Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

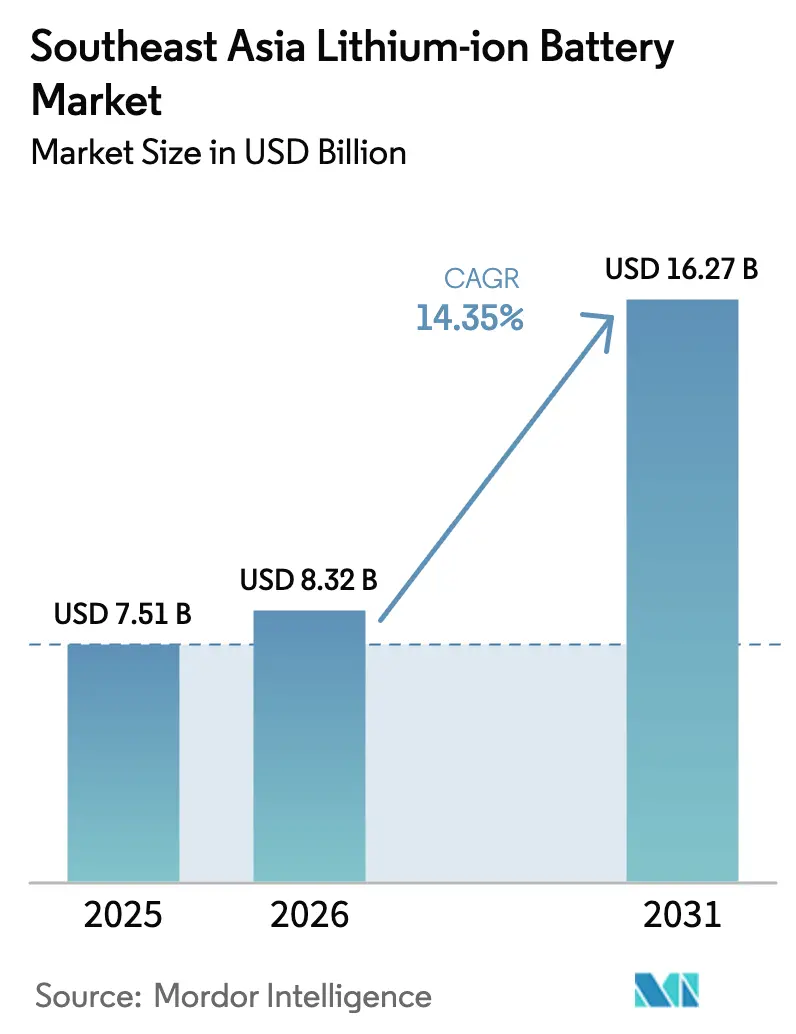

| Base Year Market Size (2025) | USD 7.51 Billion |

| Market Size (2026) | USD 8.32 Billion |

| Market Size (2031) | USD 16.27 Billion |

| Growth Rate (2026 - 2031) | 14.35% CAGR |

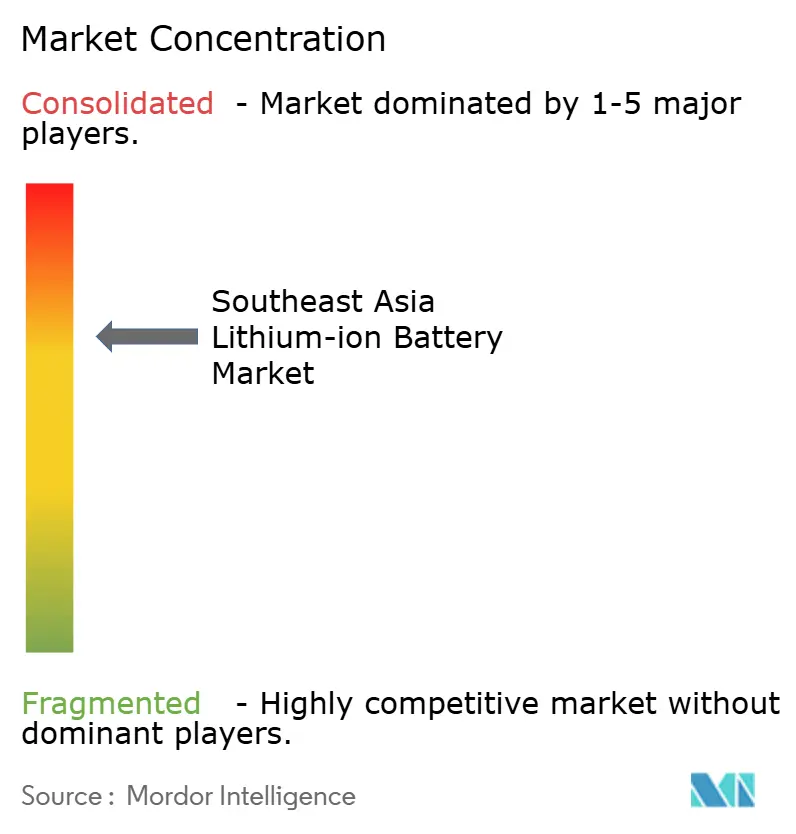

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Lithium-ion Battery Market Analysis by Mordor Intelligence

The Southeast Asia Lithium-ion Battery Market size is expected to increase from USD 7.51 billion in 2025 to USD 8.32 billion in 2026 and reach USD 16.27 billion by 2031, growing at a CAGR of 14.35% over 2026-2031.

The market size expansion reflects Indonesia’s nickel-led vertical integration, Vietnam’s established device-assembly corridor, and Thailand’s automotive retooling push.[1]Ministry of Investment Indonesia, “Indonesia EV Incentives 2024,” investindonesia.go.id Intensifying electric-vehicle (EV) incentives, sharply falling pack prices below USD 100 per kWh, and multi-billion-dollar gigafactory pipelines are compressing cell-import dependence even as lingering raw-material gaps and grid bottlenecks cap near-term stationary-storage uptake. Chinese Tier-1 suppliers leverage upstream control to offer sub-USD 100 LFP modules, forcing Korean incumbents into high-nickel niches, while Southeast Asian assemblers chase cost-sensitive marine and industrial segments. Cross-border supply chains now co-locate nickel refining, cathode synthesis, and cell assembly inside Indonesia, shaving 18% logistics cost and locking in feedstock security for high-nickel chemistries.[2]Reuters, “CATL to Invest $6 Billion in Indonesia Battery Plant,” reuters.com Regional demand skews toward large-format prismatic and pouch cells for EVs and energy-storage systems, yet 3,000-to-10,000 mAh cylindrical cells still anchor the consumer-electronics backbone in Vietnam and Thailand.

Key Report Takeaways

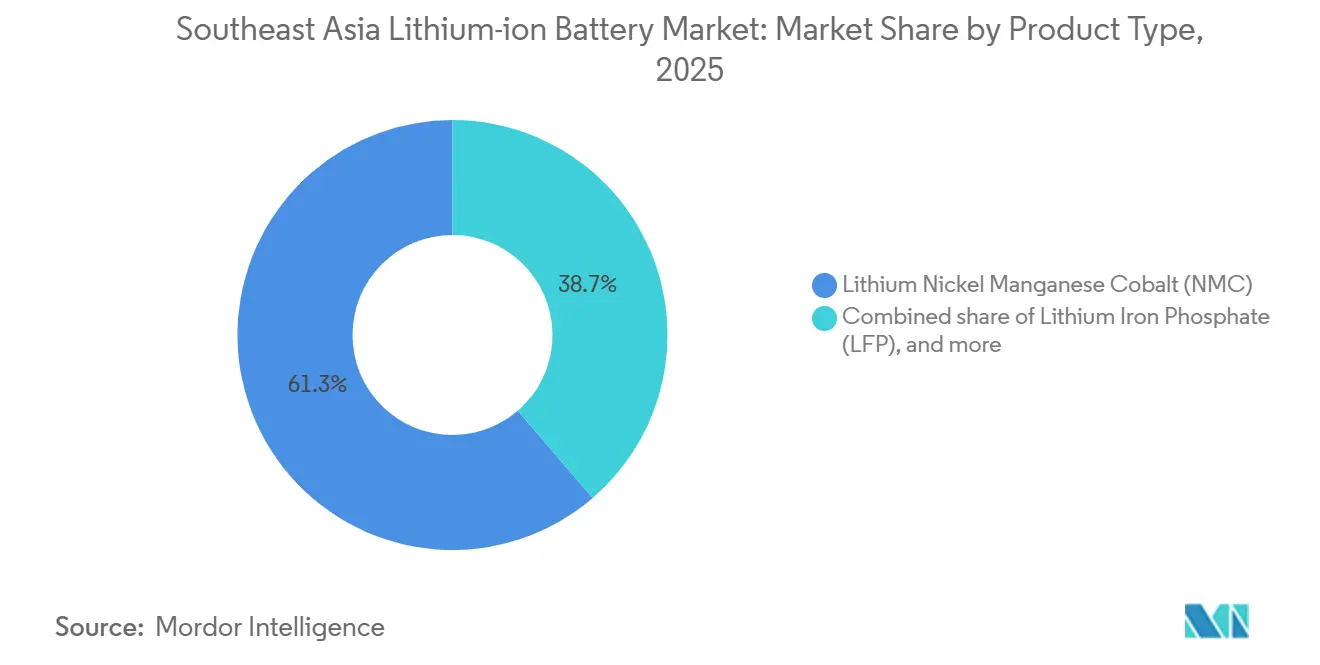

- By product type, Lithium Nickel Manganese Cobalt held 61.3% revenue share in 2025, while Lithium Iron Phosphate is projected to expand at a 38.5% CAGR through 2031.

- By form factor, prismatic cells led with 46.5% of the Southeast Asia lithium-ion battery market share in 2025; pouch architectures record the fastest CAGR at 21.1% to 2031.

- By power capacity, the 3,000-to-10,000 mAh bracket captured 38.6% share of the Southeast Asia lithium-ion battery market size in 2025, while cells above 60,000 mAh advance at a 22.7% CAGR through 2031.

- By end-use, industrial and power tools accounted for 33.3% of 2025 revenue; automotive is growing at a 28.8% CAGR to 2031 on the back of Indonesia and Thailand EV incentives.

- By geography, Vietnam dominated with a 64.1% share in 2025, whereas Indonesia posts the highest 16.2% CAGR to 2031 as nickel-to-battery complexes ramp.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Southeast Asia Lithium-ion Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid EV-adoption incentives | 3.20% | Indonesia, Thailand, Vietnam | Medium term (2-4 years) |

| Expanding consumer-electronics manufacturing | 2.10% | Vietnam, Thailand, Malaysia | Short term (≤2 years) |

| Government-backed gigafactory investments | 4.50% | Indonesia, Thailand, Vietnam | Long term (≥4 years) |

| Declining battery-pack costs | 2.80% | Region-wide, early gains in Indonesia, Vietnam | Medium term (2-4 years) |

| Indonesia nickel-laterite HPAL upsurge | 3.70% | Indonesia, spill-over to Malaysia, Philippines | Long term (≥4 years) |

| Maritime electrification of archipelagos | 1.20% | Indonesia, Philippines, Singapore | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid EV-Adoption Incentives

VAT cuts in Indonesia, registration-fee rebates in Vietnam, and Thailand’s EV 3.5 cash subsidies narrowed the total-cost-of-ownership gap against internal-combustion vehicles by up to 25 percentage points in 2025, lifting model launches across two-wheelers and compact cars.[3]Ministry of Investment Indonesia, “Indonesia EV Incentives 2024,” investindonesia.go.id Automakers now localize cell sourcing to unlock incentives, accelerating gigafactory utilization and cementing cost-competitive LFP chemistry in subsidy-capped vehicle classes.[4]Thailand Board of Investment, “EV Incentives 2024,” boi.go.th Swappable-battery fleets for last-mile delivery in Jakarta and Bangkok multiply demand for standardized 3,000-to-10,000 mAh packs. Compliance clauses that ratchet local-content thresholds every two years encourage vertical integration but expose foreign OEMs to policy shifts. The net effect is a sustained uplift in the Southeast Asia lithium-ion battery market trajectory through 2028.

Expanding Consumer-Electronics Manufacturing

Vietnam’s share of global smartphone and notebook assembly climbed to 31% in 2025 as Samsung and Apple suppliers relocated lines from China, clustering cylindrical- and prismatic-cell demand around Bac Ninh and Bac Giang. Adjacent cell plants shorten logistics lead times to under one week, lowering working capital and locking in repeat orders for 3,000-to-5,000 mAh LCO and NMC cells. Thailand’s data-center hardware lines add niche demand for high-cycle-life LTO cells in UPS modules, while compliance with IEC 62133 testing slows new SKUs by up to six weeks. Tightening labor markets raise technician wages but are offset by automation upgrades in electrode coating.

Government-Backed Gigafactory Investments

Sovereign incentives exceeding USD 15 billion between 2024 and 2026 backstop capacity build-outs such as CATL’s 50 GWh Central Java complex and Sunwoda’s 15 GWh Thai plant. Eight-year tax holidays, land grants, and R&D credits shrink payback periods below six years, convincing Tier-1 producers to co-locate precursor and cell fabrication. Import reliance on finished cells falls from 78% in 2023 to a projected 42% by 2027. Yet escalating domestic-value-add rules compel earlier backward integration into separators and electrolytes, stressing nascent local supply chains. Overall, the incentive architecture contributes the largest single lift to the Southeast Asia lithium-ion battery market CAGR.

Declining Battery-Pack Costs

Average regional pack prices slid from USD 137 per kWh in early 2024 to USD 98 per kWh by end-2025 as BYD’s module-less Blade and CATL’s Qilin platforms slashed materials and assembly overhead. At sub-USD 100, commercial-vehicle fleet operators achieve three-year paybacks, expanding large-format cell uptake above 60,000 mAh. Spot nickel-sulfate prices in Indonesia fell 22% after new HPAL lines came online, cushioning high-nickel NMC cost curves. Silicon-doped graphite anodes sourced from Malaysia deliver incremental 8% energy-density gains without new tooling, reinforcing cost declines. Lower prices raise addressable demand, driving sustained double-digit volume growth across automotive and stationary storage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported raw-material dependence | -2.30% | Vietnam, Thailand, Philippines, Malaysia | Medium term (2-4 years) |

| Safety recalls & thermal-runaway concerns | -1.10% | Region-wide, acute in Vietnam, Indonesia | Short term (≤2 years) |

| Grid-instability limiting ESS uptake | -1.80% | Thailand, Philippines, Indonesia | Medium term (2-4 years) |

| Restrictive local-content rules | -1.50% | Indonesia spill-over to Vietnam | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Imported Raw-Material Dependence

The region sources more than 95% of lithium chemicals and 87% of synthetic graphite from abroad, exposing cell makers to volatile commodity swings that eroded margins in 2025 when lithium carbonate ranged between USD 12,500 and USD 18,700/t. China’s export-licensing on graphite stretched approval cycles from two to eight weeks, delaying Malaysian cathode ramps. Cobalt price spikes following Glencore’s Mutanda force-majeure forced Vietnamese producers to hold 90-day inventories, freezing liquidity. While pilot hydroxide and separator ventures are underway, meaningful substitution is still several years out, keeping the Southeast Asia lithium-ion battery market exposed to upstream shocks.

Safety Recalls & Thermal-Runaway Concerns

Residential fires tied to uncertified e-scooter packs in Hanoi and electric-bus incidents in Jakarta sharpened regulatory scrutiny, leading Vietnam to recall 18,000 packs and impose mandatory UL 2271 certification on batteries above 500 Wh. Indonesia tightened procurement specs to include ceramic-coated separators, adding USD 80–120 per vehicle cost. Third-party abuse-testing labs remain scarce; queues run 12-16 weeks, compressing launch timelines. Heightened compliance costs and reputational risks shave more than a full percentage point off forecast growth until certification capacity catches up.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: LFP Disrupts NMC’s Chemistry Dominance

Lithium Nickel Manganese Cobalt retained 61.3% revenue in 2025, yet the Southeast Asia lithium-ion battery market size for Lithium Iron Phosphate is projected to triple at a 38.5% CAGR as automakers shift to cobalt-free packs that meet subsidy caps.[5]BYD, “BYD Blade Battery Technology 2024,” byd.com BYD’s Blade licensing to VinFast and Banpu NEXT cut module count and trimmed pack weight by 10%, shrinking per-vehicle battery cost below USD 90 per kWh. CATL’s M3P variant, produced in Indonesia from 2026, adds 15% energy density versus baseline LFP without introducing cobalt risk.

Cobalt-free chemistries collectively rise from 28.7% share in 2025 to 46.3% by 2031, propelled by Indonesia’s export levies on nickel sulfate that encourage in-country cathode production and Thailand’s preference for manganese-rich formulations. NCA remains niche at 8.2% share, reserved for Panasonic cylindrical cells used in Tesla imports, while LTO captures marine and UPS segments requiring 10,000-cycle durability. Competitive pressure revolves around cathode precursor sourcing and cell-to-pack integration efficiencies.

By Form Factor: Pouch Cells Gain Automotive Traction

Prismatic units led with 46.5% revenue in 2025 as Chinese EVs favored stackable cans for skateboard chassis, but pouch cells are growing 21.1% annually, spurred by Hyundai-LG’s Karawang line that delivers 12% lighter packs and extra driving range. The Southeast Asia lithium-ion battery market share for pouch architecture in premium sedans could top 35% by 2031 as ceramic-coated laminate reduces swelling in tropical heat.

Cylindrical formats maintain a 32.8% share, dominating power-tool and high-performance consumer devices, where automated winding yields low cost and high cycle life. Prismatic designs continue leading in utility-scale storage; CATL’s 280 Ah cans deployed in Malaysia’s 400 MWh pilot deliver 6,000 cycles at 90% efficiency. Labor-cost parity enables Thai and Vietnamese plants to mass-produce pouch and prismatic cells within 5% of cylindrical price points.

By Power Capacity: Large-Format Cells Drive EV and ESS Growth

Cells of 3,000-to-10,000 mAh held 38.6% revenue in 2025, feeding smartphones and tablets, but the Southeast Asia lithium-ion battery market size for cells above 60,000 mAh will expand at 22.7% CAGR as commercial vans, ferries, and grid-storage systems proliferate. CATL’s 280 Ah prismatic LFP cell, at 896 Wh, permits 80 kWh EV packs with only 90 cells, simplifying battery-management systems.

Mid-capacity 10,000-to-60,000 mAh cells power e-motorcycles and cordless tools; VinFast’s 48-V swappable packs completed 1.2 million swaps in 2025, validating standardized mid-capacity supply chains. Sub-3,000 mAh formats grow at a 9.2% CAGR on wearable and medical-device demand, with Murata shipping 600 million coin cells from Malaysia in 2025.

By End-Use Industry: Automotive Overtakes Industrial Tools

Industrial and power tools led with 33.3% revenue in 2025 as Makita and Bosch shipped 30 million packs from Vietnam and Thailand plants. Automotive demand now advances at 28.8% CAGR; Sunwoda’s 15 GWh Thai gigafactory and Hyundai-LG’s 10 GWh Indonesian line bring supply closer to assembly lines, cutting pack logistics by 40%. The Southeast Asia lithium-ion battery market size allocated to stationary energy storage will expand at a 19.6% CAGR once grid-code clarity unlocks utility procurements. Marine applications, though small, posted double-digit growth in Singapore and Philippine ferry retrofits.

Geography Analysis

Vietnam captured 64.1% of 2025 revenue, supported by Samsung SDI’s 12 GWh Bac Ninh plant, LG Energy Solution sub-components, and VinFast’s 2 GWh LFP line, creating a vertically integrated corridor that meets 30% local-content rules and stabilizes export flows to ASEAN and North America. Government-backed industrial parks streamline permitting, while IEC-certified labs cut product-approval cycles by 20 days compared with regional peers.

Indonesia follows with the fastest 16.2% CAGR to 2031 as CATL’s USD 6 billion Central Java complex and Hyundai-LG’s Karawang joint venture anchor 60 GWh of capacity by 2028. HPAL nickel refining onsite shaves feedstock costs and meets escalating domestic-value-add mandates, though separator films and electrolytes remain import-dependent until at least 2027.

Thailand holds a 12.3% share, leveraging decades-old automotive supply chains. Sunwoda’s Chonburi factory supplies Toyota and Honda hybrids, while Banpu NEXT-Durapower assembles 1 GWh of packs configurable for either NMC or LFP. Malaysia accounts for 8.7% on the strength of Samsung SDI’s cathode and Tokai Carbon’s anode plants, while Singapore specializes in marine and industrial ESS systems. The Philippines and other archipelagic states round out the rest, focusing on pack assembly for public-transport electrification.

Competitive Landscape

The top five producers, CATL, LG Energy Solution, Samsung SDI, BYD, and Panasonic, command 68% of regional cell capacity, yet more than 40 domestic pack integrators service localized mobility and storage niches. CATL exploits end-to-end integration, from HPAL nickel to Qilin cell-to-pack modules, capturing a 30% cost advantage in Indonesia. Korean firms concentrate on high-nickel NMC for premium EVs, filing patents for single-crystal cathodes promising 2,500-cycle durability. Local assemblers such as Banpu NEXT and LiRON LIB adapt tropicalized enclosures and salt-mist-proof thermal management, addressing marine and off-grid segments neglected by Tier-1 players.

Price pressure intensifies as EVE Energy and Sunwoda introduce sub-USD 100 per kWh LFP cells; incumbents respond by shifting mid-tier output to Malaysia and Vietnam. Certification under IEC 62619 and UL 1973 remains an entry barrier, with only eight Southeast Asian makers accredited as of end-2025. Strategic off-take pacts, such as Toyota’s 20 GWh decade-long agreement with Panasonic, lock up premium chemistries, leaving smaller OEMs to source on the spot market at higher volatility.

Southeast Asia Lithium-ion Battery Industry Leaders

BYD Co. Ltd.

LiRON LIB Power Pte Ltd

Saft Groupe SA

Samsung SDI Co., Ltd.

GS Yuasa Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: VinFast approved a USD 400 million Haiphong LFP expansion to 6 GWh by 2027.

- June 2025: Huayou Cobalt finalized a USD 9.8 billion Morowali integrated complex after LG Energy Solution’s exit.

- April 2025: LG Energy Solution withdrew from Indonesia’s Titan JV over local-content disputes, delaying the project six months.

- March 2025: Sunwoda inaugurated Thailand’s first EV-grade cell factory with 15 GWh capacity targeted for 2027.

- March 2024: Vale Indonesia commissioned the USD 2 billion Pomalaa HPAL, adding 48,000 t nickel and 3,200 t cobalt sulfate capacity.

Southeast Asia Lithium-ion Battery Market Report Scope

Lithium-ion is one of the most popular rechargeable batteries. Lithium-ion batteries power commonly used devices, like mobile phones, electric vehicles, and various other devices. Lithium-ion batteries consist of single or multiple lithium-ion cells and a protective circuit board. They are referred to as batteries once the cell, or cells, are installed inside a device with a protective circuit board.

The Southeast Asia lithium-ion battery market is segmented by product type, form factor, power capacity, end-user industry, and geography. By product type, the market is segmented into lithium cobalt oxide (LCO), lithium iron phosphate (LFP), lithium nickel manganese cobalt (NMC), lithium nickel cobalt aluminium (NCA), lithium manganese oxide (LMO), and lithium titanate (LTO). By form factor, the market is segmented into cylindrical, prismatic, and pouch. By power capacity, the market is segmented into up to 3,000 mAh, 3,000 to 10,000 mAh, 10,000 to 60,000 mAh, and above 60,000 mAh. By end-user industry, the market is segmented into automotive, consumer electronics, industrial and power tools, stationary energy storage, aerospace and defense, and marine. The report also covers the market size and forecasts for the Southeast Asia lithium-ion battery market across major countries. For each segment, the market sizing and forecasts have been done based on revenue (USD Billion) for all the above segments.

By Product Type

| Lithium Cobalt Oxide (LCO) |

| Lithium Iron Phosphate (LFP) |

| Lithium Nickel Manganese Cobalt (NMC) |

| Lithium Nickel Cobalt Aluminium (NCA) |

| Lithium Manganese Oxide (LMO) |

| Lithium Titanate (LTO) |

By Form Factor

| Cylindrical |

| Prismatic |

| Pouch |

By Power Capacity

| Up to 3,000 mAh |

| 3,000 to 10,000 mAh |

| 10,000 to 60,000 mAh |

| Above 60,000 mAh |

By End-use Industry

| Automotive (EV, HEV, PHEV) |

| Consumer Electronics |

| Industrial and Power Tools |

| Stationary Energy Storage |

| Aerospace and Defense |

| Marine |

By Geography

| Indonesia |

| Malaysia |

| Philippines |

| Singapore |

| Thailand |

| Vietnam |

| Rest of Southeast Asia |

| By Product Type | Lithium Cobalt Oxide (LCO) |

| Lithium Iron Phosphate (LFP) | |

| Lithium Nickel Manganese Cobalt (NMC) | |

| Lithium Nickel Cobalt Aluminium (NCA) | |

| Lithium Manganese Oxide (LMO) | |

| Lithium Titanate (LTO) | |

| By Form Factor | Cylindrical |

| Prismatic | |

| Pouch | |

| By Power Capacity | Up to 3,000 mAh |

| 3,000 to 10,000 mAh | |

| 10,000 to 60,000 mAh | |

| Above 60,000 mAh | |

| By End-use Industry | Automotive (EV, HEV, PHEV) |

| Consumer Electronics | |

| Industrial and Power Tools | |

| Stationary Energy Storage | |

| Aerospace and Defense | |

| Marine | |

| By Geography | Indonesia |

| Malaysia | |

| Philippines | |

| Singapore | |

| Thailand | |

| Vietnam | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

How large is the Southeast Asia lithium-ion battery market in 2026?

It stands at USD 8.32 billion and is projected to reach USD 16.27 billion by 2031.

Which chemistry is growing fastest in Southeast Asia?

Lithium Iron Phosphate is forecast to expand at a 38.5% CAGR through 2031 on cost and cobalt-free advantages.

Why is Indonesia expected to record the highest growth rate?

Integrated nickel-to-battery complexes and aggressive EV incentives push Indonesia to a 16.2% CAGR.

What is driving battery cost reduction in the region?

Blade-type cell-to-pack designs, falling nickel sulfate prices, and silicon-doped anodes pushed pack prices below USD 100 per kWh by 2025.

Which form factor is gaining favor among automakers?

Pouch cells, thanks to weight savings and flexible design, are growing 21.1% annually and penetrating premium EV segments.

What are the main obstacles to stationary energy storage deployment?

Grid instability, insufficient ancillary-service tariffs, and costly compliance requirements slow large-scale ESS adoption.

Page last updated on: