Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

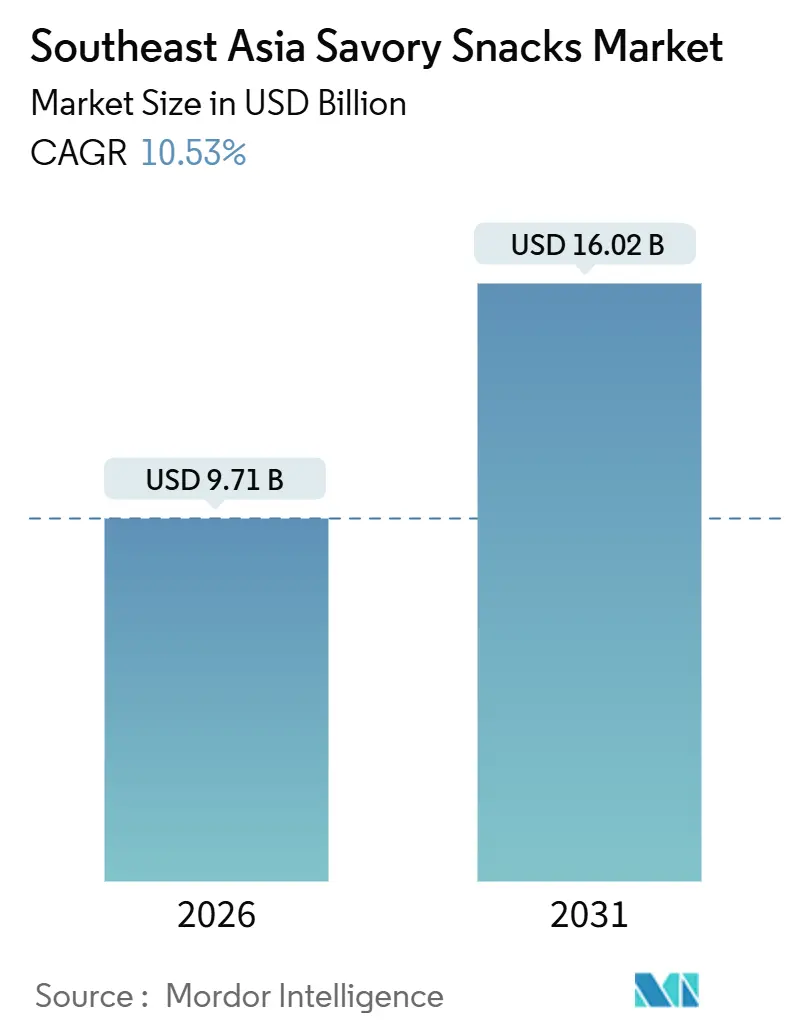

| Market Size (2026) | USD 9.71 Billion |

| Market Size (2031) | USD 16.02 Billion |

| Growth Rate (2026 - 2031) | 10.53% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Southeast Asia Savory Snacks Market Analysis by Mordor Intelligence

The Southeast Asia savory snacks market stands at USD 9.71 billion in 2026 and is projected to expand to USD 16.02 billion by 2031, registering a 10.53% CAGR. Strong population growth, rapid urbanization, and rising disposable incomes are accelerating the adoption of convenient snacks as meal replacements, especially among time-pressed city dwellers. Ongoing “snackification” is spawning an array of premium, functional, and flavor-forward innovations that appeal to Gen Z and millennials, while competitive pricing keeps core volumes resilient among value-oriented households. Digital commerce is opening low-barrier routes to consumers in dense urban corridors, giving digital-native brands and multinationals equal opportunity to capture incremental occasions. At the same time, manufacturers are confronting price pressures from volatile palm-oil and potato costs and preparing for stricter sodium- and sugar-reduction rules that are gathering momentum across the region.

Key Report Takeaways

- By product type, chips and crisp-based snacks led with 38.13% of the Southeast Asia savory snacks market share in 2025, while fruit and vegetable snacks are forecast to post a 12.50% CAGR through 2031.

- By flavor profile, classic/salted led with 52.07% of the Southeast Asia savory snacks market share in 2025, while flavored are forecast to post a 10.81% CAGR through 2031.

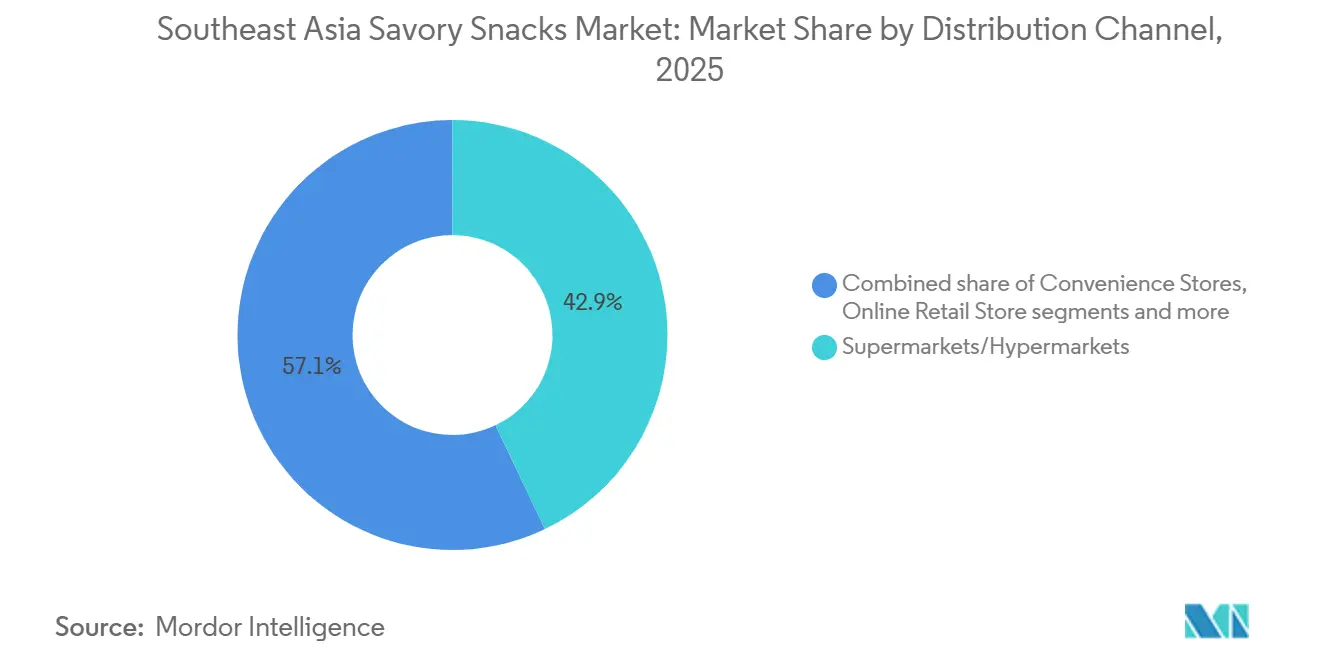

- By distribution channel, supermarkets/hypermarkets commanded 42.94% of the Southeast Asia savory snacks market size in 2025; online retail is projected to rise at an 11.45% CAGR between 2026 and 2031.

- By geography, Indonesia retained 34.11% revenue share of the Southeast Asia savory snacks market in 2025; Vietnam is projected to be the fastest-growing country at 14.32% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Southeast Asia Savory Snacks Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanisation and growth of modern retail in Indonesia, Vietnam and Philippines | +2.6% | Indonesia, Vietnam, Philippines | Medium term (2-4 years) |

| Health-oriented reformulation (reduced sodium/oil) led by Thailand and Singapore | +2.1% | Thailand, Singapore, with spillover to Malaysia | Medium term (2-4 years) |

| Local-cuisine flavour innovation (sambal, tom-yum, durian) engaging Gen-Z | +1.6% | Thailand, Indonesia, Malaysia, Singapore | Short term (≤ 2 years) |

| Domestic extruder capacity expansions lowering price points in Indonesia and Vietnam | +1.9% | Indonesia, Vietnam | Medium term (2-4 years) |

| E-commerce and quick-commerce fulfilment boosting urban snack demand | +2.3% | Singapore, Thailand, Malaysia, Philippines | Short term (≤ 2 years) |

| Tourism rebound lifting on-the-go sales in Thailand and Malaysia | +1.3% | Thailand, Malaysia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid urbanisation and growth of modern retail in Indonesia, Vietnam and Philippines

The rapid urbanization in Southeast Asia, particularly in Indonesia, Vietnam, and the Philippines, is significantly driving the growth of the savory snacks market in the region. Urbanization rates reported by the World Bank stand at 58.57% for Indonesia, 39.48% for Vietnam, and 48.28% for the Philippines [1]Source: World Bank, “Urban population (% of total population)”, data.worldbank.org. This demographic shift toward urban living has led to a growing preference for convenient, ready-to-eat snack options among consumers. Additionally, modern retail formats like supermarkets and hypermarkets have made products more accessible, catering to the changing preferences of urban consumers. Additionally, the rapid growth of retail infrastructure in the region, including a steady increase in convenience stores, is driving market growth. For instance, in Indonesia, the number of convenience stores grew from 39,714 in 2021 to 46,118 in 2023. These developments are fueling the expansion of the savory snacks market in Southeast Asia, as urban consumers increasingly prefer a wider variety of snacks that are easy to find.

Health-oriented reformulation (reduced sodium/oil) led by Thailand and Singapore

Thailand and Singapore are taking the lead in making savory snacks healthier in the Southeast Asia market by lowering sodium and oil levels. These efforts support government health initiatives like Thailand's "Healthier Choice" logo program and Singapore's "Healthier Choice Symbol" campaign, which motivate manufacturers to offer healthier snack options. The Health Promotion Board (HPB) in Singapore reports that snacks with the "Healthier Choice Symbol" are gaining popularity among consumers, driving market growth. Similarly, Thailand's Ministry of Public Health has actively promoted sodium reduction strategies, aiming to reduce sodium consumption by 30% by 2025 [2]Source: Department of Disease Control, "Government launches bid to cut people's salt intake by 30%", bangkokpost.com . These government-backed efforts are significantly influencing product innovation and reformulation trends in the region.

Local-cuisine flavor innovation (sambal, tom-yum, durian) engaging Gen-Z

Traditional flavors like sambal, tom-yum, and durian are becoming more popular, boosting the growth of the savory snacks market in Southeast Asia. These flavors are especially popular among Gen-Z consumers, who are eager to try unique and authentic tastes. Southeast Asian governments are also supporting the promotion of their local food heritage. For instance, Malaysia's Ministry of Tourism, Arts, and Culture is promoting sambal as a signature Malaysian flavor globally. Likewise, Thailand's Department of International Trade Promotion is highlighting tom-yum as an important export product with strong global potential. These initiatives, along with Gen-Z's growing interest in adventurous flavors, are creating excellent opportunities for manufacturers to introduce savory snacks inspired by local tastes to meet this rising demand.

Tourism rebound lifting on-the-go sales in Thailand and Malaysia

The resurgence of tourism in Thailand and Malaysia is significantly driving the growth of on-the-go sales, particularly in the savory snacks market. According to the Tourism Authority of Thailand (TAT), the country welcomed over 35 million international tourists in 2024 [3]Source: Ministry of Tourism and Sports Thailand, "Kingdom of Thailand welcomed 35m in 2024", bangkokpost.com , a substantial recovery from the pandemic-induced slump. In 2023, Malaysia welcomed approximately 16.1 million tourists, as reported by the Ministry of Tourism, Arts, and Culture Malaysia (MOTAC). This rise in tourist numbers has increased the demand for easy-to-carry and ready-to-eat food options like savory snacks, which are convenient for travelers. Government campaigns, such as Thailand's "Visit Thailand Year 2023: Amazing New Chapters" and Malaysia's "Malaysia Truly Asia," have also helped revive tourism. These initiatives have attracted both international and local travelers, leading to higher sales of on-the-go snack products.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile palm-oil and potato prices from climate shocks across SEA | -1.6% | Indonesia, Malaysia, Thailand, Vietnam | Medium term (2-4 years) |

| Halal-certification lead-times slowing launches in Indonesia and Malaysia | -1.3% | Indonesia, Malaysia | Short term (≤ 2 years) |

| Salt-/sugar-tax proposals in Singapore and Philippines pressuring margins | -1.0% | Singapore, Philippines, with potential expansion to Thailand | Medium term (2-4 years) |

| Fragmented rural distribution networks limiting reach beyond Tier-2 towns | -1.9% | Indonesia, Philippines, Vietnam, Myanmar | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile palm-oil and potato prices from climate shocks across SEA

Climate changes in Southeast Asia have caused unstable prices for palm oil and potatoes, which are essential raw materials for making savory snacks. These price changes are a major challenge for the Southeast Asia Savory Snacks Market because they directly increase production costs and reduce profit margins for manufacturers. Extreme weather events like floods, droughts, and high temperatures make raw material prices unpredictable, making it harder to keep pricing and supply chains steady. Higher costs for these key ingredients may force manufacturers to either bear the extra expenses or raise prices for consumers, which could lower demand. This instability not only disrupts production but also makes long-term planning and investments difficult, slowing down the market's growth in the region.

Halal-certification lead-times slowing launches in Indonesia and Malaysia

In Southeast Asia's savory snacks market, Indonesia and Malaysia grapple with delayed product launches, primarily due to prolonged halal certification lead times. These delays not only disrupt product rollouts but also hinder market entry strategies, pushing back revenue generation for companies eyeing these markets. Given that halal certification is mandatory for food products in these predominantly Muslim nations, its significance in shaping market dynamics cannot be overstated. The certification process, laden with stringent regulatory checks and extensive documentation, adds to the delays. Companies find themselves dedicating extra resources and time to meet these requirements, inflating operational costs and slowing their response to shifting consumer preferences. Consequently, these extended halal certification lead times create a supply chain bottleneck, stunting the growth potential of Southeast Asia's savory snacks market.

Segment Analysis

By Product Type: Fruit Snacks disrupting traditional categories

In 2025, chips and crisp-based snacks held a significant 38.13% share of the market. This strong position is due to consumers' long-standing preference for these snacks and the wide distribution networks that make them easily available. These snacks are a popular choice because they are convenient and familiar. Additionally, companies regularly launch new flavors and innovative products, which keep chips and crisp-based snacks appealing and help them maintain their leading position in the competitive snack market.

Meanwhile, fruit and vegetable snacks are becoming a fast-growing segment in the Southeast Asian savory snacks market. These snacks are expected to grow at a high CAGR of 12.50% during the forecast period, surpassing the overall market growth. This growth shows that consumers are shifting toward healthier and more nutritious snack options. The change is driven by increasing health awareness and a preference for natural ingredients. The popularity of plant-based diets and the availability of premium, organic snacks are also boosting this segment. The rapid growth of fruit and vegetable snacks highlights their potential to change market trends and create opportunities for new products and expansion in the future.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Flavor Type: Classic/Salted Dominates, Flavored Accelerates

In 2025, classic and salted flavors were the most popular in Southeast Asia's savory snacks market, holding 52.07% of the market share. This shows that consumers in the region prefer traditional and familiar tastes. These snacks are popular because they are easy to find, affordable, and enjoyed by people of all ages. Manufacturers are also improving the quality and packaging of these products to stay competitive. Classic and salted snacks are versatile, often paired with drinks or served during social gatherings, which further increases their demand.

Flavored snacks are expected to grow at a CAGR of 10.81% through 2031, driven by the rising demand for new and exciting flavors. The growing popularity of Western and fusion flavors, along with the trend of premium snack options, is driving this growth. Companies are working on creating unique flavor combinations and healthier alternatives to meet the needs of health-conscious consumers. Additionally, the growth of e-commerce and organized retail is making flavored snacks more accessible and visible across Southeast Asia.

By Distribution Channel: Digital transformation reshaping access

In 2025, supermarkets and hypermarkets held a 42.94% share of Southeast Asia's savory snack market. This success was driven by strategies such as combining sales channels, using loyalty-card data, and placing attractive displays at the end of aisles. These stores offer a wide range of snack products in one location, meeting different customer preferences and making shopping more convenient. Their strong presence shows they are a key distribution channel for snack manufacturers targeting a broad audience. Additionally, in-store promotions and partnerships with snack brands have made supermarkets and hypermarkets more appealing, making them a top choice for both shoppers and suppliers.

Online retail is expected to grow at an 11.45% CAGR, far outpacing traditional physical stores. This growth is fueled by more people using the internet, the rising popularity of e-commerce platforms, and the convenience of home delivery. Online retailers are also attracting customers by offering personalized marketing and competitive prices. The rapid growth of online retail highlights its increasing role in distributing savory snacks in Southeast Asia. Furthermore, the use of digital payment systems and AI-based recommendations on e-commerce platforms is improving the shopping experience, driving even more growth in this channel.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

In 2025, Indonesia holds a leading 34.11% share of the Southeast Asian savory snacks market. This dominance is driven by its large population of over 270 million and a fast-growing middle class. The country's vast consumer base helps manufacturers scale their operations and lower costs through economies of scale. Expanding domestic extruder capacities has further reduced production costs, enabling manufacturers to offer affordable prices that attract consumers across different income levels. The growing demand for convenient, packaged snacks has boosted market reach in both cities and rural areas. Additionally, Indonesia benefits from strong distribution networks and the presence of both local and global companies, solidifying its top position in the region.

Vietnam is becoming the fastest-growing market in the region, with a projected CAGR of 14.32% from 2026 to 2031, surpassing the regional average. This growth is supported by rising disposable incomes, urbanization, and the spread of modern retail beyond major cities like Hanoi and Ho Chi Minh City. The expansion of retail stores into smaller cities has made products more accessible. At the same time, the younger population's changing preferences have increased demand for new and innovative snack options. Government efforts to attract foreign investments in the food and beverage industry have also encouraged new companies to enter the market, increasing competition and driving growth.

Thailand is balancing a mature market with a focus on innovation, especially in health-focused snacks and unique flavors. The country’s well-established snack market benefits from consumers who are highly aware of and interested in premium, health-conscious products. Thai manufacturers are leading the way in creating snacks with less sugar, salt, and fat to meet the growing demand for healthier options. They are also introducing snacks with unique, locally-inspired flavors, which are gaining popularity both in Thailand and in export markets. With a strong supply chain and advanced manufacturing capabilities, Thailand remains a key player in the Southeast Asian savory snacks market.

Competitive Landscape

In the Southeast Asian savory snacks market, competition is balanced, with both multinational companies and local players actively competing. Global companies use their scale, international reach, and innovation to offer premium products that match changing consumer preferences. Meanwhile, local companies rely on their strong distribution networks and deep understanding of regional tastes to maintain their market position. Companies generally follow two main strategies: one focuses on creating premium products with health benefits and unique flavors, while the other ensures affordability and accessibility to reach a broader audience.

Newer companies are changing the market by using digital-first approaches, avoiding traditional distribution challenges, and connecting directly with consumers. These companies use e-commerce and social media to create a unique space for themselves. In response, established players are adopting technology, investing in tools to improve customer engagement through personalized marketing and loyalty programs, while also making their supply chains more efficient. These technological advancements are essential to staying competitive in the fast-changing market.

Competition is also increasing as companies from other industries, like beverage manufacturers, enter the snack market. These companies use their existing distribution networks and strong brand reputation to meet the growing demand for snacks in different situations. By combining snack products with their beverage offerings, they aim to grow their market presence and profits. This entry from other sectors makes the competition tougher, pushing existing snack companies to innovate and adapt to protect their market share.

Southeast Asia Savory Snacks Industry Leaders

-

Mondelēz International

-

PepsiCo Inc.

-

Universal Rubina Corporation

-

Kellanova

-

PT Garudafood Putra Putri Jaya Tbk

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: Indofood CBP introduced Chiki Twist Mixchief, a mystery flavor snack in a playful canister format designed to spark fun and curiosity among consumers.

- October 2024: 7-Eleven Philippines launched canister chips, enhancing its snack selection in the Philippines. Available in Barbecue and Sour Cream & Onion flavors, each canister is priced at PHP 89. This introduction aims to offer consumers affordable, high-quality snacks while reinforcing 7-Eleven’s position in the competitive snack market.

- July 2024: Baken, renowned for its premium bacon snacks, introduced its bacon snacks at Kultura stores across the Philippines. Made from 100% real bacon, these gourmet chips cater to both local and international consumers. This expansion enhances Baken’s market reach, providing Filipinos with a high-quality, uniquely crafted snack through Kultura’s extensive nationwide retail network.

- June 2024: Daesang has invested KRW 30 billion (USD 21.8 million) to expand its plant in Vietnam, with the objective of doubling its production capacity to meet growing demand. Currently, Daesang operates four factories in Vietnam, each focusing on specific product categories, including convenience foods, ready-to-eat (RTE) meals, sauces, maltose, tapioca starch, and processed fresh meat. This expansion aligns with the company's strategy to strengthen its presence in the Vietnamese market and enhance its production capabilities.

Southeast Asia Savory Snacks Market Report Scope

Savory food has a salty or spicy flavor rather than a sweet one. The Southeast Asian savory snacks market is segmented by product type, ingredient source, distribution channel, and country. By product type market is segmented into extruded snacks, meat snacks, popcorn, fruit and vegetable snacks, potato chips, nuts and seeds, pretzels & crackers, tortilla & corn chips, seaweed snacks and other savory snacks. The market is further segmented by distribution channel into supermarkets/hypermarkets, convenience stores, online retail stores, specialty stores,traditional grocery, vending & foodservice and other distribution channels. Based on Ingredient source, the market is segmented into potato-based, corn/maize based, rice & tapioca based, legume/pulse based, nut& seed based.The market is also segmented by country into Indonesia, Malaysia, Vietnam, Thailand, Philippines, Myanmar, Singapore, and the Rest of Southeast Asia. For each segment, the market sizing and forecasts have been done based on value (in USD million).

By Product Type

| Chips & Crisp- Based Snacks | Potato Chips |

| Tortilla & Corn Chips | |

| Rice & Pulse-Based Chips | |

| Multigrain Chips | |

| Seaweed & Marine-Based Crisps | |

| Nuts, Seeds & Trail Mixes | |

| Fruit and Vegetable Snacks | |

| Popcorn Snacks | |

| Meat & Jerky Snacks | |

| Extruded & Puffed Snacks | |

| Others Products |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retailers |

| Others Distribution Channels |

By Flavor Profile

| Classic Salted/ Plain |

| Flavored |

By Country

| Indonesia |

| Malaysia |

| Vietnam |

| Thailand |

| Philippines |

| Myanmar |

| Singapore |

| Rest of Southeast Asia |

| By Product Type | Chips & Crisp- Based Snacks | Potato Chips |

| Tortilla & Corn Chips | ||

| Rice & Pulse-Based Chips | ||

| Multigrain Chips | ||

| Seaweed & Marine-Based Crisps | ||

| Nuts, Seeds & Trail Mixes | ||

| Fruit and Vegetable Snacks | ||

| Popcorn Snacks | ||

| Meat & Jerky Snacks | ||

| Extruded & Puffed Snacks | ||

| Others Products | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retailers | ||

| Others Distribution Channels | ||

| By Flavor Profile | Classic Salted/ Plain | |

| Flavored | ||

| By Country | Indonesia | |

| Malaysia | ||

| Vietnam | ||

| Thailand | ||

| Philippines | ||

| Myanmar | ||

| Singapore | ||

| Rest of Southeast Asia |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the Southeast Asia savory snacks market and how fast is it growing?

The Southeast Asia savory snacks market is valued at USD 9.71 billion in 2026 and is forecast to reach USD 16.02 billion by 2031, delivering a 10.42% CAGR.

Which product segments are expanding the quickest within the Southeast Asia savory snacks market?

Fruit and vegetable snacks are the fastest-growing category in the Southeast Asia savory snacks market, advancing at a 12.50% CAGR through 2031 as consumers gravitate toward natural, nutrient-dense options.

How important is e-commerce to future growth in the Southeast Asia savory snacks market?

Online Retail is the most dynamic channel in the Southeast Asia savory snacks market, projected to post an 11.45% CAGR (2026-2031) thanks to quick-commerce platforms that fulfil impulse orders within an hour.

Which country will be the primary engine of demand in the Southeast Asia savory snacks market between 2025 and 2030?

Vietnam is set to be the fastest-growing national segment of the Southeast Asia savory snacks market, with a 14.32% CAGR driven by rising incomes, urbanization and modern retail expansion beyond Hanoi and Ho Chi Minh City.