Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 6.52 Billion |

| Market Size (2026) | USD 7.07 Billion |

| Market Size (2031) | USD 11.20 Billion |

| Growth Rate (2026 - 2031) | 9.63% CAGR |

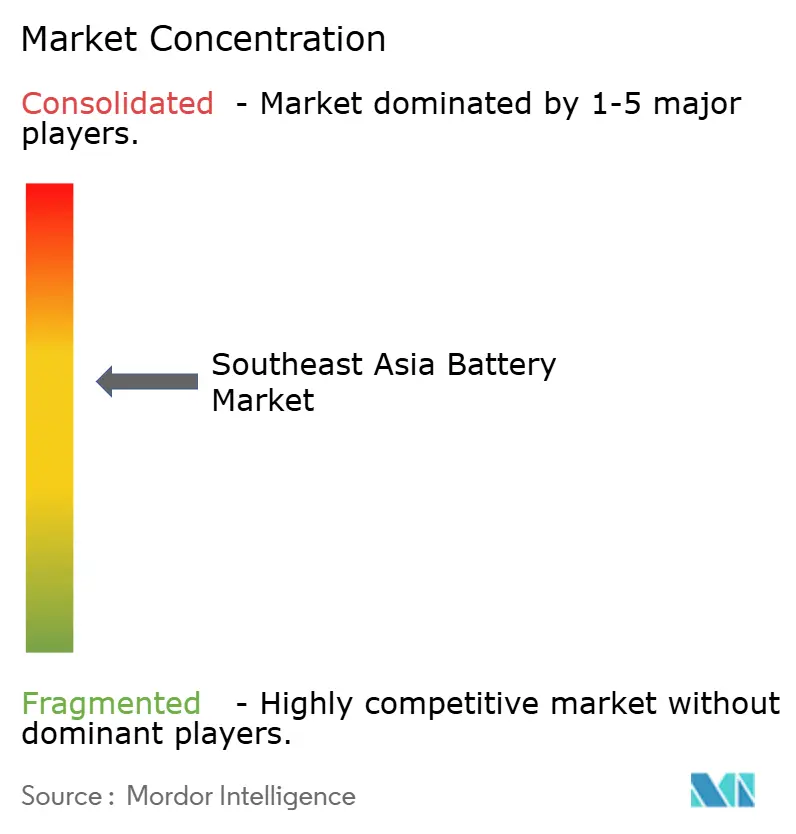

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Battery Market Analysis by Mordor Intelligence

The Southeast Asia Battery Market size is expected to grow from USD 6.52 billion in 2025 to USD 7.07 billion in 2026 and is forecast to reach USD 11.20 billion by 2031 at 9.63% CAGR over 2026-2031.

Rising electric-vehicle mandates, fast-tracking of 5G telecom towers, and utility-scale solar-plus-storage procurements are lifting lithium-ion demand while squeezing legacy lead-acid volumes. Indonesia’s nickel laterite resources are lowering precursor costs, Thailand’s automotive supply chain is attracting cell and pack investments, and Vietnam’s portable-electronics hub is anchoring pouch-cell manufacturing. Joint ventures between Chinese cell makers and ASEAN conglomerates are creating local capacity that buffers tariff exposure. Meanwhile, stricter hazmat shipping rules are nudging producers to colocate cell, module, and pack lines inside the region to curb logistics risk.

Key Report Takeaways

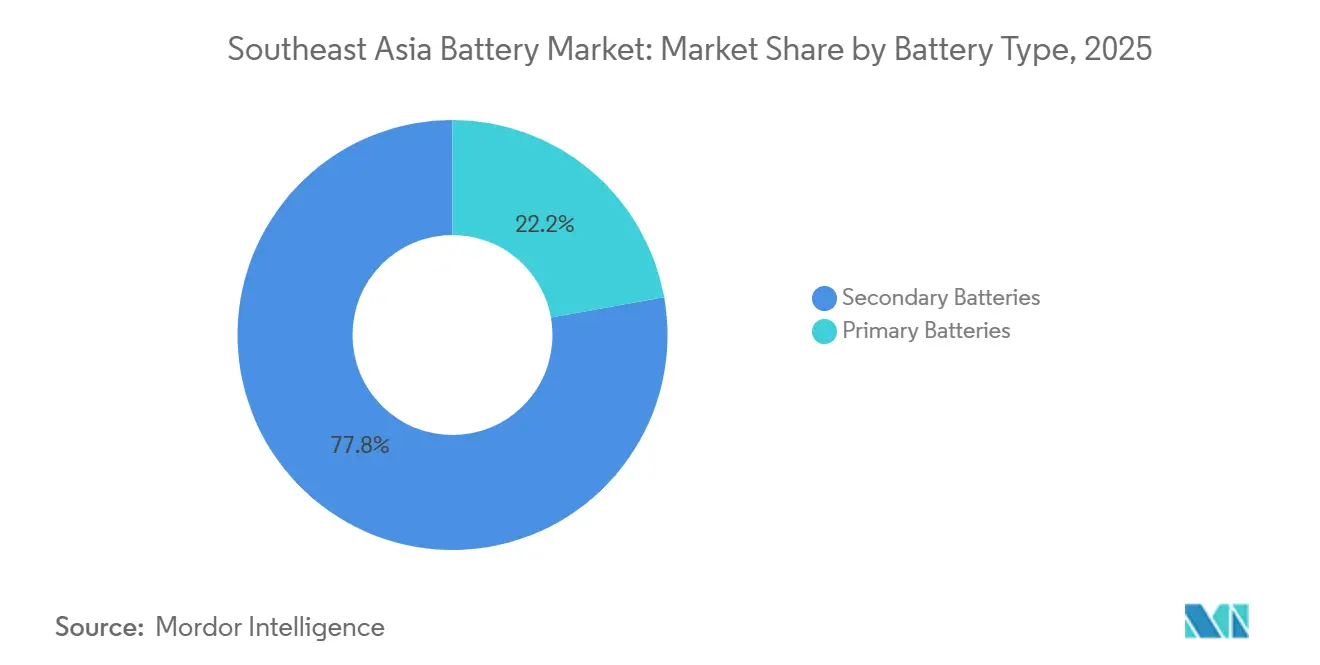

- By battery type, secondary rechargeable batteries captured 77.8% of regional revenue in 2025 and are advancing at a 10.5% CAGR through 2031.

- By technology, lead-acid retained 49.1% of the 2025 value, but solid-state batteries are projected to expand at a 34.8% CAGR into 2031 as oxide- and sulfide-based prototypes reach pilot scale.

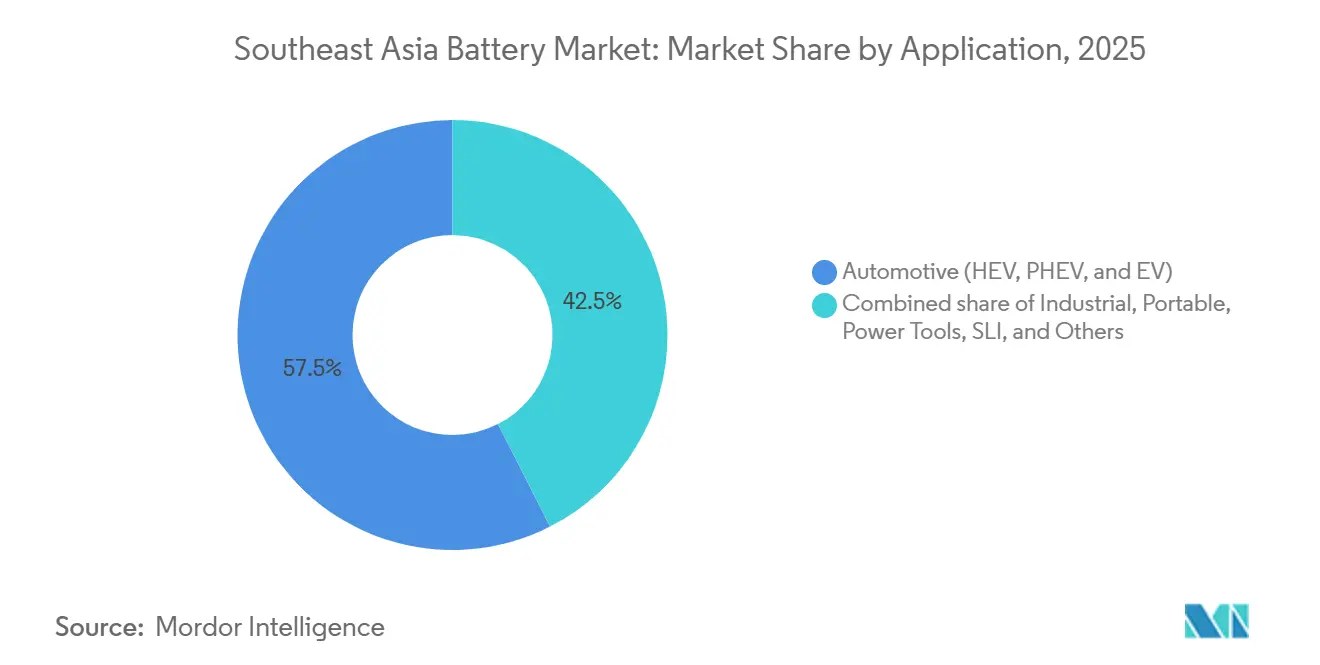

- By application, automotive traction batteries held a 57.5% share of the Southeast Asia battery market size in 2025 and are accelerating at a 15.7% CAGR to 2031, reflecting generous EV incentives in Indonesia and Thailand.

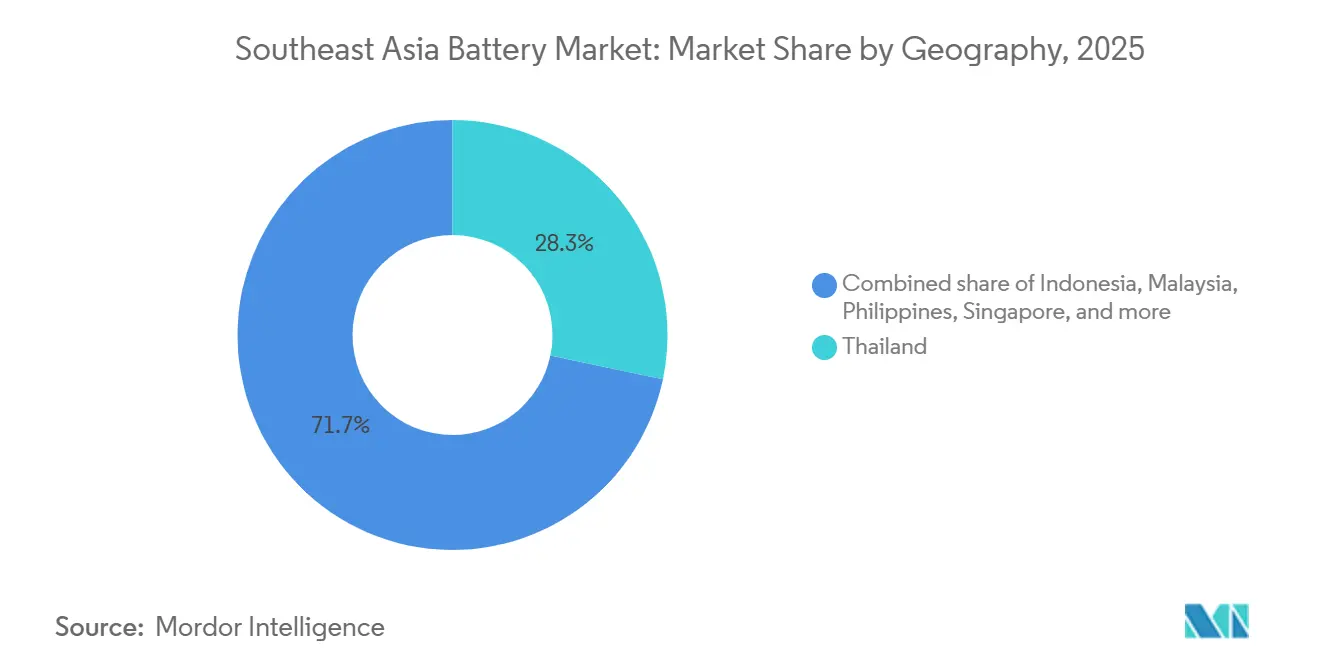

- By geography, Thailand led with 28.3% of Southeast Asia's battery market share in 2025, while Indonesia is on track for a 12.9% CAGR thanks to vertically integrated nickel-to-cathode complexes.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Southeast Asia Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid EV-adoption incentives across ASEAN | +2.8% | Indonesia, Thailand, Vietnam, Malaysia, Philippines | Medium term (2-4 years) |

| Telecom 5G tower back-up demand spike | +1.2% | Thailand, Vietnam, Indonesia urban centers | Short term (≤ 2 years) |

| Grid-scale solar + storage roll-outs | +1.9% | Malaysia, Thailand, Indonesia | Long term (≥ 4 years) |

| Regional supply-chain relocation from China | +2.1% | Indonesia, Thailand, Vietnam | Medium term (2-4 years) |

| Battery-swapping for 2-W & 3-W e-mobility | +0.9% | Vietnam, Indonesia, Thailand | Short term (≤ 2 years) |

| Nickel-laterite mining for precursor sufficiency | +1.5% | Indonesia, Philippines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid EV-Adoption Incentives Across ASEAN

Fiscal packages are compressing ownership costs for battery electric vehicles and pushing automakers to source cells locally. Indonesia waived luxury-goods tax on EVs priced below IDR 1.5 billion in 2024, prompting Hyundai and BYD to boost local assembly.[1]“Indonesia EV Incentives Boost Local Assembly,” Reuters, reuters.com Thailand extended its EV 3.5 scheme through 2027 and ties eight-year corporate income-tax holidays to domestic pack production.[2]Thailand Board of Investment, “EV 3.5 Incentive Scheme,” boi.go.th Vietnam’s Decision 876 sets a 5% penetration target by 2030, front-loading charging-infrastructure subsidies that cut the total cost of ownership by about 15%.[3]VnExpress, “Decision 876 on EV Penetration,” vnexpress.net Malaysia’s Low Carbon Mobility Blueprint exempts EVs from excise duty until 2025, though deployment trails Indonesia and Thailand. Policymakers are thus shortening supply chains and drawing cell, module, and pack lines closer to end-markets.

Telecom 5G Tower Back-Up Demand Spike

Fifth-generation base stations draw two to three times more energy than 4G, motivating operators to swap diesel gensets for lithium-ion cabinets. Smart Axiata retrofitted 1,200 Cambodian towers in 2024, cutting fuel spend by 60% and abating 8,000 t of CO₂ annually.[4]Smart Axiata, “Lithium-Ion Tower Backup Deployment,” smart.com.kh Thailand’s AIS and True Corp are piloting solar-battery hybrids at rural sites to counter erratic grid service. EnerSys launched cabinets that hold cell temperature under 35 °C to curb capacity fade in tropical heat. Regulatory uptime mandates in Singapore obligate telecoms to maintain 99.9% service, effectively requiring high-reliability storage at key nodes. Faster recharge, smaller footprints, and lower maintenance costs are driving lithium-ion adoption ahead of automotive timelines in this niche.

Grid-Scale Solar+Storage Roll-Outs

Utilities must firm intermittent solar and wind generation to meet dispatch commitments. Malaysia’s Tenaga Nasional awarded 4 GW of solar plus 5.12 GWh of lithium-ion storage in 2024, with delivery milestones set between 2026 and 2028. Thailand’s Gulf Energy brought a 200 MW PV farm coupled with 100 MWh of LFP storage online in 2025. Singapore’s Sembcorp commissioned a 285 MWh system on Jurong Island in 2024 to provide frequency regulation for industrial clients. Indonesia’s PLN signed 500 MW of solar-storage PPAs, but tariff renegotiations in 2025 delayed financial close for multiple developers. Flow and sodium-sulfur batteries are emerging for six-hour discharge, yet lithium-ion retains cost leadership for projects needing four hours or less.

Regional Supply-Chain Relocation From China

Trade friction and nickel proximity are steering cell makers toward ASEAN. CATL’s USD 5.97 billion Sorowako complex will deliver 50 GWh annually by 2027 and is colocated with PT Vale Indonesia smelters to shave 12% off precursor logistics cost. LG Energy Solution’s USD 9 billion Karawang facility started shipping cells in 2025 and targets 30 GWh by 2026. Gotion High-Tech partnered with PT Trimegah Bangun Persada for 20 GWh of LFP cells plus cathode precursor lines. Panasonic doubled automotive-cell capacity in Thailand’s Chonburi province to serve Japanese OEMs assembling hybrids locally. Relocation spans upstream cathodes and anodes, not just final assembly, shrinking lead times for ASEAN vehicle plants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Li-ion capex versus legacy chemistries | -1.4% | Indonesia, Thailand, Philippines manufacturing zones | Medium term (2-4 years) |

| Under-developed recycling ecosystem | -0.8% | ASEAN-wide, acute in Indonesia, Philippines, Myanmar | Long term (≥ 4 years) |

| Bilateral PPA policy uncertainty | -0.6% | Indonesia, Philippines, Malaysia grid projects | Medium term (2-4 years) |

| Stricter haz-mat shipping rules | -0.5% | ASEAN port hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Li-Ion Capex Versus Legacy Chemistries

Lithium-ion gigafactories cost USD 100 million to USD 150 million per GWh, versus USD 20 million to USD 40 million for lead-acid lines. This gap explains why regional firms such as Malaysia’s Favelle Favco and Indonesia’s PT Nipress keep expanding lead-acid capacity to serve price-sensitive commercial-vehicle and stationary-backup buyers. Indonesia and Thailand offer multi-year tax holidays and subsidized land, yet world-class plants still need USD 5 billion to USD 10 billion, forcing local conglomerates into foreign joint ventures. Solid-state and flow-battery formats carry even steeper upfront costs because they require specialty production tools and unproven yields, limiting early adoption to large incumbents with deep R&D budgets.

Under-Developed Recycling Ecosystem

End-of-life collection trails production, creating environmental liabilities and forfeiting cobalt and nickel recovery. Indonesia enacted an extended-producer-responsibility rule in 2024 that mandates 50% collection by 2027, but enforcement mechanisms remain weak. Singapore’s Durapower opened a hydrometallurgical plant able to process 3,000 t per year at 95% metal-recovery rates, yet regional demand may top 50,000 t by 2030. Thailand’s draft regulation funds recycling through producer levies but exempts imported cells, diluting the impact. The Philippines exports scrap packs to China or consigns them to landfills, raising groundwater-contamination risks. Absent local recycling loops, cell makers are exposed to spot nickel price spikes like those seen under Indonesia’s 2024 export curbs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Rechargeable Dominance Accelerates

Secondary batteries accounted for 77.8% of 2025 revenue, with the segment tracking a 10.5% CAGR on the back of electric-vehicle, grid-storage, and telecom installations that require thousands of charge cycles. Primary formats remain in remote sensors and emergency gear, but are losing ground as microgrid deployment spreads. Vietnam’s battery-swapping mesh, led by VinFast, underscores how recurring-use designs stretch pack utilization and drive throughput in the Southeast Asia battery market. Regulatory proposals such as Singapore’s planned levy on single-use cells further tip the balance toward rechargeables.

Solid-state prototypes from Samsung SDI and Toyota exceed 500 Wh per kg and target 3,000-cycle life, signaling a medium-term bridge to even higher rechargeable share. Manufacturing yields below 80% and triple the cost of lithium-ion confines early deployments to premium EVs and aerospace. Nonetheless, longer range and thermal stability make solid-state a credible disruptor of the Southeast Asia battery market over the next decade.

By Technology: Lead-Acid Incumbency Meets Solid-State Disruption

Lead-acid retained 49.1% of the 2025 value, upheld by automotive starting-lighting-ignition, forklifts, and telecom backup, where price trumps energy density. Lithium-ion is gaining traction in grid and portable electronics, though margin pressure from Chinese oversupply is squeezing cell makers. CATL’s average selling price per kWh fell 18% in 2024, illustrating deflationary forces in the Southeast Asia battery market. Nickel-metal hydride persists in Toyota’s mild-hybrid lines assembled in Thailand, while nickel-cadmium contracts because of cadmium-toxicity rules.

Solid-state cells are forecast to grow at a 34.8% CAGR through 2031. QuantumScape, Toyota, and Samsung SDI are closing in on pilot production that can unlock higher energy density and remove liquid-electrolyte fire risk. Sodium-sulfur and vanadium-flow variants are carving space in six-hour grid-support roles where lithium-ion economics degrade beyond four-hour discharge. NGK’s 14 MWh sodium-sulfur system in Thailand highlights growing technology pluralism.

By Application: Automotive Traction Batteries Outpace Industrial Segments

Automotive traction packs held 57.5% of 2025 revenue and are running at a 15.7% CAGR toward 2031. Indonesia’s luxury-tax waiver on EVs under IDR 1.5 billion triggered sales spikes of LFP-based compact SUVs from Wuling and BYD, funneling cell demand into new plants in Java and Sulawesi. Thailand links tax holidays to local pack content, pushing GS Yuasa, Panasonic, and Clarios to expand in the Eastern Economic Corridor. Forklifts, data-center backup, and telecom sites anchor industrial demand but grow at a mid-single-digit pace, constrained by longer replacement windows.

Portable batteries for smartphones and laptops mature in line with GDP growth, yet value is shifting toward automotive-grade pouch cells. Samsung SDI retooled its Bac Ninh facility in 2024 to allocate more lines to traction formats, reflecting the profitability pivot within the Southeast Asia battery industry. Power-tool makers such as Bosch and Makita phase out nickel-cadmium for lithium-ion to lower weight and extend runtime.

Geography Analysis

Thailand led the Southeast Asia battery market with 28.3% revenue in 2025, drawing on a deep automotive cluster and Eastern Economic Corridor incentives that streamline permitting and fund shared infrastructure. Clarios and GS Yuasa upgraded Rayong plants in 2024, and Panasonic doubled capacity to support hybrid models from Toyota and Honda. The country also hosts early pilots of sodium-sulfur and flow storage for industrial customers seeking six-hour discharge profiles.

Indonesia is on a 12.9% CAGR trajectory, underpinned by nickel-driven vertical integration. CATL, LG Energy Solution, and Gotion High-Tech are commissioning 100 GWh of combined cell capacity between 2025 and 2027, positioning the nation as a hub that ships cathodes and finished cells to ASEAN vehicle plants and Australia grid projects. Government bans on raw ore exports lock upstream value-addition inside the archipelago, further magnetizing investment.

Vietnam leverages its electronics-export engine; Samsung and LG assemble pouch cells for Galaxy devices and consumer laptops while expanding into automotive grades. The country’s battery-swapping mandate underpins mass two-wheeler electrification, lifting domestic cell pull. Malaysia pitches itself as a storage hub; Gentari’s 1 GWh system in Bukit Jalil entered service in 2024, offering capacity-reserve services under long-term offtake. Singapore focuses on R&D and recycling due to land limits, with Durapower’s hydromet facility processing end-of-life packs from across ASEAN. The Philippines remains supply-constrained, although Meralco’s 100 MWh Luzon installation signals growing utility appetite for grid-support storage.

Competitive Landscape

The Southeast Asia battery market is moderately concentrated. CATL, LG Energy Solution, Samsung SDI, and BYD together command roughly 55% of regional lithium-ion capacity, while Clarios, GS Yuasa, and Exide dominate lead-acid aftermarket channels. Chinese cell makers mitigate tariff exposure by pairing with local conglomerates; CATL’s tie-up with PT Vale and Gotion’s partnership with PT Trimegah illustrate vertical-integration plays that secure nickel and cut logistics drag. Korean firms lean on OEM relationships; LG Energy Solution supplies Hyundai’s Indonesian factory, and Samsung SDI feeds Vietnam’s electronics assembly.

Technology rivalry is intensifying around solid-state batteries. Samsung SDI ran oxide-based pilot lines in 2024, and Toyota targets a 2027 sulfide cell launch. Patent filings under IEC TC 21 rose 34% in 2024, with Chinese entities submitting 62% of lithium-ion safety and solid-electrolyte applications. Smaller entrants such as Narada Power and EVE Energy carve niches in battery-swapping and long-duration storage through localized service teams and tailored products. Overcapacity in Chinese plants is compressing margins, pushing Southeast Asian producers to compete on delivery speed and after-sales service rather than unit price.

Southeast Asia Battery Industry Leaders

LG Energy Solution

Panasonic Holdings Corp.

Samsung SDI Co. Ltd.

BYD Co. Ltd.

GS Yuasa Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Tenaga Nasional awarded 4 GW of solar and 5.12 GWh of storage in Peninsular Malaysia with tariffs fixed at MYR 0.27 per kWh.

- October 2025: Samsung SDI confirmed a Bac Ninh expansion to 8 GWh by mid-2025 and introduced a pilot line for solid-state prototypes.

- July 2025: CATL inked a USD 5.97 billion deal with PT Vale Indonesia for a 50 GWh cell plant in Sorowako, scheduled for completion in 2027.

- October 2024: Clarios finished a USD 150 million expansion of its Rayong, Thailand, lead-acid facility, raising output to 12 million units and adding closed-loop recycling that recovers 98% of materials.

- July 2024: LG Energy Solution began commercial shipments from its USD 9 billion Karawang complex in West Java, Indonesia, starting with 10 GWh of annual capacity and targeting 30 GWh by late 2026.

Southeast Asia Battery Market Report Scope

A battery is an energy source that converts chemical energy into electrical energy, consisting of one or two electrochemical cells, using a redox reaction.

The Southeast Asian battery market is segmented by battery type, technology, application, and geography. By battery type, the market is segmented into Primary Batteries and Secondary Batteries. By technology, the market is divided into Lead-acid, Li-ion, Nickel-metal hydride, Nickel-cadmium, Sodium-sulfur, Solid-state, Flow Battery, and Emerging chemistries. By Application, the market is divided into Automotive (HEV, PHEV, and EV), Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.), Portable (Consumer Electronics, etc.), Power Tools, SLI, and Other Applications. The report also covers the market size and forecasts for the market across major countries in the region. For each segment, market sizing and forecasts have been done based on revenue (USD billion).

By Battery Type

| Primary Batteries |

| Secondary Batteries |

By Technology

| Lead-acid |

| Li-ion |

| Nickel-metal hydride |

| Nickel-cadmium |

| Sodium-sulfur |

| Solid-state |

| Flow Battery |

| Emerging chemistries |

By Application

| Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) |

| Portable (Consumer Electronics, etc.) |

| Power Tools |

| SLI |

| Other Applications |

By Geography

| Indonesia |

| Malaysia |

| Philippines |

| Singapore |

| Thailand |

| Vietnam |

| Myanmar |

| Rest of Southeast Asia |

| By Battery Type | Primary Batteries |

| Secondary Batteries | |

| By Technology | Lead-acid |

| Li-ion | |

| Nickel-metal hydride | |

| Nickel-cadmium | |

| Sodium-sulfur | |

| Solid-state | |

| Flow Battery | |

| Emerging chemistries | |

| By Application | Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) | |

| Portable (Consumer Electronics, etc.) | |

| Power Tools | |

| SLI | |

| Other Applications | |

| By Geography | Indonesia |

| Malaysia | |

| Philippines | |

| Singapore | |

| Thailand | |

| Vietnam | |

| Myanmar | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

What is the projected value of the Southeast Asia battery market in 2031?

The market is forecast to reach USD 11.20 billion by 2031.

Which chemistry is growing the fastest in the region?

Solid-state batteries are projected to post a 34.8% CAGR through 2031 as oxide- and sulfide-based cells exit pilot lines.

Why are Indonesia and Thailand pivotal locations for battery investment?

Indonesia offers nickel reserves and vertical-integration incentives, while Thailand supplies established automotive chains and generous tax holidays.

How are telecom operators addressing higher 5G power needs?

Operators are replacing diesel gensets with lithium-ion cabinets that recharge quickly and lower operating costs.

What is the main hurdle to lithium-ion plant expansion in ASEAN?

Capital expenditure of USD 100 million to USD 150 million per GWh is deterring local firms without foreign joint-venture partners.

Where is Southeast Asia's first large-scale lithium-ion recycling plant located?

Durapower opened a 3,000 t facility in Singapore in 2024.

Page last updated on: