Southeast Asia Compressed Natural Gas (CNG) Dispenser Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

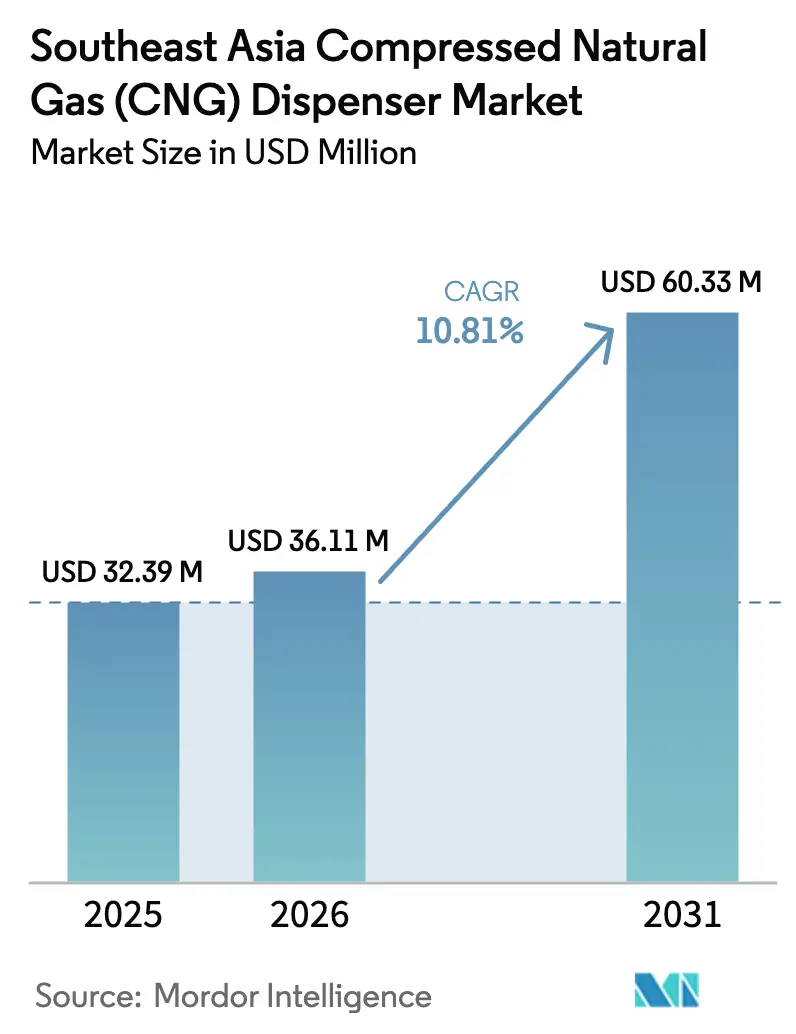

| Base Year Market Size (2025) | USD 32.39 Million |

| Market Size (2026) | USD 36.11 Million |

| Market Size (2031) | USD 60.33 Million |

| Growth Rate (2026 - 2031) | 10.81% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Compressed Natural Gas (CNG) Dispenser Market Analysis by Mordor Intelligence

The Southeast Asia Compressed Natural Gas Dispenser Market size was valued at USD 32.39 million in 2025 and is estimated to grow from USD 36.11 million in 2026 to reach USD 60.33 million by 2031, at a CAGR of 10.81% during the forecast period (2026-2031).

This trajectory is underpinned by shifting demand from urban public-transport fleets, which now pivot to battery-electric drives, toward industrial, logistics, and mining operators that view CNG as a hedge against diesel volatility and a practical emissions-reduction tool when on-site electrification is impractical.[1]S&P Global, “Asia Pacific LNG Market Analysis,” S&P Global, spglobal.com Region-wide LNG import-terminal build-outs have expanded regasification capacity by 8.1 million t p.a. since 2023, cutting feedstock costs and improving dispenser project economics.[2]S&P Global, “Asia Pacific LNG Market Analysis,” S&P Global, spglobal.com Indonesia commands the largest national foothold through Pertamina’s state-backed stations and pipeline reach, whereas Vietnam delivers the fastest growth on the back of private depot investments that insulate manufacturing clusters from fuel-price swings.[3]International Energy Agency, “Southeast Asia Energy Outlook 2024,” IEA, iea.org Technology competition now centers on IoT-enabled, multi-hose systems that maximize throughput per square meter and cut downtime via predictive maintenance analytics.[4]Gilbarco Veeder-Root, “Fuel Dispensing Solutions,” Gilbarco, gilbarco.com Policy risk, however, remains a live threat: Malaysia’s 2025 NGV phase-out proved that electrification mandates can override favorable cost curves and instantly shrink the Southeast Asia CNG dispenser market.

Key Report Takeaways

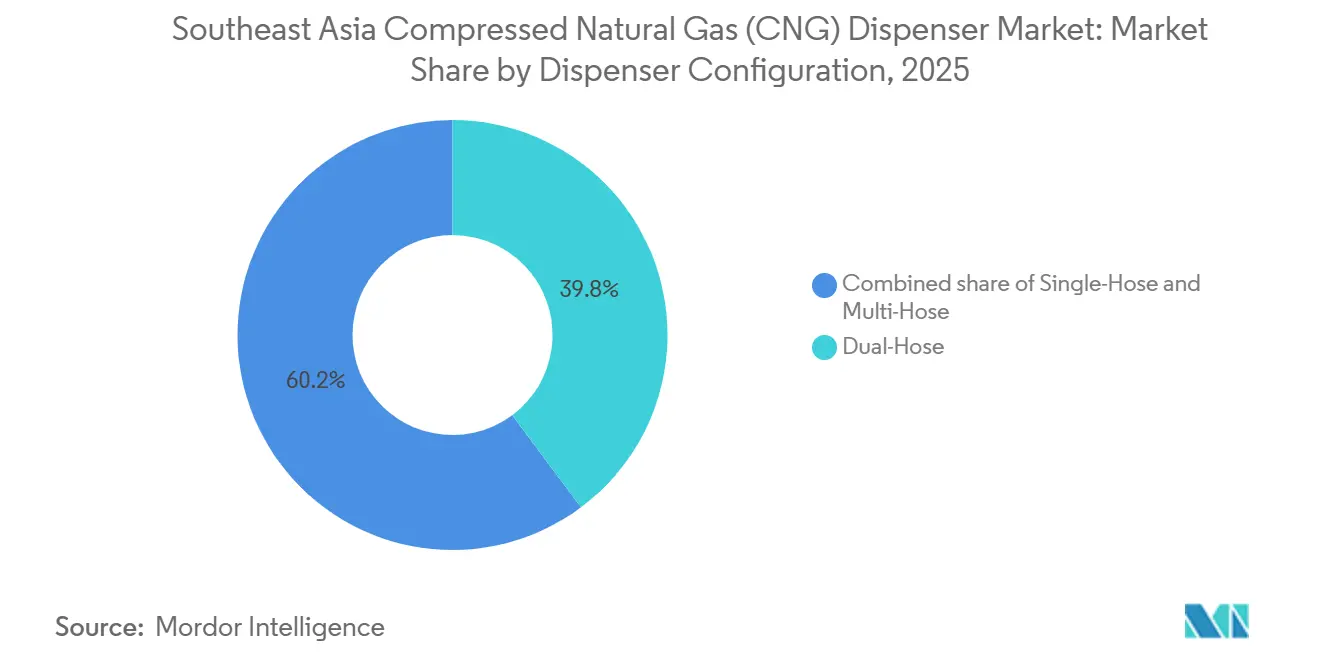

- By dispenser configuration, dual-hose units led with 39.8% of Southeast Asia CNG dispenser market share in 2025, while multi-hose units are projected to grow at a 12.8% CAGR through 2031.

- By station type, fast-fill sites captured 55.5% share of the Southeast Asia CNG dispenser market size in 2025; mobile and portable stations are advancing at a 13.5% CAGR to 2031.

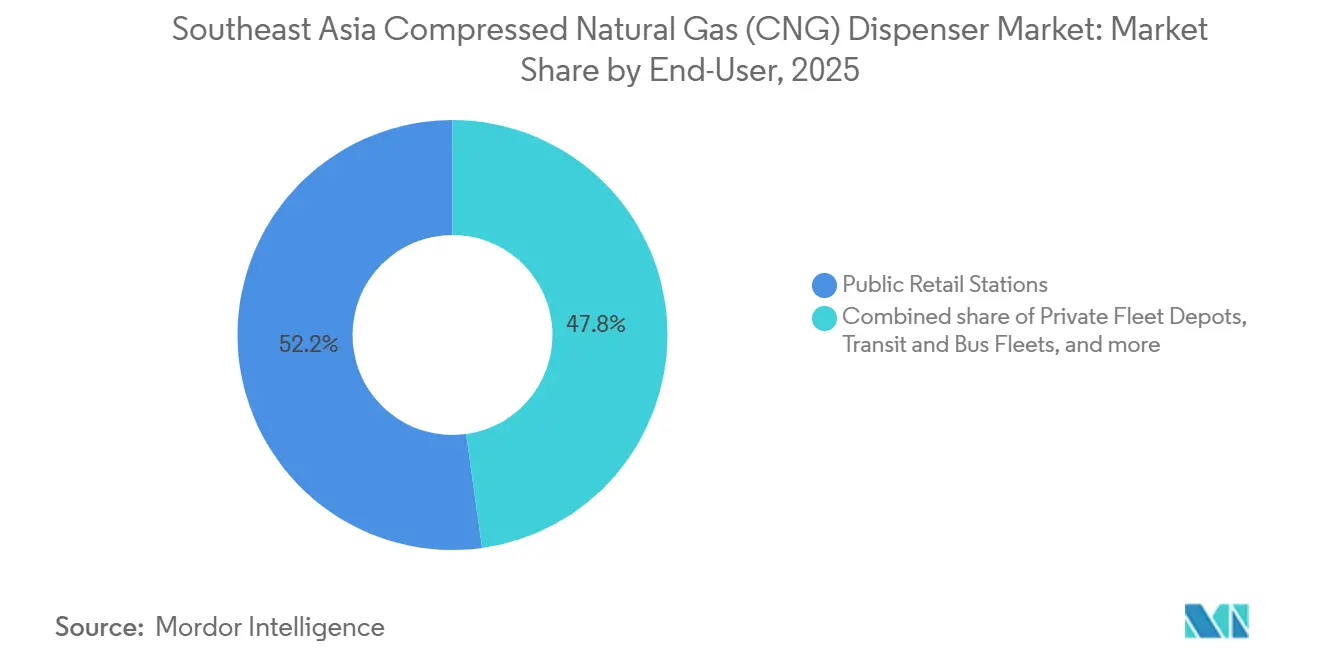

- By end user, public retail stations held a 52.2% share in 2025, whereas industrial and mining sites are forecast to register a 13.1% CAGR through 2031.

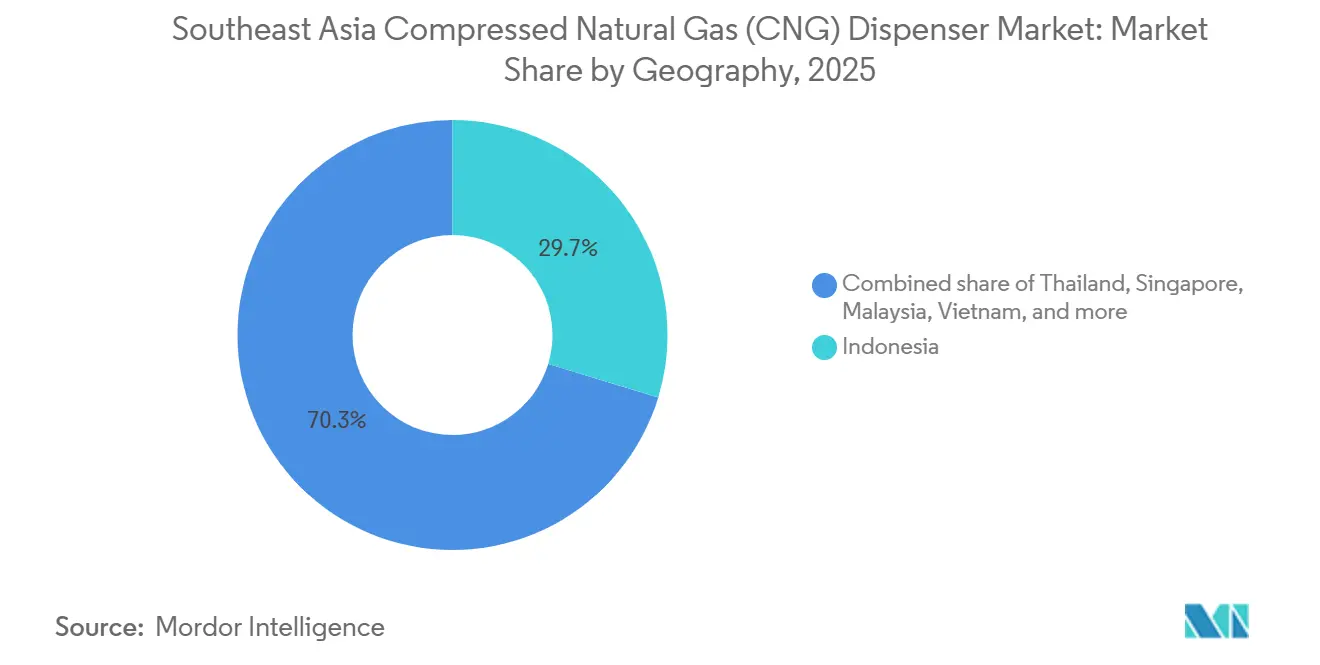

- By geography, Indonesia accounted for 29.7% of the Southeast Asia CNG dispenser market in 2025, whereas Vietnam is predicted to expand at a 13.9% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Southeast Asia Compressed Natural Gas (CNG) Dispenser Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government NGV incentives & subsidy programs | 1.8% | Indonesia, Thailand (biogas focus), Philippines | Medium term (2-4 years) |

| Lower total cost of ownership vs gasoline & diesel | 2.9% | Indonesia, Vietnam, Philippines, Rest of Southeast Asia | Long term (≥ 4 years) |

| Growing city-bus fleet conversions to CNG | 0.7% | Indonesia, Philippines (limited urban impact due to EV shift) | Short term (≤ 2 years) |

| Regional pipeline & LNG import capacity build-out | 2.1% | Global Southeast Asia, strongest in Vietnam, Indonesia, Philippines | Medium term (2-4 years) |

| Rapid biogas-to-CNG project roll-outs | 1.3% | Thailand, emerging in Indonesia and Vietnam | Long term (≥ 4 years) |

| Adoption of IoT-enabled dispensers for predictive maintenance | 1.4% | Singapore, Thailand, Indonesia (urban stations) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lower Total Cost of Ownership vs Diesel

Fleet operators in Indonesia and Vietnam have locked in five-to-seven-year CNG supply contracts that hedge against diesel swings exceeding 25% peak-to-trough in 2024, reducing depot payback periods to 3.2 years at throughputs above 150 vehicles daily. Delivered CNG costs in Java and Sumatra fell 18% after Pertamina’s pipeline extensions, cementing a 30-40% operating-cost gap versus diesel that persists even during LNG price spikes. Vietnamese manufacturers mirrored the shift as private depots grew 22% year-on-year in 2025, with operators citing maintenance and engine-life advantages that close only when utilization drops below 60%. The Southeast Asia CNG dispenser market, therefore, draws its core growth from heavy-duty fleets, not urban consumer vehicles, and is increasingly insulated from retail-price politics through direct gas-supply agreements.

Regional LNG Import Capacity Build-Out

Between 2023 and 2025, Vietnam’s Cai Mep and the Philippines’ new terminals added 8.1 million t p.a. of regasification, enabling station operators to source spot LNG cargoes when Asia-Pacific prices dip below USD 12/MMBtu. Indonesia’s state pipeline operator is pushing trunk lines into Central Java and South Sumatra, cutting virtual-pipeline truck costs. Thailand’s Eastern Economic Corridor pilots small-scale satellite LNG stations that could disrupt legacy pipeline distribution if capex falls beneath USD 2 million per site. Yet Singapore’s second terminal will not reach full output this decade, leaving operators there exposed to Malaysian pipeline imports and limiting network expansion.

Government NGV Incentives & Subsidies

Indonesia and the Philippines continue to channel fuel-tax rebates and vehicle-conversion grants toward NGV rollouts, while Thailand supports biomethane blending under its Alternative Energy Development Plan, lifting dispenser demand for units that can handle variable methane purity. Subsidy frameworks are, however, increasingly conditional on emissions outcomes, prompting operators to integrate telemetry that verifies greenhouse-gas savings. Medium-term policy visibility, therefore, underwrites purchase decisions, particularly for private-fleet depots considering multi-million-dollar commitments.

Adoption of IoT-Enabled Dispensers

Urban stations in Singapore and Bangkok retrofit dispensers with vibration, pressure, and flow sensors that feed predictive-maintenance platforms, cutting unplanned downtime by 30% and spare-parts inventories by up to 20%. Digital payment and remote shut-off features curb theft at unmanned depots, while dynamic pricing modules allow tariff changes in sync with LNG spot moves, subject to regulatory approval. Although retrofit costs run USD 8,000-12,000, high-throughput sites amortize them within two years, driving steady upgrade demand within the Southeast Asia CNG dispenser market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising competitiveness of battery-electric mobility | -2.4% | Thailand, Vietnam, Singapore (urban public transport) | Short term (≤ 2 years) |

| High upfront station CAPEX & land-leasing hurdles | -1.6% | Singapore, urban Indonesia, Malaysia, Thailand | Medium term (2-4 years) |

| Volatility of LNG spot prices impacting CNG retail price | -1.1% | Global Southeast Asia, most acute in import-dependent markets | Short term (≤ 2 years) |

| Urban zoning limits on high-pressure fueling facilities | -0.8% | Singapore, Bangkok, Ho Chi Minh City, Jakarta | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Competitiveness of Battery-Electric Mobility

Bangkok’s 2025 order for 500 battery-electric buses and Ho Chi Minh City’s December 2025 conversion of 58 CNG buses to electric cut urban CNG demand by roughly 15% year-on-year. Malaysia’s July 2025 mandate eliminating 44,383 NGVs showed that policy can abruptly shrink the addressable base. With public-transport operators chasing zero-emission targets, dispenser utilization in city cores has dipped below break-even, forcing some sites to pivot to hydrogen or LPG. Regional suppliers are therefore redirecting sales teams toward industrial and mining clients less vulnerable to electrification.

High Upfront Station CAPEX & Land-Leasing Hurdles

Permanent fast-fill stations need USD 400,000-1 million before land costs, and lease premiums in Singapore or Bangkok can boost capital outlay by 30%, stretching paybacks beyond five years when traffic projections falter. Safety permits average 12-18 months in Indonesia and Vietnam, adding financing drag. Investors thus gravitate toward multi-hose retrofits of existing footprints or mobile units that cost one-third of full builds, despite higher per-kilogram compression costs. Until zoning eases or financing models evolve, station density in secondary cities will lag underlying vehicle adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dispenser Configuration: Space-Efficient Multi-Hose Designs Take Hold

Multi-hose installations captured a rising share of the Southeast Asia CNG dispenser market as operators in Jakarta, Bangkok, and Ho Chi Minh City retrofit older dual-hose forecourts to serve three or four vehicles simultaneously. Dual-hose units still held 39.8% revenue in 2025, but multi-hose variants are projected to log a 12.8% CAGR, reflecting land constraints that make throughput per square meter critical. Single-hose equipment lingers in rural or low-traffic depots where simplicity trumps speed, although its share is ebbing as secondary cities tighten service-level rules.

Manufacturers now offer modular cabinets that add hoses in 12-month intervals, matching capex to realized demand and guarding against stranded assets. Integrating ISO 19880 compatibility prepares sites for future hydrogen blends with minimal retrofit, an insurance policy increasingly specified by risk-averse fuel retailers. Parker Hannifin and Gilbarco Veeder-Root have gained ground by bundling 24-hour parts support with software-subscription models that spread upfront costs across five-year service contracts. Chinese challengers compete on price but face perception gaps in premium urban stations, keeping competitive pressure moderate rather than destabilizing.

By Station Type: Mobile Units Underpin Remote-Site Growth

Fast-fill locations owned 55.5% of the Southeast Asia CNG dispenser market size in 2025 because retail motorists and taxi fleets demand sub-five-minute refuels. Yet mobile and portable stations are pacing future expansion with a 13.5% CAGR, answering mining and plantation operators who need relocatable infrastructure costing USD 150,000-300,000, roughly one-third of fixed-site capex. These containerized systems move within 48 hours, compress LNG or pipeline gas on site, and fuel 50-100 heavy vehicles daily in Kalimantan, Papua, and remote Vietnamese ports.

Fast-fill dominance faces headwinds from electric-bus adoption that curbs urban throughput, while mobile stations remain shielded because heavy equipment lacks viable battery alternatives. Time-fill depots, serving captive fleets overnight, are retrofitting fast-fill nozzles to improve asset utilization during daylight. Hybrid models are emerging that swing from slow-fill to burst refuels, powered by smart-compressor algorithms responding to real-time fleet needs.

By End User: Industrial & Mining Demand Outpaces Public Retail

Public retail stations held 52.2% of market revenues in 2025, but industrial and mining customers are projected to post a 13.1% CAGR to 2031 as palm-oil mills, cement kilns, and ore haulers invest in private depots that secure 30-40% fuel savings versus diesel. A 500-truck logistics fleet in northern Vietnam achieves a 3.2-year payback on a USD 800,000 installation when diesel-CNG spreads stay above USD 0.30/liter.

Mining operators prize mobile dispensers that avoid 50-80 km dead-head journeys to public sites, reclaiming two hours of equipment uptime per shift. Transit fleets, once growth engines, are retreating as Bangkok, Kuala Lumpur, and Ho Chi Minh City electrify bus systems. Taxi cooperatives and delivery vans now purchase time-fill systems that refuel overnight at lower pressure, yet even these operators retrofit fast-fill guns for midday top-ups, reflecting a broader tilt toward operational flexibility.

Geography Analysis

Indonesia led with 29.7% of Southeast Asia's CNG dispenser market share in 2025, thanks to Pertamina's pipeline reach across Java, Sumatra, and Kalimantan. Delivered CNG costs fell 18% post-2023, fueling private-depot uptake among coal mines and palm-oil refineries. ISO 16923 safety codes adopted in 2025 reinforce high-capacity, multi-hose investments that established players can afford, effectively raising entry barriers.

Vietnam is forecast to log a 13.9% CAGR, the region's fastest, as manufacturers and logistics hubs anchor private depots inside industrial parks. The Cai Mep LNG terminal, fully online by September 2025, stabilized feedstock streams and allowed operators to arbitrage spot cargoes during demand troughs. Although Ho Chi Minh City's bus electrification trims urban volumes, industrial corridors along the Red River Delta and Mekong Delta remain robust. PetroVietnam Gas intends to exit retail CNG by 2029, increasing supply-side uncertainty but also opening room for independent distributors.

Thailand shows a split profile. Bangkok's electric-bus push compresses city-station demand, yet 530 rural biogas plants channel biomethane into NGV blends under government mandates, requiring dispensers tolerant of fluctuating methane purity. Pilot trials in the Eastern Economic Corridor test unmanned fast-fill kiosks and remote monitoring that could revive the economy if reliability proves out.

Singapore's market remains small but margin-rich. Land Transport Authority zoning restricts high-pressure fueling sites to industrial parks, capping station count and steering operators toward multi-hose retrofits to squeeze throughput from scarce land. The city-state's second LNG terminal is years away, keeping gas prices tethered to Malaysian pipeline imports and tempering dispenser rollouts.

Malaysia introduced the sharpest policy shock by ordering a full NGV phase-out in July 2025, yanking roughly 15% of regional fast-fill throughput overnight. Operators are mothballing dispensers, converting sites to LPG, or considering hydrogen, underscoring how policy can nullify economic fundamentals. The Philippines and the Rest of Southeast Asia hold embryonic networks but have gained LNG capacity and could accelerate if incentive frameworks crystallize.

Competitive Landscape

Global vendors Parker Hannifin, Gilbarco Veeder-Root, Censtar Science & Technology, and Tatsuno Corporation shape a moderately concentrated field, each vying on after-sales networks and IoT feature depth rather than sticker price. Gilbarco opened a Jakarta parts hub in November 2025, slicing service calls to 24-48 hours and justifying 15-20% equipment premiums for high-utilization sites. Parker co-markets predictive-maintenance software that couples vibration analytics with warranty extensions, locking clients into multi-year subscriptions.

Regional fabricators secure cost-sensitive deals in fast-fill stations by pairing localized assembly with shorter lead times. Yet quality perceptions and limited R&D budgets hinder their share of multi-hose and IoT-rich applications. Chart Industries’ trailer-mounted compressors penetrate mining and plantation segments by offering redeployable assets at one-third of permanent-site capex, tapping a white space insulated from urban electrification.

Future differentiation revolves around ISO 19880-compliant dual-fuel (CNG-hydrogen) designs. Forward-looking operators specify such a capability to hedge against hydrogen mandates, pushing suppliers with modular component architectures to the fore. Battery-electric fleet growth in urban cores compresses dispenser order books for public stations, so vendors now prioritize industrial, mining, and remote-site prospects where electrification hurdles remain high. Competitive intensity peaks in Indonesia and Vietnam, where tender activity is brisk, while Thailand and Singapore trend toward consolidation under fuel-retail incumbents that bundle gas supply with equipment leases.

Southeast Asia Compressed Natural Gas (CNG) Dispenser Industry Leaders

Parker Hannifin Corp

FTI International Group Inc.

Censtar Science & Technology Co., Ltd.

Scheidt & Bachmann Gmbh

ComTech Energy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Ho Chi Minh City converted 58 CNG buses on routes 33 and 150 to electric buses as part of its clean transport policy. This shift reduces reliance on CNG for public transit, possibly dampening near-term demand for CNG dispensers in the city’s transport ecosystem.

- November 2024: In Malaysia, the government plans to ban CNG-powered vehicles and cease CNG sales by July 1, 2025. The decision is attributed to safety concerns and the aging condition of CNG tanks. This policy will impact approximately 44,000 natural gas vehicles (NGVs) and halt new registrations.

- March 2024: AG&P LNG has acquired a 49% stake in Vietnam’s Cai Mep LNG terminal, bolstering LNG supply infrastructure in southern Vietnam. While the focus remains on LNG, the increased availability of LNG could influence broader natural gas supply chains.

Southeast Asia Compressed Natural Gas (CNG) Dispenser Market Report Scope

A compressed natural gas (CNG) dispenser is filling equipment established in a gas station to supply compressed natural gas. It is competent in quickly refilling the empty fuel tank of vehicles. The CNG dispenser shows the temperature and pressure going into a tank and then displays how many gasoline gallon equivalents (GGEs) are going into an automobile.

The Southeast Asia compressed natural gas dispenser inverters market is segmented by dispenser configuration, station type, user, and geography. By dispenser configuration, the market is segmented into single-hose, dual-hose, and multi-hose. By station type, the market is divided into fast-fill, time-fill, and mobile/portable. By end-user, the market is divided into public retail stations, private fleet depots, transit and bus fleets, and industrial and mining sites. The report covers the market size and forecasts for Southeast Asia's compressed natural gas dispenser market across major countries in the region such as Indonesia, Thailand, Vietnam, Malaysia, and Rest of Southeast Asia. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Single-Hose |

| Dual-Hose |

| Multi-Hose |

| Fast-Fill |

| Time-Fill |

| Mobile/Portable |

| Public Retail Stations |

| Private Fleet Depots |

| Transit and Bus Fleets |

| Industrial and Mining Sites |

| Thailand |

| Singapore |

| Indonesia |

| Malaysia |

| Philippines |

| Vietnam |

| Rest of Southeast Asia |

| By Dispenser Configuration | Single-Hose |

| Dual-Hose | |

| Multi-Hose | |

| By Station Type | Fast-Fill |

| Time-Fill | |

| Mobile/Portable | |

| By End-User | Public Retail Stations |

| Private Fleet Depots | |

| Transit and Bus Fleets | |

| Industrial and Mining Sites | |

| By Geography | Thailand |

| Singapore | |

| Indonesia | |

| Malaysia | |

| Philippines | |

| Vietnam | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

What is the projected value of the Southeast Asia CNG dispenser market in 2031?

Forecasts peg the market at USD 60.33 million by 2031, at a 10.81% CAGR during 2026-2031.

Which country leads dispenser sales today?

Indonesia holds 29.7% share, buoyed by Pertamina's extensive CNG network and pipeline infrastructure advantages.

Which segment is growing fastest?

Mobile and portable stations serving mining and plantation sites are expanding at a 13.5% CAGR through 2031.

How will Malaysia's 2025 NGV phase-out affect demand?

The policy removed about 15% of regional fast-fill throughput, forcing operators to redeploy assets or exit urban retail niches.

What technology features are most sought after?

Multi-hose dispensers with IoT-enabled predictive maintenance and integrated digital payment dominate new orders.

How vulnerable is the market to electric-vehicle uptake?

Urban public-transport demand is declining, but industrial and remote heavy-duty applications still favor CNG, tempering overall impact.

Page last updated on: