Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 29.71 Billion |

| Market Size (2026) | USD 30.63 Billion |

| Market Size (2031) | USD 35.84 Billion |

| Growth Rate (2026 - 2031) | 3.19% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Fats and Oils Market Analysis by Mordor Intelligence

The Europe Fats and Oils Market size was valued at USD 29.71 billion in 2025 and estimated to grow from USD 30.63 billion in 2026 to reach USD 35.84 billion by 2031, at a CAGR of 3.19% during the forecast period (2026-2031). The European fats and oils market is driven by evolving dietary preferences that prioritize functionality, nutrition, and ingredient transparency. Consumers are increasingly opting for products with healthier lipid profiles, prompting manufacturers to reformulate foods with oils that are lower in saturated fats and higher in mono- and polyunsaturated fatty acids. This trend has boosted the use of high-oleic sunflower oil, rapeseed (canola) oil, and olive oil in products such as spreads, snacks, dairy alternatives, and ready meals. Additionally, the rising popularity of home cooking and scratch baking in several European countries has sustained consistent retail demand for cooking oils and baking fats, particularly those marketed as natural or minimally processed.

Key Report Takeaways

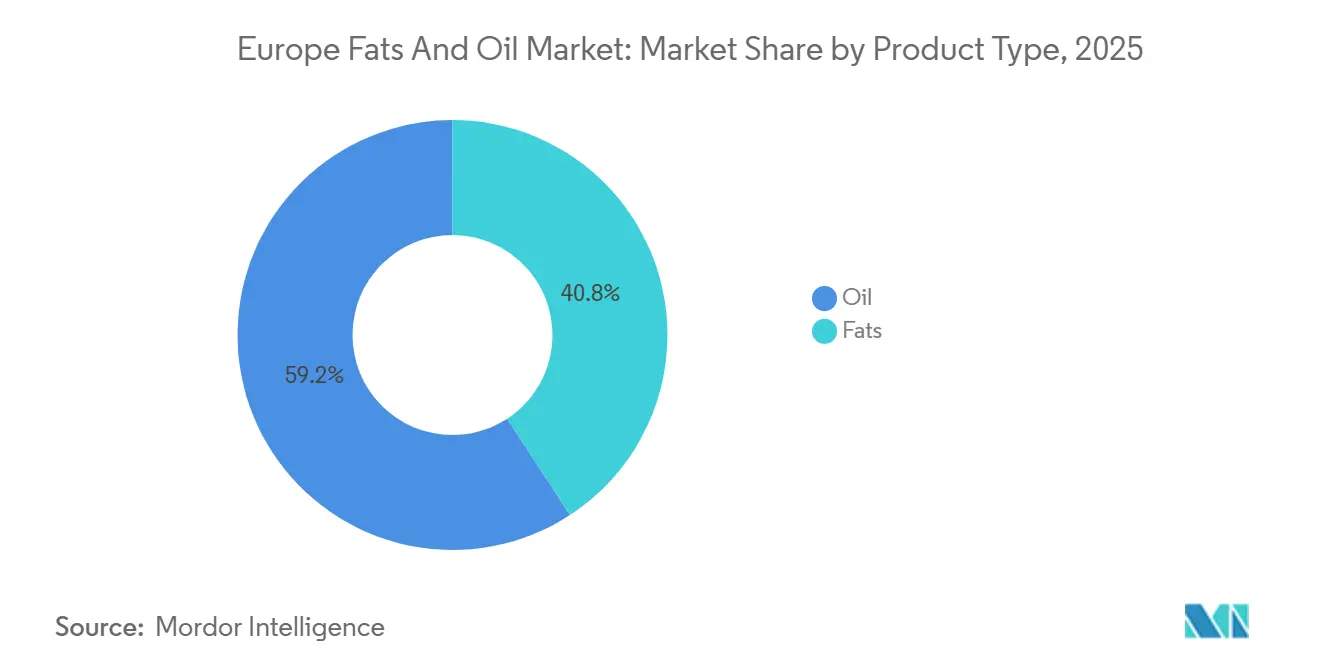

- By product type, oils led with 59.21% of the Europe Fats and Oils Market share in 2025 and are forecast to expand at a 5.48% CAGR through 2031.

- By application, food held 58.63% of 2025 value, while animal feed is projected to register the fastest 5.32% CAGR over 2026-2031.

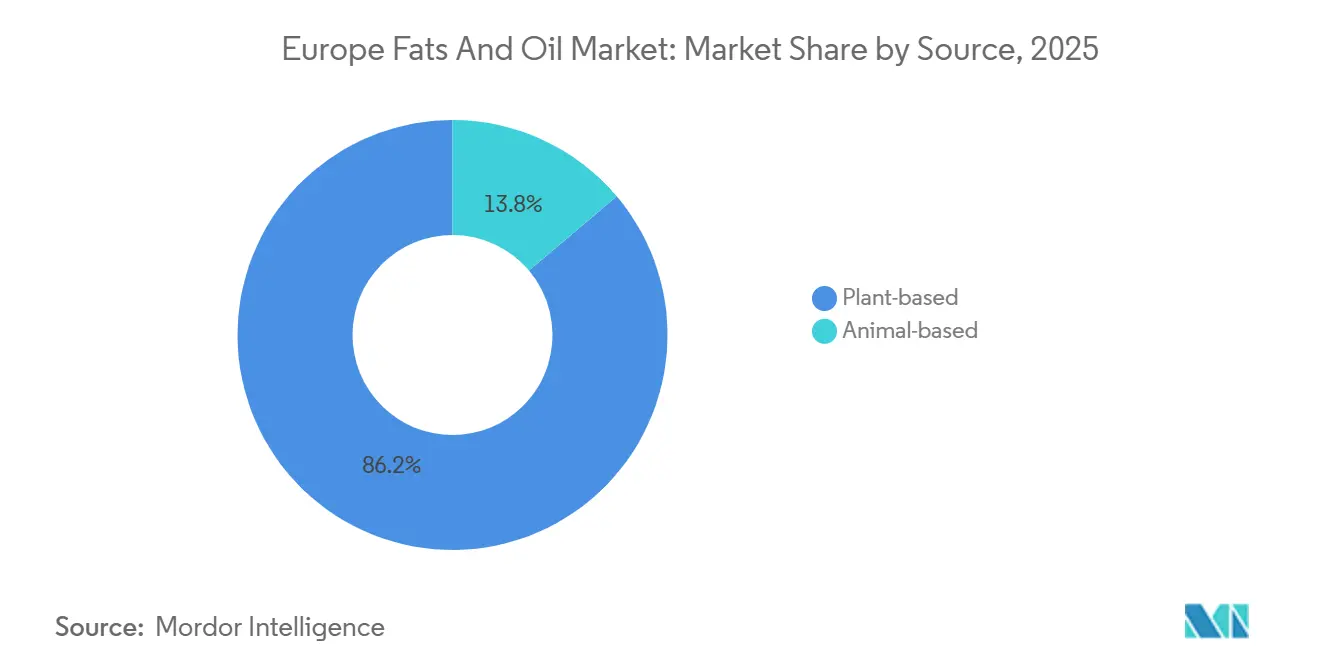

- By source, plant-based inputs captured 86.16% share in 2025; however, animal-based fats are expected to grow at 5.68% CAGR over the forecast period.

- By geography, Italy commanded 14.45% of 2025 revenue, whereas Germany is set to post the strongest 4.71% CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Europe Fats and Oils Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing use of specialty fats in bakery and confectionery applications | +0.6% | Western Europe (Germany, France, Belgium), with spillover to Poland and Czech Republic | Medium term (2-4 years) |

| Progress in fat modification technologies | +0.5% | Early adoption in Netherlands, Germany, and Denmark | Long term (≥ 4 years) |

| Growing preference for clean-label and natural ingredients | +0.7% | North and Western Europe, led by Germany, United Kingdom, and Scandinavia | Short term (≤ 2 years) |

| Rising demand for organic and non-GMO products | +0.4% | Germany, France, Austria, with emerging interest in Spain and Italy | Medium term (2-4 years) |

| Advancements in food processing technologies | +0.3% | Netherlands, Germany, Belgium | Long term (≥ 4 years) |

| Expanding adoption of plant-based diets | +0.8% | United Kingdom, Germany, Netherlands, Scandinavia, with growing momentum in France and Spain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing use of specialty fats in bakery and confectionery applications

European bakery and confectionery manufacturers are increasingly substituting cocoa butter with lauric and non-lauric specialty fats to address input-cost fluctuations and enhance shelf life without refrigeration. Lauric fats, derived from sources such as palm kernel oil and coconut oil, are known for their sharp melting profiles and are commonly used in confectionery coatings. Non-lauric fats, on the other hand, are sourced from oils like soybean and rapeseed and are valued for their stability and neutral flavor. According to Codex Alimentarius standards, specialty fats are permitted in chocolate-flavored coatings as long as they do not exceed 5 percent vegetable fat by weight[1]Source: Food and Agriculture Organization, "STANDARD FOR CHOCOLATE AND CHOCOLATE PRODUCTS - CXS 87-1981", fao.org . This regulation significantly influences product development and labeling strategies across the European Union, as manufacturers must carefully balance compliance with cost efficiency and product quality. The trend is particularly evident in Germany, where discount retailers such as Aldi and Lidl have expanded their private-label praline offerings using specialty fats. These products are priced 30 to 40 percent lower than premium brands, compelling established manufacturers to reformulate their products. The use of specialty fats allows these retailers to maintain competitive pricing while offering products with extended shelf life and consistent quality, further intensifying competition in the market.

Progress in fat modification technologies

Progress in fat modification technologies has driven the adoption of enzymatic interesterification as the preferred method for restructuring triglycerides. This method avoids the production of trans fats and glycidyl esters, addressing health concerns and process-contaminant issues that have limited the use of chemical interesterification and partial hydrogenation. For instance, Novozymes offers Lipozyme TL 100L, a lipase enzyme that enables CO2 reductions of up to 22%, allowing mid-sized refiners to implement enzymatic processes without requiring capital-intensive batch reactors. The advancement of this technology is particularly evident in the Netherlands and Denmark, where co-location with crushing plants facilitates the interesterification of crude oil immediately after degumming. This process not only preserves tocopherols but also reduces oxidative rancidity during storage, showcasing the benefits of modern fat modification techniques.

Growing preference for clean-label and natural ingredients

Clean-label positioning has transitioned from a niche concept to a mainstream trend as European consumers increasingly scrutinize ingredient lists, and retailers enforce reformulation mandates to differentiate their private-label offerings. The growing preference for clean-label and natural ingredients is a significant driver in the Europe Fats and Oils Market. Consumers in Germany, France, and the United Kingdom are willing to pay a 10% to 15% premium for oils and fats labeled as "no artificial additives" or "minimally processed." This shift reflects a broader demand for transparency and healthier options in food products. Manufacturers are also reformulating their product ranges by replacing synthetic emulsifiers with natural and clean ingredients to meet this demand. This clean-label trend is reshaping supply chains, with processors investing in physical refining methods, such as steam stripping instead of chemical neutralization, to eliminate sodium-hydroxide residues and preserve natural antioxidants.

Rising demand for organic and non-GMO products

The increasing preference for organic and non-GMO foods is significantly influencing the Europe fats and oils market, as consumers increasingly link ingredient origin to health and environmental considerations. Buyers in Western and Northern Europe closely scrutinize product labels, favoring oils that are free from synthetic pesticides, genetic modification, and chemical refining. This shift has prompted manufacturers to transition from conventional commodity oils to certified organic options such as sunflower, rapeseed, and olive oils, as well as organic butterfat alternatives used in bakery products, infant nutrition, and premium ready-to-eat foods. In response, brands are reformulating spreads, cooking oils, and dressings to include fewer additives and emphasize transparent sourcing, aligning fats with the clean-eating lifestyle trend. Agricultural developments in the region further support this movement. The share of farmland in the European Union managed under organic practices increased from 5.9% in 2012 to 10.8% in 2023. Under the European Green Deal, authorities aim to expand organic agricultural land to 25% by 2030, indicating sustained institutional backing for organic raw materials[2]Source: European Environment Agency, "Agricultural area under organic farming in Europe", eea.europa.eu. This goal is driving investments in segregated crushing facilities, traceability systems, and identity-preserved logistics for oilseeds.

Restraints Impact Analysis of Europe Fats and Oils Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict European Union labeling and food safety regulations | -0.4% | European Union-wide, with heightened enforcement in Germany, France, and Netherlands | Short term (≤ 2 years) |

| Health concerns related to animal-derived fats | -0.3% | Northern and Western Europe, particularly United Kingdom, Germany, and Scandinavia | Medium term (2-4 years) |

| Sustainability issues associated with palm oil | -0.5% | European Union-wide, with strongest consumer backlash in United Kingdom, Germany, and Netherlands | Short term (≤ 2 years) |

| Allergen risks and nutritional constraints | -0.2% | European Union-wide, with strict enforcement in France (Nutri-Score) and United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict European Union labeling and food safety regulations

Strict European Union labeling and food safety regulations pose challenges to the fats and oils market, as manufacturers must frequently reformulate products, invest in testing, and implement detailed traceability systems to meet compliance requirements across member states. The EU enforces specific compositional limits and disclosure standards for lipids. For instance, Regulation (EU) 2019/649 limits industrially produced trans fats in foods to a maximum of 2 g per 100 g of fat[3]Source: European Union, "Regulation - 2019/649 - EN - EUR-Lex", eur-lex.europa.eu. This compels processors to replace partially hydrogenated oils with alternative fat systems and conduct expensive validation trials. For fats and oils suppliers, these regulatory demands increase compliance costs, including laboratory analysis, certification, label redesign, and segregated logistics for varying formulations. Smaller producers and exporters face significant challenges, as non-compliance, such as contamination, inaccurate nutritional declarations, or improper origin labeling, can disrupt distribution across the entire EU market.

Sustainability issues associated with palm oil

Sustainability concerns regarding palm oil serve as a restraint on the European fats and oils market. While palm oil is widely used for its functional properties, it faces significant environmental scrutiny from regulators, retailers, and consumers. European buyers increasingly link palm oil cultivation to deforestation, biodiversity loss, and greenhouse gas emissions. Consequently, many food manufacturers are reformulating products or transitioning to alternative fats such as sunflower, rapeseed, or shea fractions. Retail chains often mandate certified or deforestation-free sourcing, compelling suppliers to adopt traceability systems, segregated supply chains, and third-party certifications, which substantially increase procurement and operational costs. The challenges associated with sourcing compliance and reputational risks discourage new product development involving palm-derived lipids and create instability in long-term contracts. As a result, sustainability pressures reduce palm oil's flexibility as a formulation ingredient and limit growth opportunities in the European fats and oils market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Europe Fats and Oils Market Segment Analysis

By Product Type:

Oils Capture Innovation and VolumeOils held 59.21% of the Europe Fats and Oils Market in 2025 and are forecast to expand at 5.48% CAGR through 2031. The demand for oils in Europe is driven by consumer preferences for healthier cooking options and Mediterranean-style diets, which prioritize olive, rapeseed, and sunflower oils due to their high content of unsaturated fatty acids. Additionally, clean-label requirements are fostering interest in cold-pressed, organic, and non-GMO oils, while sustainability objectives encourage the use of regionally sourced oilseeds and certified supply chains. The growing popularity of home cooking, increased salad consumption, and premium flavored oils further contribute to this demand. Food manufacturers are also incorporating functional oils enriched with omega fatty acids and vitamins into ready meals, infant nutrition, and dietary supplements. These factors collectively drive innovation toward minimally processed oils with enhanced nutritional profiles.

The fats segment is experiencing growth primarily due to the demand from bakery, confectionery, and plant-based product manufacturers for fats with specific melting behavior, aeration, and texture. Specialty fats, including cocoa butter equivalents, structured vegetable fats, and dairy alternatives, are crucial for applications such as pastries, fillings, chocolate, and vegan cheese or meat substitutes. The ongoing reformulation efforts to eliminate trans fats and optimize saturated fat levels are also driving the adoption of modified fat systems created through fractionation and enzymatic processing. Additionally, the demand for premium indulgent products and functional spreads is increasing the need for customized fat blends that meet sensory quality, regulatory, and nutritional requirements.

By Application:

Food Leads, Animal Feed Posts Fastest GrowthFood applications commanded 58.63% of the Europe Fats and Oils Market in 2025; however, animal feed application is expected to grow at 5.32% from 2026 to 2031. In the food industry, demand is driven by the need for texture, flavor release, and shelf-life stability in products such as bakery items, confectionery, dairy alternatives, and ready meals. Manufacturers utilize customized lipid systems to achieve desired properties like creaminess, aeration, and controlled melting in pastries, chocolate fillings, spreads, and plant-based products. The preference for clean-label products promotes the use of minimally processed oils, while nutritional reformulation encourages the adoption of blends with reduced trans fats and optimized saturated fat content. Additionally, premiumization and the growing popularity of diverse culinary trends, such as Mediterranean and gourmet cooking, are increasing the use of specialty and flavored oils in sauces, dressings, and convenience foods.

Oils and fats in animal nutrition serve as concentrated energy sources and aid in improving feed efficiency and nutrient absorption. Livestock and aquaculture producers utilize vegetable oils and rendered fats to enhance growth performance, improve skin and coat quality, and increase feed palatability. The growing focus on sustainable and precisely formulated feed has led to the inclusion of specific fatty acid profiles in poultry, swine, and fish diets. Furthermore, advancements in compound feed formulation and the demand for stable pelleted feed have driven the use of lipids as binders and dust-control agents, ensuring consistent feed quality and supporting animal productivity.

By Source:

Plant-Based Dominance PersistsPlant-based sources held 86.16% of the Europe Fats and Oils Market in 2025, whereas animal-based fats are expected to grow at a CAGR of 5.68% from 2026 to 2031. The growth of plant-based sources is primarily driven by the increasing adoption of flexitarian and vegan diets, which has led to a higher demand for vegetable lipids in products such as dairy alternatives, meat substitutes, spreads, and ready meals. Food manufacturers rely on plant oils to replicate creaminess, structure, and melting properties without using animal-derived ingredients. Additionally, clean-label preferences and heightened sustainability awareness promote the use of non-hydrogenated, traceable, and regionally sourced oilseeds. Reformulation policies aimed at reducing trans and saturated fats further encourage manufacturers to utilize customized vegetable oil blends. Moreover, advancements in fat structuring technologies enable plant-based lipids to achieve functionality similar to that of butter or lard, accelerating their integration into various applications.

The demand for animal-based fats and oils remains steady due to their natural flavor, texture, and functionality in traditional bakery, confectionery, and culinary applications, where ingredients like butterfat and tallow deliver unique taste and consistency. Artisanal foods, premium pastries, and specialty cheeses depend on dairy fat for authenticity and consumer appeal, ensuring continued usage despite reformulation trends. In foodservice and meat processing, animal fats enhance juiciness, stability, and heat tolerance in cooked products. Additionally, the rendering industry facilitates the circular use of by-products from the meat industry, supplying fats for pet food, animal feed, and certain industrial applications, thereby maintaining consistent demand across various sectors.

Geography Analysis

Italy Fats and Oils Market

Italy led the Europe Fats and Oils Market with a 14.45% share in 2025 driven by country's strong culinary culture, which emphasizes olive oil as a staple ingredient for salads, pasta, and vegetable dishes. Consumers show a preference for extra-virgin and regional varieties with protected origin claims, driving demand for premium and specialty oils. Simultaneously, bakery and confectionery traditions sustain consistent use of butter and specialty fats. Additionally, growing interest in natural and minimally processed ingredients boosts demand for cold-pressed and organic options in both retail and foodservice sectors.

Germany Fats and Oils Market

Germany is projected to grow at a CAGR of 4.71% through 2031. This growth is driven by health-conscious eating habits and a preference for balanced fatty acid profiles, which have increased the use of rapeseed and sunflower oils in home cooking and packaged foods. The significant bakery and confectionery industry contributes to the demand for functional fats, including shortenings and cocoa butter equivalents. Additionally, the growing plant-based food sector requires customized vegetable fat systems for meat and dairy alternatives. Rising sustainability awareness and demand for clear labeling further support the adoption of traceable and certified oil products.

United Kingdom Fats and Oils Market

In the United Kingdom, sales of fats and oil are influenced by convenience-oriented consumption patterns and a robust ready-meal and takeaway culture that heavily depends on frying and cooking oils. Demand for spreads and baking fats remains steady, supported by home baking trends, while the rise in plant-based diets drives increased use of vegetable oils in vegan meals and snacks. Furthermore, growing interest in healthier formulations prompts manufacturers to adopt blended oils and fortified products focused on nutrition and functionality.

Competitive Landscape

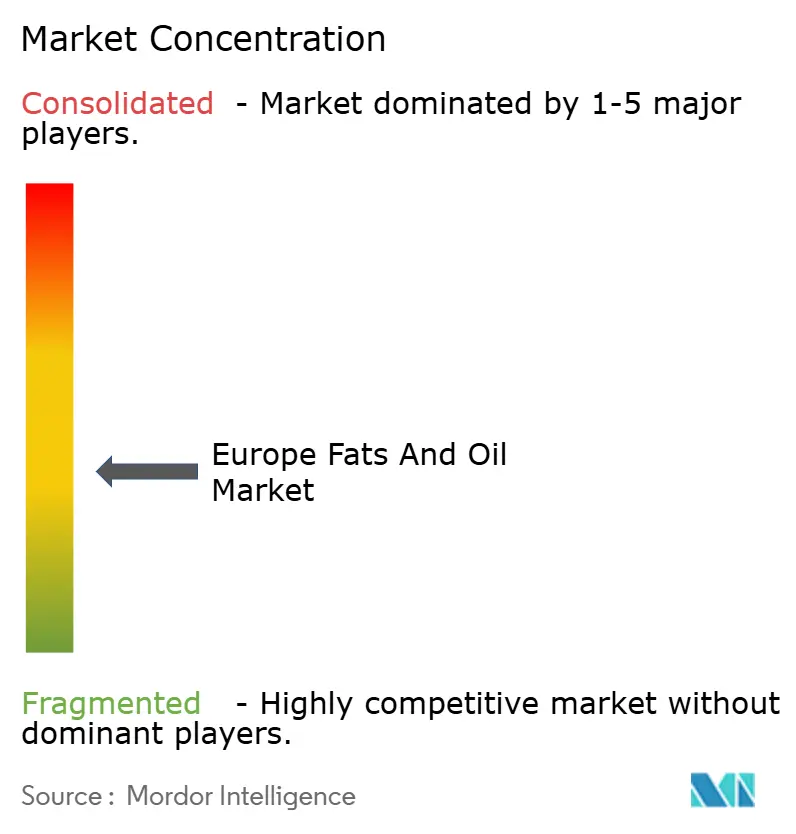

The European fats and oils market is fragmented across crushing, refining, and specialty-fat segments. Global companies dominate primary processing and port infrastructure, while regional players focus on innovation and niche markets. Major players such as Cargill, Bunge, and Archer Daniels Midland lead oilseed crushing operations in the Netherlands, Germany, and France. They utilize economies of scale, integrated logistics, and multi-feedstock flexibility to cater to biodiesel, food, and feed industries effectively.

Strategic approaches focus on vertical integration, sustainability certifications, and technology partnerships. Vertical integration allows companies to control multiple stages of the supply chain, enhancing efficiency and reducing costs. Sustainability certifications ensure compliance with environmental and social standards, which are increasingly demanded by consumers and regulatory bodies. Technology partnerships enable the development of innovative solutions to address industry challenges. Opportunities remain in areas such as carbon-neutral refining, algae-derived omega-3 oils, and traceable smallholder palm, where early adopters can establish long-term contracts with brands aiming to reduce Scope 3 emissions.

Carbon-neutral refining focuses on reducing greenhouse gas emissions during the production process, while algae-derived omega-3 oils offer a sustainable alternative to fish-based sources. Traceable smallholder palm ensures transparency and accountability in sourcing, addressing concerns about deforestation and labor practices. Collaborations between enzyme suppliers and fat modifiers are advancing, as companies work to eliminate trans fats and minimize process contaminants without relying on capital-intensive batch reactors. These partnerships are critical for developing cost-effective and scalable solutions to meet regulatory and consumer demands for healthier and safer products.

Europe Fats and Oils Industry Leaders

-

Cargill, Incorporated

-

Bunge Limited

-

Archer Daniels Midland Company

-

Wilmar International Limited

-

Olam International Ltd.

- *Disclaimer: Major Players sorted in no particular order

Europe Fats and Oils Market Companies Covered in this Report

- Cargill, Incorporated

- Bunge Limited

- Archer Daniels Midland Company

- Wilmar International Limited

- Olam International Ltd.

- AAK AB

- Fuji Oil Holdings Inc.

- Louis Dreyfus Company B.V.

- Avril Group (Saipol)

- Associated British Foods plc

- Mewah International Inc.

- Musim Mas Holdings

- Deoleo S.A.

- Aveno NV

- Vandeputte Group

- KTC Edibles Ltd.

- Aigremont NV

- Anglo Eastern Plantations PLC

- SD Guthrie International

- M.P. Evans

Recent Industry Developments in Europe Fats and Oils Market

- June 2024: OMV has launched its co-processing facility at the Schwechat refinery in Austria. The company invested nearly EUR 200 million to enable the conversion of up to 160,000 metric tons of liquid biomass into premium renewable hydrogenated vegetable oil components.

- February 2024: Bioplanete established Europe's first purely organic oil mill, known as Oil Mill Moog. This facility is dedicated to producing the BIO PLANÈTE brand of organic oils, which are crafted to meet high-quality standards and cater to the growing demand for organic products.

- July 2023: Edible Oils Limited (EOL) has completed a major investment initiative at its Erith and Belvedere locations in south-east London. This upgrade includes the installation of four new oil tanks. At the adjacent Belvedere site, EOL has successfully installed and commissioned four new oil tanks, each with a capacity of 60,000 litres, marking a significant boost to the company's tank farm capacity.

Europe Fats and Oils Market Report Scope

Fats and oils are both types of lipids, which are complex molecules that store energy. The key difference lies in their state at room temperature: fats are solid, while oils are liquid. Both are composed of triglycerides, which are esters of glycerol and three fatty acids.

The European Fats and Oil Market is segmented by type into fats, oils, application, source, and country. Based on fats, the market is segmented into butter, tallow, lard, and specialty fats. Based on Oils, the market is segmented into soybean oil, rapeseed oil, palm oil, coconut oil, olive oil, cottonseed oil, sunflower seed oil, and others. Based on application, the market is segmented into food, industrial, and animal feed. Based on the source, the market is segmented into plant-based and animal-based. Based on country, the market is segmented into Germany, the United Kingdom, France, Italy, Russia, and the Rest of Europe. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million). Source: https://www.mordorintelligence.com/industry-reports/north-america-coffee-market

Segmentation Overview

By Product Type

| Fats | Butter |

| Tallow | |

| Lard | |

| Specialty Fats | |

| Oils | Soybean Oil |

| Rapeseed Oil | |

| Palm Oil | |

| Coconut Oil | |

| Olive Oil | |

| Cotton Seed Oil | |

| Sunflower Seed Oil | |

| Others |

By Application

| Food | Confectionery |

| Bakery | |

| Dairy Products | |

| Others | |

| Industrial | |

| Animal Feed |

By Source

| Plant-based |

| Animal-based |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Netherlands |

| Switzerland |

| Belgium |

| Austria |

| Portugal |

| Denmark |

| Rest of Europe |

| By Product Type | Fats | Butter |

| Tallow | ||

| Lard | ||

| Specialty Fats | ||

| Oils | Soybean Oil | |

| Rapeseed Oil | ||

| Palm Oil | ||

| Coconut Oil | ||

| Olive Oil | ||

| Cotton Seed Oil | ||

| Sunflower Seed Oil | ||

| Others | ||

| By Application | Food | Confectionery |

| Bakery | ||

| Dairy Products | ||

| Others | ||

| Industrial | ||

| Animal Feed | ||

| By Source | Plant-based | |

| Animal-based | ||

| By Geography | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Switzerland | ||

| Belgium | ||

| Austria | ||

| Portugal | ||

| Denmark | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe Fats and Oils Market?

The market stands at USD 30.63 billion in 2026 and is forecast to reach USD 35.84 billion by 2031.

Which product type leads the Europe Fats and Oils Market?

Oils dominate with 59.21% revenue share in 2025 and show the fastest 5.48% CAGR through 2031.

What is driving the fastest growth segment?

Animal feed usage is rising at 5.32% CAGR as crushers monetize protein-meal co-products and producers seek energy-dense rations.

Which country will grow the quickest to 2031?

Germany leads with a 4.71% CAGR, driven by biodiesel capacity additions and clean-label bakery reformulations.

Page last updated on: