Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

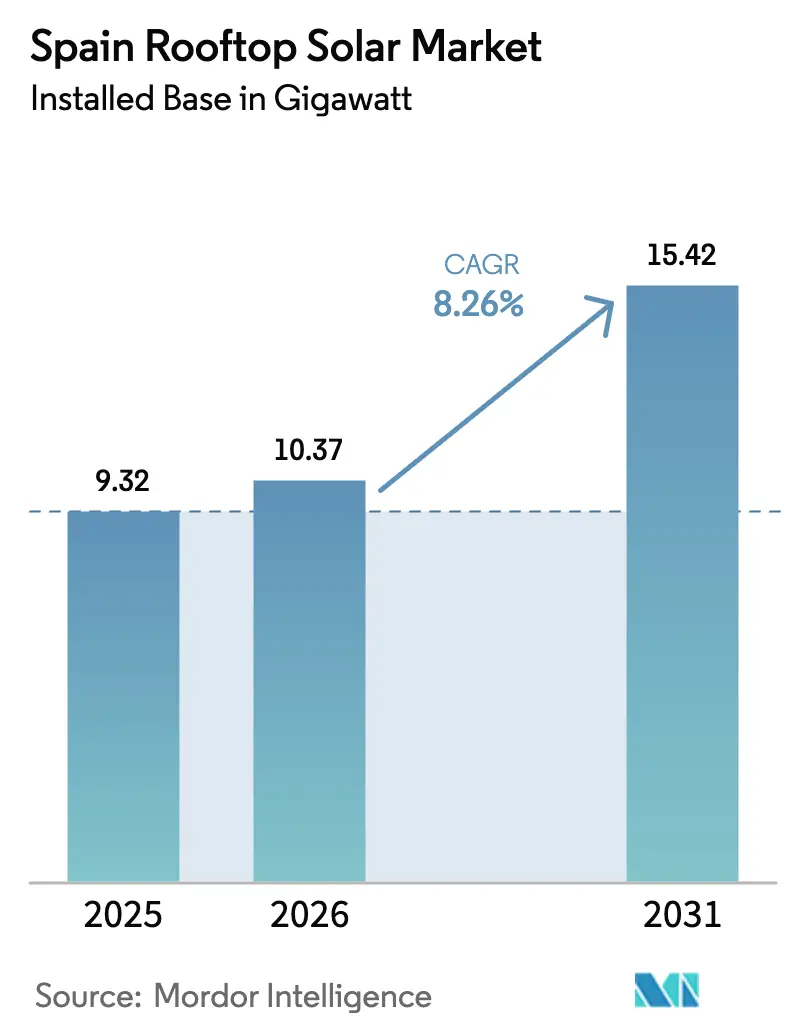

| Base Year Market Size (2025) | 9.32 gigawatt |

| Market Volume (2026) | 10.37 gigawatt |

| Market Volume (2031) | 15.42 gigawatt |

| Growth Rate (2026 - 2031) | 8.26% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Rooftop Solar Market Analysis by Mordor Intelligence

The Spain Rooftop Solar Market size in terms of installed base is projected to be 9.32 gigawatt in 2025, 10.37 gigawatt in 2026, and reach 15.42 gigawatt by 2031, growing at a CAGR of 8.26% from 2026 to 2031.

Industrial and commercial facilities drive this momentum as corporate buyers lock in self-generated power to curb exposure to wholesale-price swings and to satisfy Scope 2 decarbonization targets. Falling module prices, streamlined net-metering rules, and fresh European Green Deal grants have shifted rooftop photovoltaics from a climate gesture to a boardroom strategy. Spain’s 2024 milestone, solar becoming the country’s single-largest power source at 32,043 MW, validates the maturity and resilience of the Spain solar rooftop market. Yet grid-access bottlenecks, municipal red tape, and structural constraints on aging roofs temper the otherwise upbeat trajectory for stakeholders across the Spain solar rooftop market.

Key Report Takeaways

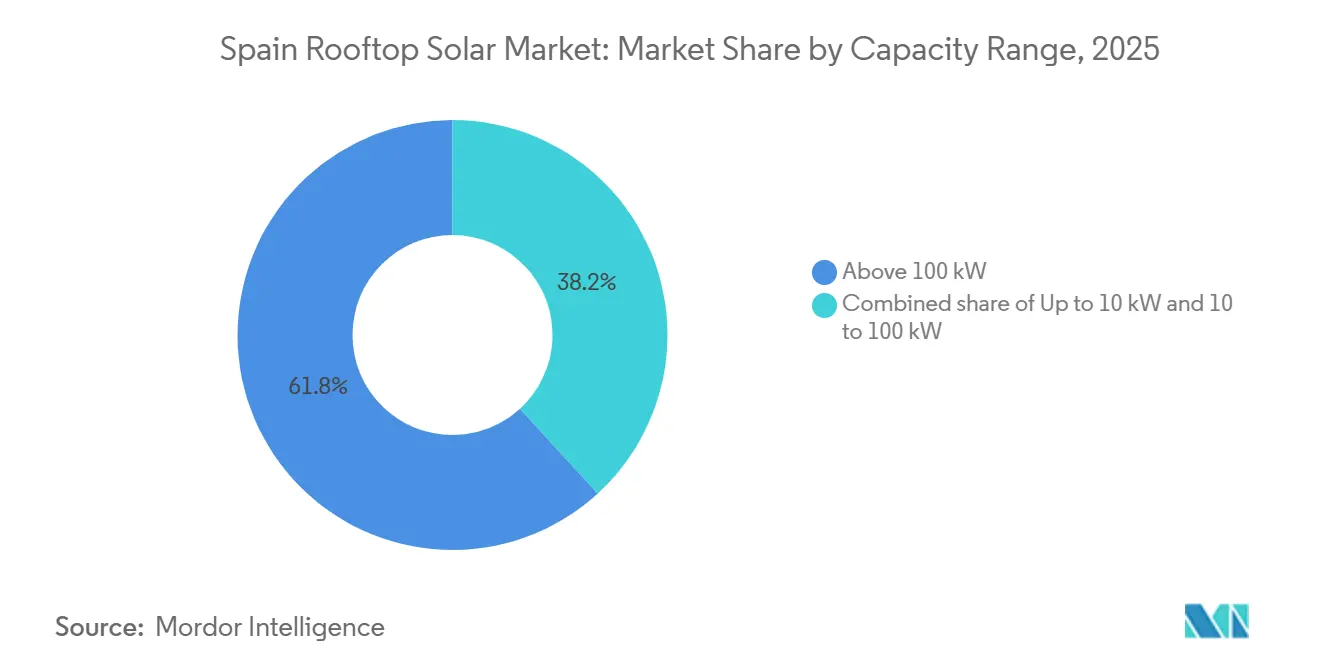

- By capacity range, installations above 100 kW captured 61.8% of Spain's solar rooftop market share in 2025 and are forecast to rise at an 11.1% CAGR through 2031.

- By installation type, retrofit systems commanded 83.5% of the Spanish solar rooftop market size in 2025, while new-build integration is tracking a 10.2% CAGR over the same horizon.

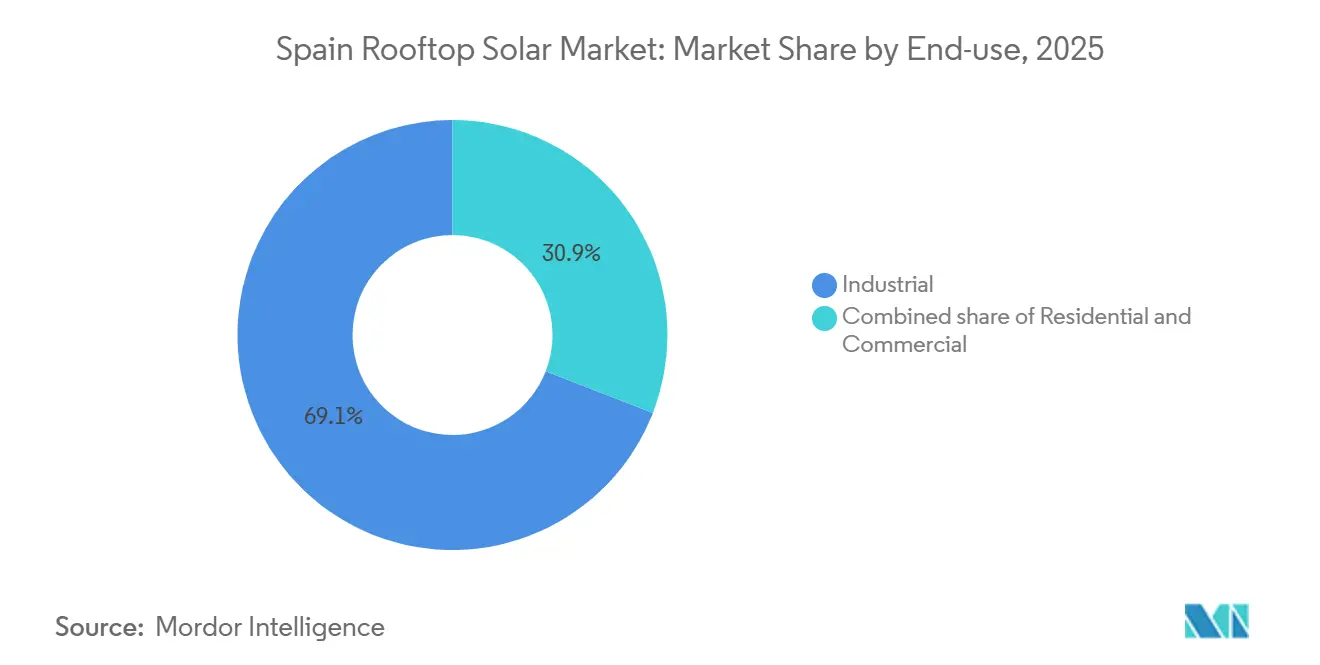

- By end-use, industrial sites accounted for 69.1% of cumulative capacity in 2025 and are projected to expand at a 10.4% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain Rooftop Solar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Net-metering expansion & surplus compensation scheme | +2.1% | National, with early gains in Catalonia, Madrid, Andalusia | Medium term (2-4 years) |

| Declining module & BOS costs | +1.8% | Global impact, amplified in price-sensitive Spanish regions | Short term (≤ 2 years) |

| Corporate sustainability & PPAs proliferation | +1.5% | National, concentrated in industrial hubs like Basque Country, Valencia | Medium term (2-4 years) |

| EU Green Deal funds allocation | +1.2% | National, with priority regions receiving enhanced support | Long term (≥ 4 years) |

| Grid-interactive smart-inverter mandate | +0.9% | National rollout, starting with major metropolitan areas | Medium term (2-4 years) |

| Rising self-consumption cooperatives | +0.7% | Regional clusters in Catalonia, Valencia, Balearic Islands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Net-metering expansion & surplus compensation scheme

Royal Decree 244/2019 eliminated the “sun tax,” allowing prosumers to credit excess power at retail rates, a windfall for multi-megawatt industrial arrays that routinely over-generate on weekends. The law also green-lights collective self-consumption within 2,000 m, enabling factory clusters to pool rooftops and share one grid interconnection. Industrial taxpayers turbo-charge returns through accelerated depreciation, lifting internal rates of return even before energy savings kick in.[1]Endesa, “IRPF Deduction for Solar Panels 2025,” endesa.com These mechanisms helped self-consumption capacity overtake nuclear in 2023, with 7,154 MW online versus 7,117 MW for reactors, most of it sitting on factory roofs.

Declining module & BOS costs

Panel prices slid 17% in 2023, and large orders for 600-W modules now clear customs for as little as USD 0.17/W. Commercial-grade inverters and aluminum racking fell in tandem, pulling the levelized cost of industrial rooftop electricity down to USD 0.044/kWh, on par with ground-mount projects.[2]International Renewable Energy Agency, “Solar PV Cost Reduction 2024,” irena.org Spain’s inverter plants, rated at 82.1 GW per year, shield supply chains from freight shocks and let EPC firms lock in fixed-price contracts despite global volatility. A EUR 750 million (USD 825 million) manufacturing grant further anchors component sourcing at home.

Corporate sustainability & PPAs proliferation

Iberdrola signed more than 900 MW of PPAs in 2023 alone, many tagged specifically to on-roof arrays for multinational tenants that aim to decarbonize without occupying land. Tesla’s 57 MW deal with Zelestra and Apple’s 134 MWp contract with ib vogt epitomize how corporate heavyweights favor Spain solar rooftop market projects that marry brand optics with clean-energy procurement.[3]PV Tech, “Plenitude Starts Operations of 330 MW,” pv-tech.org As the EU’s Corporate Sustainability Reporting Directive takes hold, industrial buyers are expected to double on-site solar adoption by 2027.

EU Green Deal funds allocation

Spain’s Recovery Plan steers EUR 931 million (USD 1.02 billion) into grid upgrades that eliminate capacity claws for factory-scale rooftops, while a separate EUR 700 million storage aid scheme smooths variable output. Former coal regions earn bonus points for shovel-ready solar factories, redirecting skilled miners into module assembly lines and inverter testing floors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy municipal permitting cycles | -0.8% | National, most severe in major cities and heritage-rich regions | Short term (≤ 2 years) |

| Rooftop structural load limitations in pre-2000 buildings | -0.6% | Urban centers with older building stock, particularly Madrid, Barcelona | Medium term (2-4 years) |

| Scarce skilled rooftop-installer workforce | -0.5% | National, acute in rural and island regions | Medium term (2-4 years) |

| Anti-glare & aesthetic restrictions in heritage zones | -0.3% | Historic city centers, UNESCO sites, protected cultural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid-interactive smart-inverter mandate

Town-hall approval for a 2 MW Barcelona retrofit can exceed 14 months, as planners juggle fire-safety reports, structural affidavits, and visual-impact statements. Brussels warned Spain that such delays jeopardize REPowerEU milestones. Girona’s seven-year saga to clear a mid-scale plant frightened risk-averse industrial CFOs, adding soft costs equal to 6% of total project spend.

Scarce skilled rooftop-installer workforce

Solar payrolls rose 59 % in 2024, yet chronic shortages persist for high-voltage electricians and licensed structural engineers. Industrial jobs, unlike residential installs, demand experience with 800 V strings, arc-flash mitigation, and thermal-imaging diagnostics, a skill set rare outside metros.[4]El Español, “Empresas Buscan Profesionales Cualificados,” elespanol.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity Range: Above 100 kW Systems Power Ahead

Spain's solar rooftop market size for arrays above 100 kW reached 5.76 GW in 2025, equal to 61.8% of total installed capacity. Within this cohort, multi-megawatt industrial roofs are logging 11.1% CAGR on the back of bulk component pricing and single interconnection fees that dilute per-kilowatt soft costs. The Spain solar rooftop market size for 10–100 kW projects stood at 2.41 GW, addressing warehouses and supermarkets that value net-metering without three-year grid studies.

Economies of scale slash installed outlays to EUR 0.68/W for 5-MW rooftops, 34% below residential benchmarks. Overdimensioning modules to inverter ratings boosts yield without extra BOS hardware. Meanwhile, under-10 kW systems lose share as subsidy caps shrink, though they remain vital in suburban feed-in clusters. Continual smart-inverter firmware updates let >100 kW systems offer voltage ride-through and synthetic inertia, turning factory roofs into microgrids that double as grid assets during contingency events.

By Installation Type: Retrofit Dominates but New-build Gathers Pace

Retrofit projects occupied 83.5% of Spain's solar rooftop market share in 2025, leveraging an enormous base of 210 million m² of existing industrial roofs. Fast-track audits identify steel-truss halls capable of hosting 4–7 kg/m² additional load, ideal for portrait-tilt configurations. Spain's solar rooftop market size for new-build integration totaled 1.54 GW, yet is climbing on the back of stricter Technical Building Code mandates requiring renewable electricity coverage.

Retrofits appeal to CFOs because performance can be benchmarked against historical load curves, letting them peg PPAs to 90 % self-consumption ratios. Nonetheless, developers increasingly influence architects pre-permit, embedding cable trays and south-facing parapets that cut future retro-work by 15 %. Building-integrated photovoltaics now appear on chilled-storage facades, marrying insulation with energy yield in one envelope layer. New-build adoption accelerates as rating agencies factor embodied carbon into lending spreads, nudging logisticians to solar-ready roof decks from day one.

By End-use: Industrial Hegemony

Industrial sites held 69.1% of cumulative capacity in 2025, more than double commercial allocations and dwarfing residential uptake. Cement plants, bottling lines, and vehicle-assembly halls each surpassed 10 MW rooftop arrays last year, turning their net-site emissions trajectories decisively downward. Spain's solar rooftop market share for industrial users is projected to grow at another 10.4% CAGR, reaching nearly 12 GW by 2031.

Commercial estates such as outlet malls and airport terminals prioritize 91 kW average system sizes that match daytime HVAC loads. They unlock 5-year paybacks through accelerated depreciation and self-consumption offsets. Residential adoption plateaus as power tariffs ease, yet battery-plus-solar bundles sustain niche growth among eco-centric homeowners. Industrial first movers deploy energy-management software that orchestrates solar generation, chill-water storage, and EV truck chargers, demonstrating the integrative frontier of the Spain solar rooftop industry.

Geography Analysis

Extremadura, Castile-La Mancha, and Andalusia collectively host 70 % of national rooftop wattage thanks to 1,800 kWh/m² insolation, vast logistics footprints, and extra-fast permitting windows. Extremadura’s regional decree waives municipal fees for systems above 100 kW installed on pre-registered industrial zones, compressing paperwork to 60 days. Castile-La Mancha piggybacks battery grants onto solar subsidies, pushing many wineries to adopt 2 h storage buffers.

Catalonia and Valencia accelerate via industrial cooperatives that share high-capacity feeders and leverage local steel fabrication for racking kits. Madrid’s 7,139 ha of untapped roofs could produce 32,163 GWh annually, enough to cover four-fifths of 2050 demand if grid-tie upgrades keep pace. Islands face diesel-priced tariffs above EUR 0.25/kWh; hence, the Balearics have earmarked EUR 700 million (USD 770 million) to subsidize behind-the-meter arrays, boosting self-consumption to 35% of peak-day load.

Former coal regions in Asturias and León realign workforces from shuttered mines to inverter QA labs, supported by NextGenerationEU reskilling funds. Grid planners schedule 110/30 kV substation upgrades adjacent to industrial parks, ensuring volt-variance stays within ±5 % even after 500 MW of new rooftop capacity fires up by 2028.

Competitive Landscape

Iberdrola tops Spain solar rooftop market rankings with 5,055 MW across 43 plants, including Europe’s 550 MW Núñez de Balboa hybrid that combines land-adjacent trackers with brewery-roof arrays. Endesa eyes a 49.99 % asset divestiture to recycle capital, yet will retain O&M contracts, preserving annuity streams. Zelestra scales fastest, ballooning its pipeline from 7 GW in 2021 to 19 GW in 2025, a third of which sits on industrial roofs.

Market fragmentation persists among EPCs; fewer than 25 % of Spain’s 4,100 licensed installers handle arrays above 500 kW. Selectra’s 2025 client survey ranked Avenir Energía (9.2/10) and Samara (8.7/10) best for industrial change-management support. Foreign OEMs, SunPower, and SMA deploy performance-guarantee packages that offset bankability concerns for financiers underwriting 15-year PPAs. Joint ventures proliferate: racking maker Gonvarri pairs with Ferrovial to bundle steel supply and EPC, shaving 5 % off turnkey quotes.

M&A heats up as asset managers chase stable euro-denominated cash flows, with BayWa r.e.’s 60 MWp portfolio sale to KGAL and Ib Vogt’s 110 MW hand-off to NextEnergy Capital closing in July 2025. Expect installer roll-ups as private-equity firms arbitrage fragmented service territories.

Spain Rooftop Solar Industry Leaders

X-ELIO Energy

Repsol SA

Acciona SA

Endesa SA

Iberdrola SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: In a groundbreaking move for Spain's industrial sector, Stellantis Group's Vigo plant, in partnership with Prosolia Energy, has unveiled the country's largest rooftop solar facility dedicated to self-consumption. Spanning 170,000 square meters and equipped with 33,000 solar panels, the plant boasts an impressive installed capacity of 18.3 megawatts peak (MWp), translating to an annual generation of 22.7 gigawatt hours (GWh). This output will satisfy 15% of the plant's electricity demands, leading to a significant reduction of over 9,000 tons of CO2 emissions annually.

- March 2025: Alstom has successfully installed over 3,500 solar panels at its industrial site in Barcelona. The solar energy initiative boasts an installed peak power of 2,041 kWp, generating energy that meets 26.5% of the factory's consumption. The recently inaugurated first phase saw the installation of 2,419 solar panels atop workshops, office buildings, and even the parking area, with specific parking spaces ingeniously covered to house the solar panels. The second phase, wrapped up by the end of June 2025, has seen the addition of solar panels in a secondary parking area, which is in the process of being outfitted with a roof.

- March 2025: The Institute for Diversification and Energy Saving (IDAE), responsible for the RENOVAL programme, unveiled provisional results. The Spanish Ministry of Ecological Transition (MITECO) has allocated over EUR 210 million (USD 227.21 million) to seven solar PV manufacturing initiatives. These funds, part of Spain’s recovery and resilience plan (PRTR) under NextGenEU, are designed to boost the production of solar panel components, batteries, electrolysers, and other technologies.

- June 2024: FutureVoltaics, a spinoff of the Spanish National Research Council (CSIC), has unveiled its pre-assembled vertical PV system tailored for rooftops. Dubbed the Vechtor system, it boasts an easy installation process: just unfold it. The system features both polished and rough metal specular reflectors, artfully arranged in a unique pattern on either side of its bifacial solar panels.

Spain Rooftop Solar Market Report Scope

The Spain Rooftop Solar market report includes:

By Capacity Range

| Up to 10 kW |

| 10 to 100 kW |

| Above 100 kW |

By Installation Type

| New-build |

| Retrofit |

By End-use

| Residential |

| Commercial |

| Industrial |

| By Capacity Range | Up to 10 kW |

| 10 to 100 kW | |

| Above 100 kW | |

| By Installation Type | New-build |

| Retrofit | |

| By End-use | Residential |

| Commercial | |

| Industrial |

Key Questions Answered in the Report

How big will Spain’s rooftop PV fleet be by 2031?

Installed capacity is projected at 15.42 GW, up from 10.37 GW in 2026.

Why do installations above 100 kW dominate capacity?

Large roofs deliver 30–40 % lower per-kW costs and qualify for streamlined PPAs, so they captured 61.8% of 2025 capacity.

Which incentive cuts payback the most for factories?

Net-metering paired with accelerated depreciation can trim industrial rooftop payback to under 5 years.

What is the main bottleneck for new industrial arrays?

Municipal permitting delays add up to 14 months in some cities, eroding IRR by roughly 1 percentage point.

Are storage systems common on rooftops?

Batteries accompany 26 % of new residential arrays and a growing share of mega-roof projects as grid-service revenues improve.

Page last updated on: