Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

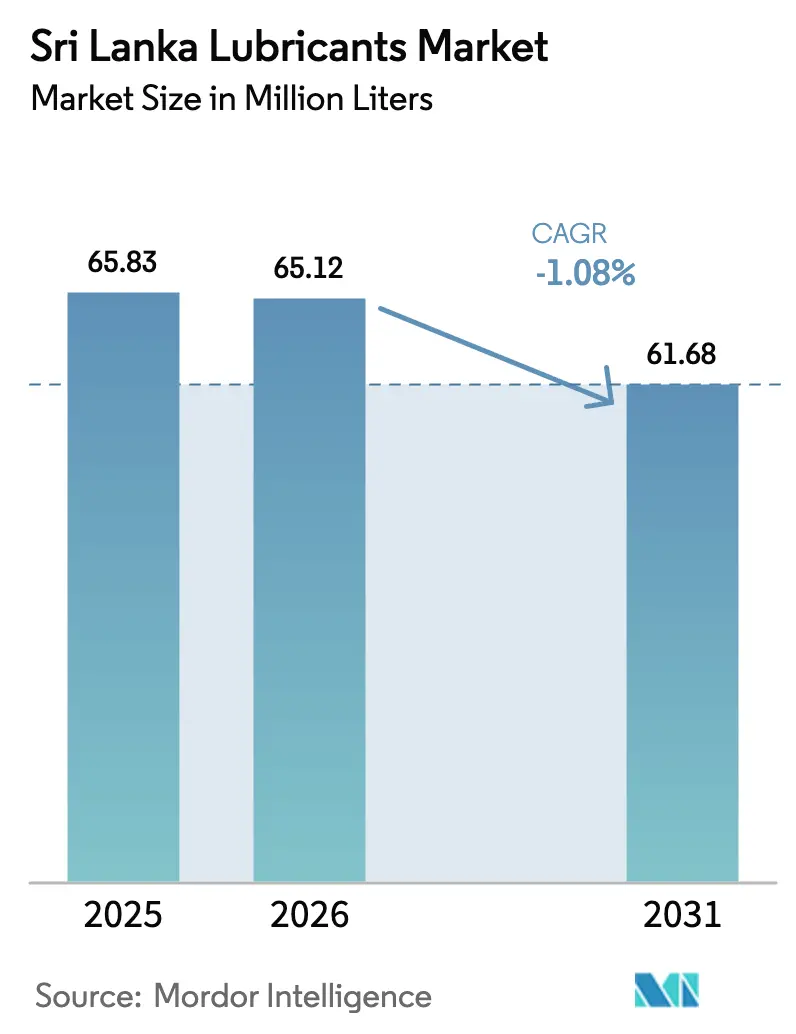

| Base Year Market Size (2025) | 65.83 Million liters |

| Market Volume (2026) | 65.12 Million liters |

| Market Volume (2031) | 61.68 Million liters |

| Growth Rate (2026 - 2031) | -1.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sri Lanka Lubricants Market Analysis by Mordor Intelligence

The Sri Lanka Lubricants Market size is projected to contract from 65.83 Million liters in 2025 and 65.12 Million liters in 2026 to 61.68 Million liters by 2031, registering a CAGR of -1.08% between 2026 to 2031. In 2024-2025, the market experienced a brief rebound, but three structural shifts have since reshaped the landscape. Firstly, the swift electrification of the three-wheeler fleet has eliminated a significant demand for engine oil. Secondly, a shift towards renewable energy sources in power generation has dampened the demand for turbine and transformer oils. Lastly, the increasing adoption of synthetic blends is extending oil-drain intervals. However, these shifts are countered by the lifting of a three-year vehicle import embargo in February 2025. This move brought in a surge of fresh vehicles, rejuvenating service activities linked to original equipment manufacturers (OEMs). Additionally, buoyed by the expansion in manufacturing and construction in 2024, industrial output saw a recovery, bolstering the demand for hydraulic fluids and greases. On another front, the liberalization of the downstream sector led to a surge in licensed lubricant players, doubling their numbers by the end of 2023. This influx intensified price competition and accelerated a trend of consumers downgrading during the crisis of 2022.

Key Report Takeaways

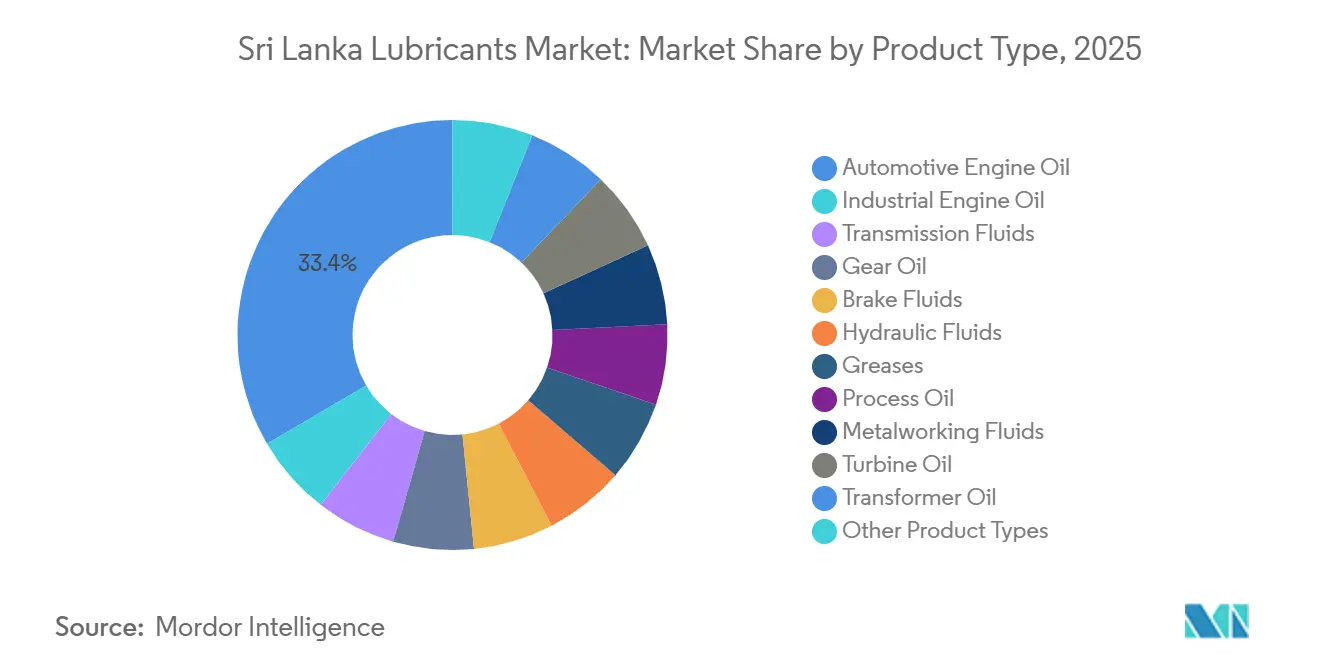

- By product type, automotive engine oil captured 33.44% of Sri Lanka's lubricant market share in 2025, while the industrial engine oil segment is projected to contract at -0.95% CAGR through 2031.

- By end-user industry, the automotive end-user segment accounted for 55.25% of Sri Lanka's lubricant market size in 2025; by contrast, the industrial segment is projected to contract at -0.54% CAGR through 2031.

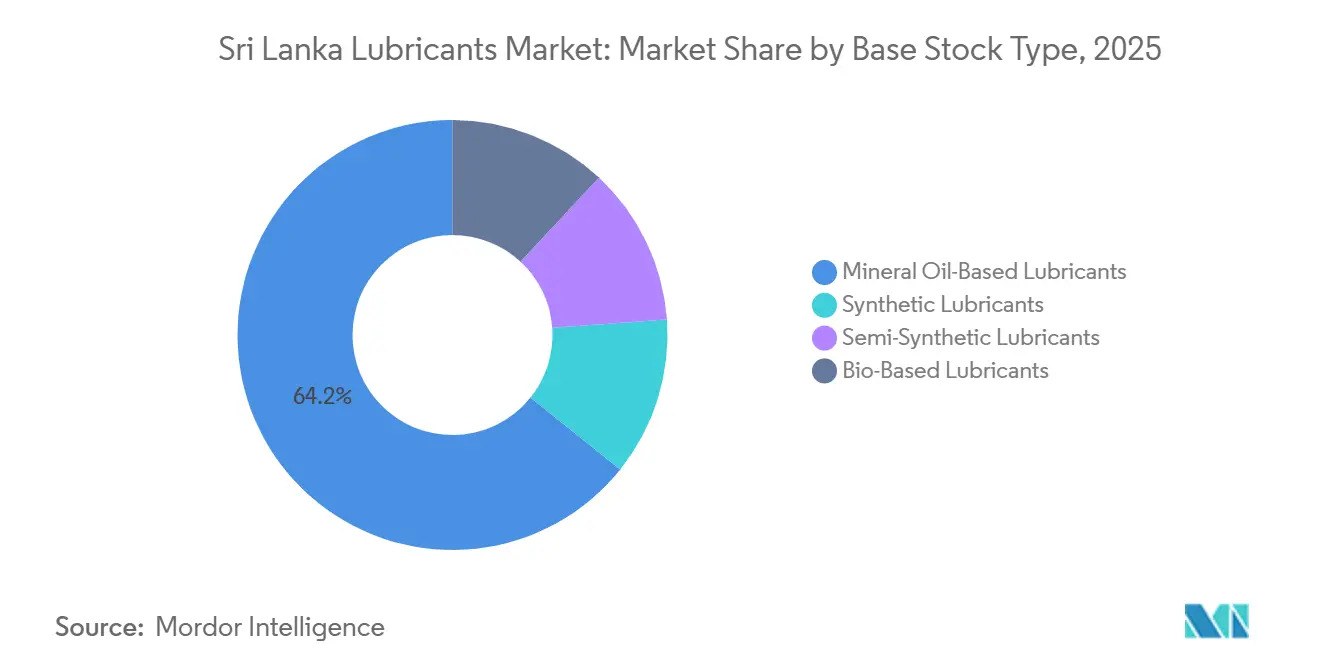

- By base stock type, mineral-oil formulations maintained a 64.23% slice of Sri Lanka's lubricant market share in 2025, while bio-based lubricants, though still niche, are the fastest-growing product category at a 0.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Sri Lanka Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing vehicle parc and replacement cycles | +0.3% | National, concentrated in Western Province (Colombo, Gampaha) | Medium term (2-4 years) |

| Expanding agricultural mechanization | +0.1% | National, with early gains in North Central, Eastern, and Northern Provinces | Long term (≥ 4 years) |

| Capacity additions in thermal and diesel power plants | +0.1% | National (minimal impact; renewable focus dominates) | Long term (≥ 4 years) |

| Stricter OEM warranty compliance pushing premium lubes | +0.2% | National, urban centers and authorized service networks | Short term (≤ 2 years) |

| Rapid rise of 2-wheeler last-mile delivery fleets | +0.2% | National, concentrated in Colombo, Kandy, Galle metro areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Vehicle-Parc and Replacement Cycles

In February 2025, Sri Lanka lifted a three-year embargo on vehicle imports, leading to an influx of new units by July. This surge not only replenished dealer inventories but also revived previously inactive service bays. By 2024, Sri Lanka's registered vehicle fleet had increased significantly[1]Department of Motor Traffic, “Registered Vehicle Statistics 2024,” dmt.gov.lk. However, as the average age of these vehicles increased, so did the demand for lubricants, with older engines necessitating more frequent oil changes. Although import duties were reduced as part of an IMF agreement, this move introduced policy uncertainties that might dampen future inflows. Nevertheless, there's been a resurgence in demand for premium synthetic lubricants at brand-authorized workshops, helping to counterbalance some volume losses attributed to the shift towards electrification. Overall, these dynamics have reshaped Sri Lanka's lubricant market demand profile.

Expanding Agricultural Mechanization

Agriculture posted GDP growth in Q2 2024, supported by programs subsidizing small-holder mechanization in paddy and export-crop estates. Compact tractors and power-tillers lift seasonal demand for hydraulic oils and diesel-engine lubricants, particularly in North Central, Eastern, and Northern provinces, where mechanization rates lag. Fragmented equipment sales data and weather-driven planting cycles limit steady pull-through, yet incremental volumes add a +0.1% lift to long-term growth. Labor out-migration and erratic monsoons temper upside, keeping agriculture a supportive but not transformative driver of the Sri Lankan lubricant market.

Stricter OEM Warranty Compliance Pushing Premium Lubes

Castrol’s ASEAN engine-warranty scheme covers repairs for customers using fully synthetic formulations, while Petronas partnered with Mercedes-Benz in April 2024 to embed factory-fill specifications in after-sales networks. Locally, LAUGFS Lubricants touts endorsements from Porsche and Volvo, signaling that warranty language is shifting buyer preferences in urban dealerships. The recovery of authorized workshops after the import ban revives adherence to OEM schedules, nudging consumers toward synthetic and semi-synthetic blends. Although price sensitivity curbs full migration, the dynamic adds +0.2% to the forecast CAGR for the Sri Lanka lubricant market.

Rapid Rise of 2-Wheeler Last-Mile Delivery Fleets

In FY 2024/25, Digital Mobility Solutions Lanka's PickMe platform boasted a significant number of active drivers and recorded substantial growth in rides compared to the previous year. Two-wheelers on the platform experienced heightened usage, which has shortened service intervals, driving up lubricant demand per bike. With a focus on Colombo, Kandy, and Galle, PickMe has established dense route networks that prioritize scheduled maintenance. While PickMe is piloting electric tuk-tuks, two-wheelers remain predominantly internal-combustion through the current forecast horizon, adding +0.2% to Sri Lanka's lubricant market forecast CAGR.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Slow-down in construction and mining projects | -0.3% | National, with concentration in Western and Southern Provinces | Medium term (2-4 years) |

| Crude-price volatility inflating base-oil costs | -0.4% | National (import-dependent supply chain) | Short term (≤ 2 years) |

| Accelerating penetration of electric 3-wheelers | -1.2% | National, urban centers (Colombo, Kandy, Galle) leading adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Price Volatility Inflating Base-Oil Costs

In 2024-2025, Brent prices fluctuated, putting pressure on blender margins in Sri Lanka, which relies entirely on imports for its base oils and additives. While the rupee saw an appreciation in 2024, reserves remained precariously low. This thin reserve exposes the currency to external shocks, potentially reversing any cost relief. Chevron Lubricants Lanka reported a significant drop in volume for 2022, yet managed a surge in earnings. This highlights that while price hikes can safeguard profits, they also drive consumers towards down-trading and adulteration. Although a planned upgrade at the Sapugaskanda refinery promises to boost local base-oil production, it's not expected to be operational before 2029. In the interim, cost volatility subtracts -0.4% from the Sri Lanka lubricant market CAGR.

Accelerating Penetration of Electric 3-Wheelers

The government targets the conversion of petrol tuk-tuks within five years, and Evolution Auto launched Mahindra Treo models in June 2025, highlighting savings over petrol variants. PickMe has signaled fleet-wide adoption once charging density improves, and early pilots show technical feasibility. Each electric 3-wheeler removes annual engine oil demand; this restraint is irreversible and deepens beyond the current forecast window for the Sri Lankan lubricant market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oils Anchor Demand Amid Specialty Segment Erosion

Automotive engine oil accounted for 33.44% of Sri Lanka's lubricant market share in 2025, solidifying its status as the dominant category, even amidst a downturn. Industrial engine oil demand is forecast to slide at -0.95% CAGR through 2031. This is largely due to the Ceylon Electricity Board's ambition to achieve a renewable capacity target, leading to more frequent maintenance cycles for diesel generators[2]Asian Development Bank, “Sri Lanka Power Sector Renewable Roadmap,” adb.org. While transmission fluids and gear oils benefit momentarily from new vehicle imports, they are likely to be overshadowed in the long run as electric drivetrains become more prevalent. Hydraulic fluid usage, primarily linked to construction machinery, faces constraints due to a limited infrastructure pipeline. Metalworking fluids, buoyed by growth in apparel exports, find support in lubricants for spinning and weaving. As projects like Adani's wind initiative replace thermal plants, the demand for turbine and transformer oils diminishes. However, the process oil demand in tire manufacturing remains stable. Greases and brake fluids maintain a consistent, albeit modest, trajectory. This is because, while electric vehicles (EVs) still need chassis lubrication and hydraulic braking, the demand is tapering off at a slower rate.

The product mix is increasingly favoring synthetic oils, which can extend oil-change intervals. This shift may reduce the volume sold in liters but boost revenue per liter. Warranty clauses from OEMs like Castrol and Petronas are steering customers towards formulations that meet API SP and ILSAC GF-7 standards. While engine oils continue to be the cornerstone of Sri Lanka's lubricant market, specialty segments are witnessing a decline as the nation moves towards electrification and digitization.

By End-User Industry: Automotive Dominance Masks Industrial Fragility

Automotive end users consumed 55.25% of Sri Lanka's lubricant market size in 2025, driven predominantly by passenger cars, commercial vehicles, and a rapidly expanding two-wheeler delivery fleet. Following the lifting of an import ban, demand for passenger vehicles showed signs of revival. However, a duty ceiling continues to exert price pressures, potentially limiting unit inflows. While domestic freight boosts volumes for commercial vehicles, rising diesel prices are tightening fleet margins. Two-wheelers, increasingly vital for last-mile logistics, are witnessing the highest utilization rates, consequently elevating oil consumption per unit. Additionally, marine bunkering at Colombo, bolstered by Lanka IOC’s market share, underscores a niche demand for environmentally friendly lubricants.

Industrial consumption is projected to decline at -0.54% CAGR through 2031. Notably, a tariff cut in 2024 signals an oversupply in baseload capacity. While textiles, which represent a significant portion of the country's merchandise exports, continue to drive demand for metalworking fluids, labor shortages are limiting their utilization. The heavy equipment sector, pivotal for construction and mining, remains tepid as elevated interest rates dissuade large civil projects. Meanwhile, agriculture's push towards mechanization contributes modestly but positively to lubricant volumes. As a result, the end-user distribution leans heavily towards the automotive sector, overshadowing the vulnerabilities of industrial demand in Sri Lanka's lubricant landscape.

By Base Stock Type: Mineral Oils Hold Volume While Bio-Based Gains Traction

Mineral oils still commanded 64.23% of Sri Lanka's lubricant market share in 2025, thanks to their price advantages and widespread availability at service stations. Meanwhile, synthetic grades, including poly-alpha-olefins and esters, are witnessing a surge in value as warranty-driven service centers increasingly recommend these longer-life products. Striking a balance between maintenance costs and operational uptime, semi-synthetics are carving out a niche, especially among commercial fleets.

Bio-based lubricants are the only category with a positive 0.66% CAGR through 2031. This growth is largely attributed to the IMO Resolution MEPC.391(81), which establishes life-cycle GHG thresholds for marine fuels and lubricants. Leveraging Colombo's strategic position as a bunkering hub, local suppliers like Lanka IOC are poised to expand their offerings of environmentally-friendly stern-tube and hydraulic oils. However, challenges loom: Sri Lanka's absence of a domestic oleochemical capacity means the segment heavily relies on imported vegetable-oil derivatives, which are benchmarked to palm-oil and soybean prices. Furthermore, with regulatory changes on the horizon, notably the petroleum regulator announced in August 2023, there's potential for stricter environmental compliance, which could further propel the adoption of bio-based lubricants.

Geography Analysis

In Sri Lanka, a unitary state, the demand for lubricants is predominantly centered in the Western Province. This province, home to the Colombo and Gampaha districts, boasts the highest density of private vehicles. Additionally, the Western Province is home to the Katunayake Export Processing Zone and the Port of Colombo, both of which are major consumers of marine and industrial lubricants. Meanwhile, the Central Province, anchored by Kandy, is witnessing a surge in two-wheeler deliveries, driven by rising e-commerce penetration, subsequently boosting the demand for engine and gear oils. In the Southern Province, tourist hotspots like Galle and the special economic zone at Hambantota Port are seeing a rise in bunkering and construction equipment activities, leading to an increased demand for hydraulic and marine lubricants.

The North Central, Eastern, and Northern provinces have seen a boost in tractor and harvester sales due to government mechanization subsidies. This, in turn, has led to seasonal spikes in hydraulic fluid demand. However, these provinces grapple with labor shortages from out-migration, limiting cropping intensity and keeping annual lubricant demand in check. Meanwhile, the Uva and Sabaragamuwa provinces, known for their tea and rubber estates, require process oils for their sheet rubber and rubber glove production. Yet, as these estates transition to modern machinery with enclosed lubrication circuits, there's a slight decrease in per-unit oil consumption.

Rural electrification has achieved 100% coverage across the island. In the Northern region, renewable energy projects are emerging near Mannar and Pooneryn, replacing thermal generation and consequently reducing turbine oil consumption. While the Western Province stands as the nucleus of Sri Lanka's lubricant market, the growth in other provinces is closely linked to localized sectoral developments, rather than a nationwide trend.

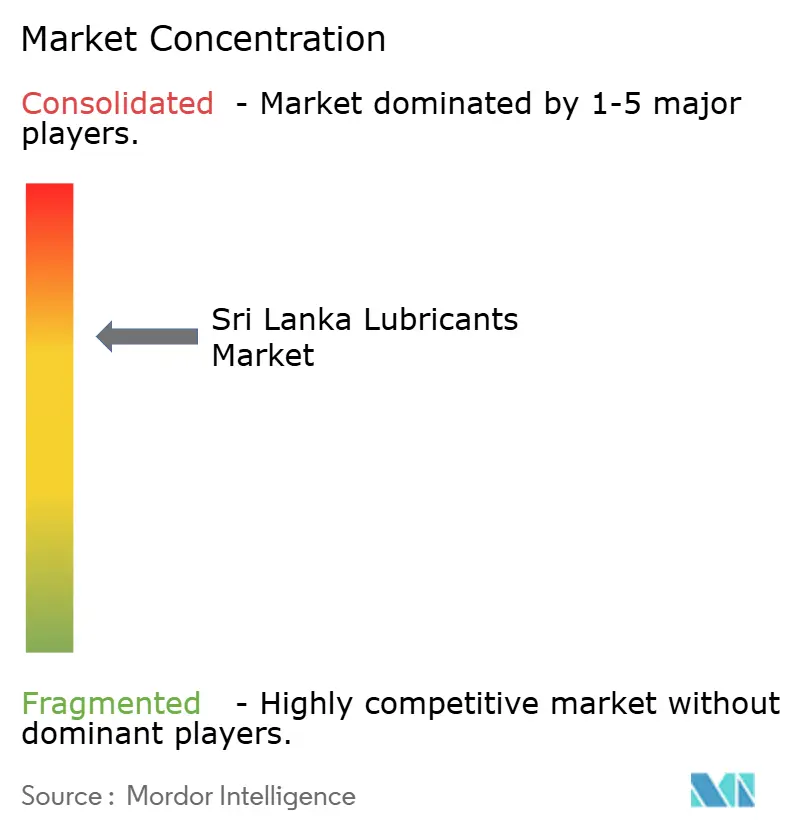

Competitive Landscape

The Sri Lankan lubricants market is moderately consolidated. Strategic plays coalesce around local-blending capacity, premium OEM tie-ups, and marine specialization. Quality assurance remains a flashpoint. The Ministry of Energy identified many unauthorized operators selling adulterated oils as early as 2015, and liberalization has not stamped out the shadow channel. A planned petroleum regulator aims to tighten product certification and labelling, but until enforcement strengthens, price gaps between branded and loose oils will persist, challenging the premium trajectory within the Sri Lankan lubricant market.

Sri Lanka Lubricants Industry Leaders

Chevron Sri lanka

Ceylon Petroleum Corporation

LAUGFS Lubricants Limited

BP Plc

Indian Oil Corporation Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BP Plc initiated the divestment of its Castrol business, valued at up to USD 10 billion, potentially reshaping Castrol’s channel strategy across South Asia.

- May 2025: TotalEnergies launched API SP and ILSAC GF-7 compliant Quartz 9000 Future engine oils suited for turbocharged and GDI engines.

Sri Lanka Lubricants Market Report Scope

Lubricants, such as oil or grease, reduce friction and wear between moving surfaces. By creating a separating film, they enable smooth and efficient operation. Beyond merely reducing friction, lubricants cool components, transmit power, seal out contaminants, and prevent corrosion. They can be found in liquid, semi-solid, solid, or even gaseous forms.

The Sri Lankan lubricant market is segmented by product type, end-user industry, and base stock type. By product type, the market is segmented into automotive engine oil, industrial engine oil, transmission fluids, gear oil, brake fluids, hydraulic fluids, greases, process oil (including rubber process oil and white oil), metalworking fluids, turbine oil, transformer oil, and other product types. By end-user industry, the market is segmented into automotive, marine, aerospace, heavy equipment, and industrial. By base stock type, the market is segmented into mineral oil-based lubricants, synthetic lubricants, semi-synthetic lubricants, and bio-based lubricants. For each segment, the market sizing and forecasts have been done based on volume (Liters).

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

Key Questions Answered in the Report

What volume decline is expected for the Sri Lankan lubricant market by 2031?

Volumes are projected to slip from 65.12 million liters in 2026 to 61.68 million liters by 2031, reflecting a -1.08% CAGR.

Which product segment still commands the largest share?

Automotive engine oil remained dominant, accounting for 33.44% of national consumption in 2025.

Why are bio-based lubricants gaining traction?

IMO life-cycle GHG rules for marine fuels and Colombo’s bunkering hub encourage shippers to switch to environmentally acceptable lubricants.

What role do OEM warranties play in lubricant selection?

Warranty clauses from brands like Castrol, Petronas, and LAUGFS push vehicle owners toward synthetic and semi-synthetic oils that meet stricter specifications.

Page last updated on: