements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Hardware: USB Integration Drives Accessibility

USB cameras secured 25.02% of the video conferencing hardware market share in 2025, underscoring enterprises’ appetite for low-touch deployment paths that trim installation labor and accelerate scale-out phases. Collaboration bars, which blend camera, microphone, speaker, and compute in a single chassis, headline the growth narrative with a 16.21% CAGR, serving as Swiss-army solutions for huddle rooms and satellite offices. Multi-control units remain critical inside boardrooms and auditoriums that demand advanced routing, while secure codec nodes retain loyalty from defense and finance verticals prioritizing on-premise media processing.

Standardized USB interfaces permit uniform firmware rollouts across device fleets, simplifying IT governance and boosting uptime. AI algorithms run directly on bar chipsets, eliminating the need for external compute and raising user expectations for intelligent layouts, adaptive noise filtering, and automatic lighting optimization. PTZ cameras equipped with optical zoom, particularly for larger venues, regain relevance when combined with AI-assisted speaker tracking. Vendor competition now focuses on management dashboards, licensing flexibility, and sustainability credentials, rather than raw audio-visual specifications. As hybrid policy permanence intersects with ESG scorecards, demand coalesces around power-efficient silicon and recycled enclosure materials, helping companies inch toward their net-zero commitments.

By End User: Healthcare Digitization Accelerates Adoption

Commercial premises maintained a 39.52% share of the video conferencing hardware market size in 2025, leveraging established procurement playbooks and large room inventories. Yet healthcare systems are outpacing every other vertical with a 16.74% CAGR, buoyed by telemedicine reimbursements, clinician collaboration needs, and HIPAA-driven security standards. The U.S. FCC’s Rural Health Care Program subsidizes connectivity for remote facilities, indirectly spurring endpoint purchases that close geographic gaps between specialists and patients. Integration with electronic health record platforms enhances device value, embedding consultations into clinical documentation workflows and accelerating the adoption of clinical-grade solutions.

Institutions such as universities and government agencies sustain steady volumes because distance learning and digitalization of public services remain strategic. Within health networks, infection-control protocols prefer wipeable surfaces and antimicrobial materials, influencing product design roadmaps. Vendors providing FDA-classified peripherals, privacy filters, and audit logging gain early-mover advantage in a segment where failure tolerance is minimal. Commercial office buyers, by contrast, scrutinize user-experience metrics, call-join velocity, AI transcription fidelity, and occupancy analytics to validate ROI against productivity baselines.

By Application: Huddle Rooms Lead Space Transformation

Huddle rooms captured the highest slice at 45.12% in 2025 and will widen their lead thanks to a 16.48% CAGR. In square-foot constrained downtown offices, repurposing underutilized alcoves into video-ready pods generates immediate uplift in collaboration frequency without costly build-outs. Small meeting rooms retain relevance for cross-functional workshops and client demos, but their growth decelerates as companies favor modular partitions that spawn multiple micro-spaces over one large venue.

Boardrooms and auditoriums remain the prestige layer, equipped with multi-camera switching, ceiling microphone arrays, and content-capture appliances suitable for investor briefings and town-hall broadcasts. These premium installs command higher margins and longer sales gestations for vendors but offer limited volume. Huddle room hardware brings scale benefits through repeatable SKUs, standardized mounting kits, and bulk firmware orchestration, traits that support fleet expansions spanning hundreds of sites. As AI analytics surface real-time occupancy and scheduling insights, facilities teams redirect real-estate budgets toward space types exhibiting the strongest meeting-to-square-foot yield.

Geography Analysis

North America held a 35.12% share of the video conferencing hardware market in 2025, driven by mature infrastructure, early adoption of AI, and security mandates from federal agencies that underpin codec demand. The United States Department of Defense's zero-trust frameworks prioritize on-premise media processing vendors that present TAA/NDAA-compliant supply chains. Growth moderation, however, is evident as many Fortune 500 companies focus on software subscription renewals rather than new business development, preferring analytics-driven optimization of existing fleets. Canada and Mexico contribute incremental upside by modernizing cross-border commerce logistics that rely on secure video interactions for customs clearance and vendor audits.

Asia-Pacific propels global upside with a 16.89% CAGR through 2031, driven by China’s smart-city investments, India’s telehealth rollouts, and Southeast Asia’s startup boom. Chinese provincial governments subsidize professional AV fit-outs inside municipal command centers, ensuring resilient demand even when private-sector sentiment softens. Indian hospital chains and higher-education providers seek cost-efficient USB bars that comply with data localization statutes, prompting Western vendors to establish local assembly hubs that circumvent import tariffs. Component proximity further enables Asia-Pacific manufacturers to pivot quickly in response to semiconductor shortages, reinforcing supply security assurances sought by global enterprise buyers.

Europe registers stable mid-single-digit expansion, tempered by economic uncertainties yet buoyed by stringent GDPR and sustainability legislation that steer procurement toward energy-labeled, data-sovereign solutions. Multinational firms headquartered in Germany and France are including stipulations for recyclable packaging and green-energy manufacturing disclosures in their RFP scoring matrices. Scandinavia pioneers net-positive buildings that embed video endpoints into smart-lighting grids, integrating room scheduling with occupancy sensors for carbon-aware meeting orchestration. Meanwhile, the Middle East and Africa are embarking on government-led digital transformation programs that deploy collaboration infrastructure across ministries, schools, and healthcare clinics, although the execution pace hinges on oil price volatility and public spending cycles.

Mordor Intelligence provides coverage of the video conferencing hardware market across other key regional markets, including Middle East and Africa, Latin America, Asia, Europe, and North America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The video conferencing hardware market exhibits moderate consolidation, with the top five suppliers controlling a significant share. Cisco dominates secure codec shipments, Logitech leads in USB peripherals volume, while the HP-Poly union carves an expansive mid-range portfolio that spans headsets to boardroom appliances. AudioCodes and Crestron differentiate themselves through AI-first designs and room-control ecosystems, respectively, staking claims in specialized areas such as intelligent meeting summaries and building automation convergence. Strategic thrusts are increasingly targeting lifecycle services, device analytics, remote diagnostics, and managed room experiences that bundle recurring revenues with hardware bases.

Vertical integration is accelerating: HP folded Vyopta’s analytics engine into its Workforce Experience Platform, extending visibility from silicon thermals to user sentiment dashboards. Cisco doubled down on native AI imaging with its dual-lens Board Pro G2, countering Logitech’s Rally Bar series, which targets cost-sensitive huddle spaces. Start-ups exploit cloud-native architectures to launch subscription-only camera offerings, reducing initial capex for SMBs yet challenging incumbents to refresh price ladders. Across the aisle, chipset firm Valens partners with regional ODMs to fast-track bespoke products that address government localization quotas in Israel and Taiwan.

Supply resilience has become a chessboard square alongside AI capabilities. Vendors employ multisource component strategies and near-shoring to hedge against geopolitical risk, while customers incorporate lead-time guarantees into contract clauses. Those able to demonstrate carbon-neutral logistics and conflict-free mineral sourcing edge ahead in public-sector tenders, particularly across Europe, where ESG reporting obligations escalate annually. In summary, competition centers on three key pillars: AI proficiency, supply chain robustness, and lifecycle analytics, setting the tone for the video conferencing hardware industry in the second half of the decade.

Video Conferencing Hardware Industry Leaders

Logitech International S.A.

Cisco Systems, Inc.

Huawei Technologies Co., Ltd.

Yealink Network Technology Co., Ltd.

EPOS Group A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: HP launched the Poly Studio V12 Video Bar for small rooms, integrating NoiseBlockAI and Acoustic Fence technologies at a USD 899 price point and targeting April 2025 availability.

- February 2025: Cisco unveiled the Board Pro G2 and Desk Phone 9800 Series to bolster hybrid-work transitions with AI-powered imaging and enterprise-grade security.

- January 2025: AudioCodes introduced an AI-First Intelligent Meeting Room solution featuring generative meeting summaries and advanced visual AI.

- December 2024: Good Way Technology showcased a videoconferencing suite powered by Valens’ VS6320 chipset for improved bandwidth and performance.

Global Video Conferencing Hardware Market Report Scope

| Multi-Control Units (MCU) |

| Collaboration Bars |

| Codec Systems |

| USB Cameras |

| USB-based Integrated Bars |

| Other Bundled Kits |

| Enterprise Headsets |

| PTZ Cameras |

| Speakerphones and Microphone Arrays |

| Institutions |

| Commercial Spaces |

| Healthcare Facilities |

| Huddle Rooms |

| Small Meeting Rooms |

| Large Conference Rooms |

| Boardrooms and Auditoriums |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of APAC | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Type of Hardware | Multi-Control Units (MCU) | ||

| Collaboration Bars | |||

| Codec Systems | |||

| USB Cameras | |||

| USB-based Integrated Bars | |||

| Other Bundled Kits | |||

| Enterprise Headsets | |||

| PTZ Cameras | |||

| Speakerphones and Microphone Arrays | |||

| By End User | Institutions | ||

| Commercial Spaces | |||

| Healthcare Facilities | |||

| By Application | Huddle Rooms | ||

| Small Meeting Rooms | |||

| Large Conference Rooms | |||

| Boardrooms and Auditoriums | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of APAC | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the video conferencing hardware market?

The video conferencing hardware market size is USD 8.1 billion in 2026, with forecasts pointing to USD 16.41 billion by 2031.

Which hardware segment is growing the fastest?

Collaboration bars lead growth with a projected 16.21% CAGR as enterprises favor integrated AI-ready devices for huddle rooms.

Why is healthcare adopting video hardware so rapidly?

Telemedicine reimbursements, HIPAA security needs, and rural-connectivity funding are pushing healthcare facilities toward a 16.74% CAGR in endpoint investments.

How big is the huddle-room opportunity?

Huddle rooms already account for 45.12% of deployment value and are expanding at 16.48% CAGR, making them the dominant application segment.

Page last updated on: