Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

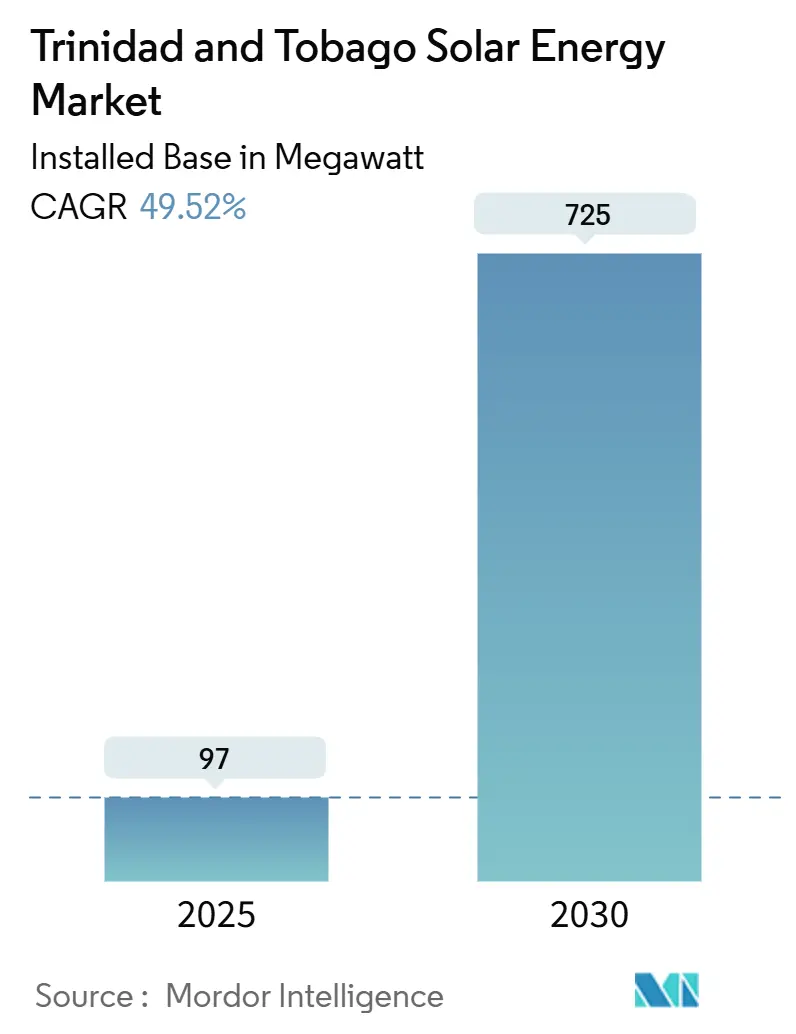

| Market Volume (2025) | 97 megawatt |

| Market Volume (2030) | 725 megawatt |

| Growth Rate (2025 - 2030) | 49.52% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Trinidad And Tobago Solar Energy Market Analysis by Mordor Intelligence

The Trinidad And Tobago Solar Energy Market size in terms of installed base is expected to grow from 97 megawatt in 2025 to 725 megawatt by 2030, at a CAGR of 49.52% during the forecast period (2025-2030).

This steep curve mirrors a national shift away from gas-fired generation and toward utility-scale photovoltaic parks that enjoy state backing and international capital. Falling module prices, rising electricity tariffs for commercial and industrial (C&I) users, and a growing pipeline of state-land projects are widening the addressable base for both grid-connected and off-grid systems. The inaugural 92 MW Brechin Castle Solar Park, synchronized in July 2025, validated grid integration and opened the door for follow-up tenders. Meanwhile, rural electrification gaps and agricultural incentives are steering fresh demand toward battery-paired off-grid arrays. Competitive intensity is still light, but joint ventures between oil majors and the National Gas Company (NGC) are setting a template for large projects while a cluster of local installers competes on speed, financing, and after-sales service.

Key Report Takeaways

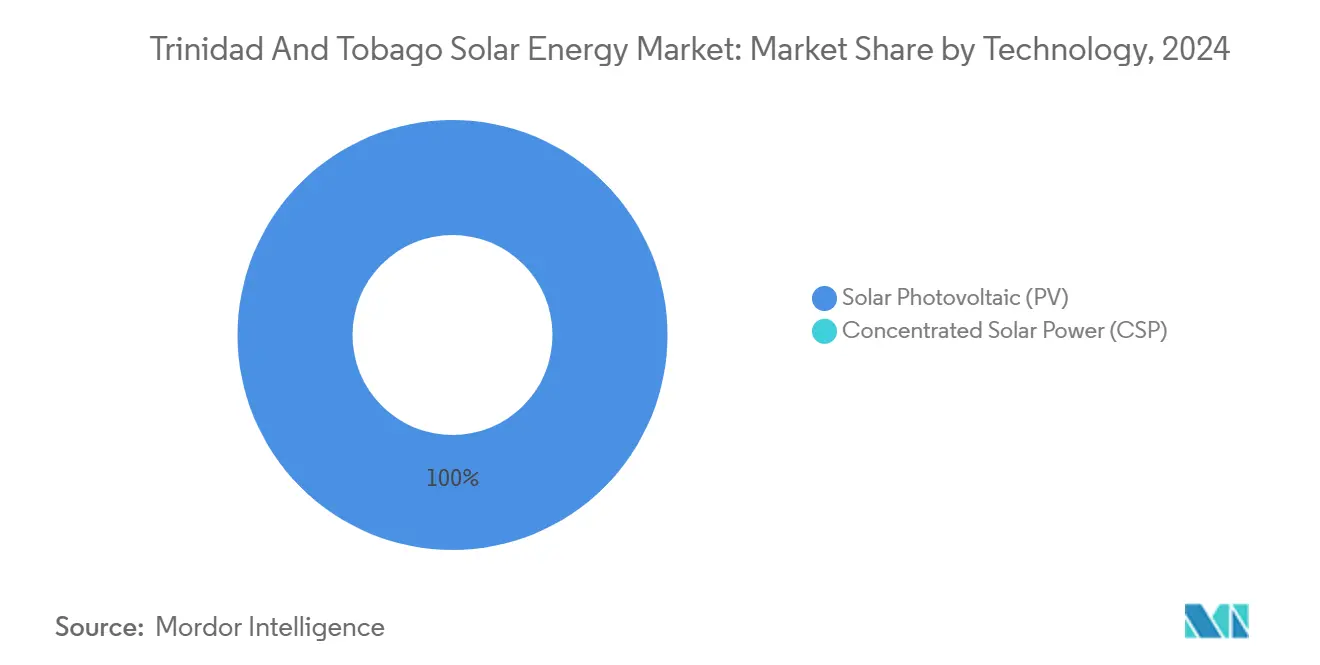

- By technology, photovoltaic systems captured 100% of Trinidad and Tobago's solar energy market share in 2024.

- By grid type, on-grid assets held 99.1% of the Trinidad and Tobago solar energy market size in 2024, while the off-grid segment is advancing at a 75.1% CAGR to 2030.

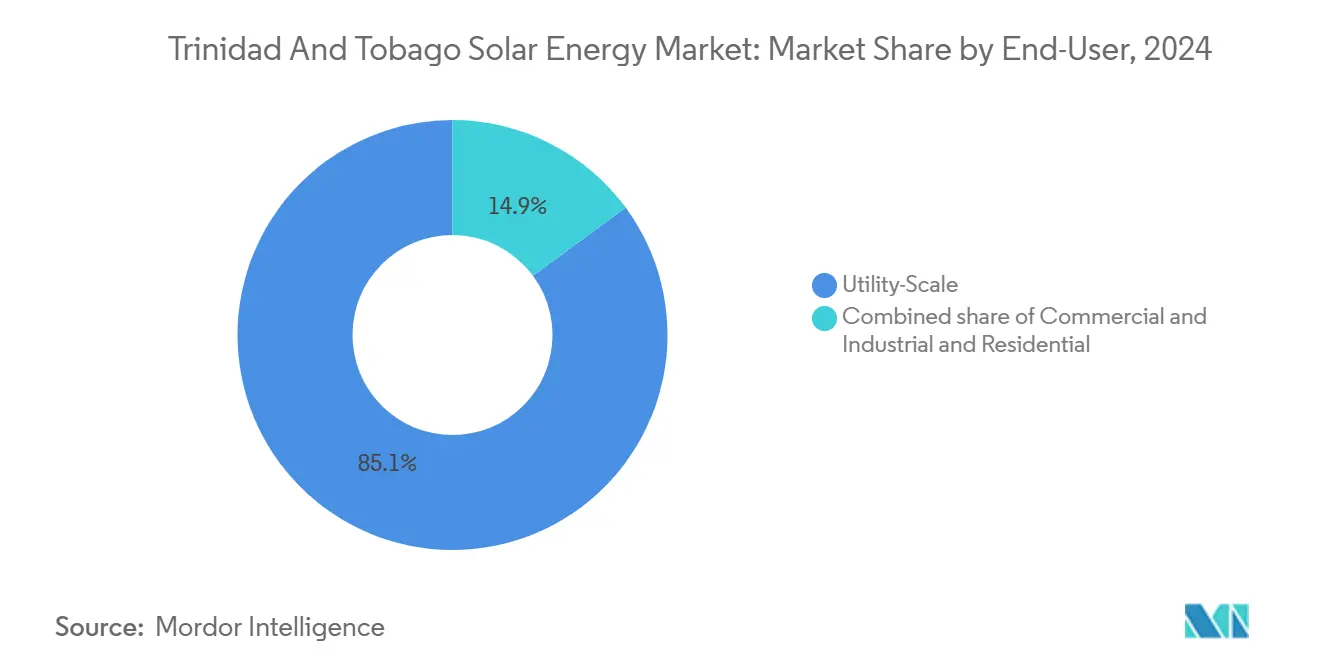

- By end-user, utility-scale installations commanded 85.1% of the Trinidad and Tobago solar energy market size in 2024; residential capacity is forecast to expand at a 58.3% CAGR through 2030.

- By geography, Trinidad accounted for 95% of total capacity in 2024 and remains the dominant demand center through 2030.

Trinidad And Tobago Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National 30% Renewable-Electricity Target by 2030 | +12.5% | Nationwide, early focus on Point Lisas and Port of Spain | Medium term (2-4 years) |

| Declining Global PV Module Prices | +8.3% | Imports via Port of Spain for residential and C&I rooftops | Short term (≤2 years) |

| 92 MW Brechin Castle Flagship Project | +10.2% | Central Trinidad grid node near Point Lisas | Short term (≤2 years) |

| Rising Electricity Tariffs and Emerging Gas Constraints | +9.8% | Country-wide, highest pain for C&I users | Medium term (2-4 years) |

| Fiscal Incentives for Local Component Manufacturing | +3.1% | National special-economic zones | Long term (≥4 years) |

| ISCC Retrofits for Gas Plants | +2.9% | Point Lisas and Penal industrial zones | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

National 30% Renewable-Electricity Target by 2030

The Vision 2030 framework obliges the grid to secure 30% renewable power by decade-end, implying 450-500 MW of additional solar and wind. Cabinet sign-off of Brechin Castle referenced Paris Agreement goals, positioning solar as a compliance tool rather than a discretionary play.[1]bp Trinidad and Tobago, “Brechin Castle Solar Park Fact Sheet,” bp.com In February 2025, the Prime Minister signaled that up to 300 MW of solar could occupy state land, hinting at auction-based procurement that should push tariffs under the USD 0.06745 /kWh benchmark. The Regulated Industries Commission (RIC) continues tariff hearings, and the Energy Ministry is still refining a feed-in tariff (FiT) bill, underscoring execution risk. Pilot systems on public schools, such as the 15 kW array in Charlotteville, were commissioned in September 2024, demonstrating proof of concept for rooftop roll-outs.

Declining Global PV Module Prices

Average global module prices slipped to USD 0.13 /Wp in 2024, down nearly 50% from early 2022 as polysilicon oversupply widened.[2]Fraunhofer ISE, “Photovoltaics Report 2024,” ise.fraunhofer.de Ex-port landed costs enjoy VAT exemptions and duty-free entry, enabling residential payback periods of 5-8 years even without net-billing.[3]Ministry of Finance, “Customs Act Schedule of Zero-Rated Goods,” finance.gov.tt Utility-scale levelized costs of USD 0.042 /kWh undershoot Trinidad’s latest PPA, suggesting room for cheaper bids once tender pipelines firm. Installers report a pivot to Tier-1 suppliers such as Canadian Solar and JA Solar because warranty terms and quality assurance outweigh marginal price gaps.

92 MW Brechin Castle Flagship Project

Synchronized in July 2025, Brechin Castle is Trinidad’s first utility-scale renewable plant and provides a 302,500 MWh yearly boost to the grid, displacing 165,500 t of CO₂. BP and Shell each hold 35% equity, while NGC controls 30%, signalling a durable public-private model for future builds. The three-year slide from preferred bidder to first power spotlights permitting delays that the Government vows to streamline.

Rising Electricity Tariffs and Emerging Gas Constraints

Residential tariffs linger near USD 0.05 /kWh, yet the RIC’s 2024 review and a confirmed 2026 C&I surcharge portend sharper climbs. Proposed hikes could take C&I bills toward USD 0.59 /kWh by 2028, tipping rooftop economics in favor of self-consumption arrays. Domestic gas production is falling; the Dragon field deal with Venezuela will prop up supply only from 2028, reinforcing renewable diversification urgency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Abundant low-cost natural-gas generation | -6.7% | National, with strongest impact on residential segment where subsidized tariffs persist | Short term (≤ 2 years) |

| Absent FiT / net-billing framework | -5.4% | National, disproportionately affecting residential and small C&I adopters | Medium term (2-4 years) |

| Limited retail & C&I financing options | -3.2% | National, with gaps most acute in rural Tobago and eastern Trinidad | Short term (≤ 2 years) |

| Cloud-driven yield volatility in tropical micro-climates | -2.1% | National, with higher variability in northern coastal zones and Tobago | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Abundant Low-Cost Natural-Gas Generation

Gas still meets 99% of electricity demand and is supplied to T&TEC under subsidized contracts, shaving fuel costs well below regional norms.[4]Energy Institute, “Statistical Review of World Energy 2025,” energyinst.org Such pricing mutes the retail signal for rooftop solar and complicates policy decisions, as lifting subsidies would inflate both utility deficits and household bills. The Dragon field tie-back will extend cheap supply to 2042, putting a ceiling on near-term solar upside unless carbon pricing or binding quotas intervene.

Absence of FiT / Net-Billing Framework

Without FiT or net-billing, small producers cannot monetize surplus generation, so system sizing sticks close to daytime load. Draft legislation has circulated since 2022 but remains unsigned, dampening lender confidence. Bilateral PPAs are viable only for large arrays, leaving households to fund systems in cash or through bank loans without export revenue.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Photovoltaic Monopolizes Capacity

Photovoltaic systems owned 100% of installed capacity in 2024 and are set to keep that lock through 2030 as crystalline-silicon modules continue to outprice any alternative. Utility-scale projects like Brechin Castle have standardized on Tier-1 panels and SMA inverters, forging a bankable template that eases financing. The Trinidad and Tobago solar energy market size for photovoltaic assets is projected to surge at 49.5% annually through 2030, while concentrated solar power remains absent.

Battery coupling remains rare, but falling lithium-iron-phosphate prices and impending time-of-use tariffs are expected to lift attachment rates later in the decade. Microinverters from Enphase and APsystems are gaining ground on residential rooftops where shading and expansion flexibility matter, whereas string inverters dominate C&I arrays seeking lower capex. Hurricane-rated racking, certified for 160 mph winds, adds 10-15% to upfront cost yet is now standard across island installations.

By Grid Type: Off-Grid Growth Accelerates in Rural Zones

On-grid arrays represented 99.1% of total capacity in 2024, a weighting driven by utility-scale builds and urban rooftops with strong interconnection. Off-grid systems, however, are forecast to compound at 75.1% per year thanks to TTD 25,000 agricultural rebates and limited grid presence in eastern Trinidad and rural Tobago. Trinidad and Tobago's solar energy market share for off-grid installations, minor today, will expand quickly as farms deploy standalone pumps, cold storage, and lighting.

T&TEC's USD 25 million grid-modernization program, including mobile substations and fault indicators, reduces interconnection hurdles, yet regions where extension costs exceed USD 20,000 per kilometer still favor solar-plus-storage microgrids. Community centers, clinics, and schools already run on donor-funded rooftops, while coastal street-light programs demonstrate durability in salt and humidity.

By End-User: Residential Pace Overtakes Utility Scale

Utility-scale plants controlled 85.1% of capacity in 2024, underpinned by Brechin Castle. Nonetheless, residential rooftops are forecast to grow at a 58.3% CAGR to 2030, supported by 100%-financed loans from CIBC Caribbean and emerging tariff reform. The commercial-and-industrial segment faces a fresh TTD 0.05 /kWh surcharge in 2026, nudging energy-intensive firms toward self-generation.

Trinidad and Tobago solar energy market size for residential users is poised to expand sharply as loan amortization begins to mirror monthly bills. Meanwhile, a state-backed real-estate investment trust, launched in 2026, could buy completed utility-scale assets, recycling developer capital into new projects.

Geography Analysis

Trinidad owned 95% of installed capacity in 2024, anchored along the Port of Spain–San Fernando industrial corridor. Brechin Castle and the forthcoming Couva Solar Park cluster around robust 132 kV lines near Point Lisas, easing transmission and serving ammonia and methanol plants. Urban rooftops proliferate in Port of Spain, San Juan, Maraval, and Chaguanas, where installer networks and financing are strong.

Tobago lags with less than 5% share but is gaining traction through school and clinic pilots. The Charlotteville Methodist Primary School array embodies a template for 500-plus public buildings nationwide. Rural districts from Sangre Grande to Cedros still rely on diesel, making them prime candidates for off-grid solar that leverages agricultural rebates.

Average annual insolation of 1,610 kWh/m² supports a 13.2% capacity factor, yet Saharan dust and high ambient temperatures trim yields, underscoring the need for performance-ratio adjustments and robust operations and maintenance (O&M) protocols.

Competitive Landscape

International developers dominate the Trinidad and Tobago solar energy market utility projects. Lightsource bp manages construction at Brechin Castle while bp and Shell each hold 35% equity, and NGC keeps 30%, forging a reliable public-private template. The 112.2 MW Couva Solar Park, announced in April 2025, signals further scale and may invite new entrants if auctions proceed.

Domestic installers, including Resscott, AIMS Power, SolarWorld-tt, and Trifactor, compete on financing, speed, and O&M. Resscott’s alliance with U.K.-based JCE Energy expands its reach into explosion-proof solutions for petrochemical sites [jceenergy.com]. Bank partnerships underpin residential momentum; CIBC Caribbean has already lent over USD 150 million across 130 MW of Caribbean renewables.

Three white-space niches stand out: agrivoltaics under the TTD 25,000 rebate, solar-plus-storage resilience systems for C&I properties, and desalination powered by rooftop arrays along tourism-heavy coasts. The new disclosure law for special-purpose vehicles adds compliance cost but should reassure project-finance lenders.

Trinidad And Tobago Solar Energy Industry Leaders

Lightsource BP / BCSL JV

Shell Renewables Caribbean

SolarWorld-tt

Resscott Ltd

AMBA Energy Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Energy Minister Stuart Young revealed that a consortium of Lightsource BP, Shell, and BP is set to break ground on two expansive solar farms. Positioned at Brechin Castle and Orange Grove, these projects aim for completion in the next 18 to 24 months.

- April 2025: In Trinidad and Tobago, Digicel and Caban Energy teamed up to offer holistic solar energy solutions. Their goal is to roll out cutting-edge solar technology throughout the islands, thereby shrinking the nation's carbon footprint and promoting enhanced energy autonomy.

- November 2024: 15 kW rooftop array energized at Charlotteville Methodist Primary School, Tobago’s first solar-powered public building

Trinidad And Tobago Solar Energy Market Report Scope

Solar energy is heat and radiant light from the Sun that can be harnessed with technologies such as solar power (which is used to generate electricity) and solar thermal energy (which is used for applications such as water heating).

The Trinidad and Tobago solar energy market is segmented by technology, grid type, end-user, and geography. By technology, the market is segmented into solar photovoltaic PV) and concentrated solar power CSP. By grid type, the market is segmented into on-grid and off-grid. By end-user, the market is segmented into utility-scale, commercial and industrial C&I, and residential. By component, the market is segmented into solar modules, inverters, mounting and tracking systems, balance-of-system and electricals, energy storage, and hybrid integration. The market sizing and forecasts have been done based on installed capacity (MW).

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Key Questions Answered in the Report

How large is the Trinidad and Tobago solar energy market in 2025?

Installed capacity stands at 97 MW, and the Trinidad and Tobago solar energy market size is forecast to hit 725 MW by 2030.

What CAGR is expected for solar capacity through 2030?

Capacity is projected to grow at a 49.52% CAGR between 2025 and 2030.

Which segment is expanding fastest?

Off-grid systems lead with a 75.1% annual growth rate as rural and agricultural users adopt standalone arrays.

Who are the leading utility-scale developers?

Lightsource bp, bp, Shell, and the National Gas Company dominate large projects, starting with the 92 MW Brechin Castle park.

How do electricity tariffs influence adoption?

Rising C&I tariffs and a planned surcharge in 2026 shorten payback periods to 5-8 years for rooftop systems, boosting uptake.

What policy gap most hinders residential solar?

The absence of a feed-in tariff or net-billing scheme limits revenue from surplus power exports, constraining system sizing.

Page last updated on: