Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

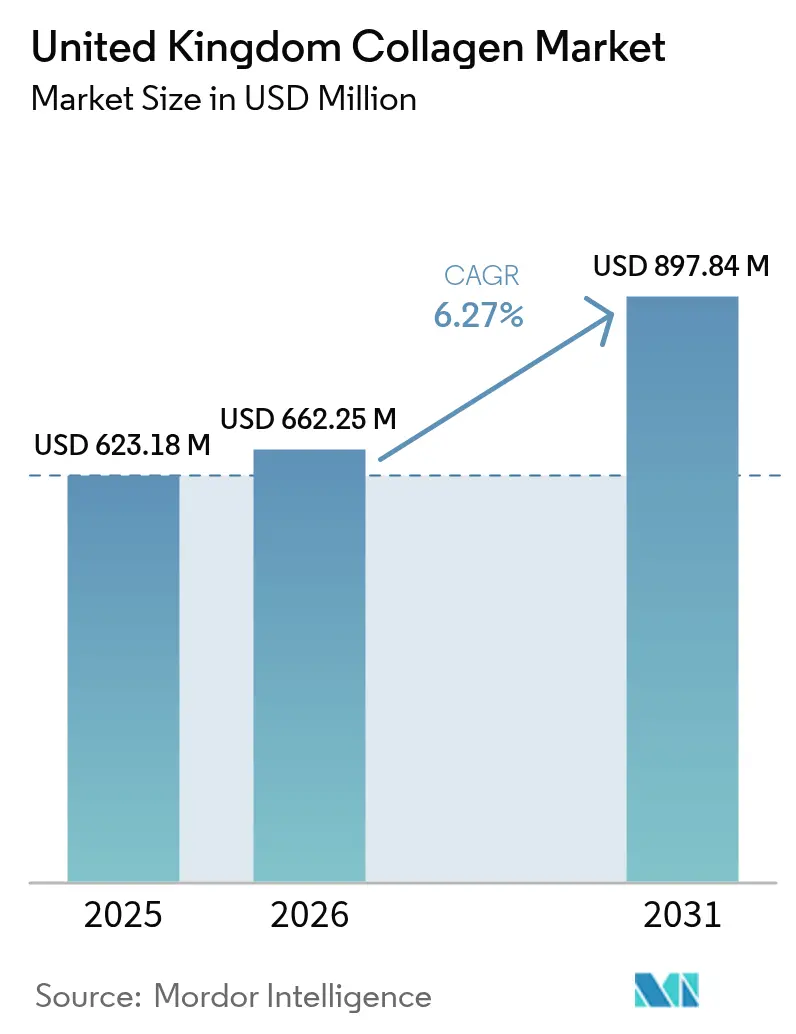

| Base Year Market Size (2025) | USD 623.18 Million |

| Market Size (2026) | USD 662.25 Million |

| Market Size (2031) | USD 897.84 Million |

| Growth Rate (2026 - 2031) | 6.27% CAGR |

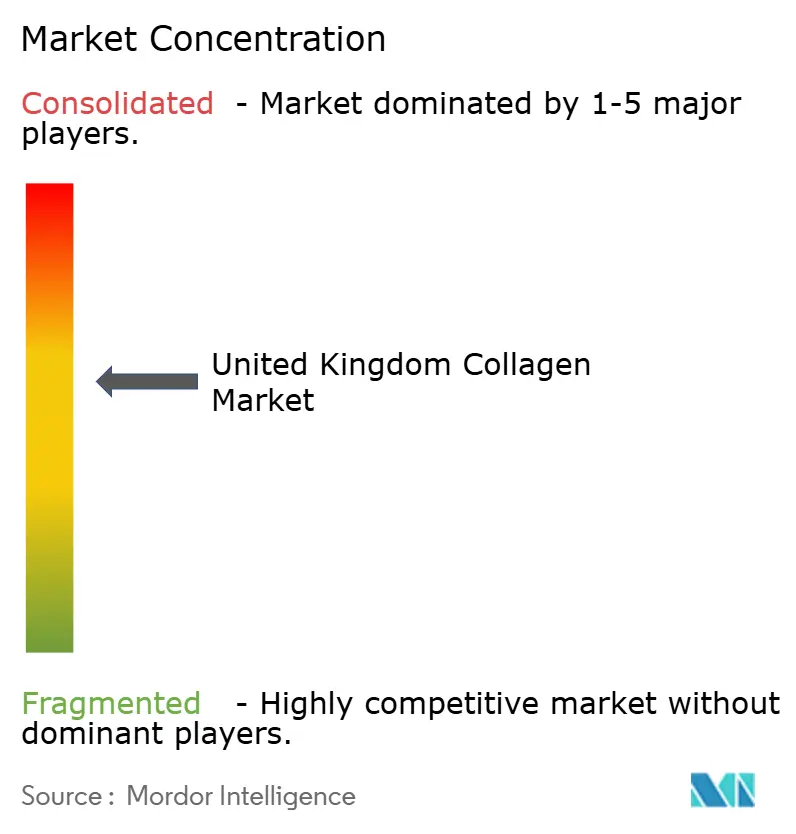

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Collagen Market Analysis by Mordor Intelligence

United Kingdom collagen market size in 2026 is estimated at USD 662.25 million, growing from 2025 value of USD 623.18 million with 2031 projections showing USD 897.84 million, growing at 6.27% CAGR over 2026-2031. Robust growth in the industry is driven by an aging population, the National Health Service's (NHS) expanding adoption of collagen biomaterials, and a consumer shift towards high-protein, multifunctional ingredients. This demand is bolstered by a diverse range of applications, including dietary supplements that support overall health, medical dressings that enhance wound healing, and premium beauty products that cater to skin rejuvenation and anti-aging needs. Industry players are rolling out bioactive peptide formats that promise quicker absorption and target specific health benefits, focusing on joint comfort, improved skin elasticity, and accelerated post-operative wound healing. The Food Standards Agency's (FSA) post-Brexit Novel Food pathway offers regulatory clarity, spurring product launches and fostering innovation in the market. At the same time, rising costs of livestock-based raw materials are pushing the industry to explore marine and biotech alternatives, which provide sustainable and cost-effective solutions while meeting consumer demand for environmentally friendly products.

Key Report Takeaways

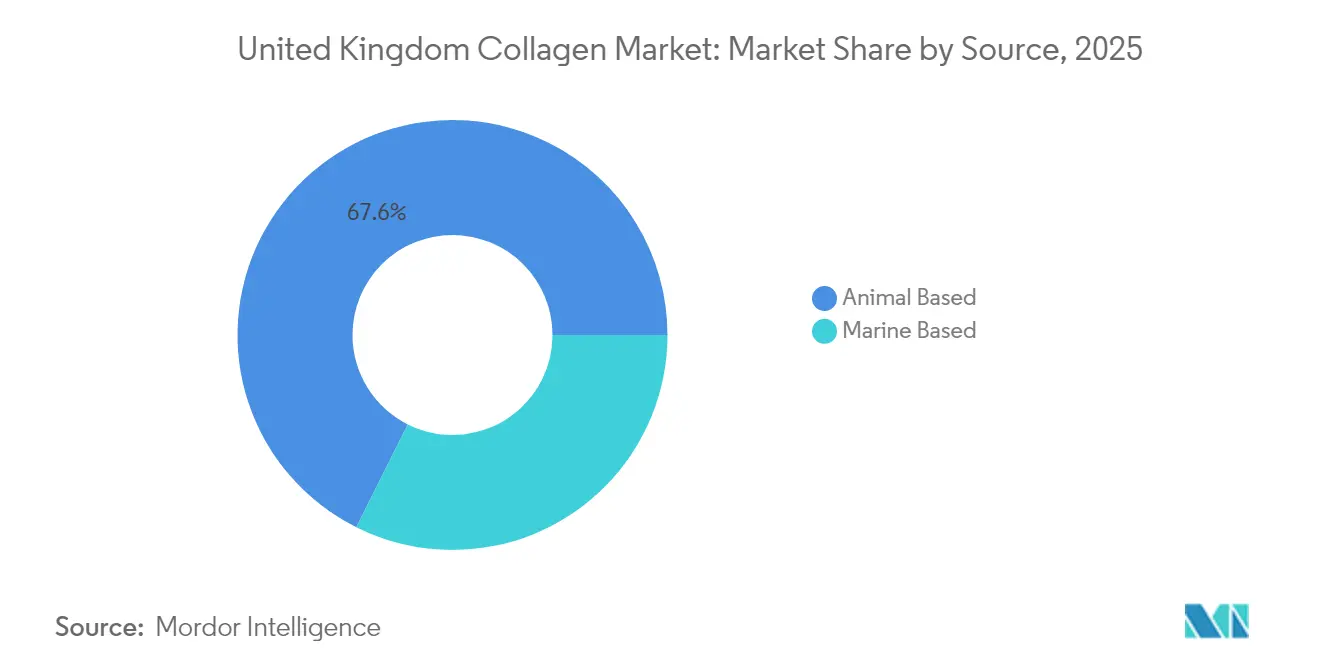

- By source, animal-based collagen captured 67.62% of the United Kingdom collagen market share in 2025, while plant-based formats are forecast to register the fastest 8.11% CAGR between 2026-2031.

- By end user, dietary supplements commanded 46.85% of the United Kingdom collagen market size in 2025, whereas personal care and cosmetics is projected to expand at a 6.63% CAGR through 2031.

- By geography, Southeast England led consumption with 28.75% value share in 2025; Scotland’s coastal belt is forecast to grow the fastest at a 7.01% CAGR owing to marine-collagen production clusters.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Collagen Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population seeking joint and skin benefits | +1.8% | Nationwide, strongest in Southeast England | Long term (≥ 4 years) |

| Sports-nutrition and high-protein lifestyles | +1.2% | Urban centers, notably London and Manchester | Medium term (2-4 years) |

| Beauty-driven nutricosmetics boom | +1.5% | Affluent postal codes across the UK | Medium term (2-4 years) |

| NHS uptake of collagen wound biomaterials | +0.9% | Nationwide hospitals and clinics | Long term (≥ 4 years) |

| Expansion of sustainable marine supply chain | +0.7% | Scottish and Southwest coastal regions | Long term (≥ 4 years) |

| Subscription-led D2C e-commerce models | +0.6% | Metropolitan areas nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ageing population seeking joint and skin health benefits

With the number of citizens aged 65 and older steadily increasing, the market for mobility and skin health solutions is expanding. Seniors participating in randomized-controlled trials showed marked improvements in joint function and retention of lean mass through physiotherapy and daily collagen peptide intake. This demographic's purchasing power allows for premium pricing, as they are often willing to invest in products that enhance their quality of life. Additionally, the trust in supplement efficacy is heightened by the clinical spill-over from NHS wound-care products, which have established a strong reputation for reliability and effectiveness. As the mindset of active aging becomes more prevalent, formulators are combining collagen with vitamin C and hyaluronic acid, creating holistic benefit stacks that address multiple health concerns, such as skin elasticity, hydration, and joint health, appealing to self-managing seniors who prioritize overall well-being.

Growth of sports-nutrition and high-protein lifestyles

Urban consumers, increasingly adopting strength training and recovery routines, are turning to collagen. They value it as a functional protein, noting its unique glycine and proline ratios, which differ from those found in whey and contribute to its distinct benefits for muscle repair, joint health, and skin elasticity. Convenient formats like ready-to-drink beverages and snacks cater to their on-the-go lifestyle, offering ease of consumption without compromising nutritional goals. This is further enhanced by peptide technologies, boasting absorption rates four times faster than native proteins, which makes collagen an efficient option for post-workout recovery and daily wellness. Once the domain of elite athletes, this segment now appeals to a broader lifestyle audience, including fitness enthusiasts, aging populations, and individuals seeking overall wellness. The marketing narrative has evolved too, shifting focus from mere muscle-building to a holistic approach emphasizing body composition, joint support, skin health, and the resilience of connective tissues.

Beauty and nutricosmetics boom in the United Kingdom

Despite macroeconomic uncertainties, the nation's premium beauty spending has surged, with collagen supplements now touted as "ingestible skin care." Major brands bolster their premium pricing by leveraging third-party dermatological accreditations to validate their wrinkle-reduction claims, which resonate strongly with consumers seeking scientifically backed solutions. Social media trends, going viral, have intensified word-of-mouth marketing, especially for single-serve sachets and flavored powders sold through direct-to-consumer channels, making these products more accessible and appealing to a broader audience. Additionally, the convenience of these formats aligns with the busy lifestyles of modern consumers, further driving their popularity. For environmentally conscious beauty shoppers, sustainable sourcing credentials, particularly marine peptides certified by the Marine Stewardship Council, further enhance the product's value proposition by addressing growing consumer demand for eco-friendly and ethically sourced ingredients. These certifications not only reinforce brand trust but also position the products as a responsible choice in the premium beauty market.

NHS uptake of collagen-based wound-care biomaterials

Collagen-based wound care products are gaining traction within the National Health Service (NHS), bolstering market fundamentals and affirming their therapeutic benefits across diverse consumer segments. The NHS allocates £587 million through its procurement frameworks for advanced wound care products, with collagen dressings firmly positioned in standardized categories. The inclusion of collagen dressings, like the Generic Biopad Collagen dressing, in the NHS Drug Tariff underscores both regulatory endorsement and established reimbursement channels, effectively lowering barriers to adoption[1]Source: National Health Survey," Generic Biopad Collagen dressing 5cm x 5cm square 1 dressing", dmd-browser.nhsbsa.nhs.uk. These frameworks ensure consistent availability and affordability of collagen-based products, further driving their usage in clinical settings. Beyond conventional wound care, clinical uses now encompass treatments for diabetic foot ulcers and surgical procedures, addressing critical healthcare needs. Companies such as Convatec are at the forefront, crafting specialized products tailored for NHS integration[2]Source: Health Care Spending Account," Convatec warns of UK investment risk if wound product rejected," nhsprocurement.org.uk. This institutional endorsement not only validates collagen's therapeutic efficacy but also amplifies consumer trust across its varied applications, fostering broader acceptance and market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising veganism and ethical concerns | -0.8% | Nationwide, stronger in major cities | Medium term (2-4 years) |

| Volatile livestock raw-material pricing | -1.1% | Processing hubs and import corridors | Short term (≤ 2 years) |

| Novel-Food regulatory hurdles | -0.6% | UK regulatory jurisdiction | Long term (≥ 4 years) |

| Consumer skepticism over health claims | -0.4% | Educated urban populations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising veganism and ethical concerns

With one of Europe's highest rates of vegan adoption, the United Kingdom is significantly impacting the sales of animal-derived collagen. This shift in consumer preferences has prompted brands to innovate by introducing recombinant-fermentation peptides, such as Evonik's Vecollage Fortify L, which replicate Type I and III collagen sequences without relying on animal inputs. These alternatives not only cater to vegan consumers but also align with the growing demand for sustainable and ethical products. Additionally, recombinant-fermentation technology offers scalability and consistency in production, addressing challenges associated with traditional collagen sourcing. To effectively appeal to flexitarian skeptics, brands must prominently emphasize cruelty-free sourcing and reduced carbon footprints on the front label, ensuring transparency and building trust with environmentally conscious consumers.

Volatile livestock-derived raw-material pricing

Animal-derived collagen manufacturers, reliant on stable raw material prices and availability, grapple with margin compression risks due to agricultural input volatility. The 2024 UK Food Security Report highlights significant surges in agricultural input costs[3]Source: UK Government," United Kingdom Food Security Report 2024: Theme 3: Food Supply Chain Resilience", gov.uk. Geopolitical events have notably driven up fertilizer prices, which in turn have escalated livestock feed costs and, subsequently, collagen raw material prices. Adding to this pricing volatility are Brexit-related trade dynamics: with 64% of the UK's food imports sourced from the EU, manufacturers face currency fluctuations and regulatory compliance costs that influence collagen ingredient pricing. In response, manufacturers are turning to vertical integration and alternative sourcing strategies to buffer against these cost fluctuations. However, these strategies demand both capital and operational adjustments. While there's a notable shift towards marine collagen sources to reduce reliance on livestock, marine raw materials come with their own set of sustainability and availability challenges, curbing scalability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Sustainability-Anchored Diversification

In 2025, the UK collagen market saw animal-derived peptides firmly at the helm, commanding a robust 67.62% market share. This dominance is largely attributed to established supply chains, competitive pricing, and a consumer base well-acquainted with bovine and porcine sources. Even with rising sustainability concerns, the versatility of animal collagen in nutraceuticals, functional foods, and personal care ensures its continued preference. UK manufacturers enjoy the advantages of a seasoned processing infrastructure and dependable sourcing channels, leading to consistent pricing benefits. Retailers, recognizing the demand, allocate prime shelf space to these traditional formats. Thus, while there's a burgeoning interest in alternative sources, animal peptides steadfastly anchor the UK's collagen market, ensuring both stability and revenue.

On the other hand, marine and biotech collagen formats, though starting from a smaller base, are witnessing rapid growth and attracting significant investments. Marine collagen, boasting a systemic absorption rate four times faster, is particularly sought after in sports nutrition, glycemic-control beverages, and markets catering to active lifestyles. Its appeal is further bolstered by sustainability credentials, with brands emphasizing zero-waste strategies by valorizing fish-processing by-products. This aligns seamlessly with the UK's rising consumer inclination towards circular economy principles. Biotech collagen, while demanding substantial capital, is carving its niche due to its consistent batch quality, a trait highly valued by cosmetic formulators for achieving desired texture and performance. The FSA's clearer Novel Food pathway is streamlining the adoption of fermentation-derived molecules by easing regulatory hurdles. Additionally, regional investments in purification units at Grangemouth and Plymouth are fortifying local supply chains, especially in the evolving post-Brexit trade landscape. Collectively, marine and biotech collagens are not just reshaping the competitive arena but are elevating the category from mere commodities to specialized functional bioactives, emphasizing metabolic health benefits.

By End User: Healthcare Backbone Supports Consumer Upside

In 2025, dietary supplements dominated the United Kingdom's collagen market, capturing 46.85% of the total revenue. This stronghold is primarily bolstered by an aging population, especially women, who are increasingly turning to proactive measures for joint health and skin care. The supplement category has evolved, with gummies and stick packs leading the charge in mass-market retail, thanks to their convenience and taste. Concurrently, specialized e-commerce platforms have carved out a niche for premium hydrolyzed collagen powders, often bundled in subscription models to foster repeat purchases and build consumer loyalty. These trends position supplements as the primary driver of volume, seamlessly intertwining wellness, beauty, and preventive health in ways unmatched by other sectors. Given the sustained enthusiasm from proactive consumers, dietary supplements are set to cement their pivotal role in bolstering the UK collagen market.

Conversely, the personal care and cosmetics sector is emerging as the fastest-growing application, with projections indicating a CAGR of 6.63% through 2031. This surge is fueled by a growing consumer fascination with "ingestible beauty," now seen as a natural extension of daily skincare. While millennials were the early adopters, Gen X's swift embrace has broadened the demographic reach. This segment capitalizes on collagen's versatile benefits: topical applications cater to surface needs, while ingestibles promote internal beauty, fostering a synergistic demand cycle. Furthermore, cosmetic formulators are drawn to collagen for its consistency and functionality, enhancing its allure in premium skincare and nutricosmetic offerings. As trust in collagen as a sustainable beauty and wellness remedy deepens, the personal care and cosmetics sector is poised to outstrip all other collagen applications in growth, potentially redefining the market's future demand landscape.

Geography Analysis

In the UK collagen market, regional dynamics are influenced by factors like income levels, industrial history, and access to raw materials. Southeast England, led by London, dominates with a 28.75% share of consumption. This is largely due to the presence of numerous specialty retailers, private aesthetic clinics, and direct-to-consumer fulfillment hubs. This concentration not only boosts consumption but also accelerates the introduction of new products, particularly from digitally-savvy supplement brands targeting affluent households. The region's well-developed logistics infrastructure and proximity to high-income consumers further enhance its position as a key market hub.

Scotland's coastal stretch, from Aberdeen to Oban, is emerging as the fastest-growing area, with projections of a 7.01% CAGR. This growth is driven by marine collagen extraction facilities, strategically located near fisheries and operating under zero-waste mandates. Local councils are incentivizing the upcycling of fish skins with green grants, attracting processing investments. This not only shortens supply chains but also fosters skilled job creation. Additionally, the region's focus on sustainability aligns with global collagen market trends, making it an attractive destination for investors seeking eco-friendly production practices.

The Midlands and Northern regions play a pivotal role, producing significant outputs through established bovine-rendering and pharmaceutical-grade gelatin plants catering to healthcare clients. In the wake of Brexit, customs challenges led many processors to shift their raw-material inflow routes from Dover to Liverpool, aiming to alleviate congestion. This strategic adjustment has helped maintain supply chain efficiency despite regulatory changes. Additionally, Northern Ireland is capitalizing on its dual-market access, maintaining robust cross-border trade with the Republic of Ireland. This is particularly evident in the export of medical-device collagen, which meets the stringent standards of both UKCA and CE markings. The region's ability to navigate complex regulatory environments has positioned it as a critical player in the collagen supply chain.

Competitive Landscape

The United Kingdom's collagen market exhibits moderate concentration. Strategic consolidation is on the rise, highlighted by RTI Surgical's 2024 acquisition of Glasgow's Collagen Solutions. This move gives the U.S. firm comprehensive oversight, spanning from biomaterial research and development to the production of finished medical devices. The acquisition underscores a trend towards vertical integration, particularly in hastening innovation cycles for cardiac and orthopedic implants.

Rousselot and Nitta Gelatin are carving out a niche through technological differentiation, rolling out peptide platforms tailored for glucose modulation and supporting the gut-joint axis. Their collaborations with contract formulation firms in Surrey and Nottingham facilitate the swift transition of these peptide innovations into market-ready products. Meanwhile, biotech newcomers like Evonik are pioneering fermentation-derived vegan collagen, garnering swift traction with ethical cosmetics brands prioritizing cruelty-free standards.

Direct-to-consumer brands are harnessing micro-influencer strategies and data-driven subscription pricing to capture market share, all without the heft of traditional ad budgets. However, they tread carefully under compliance watch; only those brands bolstering their claims with randomized-controlled data enjoy sustained success. Established players, armed with regulatory know-how, adeptly maneuver through FSA dossiers and MHRA device registrations, a savvy edge that leaves underfunded startups grappling with extended approval delays.

United Kingdom Collagen Industry Leaders

-

Darling Ingredients Inc.

-

Nitta Gelatin Inc.

-

Tessenderlo Group

-

Weishardt Holding SA

-

GELITA AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Absolute Collagen unveiled its Crystal Clarity Marine Collagen Powder, earning accolades from both the Skin Health Alliance and B Corp. A clinical trial involving 130 participants revealed that every user noted enhancements in fine lines and skin evenness after just 12 weeks, establishing a new benchmark for efficacy.

- February 2025: Italgel SpA bolstered its foothold in the food, pharmaceutical, and nutraceutical arenas by acquiring Protein SA, a Spanish collagen producer. This strategic acquisition is poised to amplify Italgel's capacity and broaden its offerings in the burgeoning gelatin and collagen market.

- February 2024: Evonik rolled out Vecollage Fortify L, a vegan collagen ingredient derived from fermentation, targeting the beauty and personal care industry. This biotech innovation not only meets the rising demand for sustainability and ethics among consumers but also delivers benefits akin to natural skin collagen.

- January 2024: Proto-col debuted its Marine Beauty Collagen supplement, packed with 10,000mg of Bioactive Collagen Peptides, hyaluronic acid, and essential vitamins, all tailored for optimal skin health. To enhance accessibility, the supplement comes with subscription options and attractive discounts.

United Kingdom Collagen Market Report Scope

Collagen is a structural protein found in skin, tendons, and bones, offering nutritional, skin, and health benefits.

The United Kingdom collagen market is segmented by form and end-user. Based on the form, the market is segmented into animal-based and marine-based. By end-user, the market is segmented into animal feed, personal care and cosmetics, food and beverages, and supplements. The food and beverage segment is further sub-segmented into bakery, beverages, breakfast cereals, and snacks. The supplement segment is further sub-segmented into elderly nutrition and medical nutrition, and sport/performance nutrition.

The market sizing has been done in value terms in USD and for volume terms in volume in tons for all the abovementioned segments.

By Source

| Animal-based |

| Marine-based |

By End User/Application

| Food and Beverages |

| Dietary Supplements |

| Personal Care and Cosmetics |

| Pharmaceuticals |

| Animal Nutrition |

| By Source | Animal-based |

| Marine-based | |

| By End User/Application | Food and Beverages |

| Dietary Supplements | |

| Personal Care and Cosmetics | |

| Pharmaceuticals | |

| Animal Nutrition |

Key Questions Answered in the Report

How large is the United Kingdom collagen market today?

The market measured USD 662.25 million in 2026 and is projected to reach USD 897.84 million by 2031.

Which segment consumes the most collagen in the UK?

Dietary supplements led with 46.85% share in 2025, driven by seniors and wellness-oriented consumers.

What CAGR is expected for personal-care uses of collagen?

Personal care and cosmetics is forecast to grow at a 6.63% CAGR during 2026-2031.

How important is marine collagen in future supply?

Marine peptides offer faster absorption and sustainability benefits, supporting a 7.01% CAGR in Scottish coastal production zones.

Page last updated on: