Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

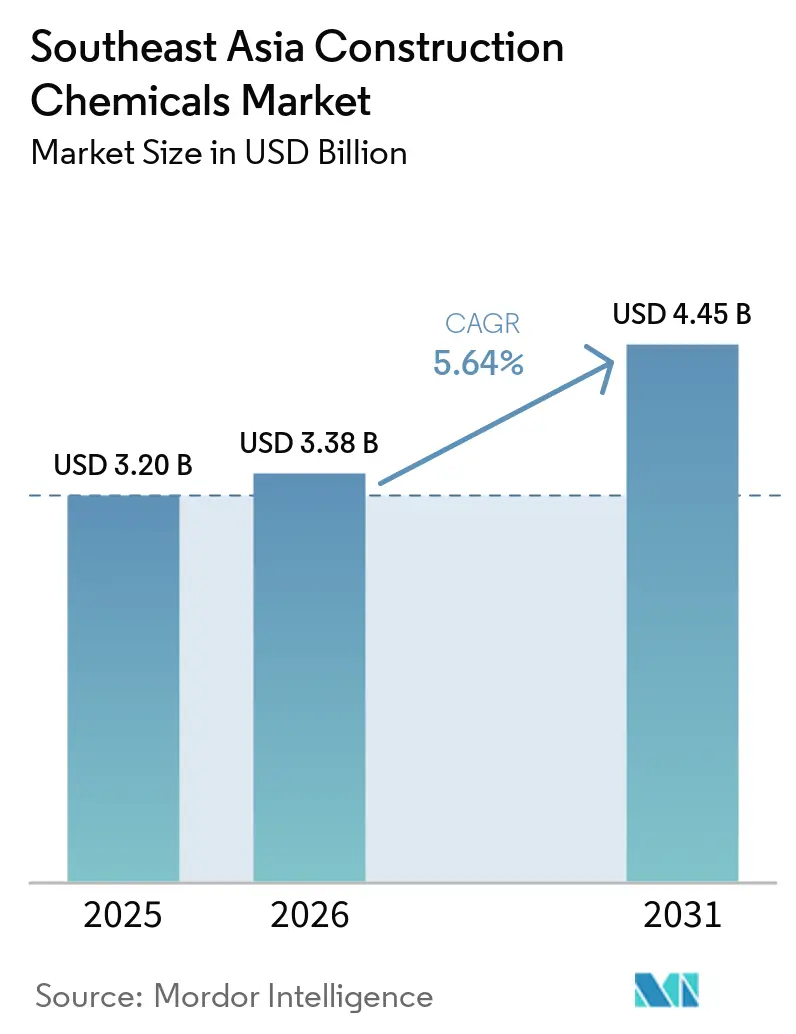

| Base Year Market Size (2025) | USD 3.20 Billion |

| Market Size (2026) | USD 3.38 Billion |

| Market Size (2031) | USD 4.45 Billion |

| Growth Rate (2026 - 2031) | 5.64% CAGR |

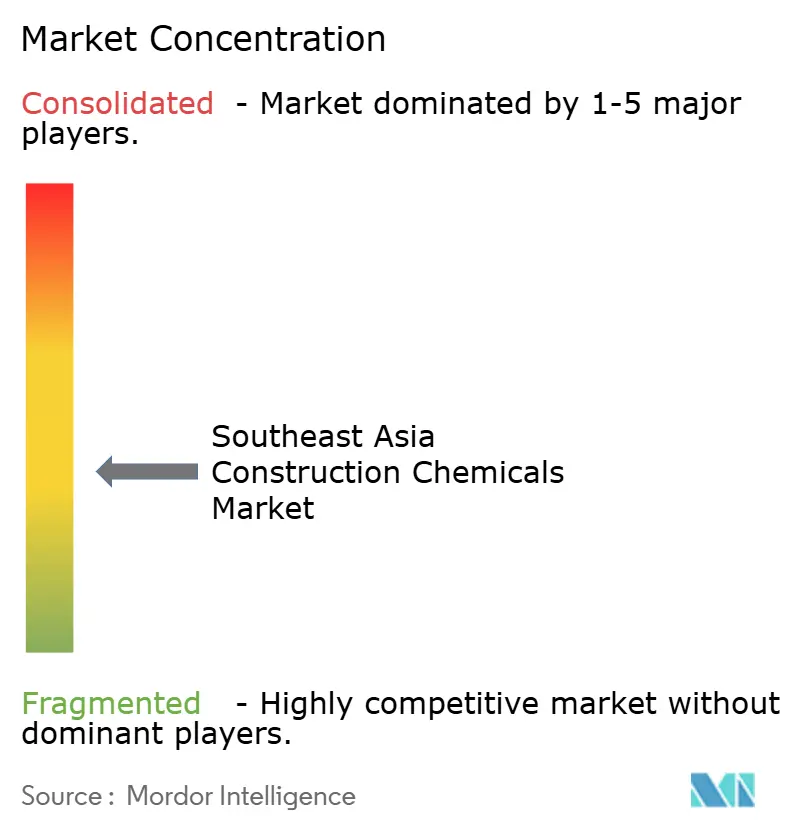

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Construction Chemicals Market Analysis by Mordor Intelligence

The Southeast Asia construction chemicals market size was valued at USD 3.20 billion in 2025 and estimated to grow from USD 3.38 billion in 2026 to reach USD 4.45 billion by 2031, at a CAGR of 5.64% during the forecast period (2026-2031). A sizable public-sector infrastructure pipeline, rapid urbanization, and stricter performance standards are increasing demand for advanced admixtures, waterproofing agents, and protective coatings throughout the region. Elevated public spending on transport corridors, housing, and industrial estates is amplifying the volume of concrete placed each year, while swelling renovation needs for aging bridges, ports, and buildings expand opportunities for high-performance repair products. Parallel regulatory pressure, led by Singapore’s 2025 restrictions on persistent chemicals, is accelerating the switch toward low-VOC and bio-based formulations. Intensifying consolidation among global suppliers, exemplified by Saint-Gobain’s purchase of FOSROC, is raising the competitive bar on both innovation and service capability across the Southeast Asia construction chemicals market.

Key Report Takeaways

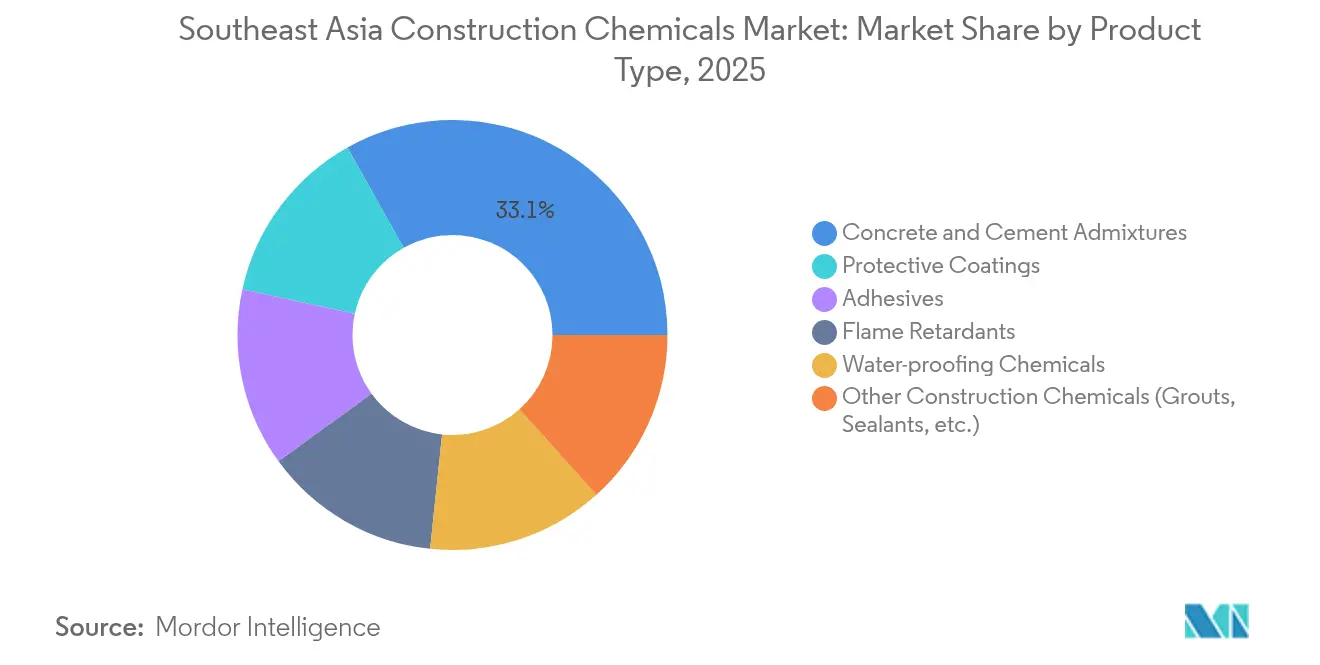

- By product type, concrete and cement admixtures led with 33.12% of Southeast Asia construction chemicals market share in 2025, while protective coatings are projected to expand at a 6.66% CAGR through 2031.

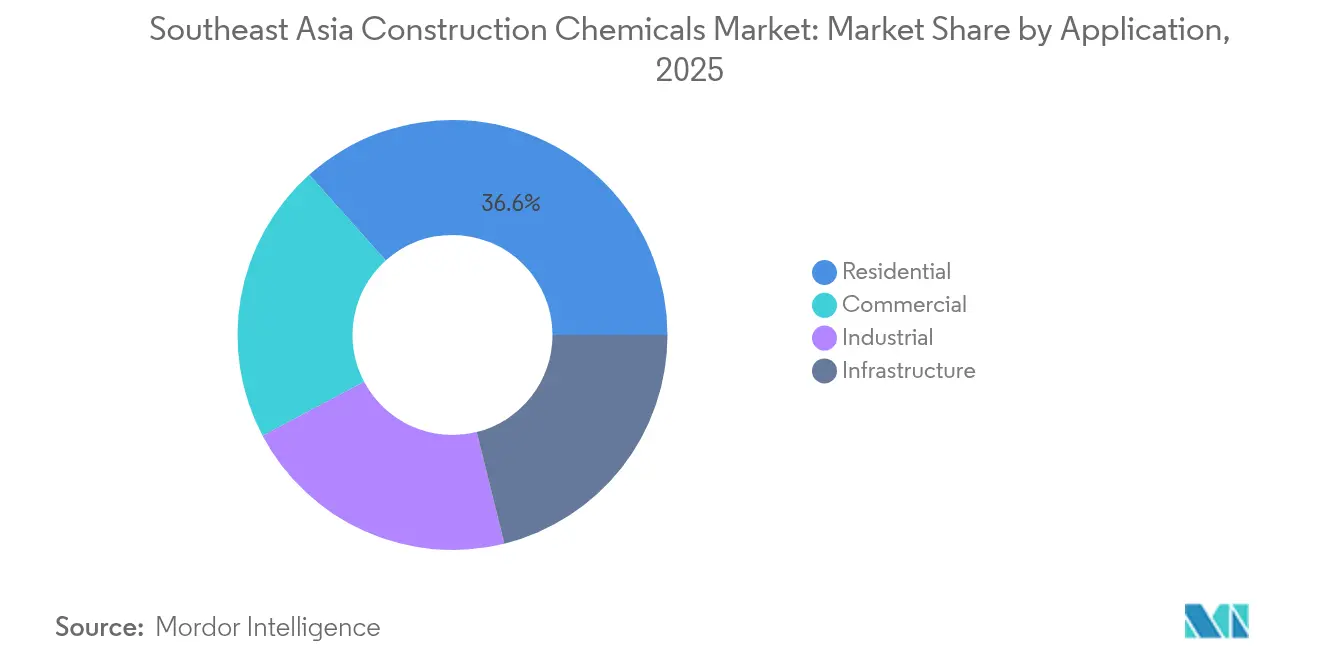

- By application, the residential segment commanded 36.62% share of the Southeast Asia construction chemicals market size in 2025 and is advancing at a 6.70% CAGR through 2031.

- By function, strength enhancement captured 35.80% of the Southeast Asia construction chemicals market size in 2025 and is projected to grow at a 6.79% CAGR to 2031.

- By geography, Indonesia held 35.20% of Southeast Asia construction chemicals market share in 2025 and is forecast to post a 6.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Southeast Asia Construction Chemicals Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Public-Sector Infrastructure Investments | +1.80% | Indonesia, Vietnam, Thailand, spillover to Philippines, Malaysia | Medium term (2–4 years) |

| Booming Prefabricated and Modular Building Adoption | +1.20% | Malaysia, Singapore, expanding to Indonesia, Vietnam | Long term (≥ 4 years) |

| Increased Adoption of Innovative Construction Procedures | +0.90% | Singapore, Malaysia, gradual uptake region-wide | Medium term (2–4 years) |

| Rising Demand for Water-Based, Low-VOC Construction Solutions | +0.70% | Singapore, Vietnam, region-wide | Short term (≤ 2 years) |

| Growing Renovation Requirements for Aging Infrastructure | +0.60% | Thailand, Philippines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Public-sector Infrastructure Investments

Governments are boosting construction budgets to relieve capacity bottlenecks and spur economic growth. Indonesia construction activity is accelerating as the country earmarks IDR 423.3 trillion for 2024 infrastructure work, while its USD 35 billion New Capital City is expected to consume 2 million tons of cement, stimulating demand for concrete admixtures and protective coatings. Vietnam began 13 transport projects worth USD 1.2 billion in 2024, raising requirements for corrosion-resistant coatings and high-early-strength grouts[1]U.S. Department of Commerce, “Vietnam Transport Projects 2024,” trade.gov . Thailand’s Eastern Economic Corridor megaprojects and the Philippines’ drive to narrow a 10 million-unit housing backlog reinforce a steady call for waterproofing and sealants. Malaysia’s 14.6% construction growth in H1 2024 further illustrates how fiscal outlays translate into higher consumption of admixture and repair compounds.

Booming Prefabricated and Modular Building Adoption

Industrialized Building Systems shorten schedules and cut labor hours, reshaping chemical specifications. Gamuda IBS has erected 50-story towers in two-thirds of the traditional timelines in Malaysia, spurring the uptake of fast-setting grouts and connection adhesives. Indonesian precast concrete delivers 5–10% cost savings and enhanced seismic resilience, driving interest in flexible jointing compounds. Singapore’s Housing Development Board has embedded polymer concrete in more than 700,000 units, guiding performance benchmarks across the Southeast Asia construction chemicals market[2]Advanced Materials Research, “Polymer Concrete Applications in Singapore Housing,” scientific.net . Vietnam’s rising foreign investment inflows into manufacturing fuel modular construction that depends on specialty sealants for off-site assembly.

Rising Demand for Water-based, Low-VOC Construction Solutions

Environmental stewardship is gaining legal teeth. Singapore’s National Environmental Agency will bar long-chain perfluorocarboxylic acids and medium-chain chlorinated paraffins from August 2025, nudging suppliers toward water-based coatings. Vietnam’s revised Chemical Law incentivizes low-VOC products, prompting local plants to retool resin lines. Malaysia’s builders now specify green waterproofing to align with national standards on sustainable materials. The Asia-Pacific adhesives market’s pivot toward bio-based inputs is inspiring innovations such as Saint-Gobain’s 40% bio-content Ethyl Acrylate, which slashes carbon footprint by 30%.

Growing Renovation Requirements Due to Aging Infrastructure

Ports, bridges and public housing erected in the 1970s-90s are approaching end-of-design life, stoking demand for polymer repair mortars with improved adhesion under tropical weather cycles. Thailand and the Philippines each prioritize structural retrofits in annual budgets, supporting stable volume growth for crack fillers and anti-corrosion primers.

Restraints Impact Analysis of Southeast Asia Construction Chemicals Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC and Formaldehyde Emission Caps | -0.80% | Singapore, Vietnam, region-wide | Short term (≤ 2 years) |

| High Raw-Material Price Volatility | -1.10% | Region-wide, Indonesia petrochemical constraints | Medium term (2–4 years) |

| Lack of Skilled Labour | -0.60% | Malaysia, Philippines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC and Formaldehyde Emission Caps

The Environmental Protection and Management Act amendments in Singapore require handling licences for persistent organic pollutants, adding compliance costs for solvent-borne products. Vietnam’s QCVN 01:2025/BYT regulation sets workplace limits on 70 substances, forcing reformulation of legacy adhesives. Thailand’s broad environmental framework tightens factory emissions, with smaller suppliers struggling to finance R&D for greener recipes. Indonesian coatings makers project continued construction growth, yet warn that limited consumer acceptance of premium eco-products could restrain uptake.

Lack of Skilled Labour

Malaysia’s “3D” perception of construction (dirty, dangerous, difficult) limits local talent supply, even as mechanization rises. Industrialized Building Systems help bridge gaps, yet installers still need training on mixing ratios and application sequences for advanced chemicals. Philippine infrastructure projects also compete for limited specialists, occasionally delaying waterproofing and coating schedules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Southeast Asia Construction Chemicals Market Segment Analysis

By Product Type:

Concrete Admixtures Lead Infrastructure ModernizationConcrete admixtures held a 33.12% slice of the Southeast Asia construction chemicals market in 2025, cementing their role in large-scale transport and housing programs. Indonesia’s cement dispatches of 64.887 million tons in 2024, paired with Vietnam’s 20% consumption surge in Q1 2025, created fertile territory for water reducers and set-controllers that accelerate turnaround of cast-in-place structures. Protective coatings, the fastest-growing sub-segment at 6.66% CAGR, ride on rehabilitating bridges, wharves and pipelines that need high-build epoxies to resist chloride ingress. Adhesives and flame retardants cater to the expanding modular-building scene, while waterproofing membranes protect projects exposed to monsoon cycles and high groundwater tables.

Technological trajectories within the Southeast Asia construction chemicals market emphasize multi-functional admixtures that shorten cycle times and shrink cement consumption. Sika’s integration of MBCC is slated to deliver CHF 180–200 million in annual synergies by 2026, underpinning broader portfolios that address concrete, flooring and sealant demands simultaneously. Henkel’s acquisition of Seal For Life enlarges its offering in long-life anticorrosion wraps tailored to coastal infrastructure. Regional formulators also localize additives to match tropical humidity and seismic stresses, winning share from imports less attuned to local job-site realities.

By Function:

Strength Enhancement Addresses Seismic and Climate ChallengesStrength enhancement solutions accounted for 35.80% of the Southeast Asia construction chemicals market in 2025 and are forecast to grow at 6.79% CAGR, mirroring the need for earthquake-ready and typhoon-resistant structures. Indonesia’s precast systems require bonding agents with high ductility to meet stringent seismic codes, whereas Singapore deploys polymer concretes in tunnel linings to combat aggressive groundwater attack. Durability and corrosion protection supplements strength additives by extending service life of marine facilities and industrial tanks.

Fire and thermal protection chemicals register solid adoption in high-rise developments, complying with tightened safety codes across ASEAN capitals. Aesthetic and surface finishing agents close the loop as homeowners seek premium textures and color-stable façades that withstand UV exposure. Overall, shifting design standards foster crossover products that deliver both mechanical reinforcement and environmental resistance within the Southeast Asia construction chemicals market.

By Application:

Residential Dominance Reflects Urbanization ImperativeResidential projects generated 36.62% of the Southeast Asia construction chemicals market in 2025 and are advancing at a 6.70% CAGR to 2031, propelled by government housing drives and rising middle-class expectations for quality finishes. Indonesia’s Three Million Houses Programme and the Philippines’ 10 million-unit backlog pull in waterproofing slurries, tile adhesives and acrylic sealants for bathrooms and kitchens. Vietnam’s USD 80 billion green-building opportunity, marked by nearly 430 certified sites by Q1 2024, steers demand toward low-VOC paints and bio-based bonding agents.

Commercial and industrial builds attract high-value flooring systems and protective linings for manufacturing expansion, while infrastructure applications secure a steady baseline for heavy-duty admixtures and grouts. The Southeast Asia construction chemicals market size for residential construction is projected to expand alongside mortgage reforms and smart-city blueprints, yet commercial and civil works remain key in introducing next-generation fire-resistant and energy-saving chemistries that later filter into housing projects.

Geography Analysis

Indonesia Construction Chemicals Market

Indonesia generated the largest revenue stream, holding 35.20% of the Southeast Asia construction chemicals market in 2025 and marching toward a 6.90% CAGR through 2031. The USD 35 billion New Capital City, plus an IDR 422.7 trillion 2024 infrastructure budget, accelerates concrete demand across bridges, mass-transit lines and smart-city districts. Local suppliers scale up polycarboxylate admixture plants to curb imports and meet climate-specific performance benchmarks.

ASEAN Construction Chemicals Market

Vietnam demonstrates strong growth momentum, buoyed by 13 transport projects worth USD 1.2 billion initiated in 2024 and a structural shift toward eco-certified buildings. Its coastal environment triggers strong uptake of epoxy-modified mortars for port rehabilitation. Thailand leverages Eastern Economic Corridor investments to raise outlays on industrial estates, fostering demand for high-build floor coatings and chemical anchors that resist heavy equipment vibration. The Philippines leans on Build Better More programs, pairing road expansion with extensive public housing exercises that favor bulk procurement of waterproofing emulsions. Malaysia’s 14.6% construction jump in H1 2024, led by rail and highway corridors, sustains purchases of set-accelerating admixtures that keep pace with tight erection windows. Singapore, though smaller in volume, exerts an outsized influence through its regulatory leadership and adoption of digital construction methods. Its Green Mark standards encourage lower-carbon chemistries that ripple across the wider Southeast Asia construction chemicals market. Emerging economies such as Cambodia and Laos round out the region, presenting frontier opportunities for mid-tier formulators able to provide affordable yet performance-oriented solutions.

Competitive Landscape

The Southeast Asia construction chemicals market is moderately fragmented, with global players expanding through acquisitions and capacity growth. Saint-Gobain's USD 1.025 billion acquisition of FOSROC strengthens its supply of admixtures, grouts, and waterproofers across 73 countries, enhancing its ASEAN presence. Sika reports high single-digit organic growth, opens a polymer flooring plant in Singapore, and boosts Indonesian production to reduce lead times[3]Sika, “Sika Continues Growth in Southeast Asia,” sika.com . MAPEI, with 102 subsidiaries and a EUR 3.977 billion turnover, drives rapid-setting mortars into fast-cycle housing projects, supported by local technical teams.

Regional specialists focus on localization to maintain their positions. SILKROAD HANOI customizes superplasticizers for Vietnamese cement blends, securing mass-housing contracts. Thai formulators develop elastomeric waterproofing for monsoon conditions, while Malaysian SMEs produce low-odor wall putties meeting green standards. Digitalization differentiates leaders, with real-time batch monitoring ensuring consistent dosage quality and compliance with concrete strength requirements. As seen in BASF's 40% bio-content Ethyl Acrylate, sustainability is a growing focus, reflecting the impact of carbon footprint metrics on purchasing. The market is shifting toward service-plus-solution models that integrate product supply, onsite advisory, and specification support, raising entry barriers for commodity-focused players in the Southeast Asia construction chemicals market.

Southeast Asia Construction Chemicals Industry Leaders

BASF SE

Holcim

MAPEI S.p.A.

Sika AG

Saint Gobain

- *Disclaimer: Major Players sorted in no particular order

Southeast Asia Construction Chemicals Market Companies Covered in this Report

- 3M

- Akzo Nobel N.V.

- Arkema

- Ashland

- BASF SE

- Dow

- H.B. Fuller

- Henkel AG & Co. KGaA

- Holcim

- MAPEI S.p.A.

- Nippon Paint Holdings Co., Ltd.

- Pidilite Industries Ltd.

- RPM International Inc.

- Saint Gobain

- Sika AG

- The Euclid Chemical Company

- Wacker Chemie AG

Read Analysis of Southeast Asia Construction Chemicals Companies

Recent Industry Developments in Southeast Asia Construction Chemicals Market

- April 2025: Sika has established its fourth factory in Kazakhstan with the opening of a facility in Ust-Kamenogorsk, a key industrial region in the eastern part of the country. The new plant features production lines for mortar and concrete admixtures and a modern laboratory.

- February 2025: Saint-Gobain has enhanced its global operations in the construction sector through the acquisition of FOSROC, one of the leaders in construction chemicals. This acquisition significantly strengthens Saint-Gobain's presence in key regions, including India, the Middle East, and the Asia-Pacific, further solidifying its position in the global market.

Southeast Asia Construction Chemicals Market Report Scope and Research Methodology

Market Definition and Coverage

Mordor Intelligence defines the Southeast Asia construction chemicals market as the yearly value of specialty additives, such as concrete and cement admixtures, waterproofing agents, protective coatings, sealants, grouts and related modifiers, sold for on-site or prefabricated building and infrastructure works across Indonesia, Vietnam, the Philippines, Thailand, Malaysia, Singapore and the remaining ASEAN members.

Scope exclusion: bulk commodity binders (ordinary Portland cement, lime, bitumen) and downstream decorative paints are not counted.

Segments Covered in This Report

- By Product Type

- Adhesives

- Concrete and Cement Admixtures

- Flame Retardants

- Protective Coatings

- Water-proofing Chemicals

- Other Construction Chemicals (Grouts, Sealants, etc.)

- By Application

- Commercial

- Industrial

- Infrastructure

- Residential

- By Function

- Strength Enhancement

- Durability and Corrosion Protection

- Fire and Thermal Protection

- Aesthetic and Surface Finishing

- By Geography

- Indonesia

- Vietnam

- Philippines

- Thailand

- Malaysia

- Singapore

- Rest of Southeast Asia

Data Sources, Market Sizing, and Validation

Primary Research

Multiple structured interviews with ready-mix suppliers, EPC contractors, project consultants, and regulatory officers across the six core ASEAN economies help us verify dosage assumptions, procurement margins, and emerging preferences for PCE-based admixtures and water-borne coatings. Feedback also calibrates how public-sector infrastructure outlays funnel into chemical demand by application.

Desk Research

Our analysts first sift through open datasets from agencies such as Indonesia's BPS, Thailand's NSO, Vietnam's GSO and ASEANstats, then cross-match them with building-permit filings, customs import codes for HS 3824 and HS 3506, tender awards posted on Tenders Info and technical papers from the Asian Concrete Institute.

Company 10-Ks and investor decks supply dosage rates and average selling prices, while D&B Hoovers and Dow Jones Factiva validate manufacturer revenues.

These sources anchor baseline demand, provide pricing corridors and flag regulatory shifts, for example, Singapore's 2025 low-VOC rules.

The list above is illustrative; many additional databases and trade journals are consulted before figures are locked.

Market-Sizing & Forecasting

A top-down build starts from cement consumption, ready-mix output and prefabrication volumes, which are then multiplied by standardized chemical dosage factors and filtered through country-level import-export balances.

Sampled supplier roll-ups and channel checks act as a bottom-up reasonableness screen before totals are finalized.

Key variables in the model include government capital-expenditure pipelines, residential housing starts, average admixture dosage (kg per ton of cement), ASP movements for acrylic polymers, and the adoption rate of low-VOC formulations.

Forecasts use multivariate regression coupled with scenario analysis, allowing elasticity tests under differing raw-material price and infrastructure-spend paths.

Data gaps, such as informal builder purchases, are bridged by calibrated ratios validated during primary interviews.

Data Validation & Update Cycle

Outputs undergo variance checks against historical customs trends, regional CPI shifts and producer earnings; anomalies trigger re-checks with sources.

A senior analyst reviews each workbook before sign-off.

The study refreshes annually, with interim updates if material events, like subsidy cuts or force-majeure plant shutdowns, occur.

How Mordor Intelligence's Southeast Asia Construction Chemicals Market Size Compares to Other Published Estimates

Published numbers often differ because firms widen or narrow geography, bundle adjacent product families, or project growth from untested price decks.

Key gap drivers here include some studies co-mixing asphalt additives and decorative paints; others roll India or Greater China into 'ASEAN'; a few rely solely on supplier revenue declarations without netting distributor discounts; refresh cadences also vary, leading to outdated base years.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.2 Bn (2025) | Mordor Intelligence | - |

| USD 8.7 Bn (2024) | Regional Consultancy A | Adds India and excludes channel mark-downs |

| USD 5.2 Bn (2023) | Trade Journal B | Uses supplier gross sales; omits gray-market imports |

| USD 4.5 Bn (2025) | Global Consultancy C | Bundles asphalt emulsifiers; relies on five-year-old price deck |

Taken together, the comparison shows that our disciplined scope, dual-layer modeling and annual refresh cadence deliver a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current value of the Southeast Asia construction chemicals market?

The market is valued at USD 3.38 billion in 2026 and is projected to reach USD 4.45 billion by 2031.

Which product segment holds the largest share in the Southeast Asia construction chemicals market?

Concrete admixtures lead with 33.12% share in 2025, reflecting heavy use in infrastructure and housing.

Which application area is expanding the fastest?

The residential segment posts the highest growth at a 6.70% CAGR to 2031, driven by housing programs across ASEAN.

Why are protective coatings growing rapidly?

Aging infrastructure and harsh marine conditions are boosting demand for high-performance protective coatings that can withstand corrosion and chloride attack.

How is regulation affecting product development?

New low-VOC rules in Singapore and Vietnam are accelerating the shift toward water-based and bio-based formulations, prompting suppliers to invest in greener chemistries.

Which country contributes the most to regional revenue?

Indonesia leads with 35.20% of market revenue in 2025, supported by its New Capital City project and large infrastructure budget.

Page last updated on: