Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 38.97 Billion |

| Market Size (2026) | USD 41.08 Billion |

| Market Size (2031) | USD 53.44 Billion |

| Growth Rate (2026 - 2031) | 5.40% CAGR |

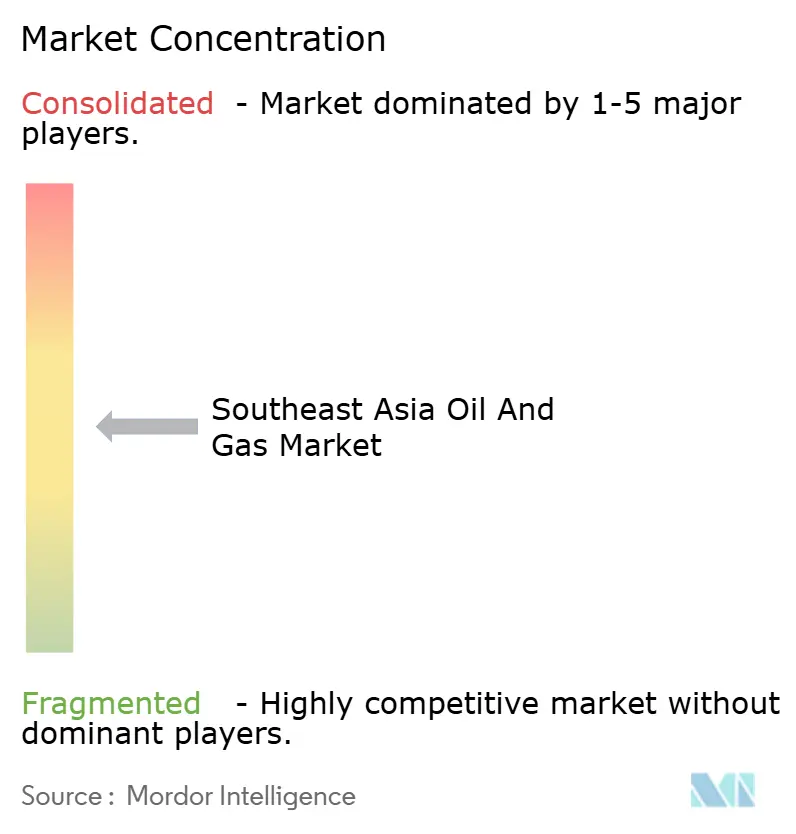

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Oil And Gas Market Analysis by Mordor Intelligence

The Southeast Asia Oil And Gas Market size was valued at USD 38.97 billion in 2025 and estimated to grow from USD 41.08 billion in 2026 to reach USD 53.44 billion by 2031, at a CAGR of 5.40% during the forecast period (2026-2031).

Robust government backing for domestic resource development, accelerated post-pandemic capital spending, and rapid sanctioning of deepwater projects underpin this expansion. Elevated LNG infrastructure investment, particularly in floating storage and regasification units, is expanding regional supply options while facilitating coal-to-gas switching in power generation. Carbon capture and storage (CCS) initiatives are unlocking high-CO₂ fields, and digitalization is lowering breakeven costs at mature assets, jointly lengthening field life cycles. Competitive intensity remains moderate because national oil companies (NOCs) protect upstream acreage, yet international partners find opportunities through joint ventures that deliver advanced subsea, drilling, and CCS technologies.

Key Report Takeaways

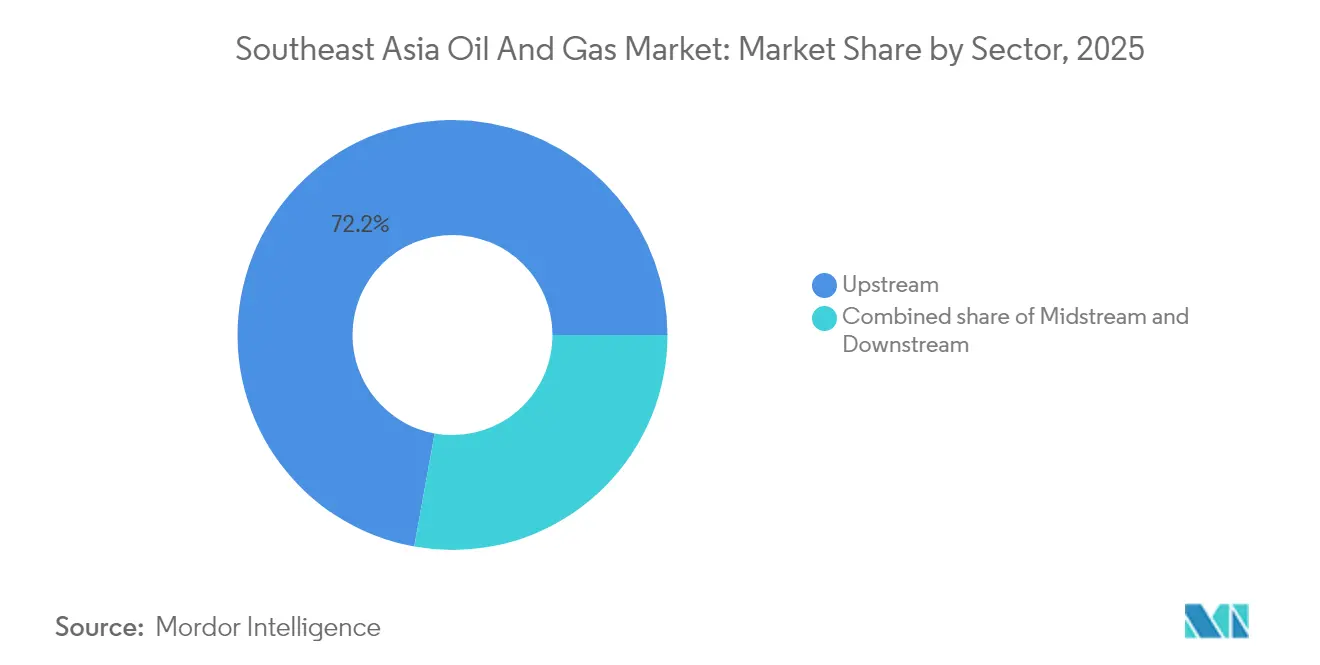

- By sector, the upstream sector accounted for a 72.15% revenue share in 2025 and is forecast to register a 5.67% CAGR through 2031.

- By location, offshore operations accounted for 60.25% of activity in 2025, while onshore projects trailed but still posted a solid 3.98% CAGR to 2031.

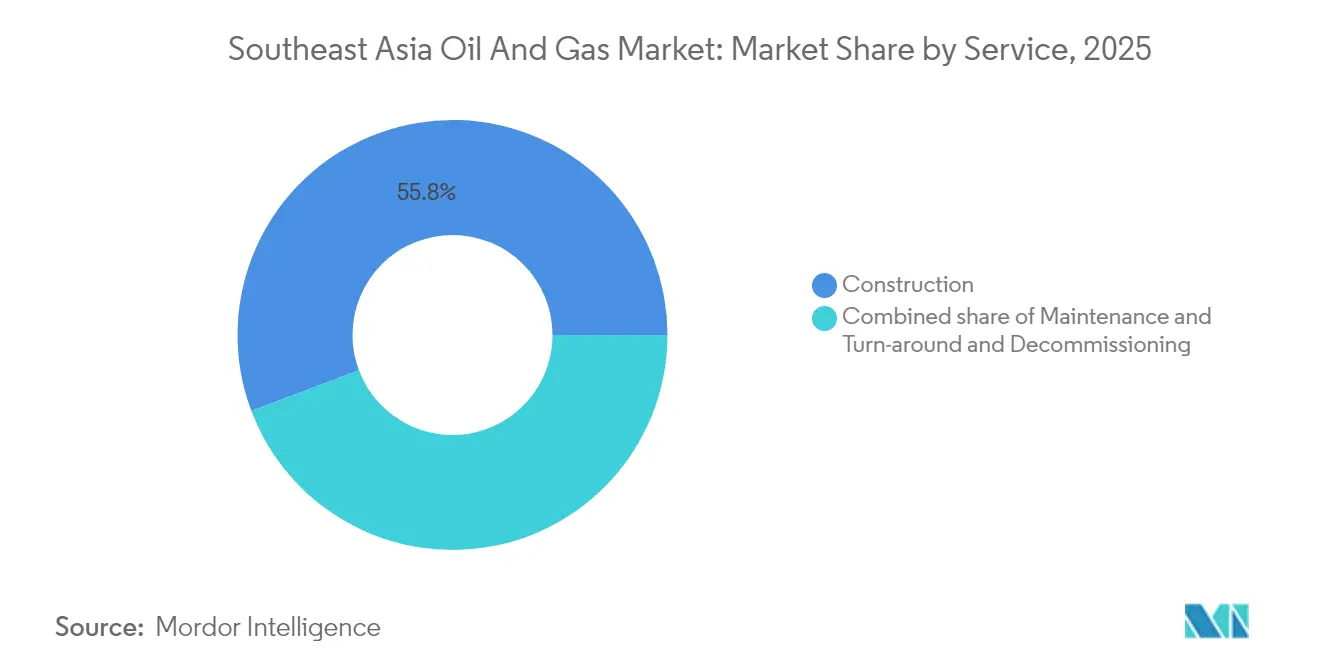

- By service, construction captured a 55.75% share of sector spend in 2025; decommissioning services are expected to expand at the fastest rate, with a 7.74% CAGR through 2031.

- By geography, Indonesia led with 35.22% market share in 2025; the Philippines is expected to post the highest 6.08% CAGR between 2026 and 2031.

- PETRONAS, PT Pertamina, and PTT collectively held a 41% share of 2024 regional upstream output, underscoring NOC dominance in the Southeast Asia oil and gas market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Southeast Asia Oil And Gas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic investment rebound in upstream & LNG supply chains | +1.20% | Indonesia, Malaysia, Thailand core markets | Short term (≤ 2 years) |

| Energy-security push for domestic production & storage | +0.80% | Philippines, Vietnam, Myanmar priority regions | Medium term (2-4 years) |

| Rapid build-out of LNG import terminals & regas capacity | +0.90% | Singapore hub, Philippines, Thailand expansion | Medium term (2-4 years) |

| CCS deployment unlocking high-CO₂ gas fields | +1.10% | Indonesia, Malaysia offshore fields | Long term (≥ 4 years) |

| Biofuel/hydrogen blending pilots in existing gas networks | +0.70% | Singapore, Malaysia regulatory frameworks | Long term (≥ 4 years) |

| Digitalisation enabling marginal field commercialisation | +0.60% | Regional, led by PETRONAS, PTT initiatives | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-pandemic investment rebound accelerates upstream recovery

Capital spending on Southeast Asian upstream projects increased by 34% in 2024 to USD 28.5 billion, as operators reinstated delayed exploration and development programs. PETRONAS dedicated USD 8.2 billion to Malaysian offshore work, and PT Pertamina allocated USD 4.7 billion for Indonesian expansions, signaling restored confidence in demand growth. Approximately 40% of that is spent on targeted LNG supply chains, with Malaysia’s floating LNG and Indonesia’s onshore liquefaction benefiting most. The rapid outlays clear a project backlog dating from 2020-2022 deferrals and position the region as a swing LNG supplier for wider Asia. Real-time reservoir analytics and subsea tie-backs are compressing payback periods, further stimulating upstream commitments.

Energy-security imperatives drive domestic resource development

Governments are intensifying efforts to cut import dependence. The Philippines initiated a strategic petroleum reserve program in 2024, which provides 30 days of coverage, while Vietnam increased its gas storage capacity by 25%. Thailand’s PTT boosted exploration spending 45% in the Gulf of Thailand to offset mature-field decline, and Myanmar awarded 12 new blocks despite political risks. Revised fiscal terms—higher cost-recovery ceilings and accelerated depreciation—have improved project economics, drawing both local and foreign capital. These actions align with broader ASEAN goals of supply resiliency amid volatile global markets.

LNG-terminal construction transforms regional gas infrastructure

Regasification capacity expanded 18 MTPA in 2024, led by the Philippines’ Bataan facility and Thailand’s Map Ta Phut expansion. Singapore’s Jurong Island processed 14.2 MTPA, cementing its role as Southeast Asia’s trading hub. New import capacity is 85% contracted under long-term deals with QatarEnergy and U.S. suppliers, de-risking utilization. FSRUs supply 60% of new capacity, offering rapid deployment and lower costs compared to onshore terminals. Enhanced gas access facilitates coal-to-gas switching, enabling the meeting of emissions targets without compromising grid reliability.

Biofuel integration pilots transform gas-network utilization

Singapore has approved hydrogen blends of up to 20% in existing gas grids, targeting a commercial rollout in 2026.(1)Malaysia Energy Market Authority, “Hydrogen Blending Pilot Approval 2024,” ema.gov.sgPetronas Gas is running biogas injection trials on Peninsular Malaysia lines, proving compatibility without major infrastructure modification. Blending leverages sunk pipeline costs while creating demand for renewable molecules, turning networks into low-carbon enablers. Operators earn premium tariffs for low-carbon content and defer large-scale pipeline retirement, aligning shareholder returns with transition goals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining legacy fields & reserve replacement gap | -0.80% | Indonesia, Malaysia mature basins | Short term (≤ 2 years) |

| Regulatory & fiscal uncertainty across ASEAN members | -0.70% | Regional, varying by jurisdiction | Medium term (2-4 years) |

| ESG-driven capital flight from fossil assets | -0.60% | Regional, affecting international majors | Medium term (2-4 years) |

| South China Sea maritime disputes delaying drilling | -0.50% | Vietnam, Philippines, Malaysia contested areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy field decline outpaces reserve-replacement efforts

Indonesian basins recorded 8-12% annual depletion in 2024, exceeding the global 5-7% norm.(2)Indonesian Ministry of Energy and Mineral Resources, “Field Decline Statistics 2024,” esdm.go.idMalaysia’s aging offshore assets need USD 2.3 billion of maintenance by 2026 to sustain plateau output, straining operator cash flow. The regional reserve-replacement ratio fell to 0.7 times, underscoring the insufficient number of discoveries. Infill drilling and enhanced recovery provide only tactical relief. Operators face steeper lift costs and heightened abandonment liabilities, which intensify capital discipline and can delay frontier exploration.

Regulatory fragmentation creates investment uncertainty

Frequent fiscal-term revisions and tightening local-content rules complicate economic modeling. Indonesia’s 2024 cost-recovery overhaul reduced contractor margins by 8-12%, while Malaysia increased mandated local content to 70% for certain offshore scopes, thereby raising procurement costs. Approval cycles in Thailand lengthened by up to two years. These variances oblige investors to demand higher returns, which can shelve marginal projects. ASEAN harmonization remains aspirational because member states are reluctant to cede resource sovereignty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Upstream dominance reflects resource endowment

Upstream activities generated 72.15% of 2025 revenue, and the segment is projected to grow at a rate of 5.67% through 2031, maintaining its largest share of the Southeast Asia oil and gas market. Massive projects such as Indonesia’s Abadi LNG and Malaysia’s Kasawari gas development underpin spending, while midstream networks expand in tandem to evacuate new volumes. Downstream capacity growth lags because stricter emission standards curb new refinery builds.

Digital reservoir models and advanced subsea processing are elevating recovery factors, reinforcing upstream leadership. Governments favor domestic production to enhance energy security, and new fiscal incentives tend to direct capital toward exploration rather than refining upgrades. Enhanced oil recovery and unconventional resource pilots will keep the upstream segment at the forefront of the Southeast Asia oil and gas industry.

By Location: Offshore operations drive technical innovation

Offshore projects accounted for 60.25% of total 2025 expenditure and are expected to grow at a 6.17% CAGR through 2031 as operators expand their operations into regional basins. Water-depth records are continually broken in Malaysia’s Sabah and Sarawak plays, validating commercial viability beyond 1,000 meters. Onshore assets remain important for gas processing and storage, yet lack comparable growth momentum.

Floating production systems account for 45% of new capacity, offering cost flexibility and a reduced environmental footprint. ASEAN regulators are gradually aligning offshore safety and environmental codes, easing cross-border collaboration. The maturity of shallow-water supply chains shortens learning curves for deepwater development, sustaining offshore dominance in the Southeast Asia oil and gas market.

By Service: Construction leads while decommissioning accelerates

Construction services accounted for 55.75% of revenue in 2025, as LNG terminals and offshore platforms proliferated. Decommissioning, although smaller, is projected to advance at a rate of 7.74% annually to 2031, reflecting the strict removal deadlines for end-of-life installations in Malaysia and Indonesia. Maintenance and turnaround retain steady demand by preserving uptime at aging fields.

TechnipFMC secured USD 1.2 billion in Southeast Asian awards in 2024, encompassing subsea umbilicals and LNG modules. Local-content mandates foster consortia pairing global service majors with domestic fabricators, enabling capability transfer. As decommissioning volumes rise, specialized heavy-lift and well-plugging services are expected to flourish, diversifying revenue beyond greenfield build-out in the Southeast Asian oil and gas industry.

Geography Analysis

Indonesia retains market leadership with a 35.22% share in 2025, thanks to extensive offshore reserves, mature onshore facilities, and PT Pertamina’s USD 4.7 billion upstream program, which targets an incremental 180,000 BOPD by 2026. The Abadi LNG project, seeking a final investment decision, will add strategic export capacity upon sanction. Malaysia remains a strong second through PETRONAS’s integrated value chain; the Kasawari field delivered its first gas in 2024 at 1.2 BCFD, reinforcing domestic supply security. Thailand balances declining legacy output with unconventional exploration and an 11 MTPA Map Ta Phut regas expansion that anchors import flexibility.

The Philippines is expected to achieve the highest growth rate of 6.08% through 2031, as Malampaya Phase 2 ramps up and multiple LNG terminals come online to displace coal in power generation. Vietnam’s Nam Con Son developments and industrial demand boost its trajectory, supported by PetroVietnam’s 15% production growth plan. Singapore’s Jurong hub maintains regional supply liquidity by providing storage, blending, and facilitating price discovery. Myanmar’s output remains modest due to political uncertainty; however, the success of the Shwe field drilling demonstrates ongoing international engagement.

Cross-border projects knit markets closer. The Trans-ASEAN Gas Pipeline facilitates volumetric swaps, allowing countries with seasonal surpluses to support their neighbors. Regulators are drafting unified HSE and metering standards to lower transaction friction. Geography thus exerts a dual influence, granting incumbent producers scale benefits while opening up niche growth opportunities for import-reliant economies within the Southeast Asia oil and gas market size calculus.

Competitive Landscape

National champions PETRONAS, PT Pertamina, and PTT dominate upstream acreage due to state mandates and preferential access, jointly supplying roughly 41% of the 2024 regional output. International oil companies, such as Shell, ExxonMobil, and TotalEnergies, pursue deepwater or technologically complex projects where their engineering expertise justifies participation fees. Sovereign resource policies limit majority foreign ownership, channeling collaboration into joint ventures that share risk and transfer knowledge.

Digital transformation amplifies competitive gaps. PETRONAS’s AI reservoir-optimization platform increased average well productivity by 12% across more than 200 wells, and PTT’s predictive maintenance reduced unplanned downtime by 18%. Service majors TechnipFMC, Saipem, and Samsung Engineering win large EPC packages by pairing their subsea credentials with strong local content compliance. White-space competition is growing in CCS deployment, decommissioning, and renewable-gas integration fields, where first-mover technical proficiency can secure long-term service revenues.

Capital markets also shape rivalry. ESG-aligned Western investors retreat, whereas Middle Eastern and Asian funds acquire divested assets, often negotiating favorable fiscal terms from host governments keen to sustain output. As a result, regional cost structures stabilize, ensuring a moderate level of concentration in the Southeast Asian oil and gas market.

Southeast Asia Oil And Gas Industry Leaders

TechnipFMC

Saipem SpA

PT. JGC Indonesia

Bechtel Corporation

Fluor Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: PETRONAS announced a final investment decision for the Kasawari North development offshore Sarawak, committing USD 3.2 billion to expand production capacity by 800 MMSCFD.

- November 2024: PT Pertamina completed the acquisition of ConocoPhillips' Indonesian assets for USD 1.3 billion, adding 45,000 BOPD production capacity and strengthening domestic resource control.

- October 2024: Shell and PTT signed a joint venture agreement for Thailand's Bongkot South development, investing USD 2.1 billion in deepwater infrastructure and subsea systems.

- September 2024: TotalEnergies sanctioned the Papua LNG project in Indonesia with a USD 6.0 billion investment, targeting 9.5 MTPA production capacity by 2028.

Southeast Asia Oil And Gas Market Report Scope

Oil and natural gas are major industries in the energy market and significantly impact the global economy. Oil and gas production and distribution processes and systems are extremely complex, capital-intensive, and require cutting-edge technology. The industry is frequently split into three segments: upstream (oil and gas research and production), midstream (transportation and storage), and downstream (refining and marketing).

Southeast Asia's oil and gas market is segmented by sector and geography. By sector, the market is segmented into upstream, midstream, and downstream. The report also covers the market size and forecasts across major countries. For each segment, market sizing and forecasts have been done based on revenue (USD billion).

By Sector

| Upstream |

| Midstream |

| Downstream |

By Location

| Onshore |

| Offshore |

By Service

| Construction |

| Maintenance and Turn-around |

| Decommissioning |

By Geography

| Indonesia |

| Malaysia |

| Thailand |

| Vietnam |

| Philippines |

| Singapore |

| Myanmar |

| Rest of Southeast Asia |

| By Sector | Upstream |

| Midstream | |

| Downstream | |

| By Location | Onshore |

| Offshore | |

| By Service | Construction |

| Maintenance and Turn-around | |

| Decommissioning | |

| By Geography | Indonesia |

| Malaysia | |

| Thailand | |

| Vietnam | |

| Philippines | |

| Singapore | |

| Myanmar | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

How large is the Southeast Asia oil and gas market?

The Southeast Asia oil and gas market size is valued at about USD 41.08 billion in 2026 and is on track to top USD 53.44 billion by 2031, growing at 5.40% annually.

Which segment shows the fastest growth through 2031?

Decommissioning services are projected to advance at 7.74% CAGR as regulators enforce platform-removal deadlines across Malaysia and Indonesia.

Why is the Philippines considered the fastest-growing geography?

New LNG import terminals and the Malampaya field expansion lift the Philippines to a 6.08% CAGR, outpacing other ASEAN members.

How are CCS projects influencing regional supply?

Commercial CCS at fields such as Kasawari captures CO₂ and enables development of high-CO₂ reservoirs, unlocking reserves previously uneconomic under conventional processing.

What role does digitalization play in field economics?

AI-driven reservoir optimization and predictive maintenance raise production up to 15% and cut development costs by about 25%, improving marginal-field viability.

Which companies dominate regional output?

PETRONAS, PT Pertamina, and PTT together supply about 41% of Southeast Asian output, underscoring strong but not monopolistic NOC control.

Page last updated on: