Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

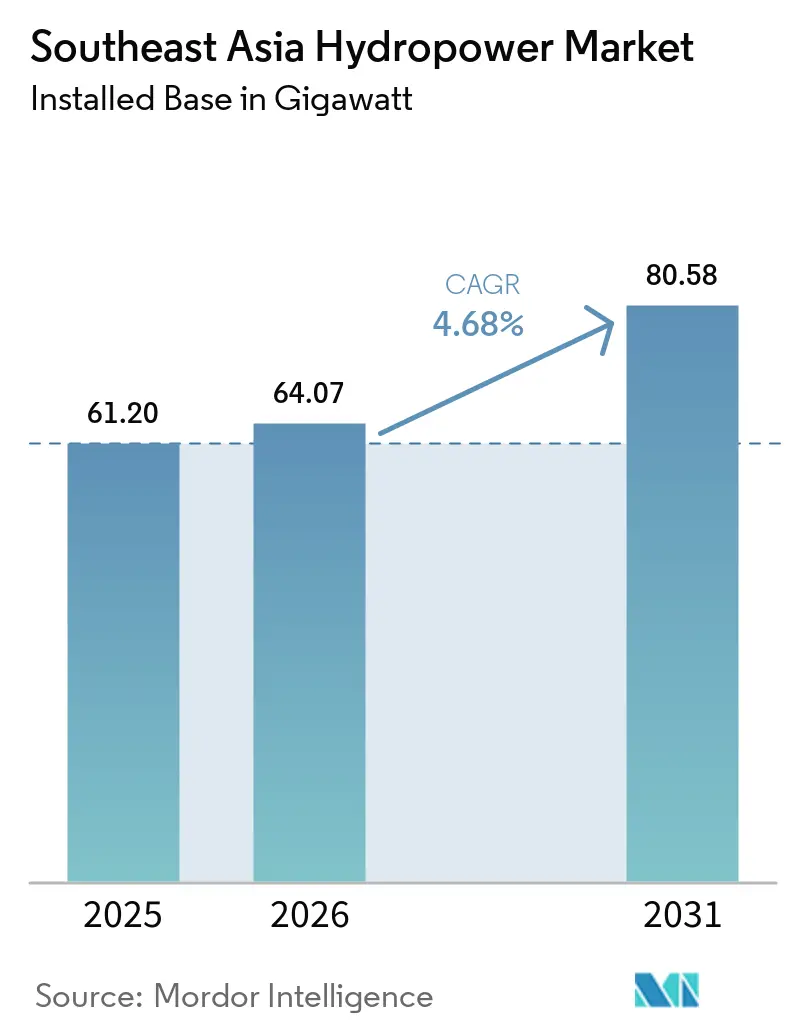

| Base Year Market Size (2025) | 61.20 gigawatt |

| Market Volume (2026) | 64.07 gigawatt |

| Market Volume (2031) | 80.58 gigawatt |

| Growth Rate (2026 - 2031) | 4.68% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Hydropower Market Analysis by Mordor Intelligence

The Southeast Asia Hydropower market size is expected to grow from 61.20 gigawatt in 2025 to 64.07 gigawatt in 2026 and is forecast to reach 80.58 gigawatt by 2031 at 4.68% CAGR over 2026-2031.

Market Analysis

Utilities that once favored large reservoir dams now channel budgets into pumped-storage projects that soak up midday solar oversupply, while independent power producers (IPPs) record the fastest end-user expansion at a 6.7% CAGR by locking in data-center power purchase agreements (PPAs) in Indonesia and Malaysia.[1]World Bank, “ASEAN Power Grid Facility Launch,” worldbank.org The ASEAN Power Grid (APG) roadmap, which targets 17.6 GW of cross-border transfer capacity by 2040, up from 7.7 GW in mid-2023, indicates that the Southeast Asian hydropower market is increasingly serving as a regional flexibility asset rather than a purely national baseload resource.

Key Report Takeaways

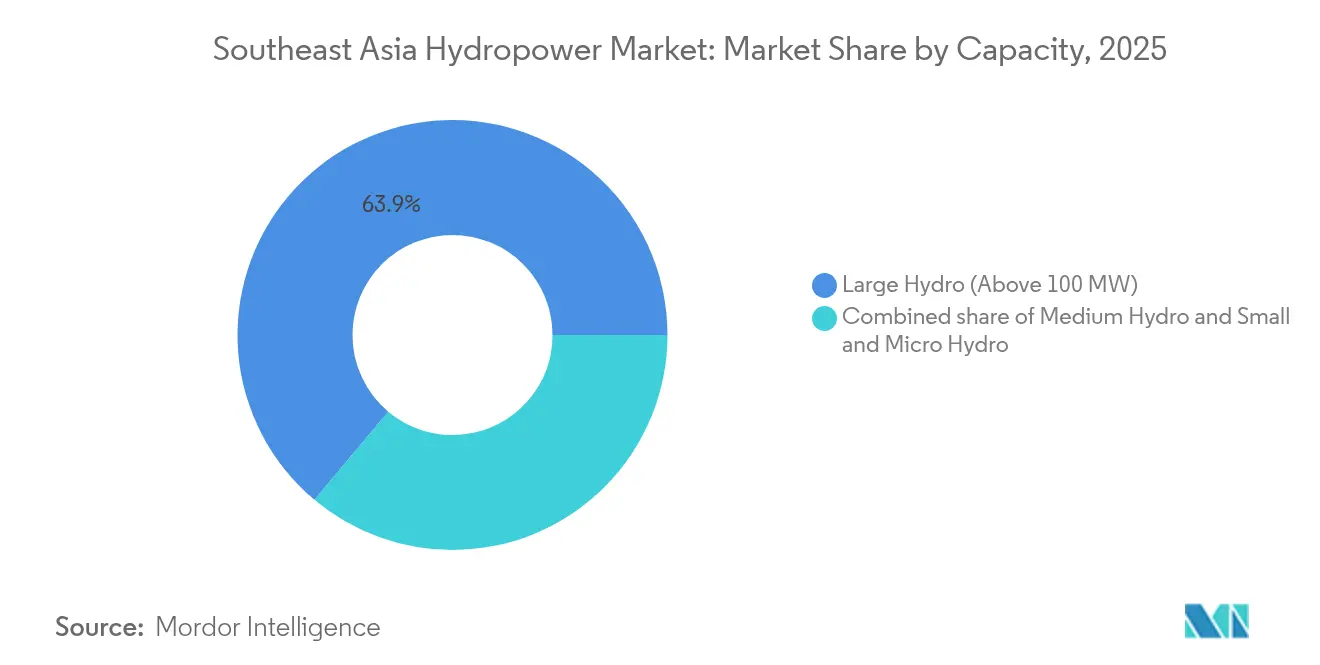

- By capacity, installations above 100 MW held 63.90% of the Southeast Asia hydropower market share in 2025, while small and micro plants below 10 MW are projected to expand at a 5.62% CAGR through 2031.

- By technology, reservoir-based systems commanded a 53.25% share of the Southeast Asia hydropower market size in 2025, yet pumped storage is advancing at an 8.12% CAGR to 2031.

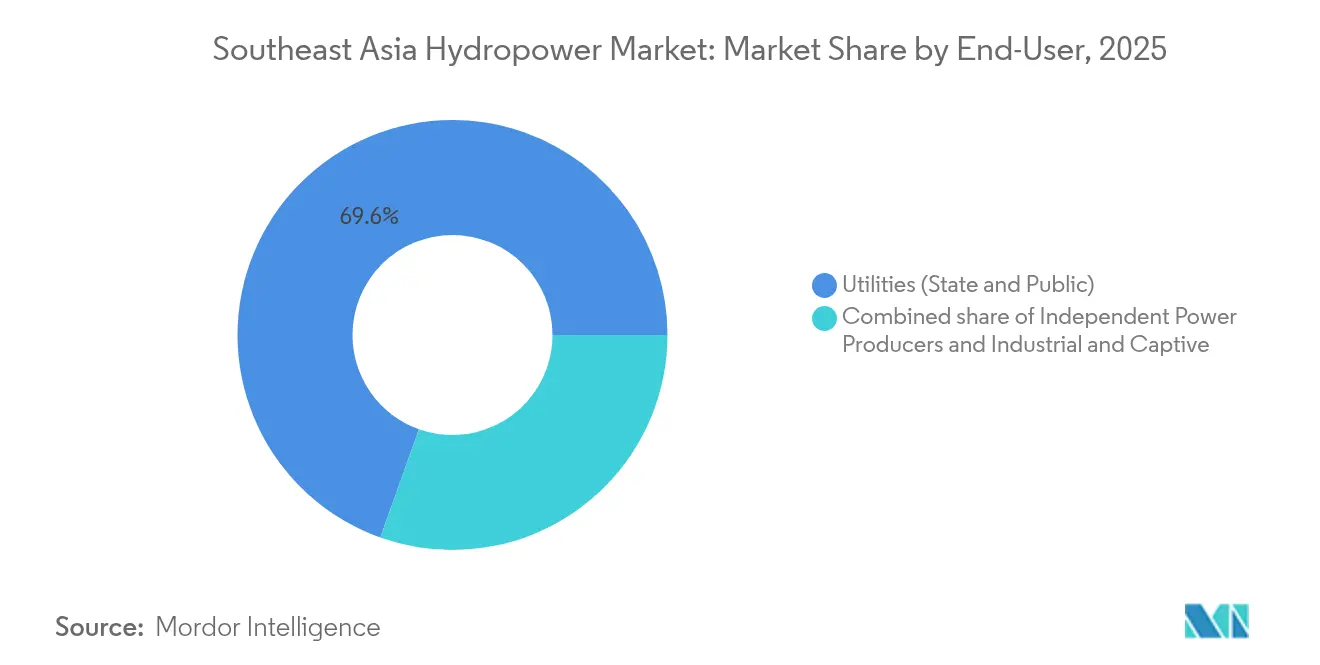

- By end-user, utilities (state and public) retained 69.55% of the Southeast Asia hydropower market in 2025, while independent power producers (IPPs) will post the fastest uptick at 6.62% CAGR to 2031.

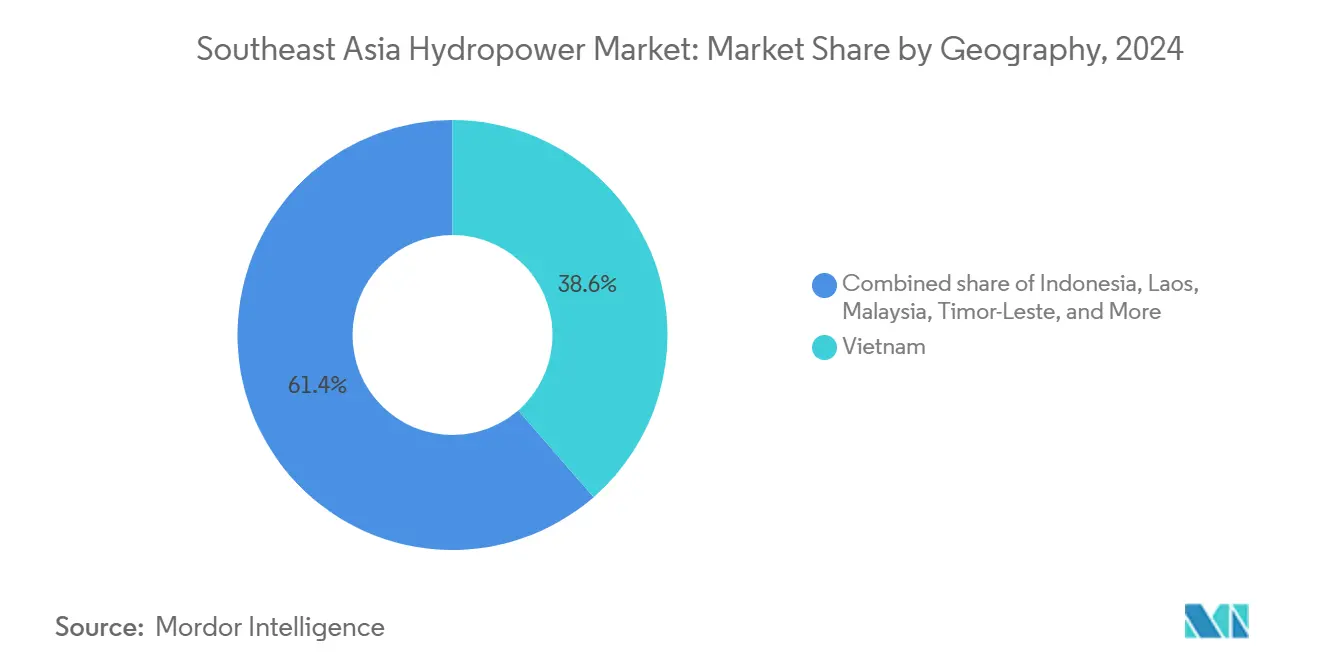

- By geography, Vietnam led with 38.10% of regional capacity in 2025; Malaysia is forecast to grow at a 8.86% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Southeast Asia Hydropower Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging grid-stabilization need amid variable solar and wind integration | +1.20% | Thailand, Philippines, Vietnam, Indonesia | Medium term (2-4 years) |

| Low-interest ASEAN green-bond inflows | +0.90% | Indonesia, Malaysia, Vietnam | Short term (≤ 2 years) |

| Regional power trade under ASEAN Power Grid roadmap | +0.80% | Laos, Thailand, Malaysia, Singapore, Vietnam | Long term (≥ 4 years) |

| Data-center-backed private PPAs in Indonesia and Malaysia | +0.60% | Java, Johor, Metro Manila | Medium term (2-4 years) |

| Water-battery pumped storage for solar over-generation | +1.10% | Philippines, Thailand, Indonesia, Vietnam | Medium term (2-4 years) |

| AI-assisted hydrology forecasting cuts O&M costs | +0.30% | Regional | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Grid-Stabilization Need Amid Variable Solar and Wind Integration

Battery energy-storage systems commissioned in Thailand in 2023 offer a two-hour duration, yet evening peaks persist when air-conditioning demand climbs after sunset. Feasibility studies for 500 MW pumped-storage at Lam Ta Khlong target 8- to 12-hour discharge windows, bridging the sunset-to-midnight ramp.[2]Electricity Generating Authority of Thailand, “Pumped-Storage Feasibility Studies,” egat.co.th In the Philippines, a 5.7 GW pumped-storage pipeline is anchored by Luzon and Mindanao sites that satisfy a Department of Energy rule mandating dispatchable storage for grid-connection priority. Similar pivots appear in Vietnam’s Power Development Plan 8, which caps new large hydro while steering investment toward daily-cycling pumped storage that balances a 16.5 GW solar fleet.[3]Ministry of Industry and Trade Vietnam, “Power Development Plan 8,” moit.gov.vn Indonesia’s PLN plans 3.7 GW of pumped storage as it retires 9.2 GW of coal capacity under the Just Energy Transition Partnership.

Low-Interest ASEAN Green-Bond Inflows

Outstanding ASEAN sustainable bonds climbed to USD 72.7 billion in 2023, with 37% of proceeds earmarked for renewable energy. The ASEAN Catalytic Green Finance Facility committed USD 2.3 billion across 15 hydropower projects that meet Climate Bonds Initiative criteria, including run-of-river clusters in Laos and the Philippines. Indonesia’s sovereign green sukuk raised USD 3 billion in 2024, channeling funds to pumped-storage pre-development in West Java and Sumatra. Malaysia’s SRI sukuk lowered Sarawak Energy’s financing cost for the 1,285 MW Baleh dam scheduled for 2027 completion.

Regional Power Trade Under ASEAN Power Grid Roadmap

The Lao-Thailand-Malaysia-Singapore Power Integration Project achieved full operation in 2024, wheeling 100-200 MW from Laos to Singapore and displacing liquefied natural gas in island grids. The World Bank’s ASEAN Power Grid Facility, launched in 2025 with USD 500 million seed capital, seeks to mobilize USD 800 billion for transmission and storage that lifts interconnection capacity to 17.6 GW by 2040. Vietnam and Cambodia signed a 2024 MoU to exchange up to 500 MW seasonally, improving utilization of wet-season surpluses. Regulatory harmonization, however, remains uneven as wheeling charges and renewable-certificate rules differ across bilateral deals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cheaper utility-scale battery prices | -0.70% | Thailand, Philippines, Indonesia | Short term (≤ 2 years) |

| Escalating anti-dam social activism | -0.50% | Mekong basin nations | Long term (≥ 4 years) |

| Prolonged La Niña/El Niño flow volatility | -0.60% | Vietnam, Philippines, Thailand | Medium term (2-4 years) |

| Cross-border ESG due-diligence delays Chinese EPC loans | -0.40% | Laos, Myanmar, Cambodia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Center-Backed Private PPAs in Indonesia and Malaysia

Microsoft, Google, and Amazon Web Services announced USD 12 billion in data-center investment during 2024, clustering in Java and Johor due to fiber connectivity and land availability. These hyperscalers require 24/7 carbon-free energy, spurring PLN’s first hydro-backed corporate PPA that allocates 150 MW from the Asahan cascade with hourly blockchain verification. Sarawak Energy followed by assigning 300 MW from Bakun and Murum to a hyperscaler under a premium-priced contract. IPPs such as Aboitiz Power and CK Power now target 20-50 MW pumped-storage and small-hydro PPAs with colocation firms and cryptocurrency miners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cheaper utility-scale battery prices | -0.7% | Thailand, Philippines, Indonesia | Short term (≤ 2 years) |

| Escalating anti-dam social activism | -0.5% | Mekong basin nations | Long term (≥ 4 years) |

| Prolonged La Niña/El Niño flow volatility | -0.6% | Vietnam, Philippines, Thailand | Medium term (2-4 years) |

| Cross-border ESG due-diligence delays Chinese EPC loans | -0.4% | Laos, Myanmar, Cambodia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cheaper Utility-Scale Battery Prices

BloombergNEF pegged lithium-ion pack costs at USD 139 /kWh in 2024 and expects USD 100 by 2027, squeezing pumped-storage economics for two- to four-hour services. Lazard’s 2023 levelized-cost figures show battery storage overlapping pumped hydro for short durations, prompting 4.5 GW of approved battery projects in the Philippines.[4]Philippine Department of Energy, “2024 Renewable Energy Roadmap,” doe.gov.ph Thailand’s 200 MW BESS demonstrated 90-millisecond response times that outperform pumped hydro’s 5-10 minute start-up.

Escalating Anti-Dam Social Activism

Laos paused the 1,460 MW Luang Prabang dam in 2021 amid downstream protests citing sediment loss and fishery decline.[5]Mekong River Commission, “Luang Prabang Prior Consultation Report,” mrcmekong.org The Lower Sesan 2 dam displaced 5,000 villagers and spurred legal actions that now challenge new Mekong proposals. Myanmar’s 6,000 MW Myitsone remains suspended, highlighting social-license risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity: Small Hydro Gains as Megaproject Permitting Stalls

Small and micro plants below 10 MW posted the fastest growth, expanding at a 5.62% CAGR as developers favored streamlined permitting and lower social-license risk. The Philippines added 175 MW of small hydro by 2024 with another 500 MW in the pipeline, targeting diesel displacement on off-grid islands. Vietnam hosts more than 2,500 small plants, but suspended new licenses in 2024 pending cumulative-impact studies.

Large hydro above 100 MW still held 63.90% of the Southeast Asia hydropower market share in 2025, anchored by legacy assets such as Bakun (2,400 MW) and Srinagarind (720 MW). New capacity now concentrates in Laos, where the Chinese-financed Xayaburi (1,285 MW) reached full operation in 2024. Medium hydro between 10-100 MW fulfills a middle-ground strategy; PLN scheduled 680 MW of such schemes in Sumatra and Kalimantan to balance build-time, unit size, and social acceptance.

By Technology: Pumped Storage Captures Solar Arbitrage Premium

Pumped storage is advancing at an 8.12% CAGR as its 8-24 hour duration matches the region’s widening peak-to-trough spreads. The Philippines’ 5.7 GW pipeline, led by the 420 MW Wawa project, aims for 2028-2030 commissioning. Thailand committed THB 90 billion for 1.6 GW of new pumped storage, and Indonesia mapped 3.7 GW of opportunity where arbitrage spreads exceeded USD 55 /MWh in 2024.

Reservoir-based plants kept 53.25% of the Southeast Asia hydropower market size in 2025, dominated by multipurpose dams such as Bakun and Hoa Binh. Run-of-river assets now account for roughly 28% of capacity after the Mekong River Commission guidelines favored the design for tributaries supporting migratory fish. In-stream and conduit systems remain niche but show promise in Indonesian irrigation canals.

By End-User: IPPs Exploit Data-Center and Corporate PPA Demand

IPPs posted a 6.62% CAGR by 2031, almost twice the rate of state utilities, by signing premium corporate PPAs that pay fixed prices for carbon-free energy. Aboitiz Power’s 150 MW agreement with a Philippine data center in 2024 priced power 30% above spot and included hourly renewable-certificate matching. Sarawak Energy allocated 300 MW to a hyperscaler at a USD 5 /MWh green premium.

State-owned enterprises still supplied 69.55% of output in 2025, but debt ceilings slowed their build-out; EVN disclosed a USD 4.2 billion financing gap for its plan to 2030. Industrial and captive users expanded modestly with micro-hydro retrofits at palm-oil mills delivering sub-4-year paybacks.

Geography Analysis

Vietnam accounted for 38.10% of installed capacity in 2025, yet now channels new investment toward 4.5 GW of pumped storage, Gia Lai, Bac Ai, and the Hoa Binh expansion, to stabilize its 16.5 GW solar portfolio. Vietnam power infrastructure is shifting toward pumped storage to balance renewable intermittency. Indonesia followed with 6.2 GW, but PLN’s 2024-2030 roadmap pivots to pumped storage in Java and Bali as coal units retire. The Philippines operated 3.9 GW and targets 5.7 GW of pumped storage to cut imported LNG reliance, which reached 35% of generation in 2024.

River-basin limits cap Thailand’s 3.4 GW hydro fleet, so EGAT is adding 1.6 GW of pumped storage and importing 2.1 GW from Laos via cross-border lines. Malaysia’s 2.1 GW concentrates in Sarawak, where Baleh (1,285 MW) will lift exports to Singapore through a 100 MW subsea cable that went live in 2024 (3). Timor-Leste, starting from near zero, records a 112.95% CAGR as the 60 MW Iralalaro I nears completion by 2026; a second 140 MW phase awaits financing.

Laos, Cambodia, and Myanmar collectively held 8.5 GW in 2024, with Laos exporting 90% of output to Thailand and Vietnam, reinforcing its moniker as the “battery of Southeast Asia”.

Competitive Landscape

Competitive intensity is moderate. State utilities, EVN, EGAT, PLN, Tenaga Nasional Berhad, controlled 68% of installed capacity and owned transmission assets in 2024. Chinese EPC contractors PowerChina, Sinohydro, and China Three Gorges compete on turnkey speed and concessional Belt and Road finance but now face added ESG hurdles that lengthen approvals by 12-18 months. IPPs such as Aboitiz Power, CK Power, and Sarawak Energy occupy white space in pumped storage and small hydro where state budgets or risk appetite are limited.

Equipment suppliers Andritz, Voith, and GE Vernova contest turbine-rehabilitation tenders as Thailand and the Philippines tighten grid codes. Andritz’s 2024 variable-speed Francis turbine patent claims 8-12% part-load efficiency gains, a differentiator in ancillary service markets valued at USD 15-25 /MWh.[7]European Patent Office, “Variable-Speed Francis Turbine EP4012345,” epo.org

Digitalization is the new yardstick. EGAT’s multireservoir AI optimizer and PLN’s predictive-maintenance edge modules cut O&M costs by USD 2-5 /MWh, extending asset life without fresh capital. Battery developers now undercut pumped storage for two- to four-hour services, while blockchain renewable-certificate platforms let IPPs bypass utility intermediaries for corporate PPAs.

Southeast Asia Hydropower Industry Leaders

Vietnam Electricity Construction JSC

Tenaga Nasional Berhad

Andrtiz AG

PT Perusahaan Listrik Negara

Electricity Generating Authority of Thailand

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The World Bank launched the ASEAN Power Grid Facility with an initial USD 500 million commitment aimed at mobilizing USD 800 billion for cross-border lines that lift interconnection capacity to 17.6 GW by 2040.

- October 2024: Sarawak Energy awarded China Three Gorges the EPC contract for the 1,285 MW Baleh project, including a 300 MW hyperscaler PPA, Southeast Asia’s largest hydro-backed corporate deal.

Southeast Asia Hydropower Market Report Scope

Hydropower, or hydroelectric power, is one of the largest and oldest renewable energy sources, which uses the natural flow of moving water to generate electricity. Hydropower technologies generate electricity by the elevation difference created by a dam or diversion structure between water flowing in one direction and out in the other direction.

The Southeast Asia Hydropower Market is segmented by capacity, technology, component, end-user, and geography. By capacity, the market is segmented into large hydro (above 100 MW), medium hydro (10 to 100 MW), and small and micro hydro (below 10 MW). By technology, the market is segmented into reservoir-based, run-of-river, pumped-storage, and in-stream and micro-conduit. By end-user, the market is segmented into utilities (state and public), independent power producers, and industrial and captive. By geography, the market is segmented into Vietnam, Indonesia, Philippines, Thailand, Malaysia, Singapore, and Rest of Southeast Asia (Brunei, Cambodia, Laos, Myanmar, and Timor-Leste). The report also covers the market size and forecasts for Southeast Asia.

For each segment, the market sizing and forecasts have been done based on the installed capacity (GW).

By Capacity

| Large Hydro (Above 100 MW) |

| Medium Hydro (10 to 100 MW) |

| Small and Micro Hydro (Below 10 MW) |

By Technology

| Reservoir-Based |

| Run-of-River |

| Pumped-Storage |

| In-Stream and Micro-conduit |

By Component (Qualitative Analysis only)

| Turbines |

| Generators |

| Control and Automation |

| Balance-of-Plant |

By End-User

| Utilities (State & Public) |

| Independent Power Producers |

| Industrial and Captive |

By Geography

| Vietnam |

| Indonesia |

| Philippines |

| Thailand |

| Malaysia |

| Singapore |

| Rest of Southeast Asia (Brunei, Cambodia, Laos, Myanmar, and Timor-Leste) |

| By Capacity | Large Hydro (Above 100 MW) |

| Medium Hydro (10 to 100 MW) | |

| Small and Micro Hydro (Below 10 MW) | |

| By Technology | Reservoir-Based |

| Run-of-River | |

| Pumped-Storage | |

| In-Stream and Micro-conduit | |

| By Component (Qualitative Analysis only) | Turbines |

| Generators | |

| Control and Automation | |

| Balance-of-Plant | |

| By End-User | Utilities (State & Public) |

| Independent Power Producers | |

| Industrial and Captive | |

| By Geography | Vietnam |

| Indonesia | |

| Philippines | |

| Thailand | |

| Malaysia | |

| Singapore | |

| Rest of Southeast Asia (Brunei, Cambodia, Laos, Myanmar, and Timor-Leste) |

Key Questions Answered in the Report

How large is hydropower capacity in Southeast Asia in 2026?

Total installed capacity reaches 64.07 GW in 2026, and it is forecast to grow to 80.58 GW by 2031.

Which technology is expanding fastest in the region?

Pumped-storage projects post the highest growth, advancing at an 8.12% CAGR through 2031 as they complement rising solar output.

Why are IPPs gaining ground against state utilities?

IPPs sign premium corporate PPAs with hyperscalers and industrial clients, capturing a 6.62% CAGR versus 3.76% for state utilities.

What role does the ASEAN Power Grid play?

The APG roadmap aims for 17.6 GW of cross-border capacity by 2040, turning hydropower into a regional flexibility resource that replaces gas imports.

How do battery prices affect pumped-storage economics?

Falling lithium-ion costs narrow the cost gap for two- to four-hour services, yet pumped storage remains competitive for 8-24 hour durations.

Which country is adding capacity most rapidly?

Timor-Leste shows a 112.95% CAGR from a small base as the 60 MW Iralalaro I project comes online by 2026.

Page last updated on: