Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.01 Billion |

| Market Size (2026) | USD 1.05 Billion |

| Market Size (2031) | USD 1.28 Billion |

| Growth Rate (2026 - 2031) | 4.06% CAGR |

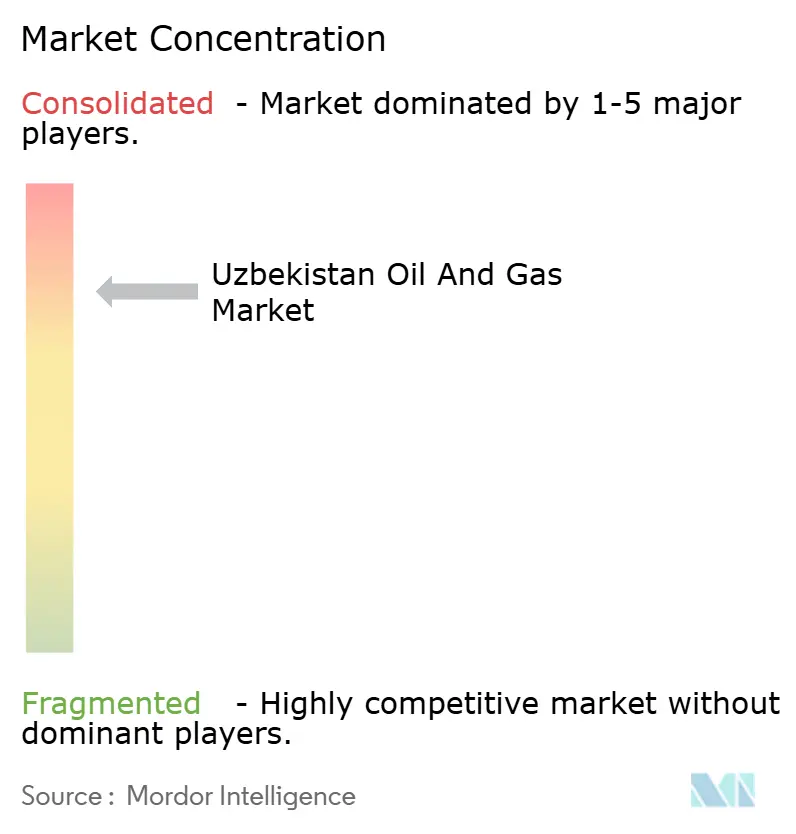

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Uzbekistan Oil And Gas Market Analysis by Mordor Intelligence

Uzbekistan Oil And Gas Market size in 2026 is estimated at USD 1.05 billion, growing from 2025 value of USD 1.01 billion with 2031 projections showing USD 1.28 billion, growing at 4.06% CAGR over 2026-2031.

This growth reflects a policy-driven swing from raw-gas exports toward domestic value addition, steady transit-fee receipts, and continued foreign capital inflows through production-sharing agreements. Upstream consolidation, midstream pipeline upgrades, and downstream gas-to-liquids projects together anchor the medium-term outlook even as mature fields decline. Rising industrial gas demand, new digital oilfield pilots, and tariff liberalization are further expanding revenue streams for companies willing to modernize their operations and embrace data analytics. In parallel, Uzbekistan’s land-linked position keeps transit projects economically attractive, cushioning the system against short-term production headwinds.

Key Report Takeaways

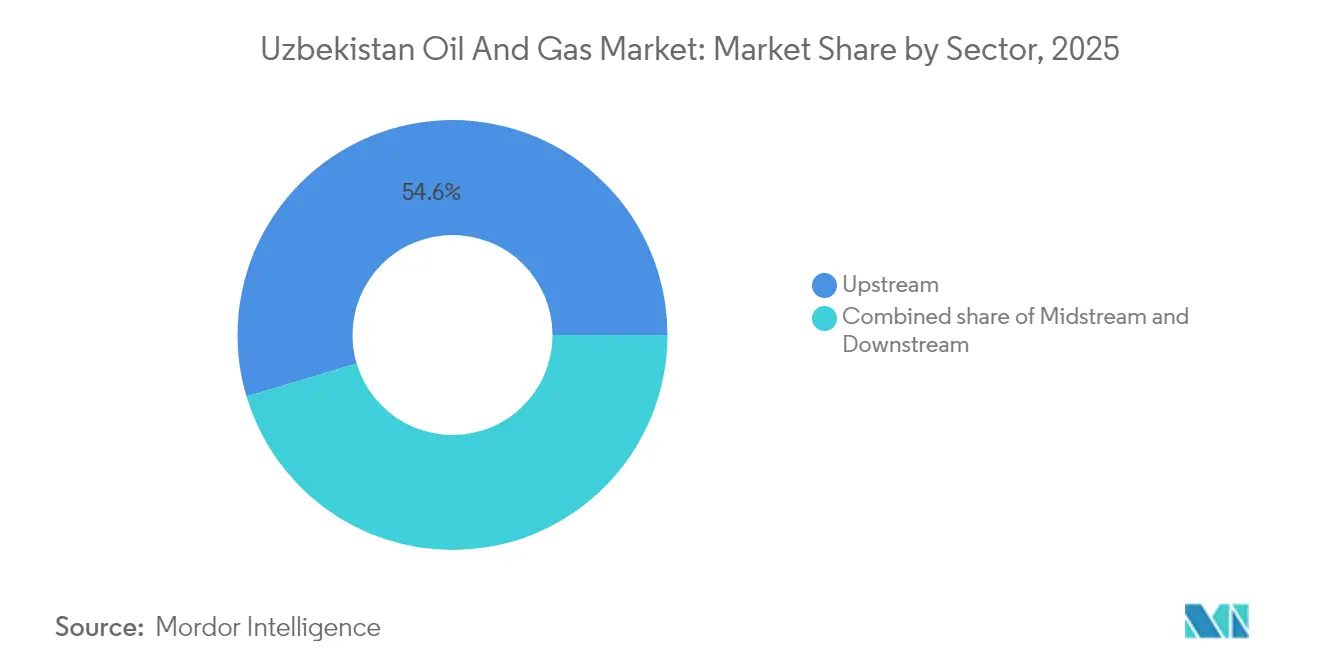

- By sector, upstream activities held 54.62% of the Uzbekistan oil and gas market share in 2025, while midstream recorded the strongest growth at a 6.55% CAGR through 2031.

- By location, onshore assets dominated the Uzbekistan oil and gas market with a 94.55% share in 2025, and offshore activities, although small, are expected to rise at a 4.78% CAGR through 2031.

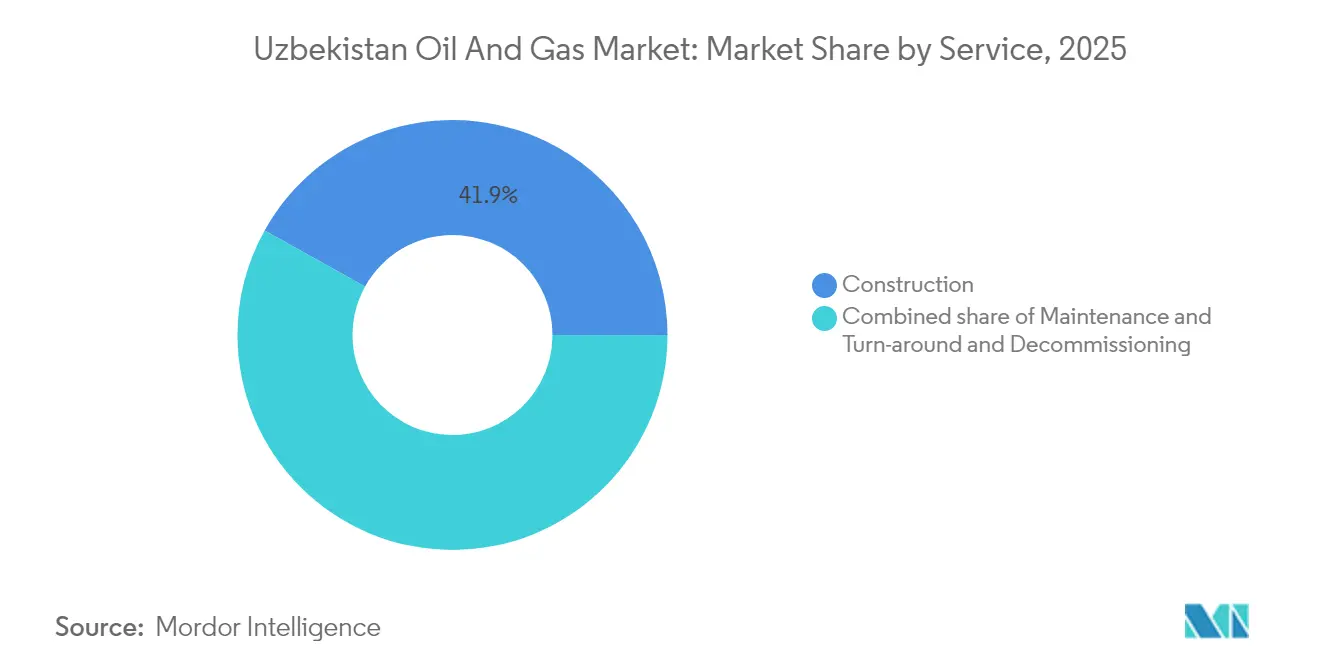

- By service, construction accounted for 41.92% of 2025 revenue, whereas maintenance and turnaround services are expanding at the fastest rate, with a 4.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Uzbekistan Oil And Gas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising domestic gas demand from energy-intensive industries | +0.6% | National, with concentration in Tashkent, Samarkand industrial zones | Medium term (2-4 years) |

| Government incentives for upstream foreign investment (PSAs, tax breaks) | +0.5% | National, with focus on Ustyurt Plateau, Amu Darya Basin | Long term (≥ 4 years) |

| Strategic transit position spurring pipeline investments | +0.4% | Regional corridors: China-Europe, Russia-South Asia transit routes | Long term (≥ 4 years) |

| State plan to end gas exports driving downstream GTL & petrochemicals | +0.7% | National, with early development in Kashkadarya, Surkhandarya regions | Medium term (2-4 years) |

| Deregulation of wholesale gas pricing enabling private sector entry | +0.3% | National, with pilot implementation in major urban centers | Short term (≤ 2 years) |

| Digital-oilfield pilots in Bukhara-Khiva using AI reservoir management | +0.2% | Bukhara-Khiva Basin, potential expansion to Fergana Valley | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Domestic Gas Demand From Energy-Intensive Industries

Between 2016 and 2021, industrial electricity use increased from 57.6 billion kWh to 74.9 billion kWh as cement, steel, and chemical plants expanded their production.[1]Kun.uz Editorial, “Industrial Energy Demand Rises in Uzbekistan,” kun.uz Energy-intensive companies now absorb roughly 40% of national gas output, up from 35% in 2020, which tightens the domestic balance and supports premium pricing for processed volumes. Imports routed through Kazakhstan are projected to reach 11 billion cubic meters per year by 2026 to plug the widening supply gap. This shortfall justifies accelerated investments in gas processing, compression, and last-mile distribution. The Ministry of Energy anticipates an additional 8-10 billion m³ of demand by 2030, primarily concentrated around the Tashkent and Samarkand industrial parks.

Government Incentives For Upstream Foreign Investment

A 2024 subsoil law eliminated numerous approval bottlenecks and offered 15-year tax holidays for projects exceeding USD 100 million. The measures unlocked USD 2 billion in firm commitments within twelve months, reversing a decade of underspend in exploration. International operators gain cost-recovery assurances and accelerated depreciation, which sharply improves their internal rates of return in the Ustyurt Plateau’s technically complex shale prospects. Domestic-content rules set at 30% still channel procurement to local suppliers, safeguarding job creation and skill transfers. Longer-dated incentives also reassure lenders, lengthening debt tenors and reducing borrowing costs for frontier acreage work programs.

Strategic Transit Position Spurring Pipeline Investments

Uzbekistan’s central location underpins USD 470 million of committed pipeline upgrades aimed at bi-directional flows to China, Europe, and South Asia. The Central Asia–Center network is expected to handle 10-15 billion m³ in reverse-flow mode by 2027, unlocking transit fees of USD 5-12 million annually for operator Uztransgaz. Projects include doubling Gazli storage capacity and installing digital leak-detection systems that align with EU safety protocols. Transit earnings offer a quasi-fixed income stream, partly insulating state revenue from upstream price swings. Coupled with trilateral transport accords signed with Turkmenistan and Azerbaijan in 2025, the build-out positions the country as a dependable regional gas hub.

State Plan To End Gas Exports Driving Downstream GTL & Petrochemicals

A presidential decree mandates that 15-20 billion m³ of formerly exported gas be redirected into domestic petrochemical feedstock starting in 2025. Flagship projects include the USD 5 billion Karakul methanol-to-olefins complex and a synthetic-fuels unit capable of producing 1.5 million tonnes per annum (tpa), elevating Uzbekistan to the world’s fifth-largest GTL location. Captive feedstock at regulated prices de-risks cash flows for investors while shielding the state from commodity-cycle volatility. The import substitution of polymers and solvents, valued at over USD 1 billion per year, could help narrow the trade deficit and strengthen foreign-exchange buffers. The pivot also spurs auxiliary markets—such as logistics, specialty chemicals, and engineering services—magnifying downstream multipliers across the broader economy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing oilfields with rising lifting costs | -0.5% | Legacy fields in Fergana Valley, Bukhara-Khiva Basin | Short term (≤ 2 years) |

| Insufficient pipeline & storage infrastructure | -0.4% | National, particularly remote production areas in Karakalpakstan | Medium term (2-4 years) |

| Winter gas shortages pressuring retail price caps | -0.3% | National, with acute impact in northern regions during peak demand | Short term (≤ 2 years) |

| FX-convertibility limits delaying profit repatriation for IOCs | -0.2% | National, affecting all foreign investment projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing Oilfields With Rising Lifting Costs

Declining rates of 8-12% per year in legacy reservoirs increase extraction costs by USD 15-25 per barrel of oil equivalent.[2]Tashkent Times Staff, “Aging Fields Weigh on Uzbek Gas Output,” tashkenttimes.uz Uzbekneftegaz’s 2025 outlook of 26.5 billion m³ is 2.8 billion m³ below its 2024 plan, underscoring the drag mature assets impose on national volumes. The capital required for geological infill wells and water-handling facilities exceeds internal cash flows, risking deferred maintenance and unplanned shutdowns. Higher lifts compress margins and reduce free cash available for reinvestment, which in turn can slow modernization across the supply chain. Without the widespread adoption of enhanced recovery and AI-enabled production optimization, output could undershoot targets, tempering the growth trajectory of the Uzbekistan oil and gas market.

Insufficient Pipeline & Storage Infrastructure

Many export-era trunklines date back to the Soviet period, and bottlenecks remove 5-8% of potential supply during peak winter demand. Gazli, the country’s principal storage site, runs near capacity each January, limiting load-balancing options and forcing short-notice imports at elevated spot prices. Remote Karakalpakstan fields still vent or flare associated gas worth up to USD 80 million a year because gathering systems are incomplete. Upgrading lines to modern integrity standards will cost USD 2-3 billion through 2030, an outlay that competes with spending on new wells and refineries. Until then, flow interruptions and seasonal shortages keep wholesale prices volatile, complicating demand forecasts for power plants and industrial buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Upstream Consolidation Amid Midstream Expansion

Upstream operations continued to generate 54.62% of 2025 revenue, yet a natural decline in mature basins is steering capital into midstream projects that are growing at a 6.55% CAGR. The Uzbekistan oil and gas market size tied to midstream is poised to swell as the Central Asia–Center retrofit, new compressor stations, and gas-to-liquids feedstock lines absorb redirected export volumes. Consolidation among field operators accelerates because higher lifting costs favor companies with cash and technology advantages. AI-based reservoir models used in Bukhara-Khiva pilots improved uptime by 15-20%, underscoring the value of digital workflows.

Modern seismic campaigns and ultra-deep wells raised Sanoat Energetika Guruhi’s output 350% between 2019 and 2025, validating the payoff from data-driven exploration in aging plays. As GTL and petrochemical plants come online, their stable off-take contracts shift profit centers farther downstream. Service providers are adapting, selling predictive maintenance and integrated project-management suites rather than traditional roughnecking. Collectively, these moves reshape the Uzbekistan oil and gas market, making midstream margins and downstream integration just as critical as raw-barrel production.

By Location: Onshore Dominance With Limited Offshore Potential

Onshore assets accounted for a commanding 94.55% of 2025 turnover, evincing Uzbekistan’s landlocked geography and the shallow reserves in its portion of the Aral Sea. Offshore prospects exhibit a modest 4.78% CAGR, which is insufficient to materially shift the portfolio mix, but is relevant as a proof-of-concept for low-impact, shallow-water techniques. The Uzbekistan oil and gas market share tied to onshore acreage remains unmatched; however, rising carbon commitments may prompt operators to decarbonize by electrifying rigs and reducing flaring in high-traffic basins, such as Fergana.

In the Ustyurt Plateau, the lure of 47 billion t of shale resources excites majors hunting long-dated barrels despite transport hurdles. Drilling there requires ice-road logistics, tele-drilling, and modular processing units, which raise capital expenditures (capex) 25-40% above basin averages. Still, new sub-salt discoveries could offset the decline in legacy plays if paired with state-backed trunkline extensions. Environmental mandates are stricter following the 2021 Code, compelling operators to install water-treatment and wildlife-protection systems or face penalties. These factors collectively sustain onshore pre-eminence while nudging the frontier farther into technologically demanding zones.

By Service: Construction Leads Amid Maintenance Growth

Construction retained a 41.92% revenue edge in 2025, as mega-projects—from pipeline loops to the USD 5 billion Karakul MTO plant—drove demand for engineering, procurement, and civil works. Yet maintenance and turnaround work is gaining momentum at a 4.98% CAGR as plants and pipelines commissioned two or three decades ago approach mid-life. Predictive analytics platforms that identify compressor wear or corrosion before failure enable service firms to justify premium contracts.

Global firms like Schlumberger and Halliburton are expanding their Tashkent tech centers to localize diagnostics and remote-monitoring support, complying with the 30% local-content rule while integrating advanced workflows. Smaller Uzbek contractors win sub-lots for scaffold, weld, and instrumentation tasks, gaining capability transfers in the process. Decommissioning remains a niche market but will scale once major fields near their economic limit, opening another revenue vertical. Combined, these shifts diversify service income streams and deepen the core talent pool that underpins future competitiveness of the Uzbekistan oil and gas market.

Geography Analysis

Uzbekistan straddles the main east-west and north-south gas corridors that connect Siberia, Turkmenistan, China, and South Asia—an alignment turning transit into an earnings hedge. The new tripartite agreement between Turkmenistan and Azerbaijan, signed in August 2025, could increase throughput by up to 30% over the next decade. Reverse-flow capability on the Central Asia–Center line enables imports from Russia when domestic supply is tight, with volumes projected at 11 billion m³ per year by 2026.

Internally, resource endowment is uneven: Bukhara-Khiva holds roughly 60% of the remaining gas, while Fergana’s oilfields require steamfloods and polymer drives to curb double-digit decline. Northern provinces suffer winter deficits because aged lines restrict peak flows; consequently, retail caps stay in place, distorting price signals and deterring private retail investment. The government’s spatial plan aims to twin transit lines with regional spur lines, blending commercial viability with equitable access.

Unconventional activity intensifies in the vast, sparsely populated Ustyurt Plateau, where shale plays may deliver multi-decade output once the necessary infrastructure is in place. Meanwhile, ongoing storage expansion at Gazli should hike working gas by 1 billion m³, damping seasonal volatility and improving contract reliability for industrial offtakers. As infrastructure densifies, previously stranded resources become economically feasible, reinforcing Uzbekistan’s aspiration to transition from a pure producer to a versatile regional energy hub.

Regulatory Landscape

Uzbekistan hydrocarbons are governed under a state-ownership model, with policy and sector regulation led by the Ministry of Energy, subsoil administration handled by the Ministry of Mining Industry and Geology, and operational compliance oversight conducted by the Cabinet of Ministers Inspection for Control in the electric power industry, oil products, and gas usage (Uzenergoinspeksiya). Law No. ZRU-987, On Subsoil (signed October 31, 2024; effective February 2, 2025) reinforces that subsoil resources are exclusive state property and cannot be privately owned or pledged. This framework shapes how IOCs and private players participate through licenses and contractual frameworks (including PSAs), rather than through resource title.

Pricing and consumption-side governance also feed into project economics. The Cabinet of Ministers Resolution No. 243 dated May 15, 2026, approved updated pricing for fuel and energy resources effective June 1, 2026, as part of measures aimed at stabilizing the financial condition of energy enterprises. For industrial projects, Uzenergoinspeksiya oversight includes energy conservation and efficiency compliance, including requirements for energy audits by accredited expert organizations, which affects permitting timelines and the scope of pre-commissioning work for large gas-consuming facilities and midstream upgrades.

Competitive Landscape

The market remains moderately concentrated, with state-run Uzbekneftegaz anchoring the upstream sector through majority stakes in legacy blocks. However, its share is gradually slipping as joint ventures proliferate. Fitch-rated BB- Eurobonds, worth USD 700 million, issued in 2025, provide the company with low-cost capital for brownfield upgrades and GTL equity. Lukoil, CNPC, and TotalEnergies cooperate on deep-gas and tight-oil pilots, bringing directional drilling and reservoir stimulation know-how uncommon among local firms.

Private challenger Sanoat Energetika Guruhi has boosted output by 350% since 2019 by combining 3D seismic with flare-gas capture, illustrating how data and sustainability can outperform legacy methods. Western service majors reinforce their positions through digital platform roll-outs that bundle analytics, maintenance, and training into long-term service agreements. An influx of Japanese, Korean, and Turkish EPC contractors around the Karakul complex adds another layer of competition in the construction industry.

In the future, white-space lies in unconventional acreage, pipeline automation, and specialty chemicals, where technical barriers to entry deter smaller peers. Yet currency-convertibility caps and winter gas rationing still color board-level risk assessments for multinationals. Overall, the shifting blend of state guidance, private ingenuity, and foreign capital is shaping an increasingly diversified Uzbekistan oil and gas market where value pools are tilting from pure extraction toward integrated midstream and chemical chains.

Uzbekistan Oil And Gas Industry Leaders

JSC Uzbekneftegaz

Gazprom PAO

China National Petroleum Corporation (CNPC)

TotalEnergies SE

Lukoil Uzbekistan Operating Co.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity is technically complex onshore exploration in the Ustyurt Plateau under PSA structures that bring capital and subsurface know-how into frontier acreage. In May 2026, BP entered the North Ustyurt PSA for six onshore exploration blocks with a 40% participating interest alongside SOCAR and Uzbekneftegaz (30% each), and Uzbekneftegaz communicated a schedule to launch drilling operations in the Ustyurt region by the end of 2026. This points to near-term whitespace across drilling, seismic, well services, and field logistics tailored to remote onshore operations, while also aligning with the report's emphasis on upstream consolidation supported by targeted foreign participation.

Midstream and downstream-adjacent opportunities are concentrated in integrity upgrades and domestic value-add chains that reduce losses and improve supply reliability during seasonal peaks. Uzbekistan's documented need to upgrade aged pipelines and storage (including Gazli and broader trunkline modernization) is reinforced by 2026 actions, including Uzbekneftegaz signing a pipe supply contract with China-based IMBSU Steel Industry to support infrastructure maintenance and development. At the same time, policy measures aimed at demand-side efficiency, including an April 2026 presidential decree targeting natural gas savings via upgrades at major industrial enterprises, broaden the scope for energy audits, metering, digital monitoring, and turnaround services at large gas-consuming sites. These measures complement the market shift from raw-gas flows toward processing capacity, system reliability, and optimization.

Recent Industry Developments

- July 2026: Condor Energies reported record production of 16,921 boed at the Kumli Northwest field after successful testing of the K-42 well and its connection to facilities. The update signals tangible output upside from focused field development and debottlenecking, supporting activity across upstream services and tie-in infrastructure within Uzbekistan.

- June 2026: Uzbekneftegaz stated that drilling in the Ustyurt region under its partnership with BP is scheduled to start by the end of 2026. The timeline underscores accelerated upstream work programs in frontier onshore blocks, lifting demand for rigs, well services, and supporting midstream hookups where new wells move toward production.

- September 2025: Sanoat Energetika Guruhi reported that its gas output rose 350% to 1.4 billion cubic meters following flare-gas capture and modern exploration activity in the Bukhara-Khiva area. The operational result highlights monetization pathways for previously wasted gas and reinforces investment interest in brownfield optimization and emissions-reduction-linked production gains.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the value generated from oil and gas activities inside Uzbekistan, covering upstream, midstream, and downstream work that supports finding, producing, processing, and moving hydrocarbons.

Scope exclusions: We exclude non-hydrocarbon energy (such as renewables), and we do not treat broader chemicals as part of the oil and gas total unless they are directly tied to downstream processing activity.

Segmentation Overview

- By Sector

- Upstream

- Midstream

- Downstream

- By Location

- Onshore

- Offshore

- By Service

- Construction

- Maintenance and Turn-around

- Decommissioning

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the model and to set realistic boundary conditions for Uzbekistan. We relied on official statistics and energy data series to understand production, processing, and trade direction before assumptions were finalized.

Sources referenced include public materials such as Uzbekistan national statistics releases, customs and trade disclosures, international energy statistics (for example, IEA-style country tables), OPEC style production summaries, World Bank macro indicators, and peer-reviewed energy economics papers. We also used company filings, investor presentations, and credible press to validate project timing, capacity changes, and commissioning schedules, with paid subscriptions for company financials, news and financials, and shipment-level trade signals when clarification was needed. These examples are not exhaustive, and we also drew on other public sources for collection, validation, and gap checks.

Primary Interviews and Surveys

Primary work was used to pressure-test what desk research could not fully explain, especially around capacity utilization, maintenance cycles, and how domestic demand is prioritized versus exports. We spoke with operators, midstream and downstream participants, service providers, and industry advisers across APAC, EMEA, and the Americas, so the assumptions were checked from more than one angle.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 19% | APAC: 47% |

| Mid tier: 55% | Functional/Unit leaders: 32% | EMEA: 31% |

| Smaller Players: 20% | Managers: 49% | Americas: 22% |

Market-Sizing & Forecasting

The sizing starts with a top-down reconstruction that links Uzbekistan production and processing activity to monetized value, and then we corroborate it using selective bottom-up checks. On the top-down side, the model is anchored on indicators such as crude and gas output trends, refinery and processing capacity with utilization, import and export direction, and the timing of major field or plant additions.

To keep the totals realistic, bottom-up approximations were used where data allowed, such as sampled volume-by-activity builds and reasonableness checks on average pricing assumptions across key value pools. Where a data point was missing, we filled gaps using conservative ranges agreed during interviews, and then we narrowed those ranges after checking against trade signals and macro constraints.

For forecasting, scenario analysis was used because the outlook can swing with policy priorities, project delays, and demand balancing between domestic use and exports. Assumptions on utilization, project commissioning, and price normalization were refreshed each cycle so year-by-year movement remains explainable and repeatable.

Data Validation & Update Cycle

Validation is done in layers so the final number is not driven by one source or one assumption. We compare the model outputs against independent signals like production and trade direction, capacity change announcements, and macro energy demand context, and then any large variance is reviewed again before sign-off.

If an input shifts materially, like a project schedule change or an unexpected trade swing, the team re-contacts relevant experts to confirm what changed and whether it is temporary or structural. Reports are refreshed annually, with interim updates for material events, and a final pre-delivery pass is completed so clients receive the latest view available at the time of release.

Mordor Intelligence's Uzbekistan Oil and Gas Market Size Measured Against Other Published Estimates

It is normal to see different market size numbers for Uzbekistan oil and gas because each publisher draws the market boundary differently and then uses different value drivers to convert activity into USD. Differences also show up when one study mixes oil and gas with adjacent energy or chemicals value pools, or when currency timing and inflation handling are not aligned.

By tracking production and processing activity and refreshing utilization and pricing assumptions with field checks, Mordor Intelligence keeps the estimate tied to what is actually executed in-country rather than a broad energy spend number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.05 B (2026) | |

| Government Trade Brief A | USD 6.00 B (2023) | Uses a trade-balance style formula that adds local production and imports and subtracts exports, which can behave like a broader market flow value and may not match a sector activity-based oil and gas definition. |

| Commercial Publisher B | USD 10.30 B (2024) | Appears to apply a wider value boundary and a different base-year setup, which can fold in downstream and related spend pools with less visibility on how pricing, exchange rates, and utilization are normalized. |

Taken together, the spread is mainly explained by what gets counted and how activity is converted into USD in each year. Our approach stays transparent by linking the total to clear operating variables and then checking those assumptions with interviews, which makes updates easier when production, trade, or capacity conditions change.

Key Questions Answered in the Report

How large is the Uzbekistan oil gas market in 2026?

The Uzbekistan oil gas market size stands at USD 1.05 billion in 2026 and is projected to hit USD 1.28 billion by 2031.

What is the forecast CAGR for Uzbekistan’s oil and gas sector?

Market revenue is expected to expand at a 4.06% CAGR over 2026-2031, led by midstream and downstream investments.

Which segment is growing fastest within the sector breakdown?

Midstream activities—chiefly pipeline upgrades and gas-processing plants—are registering a 6.55% CAGR through 2031.

Why is Uzbekistan ending natural-gas exports?

A state directive redirects 15-20 billion m³ of gas toward domestic GTL and petrochemical projects to create higher-value products and cut exposure to commodity cycles.

How are foreign investors protected in Uzbek upstream projects?

Production-sharing agreements enacted in 2024 grant 15-year tax holidays, full cost recovery, and accelerated depreciation, improving project economics for international oil companies.

Page last updated on: