Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

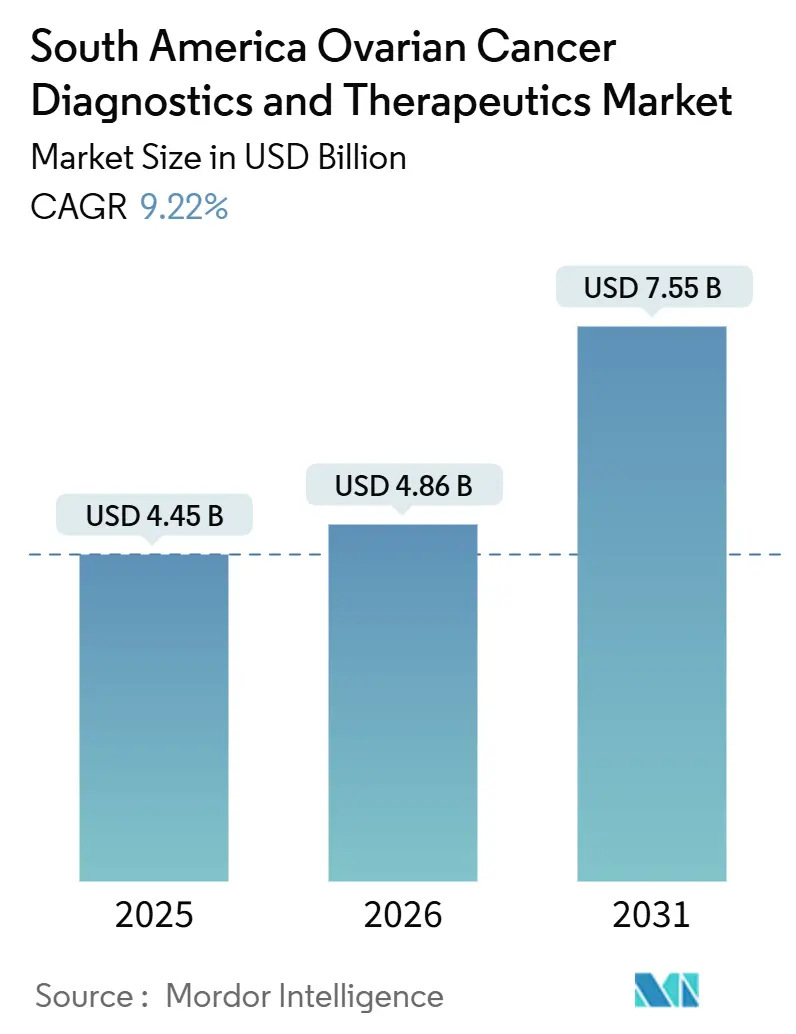

| Base Year Market Size (2025) | USD 4.45 Billion |

| Market Size (2026) | USD 4.86 Billion |

| Market Size (2031) | USD 7.55 Billion |

| Growth Rate (2026 - 2031) | 9.22% CAGR |

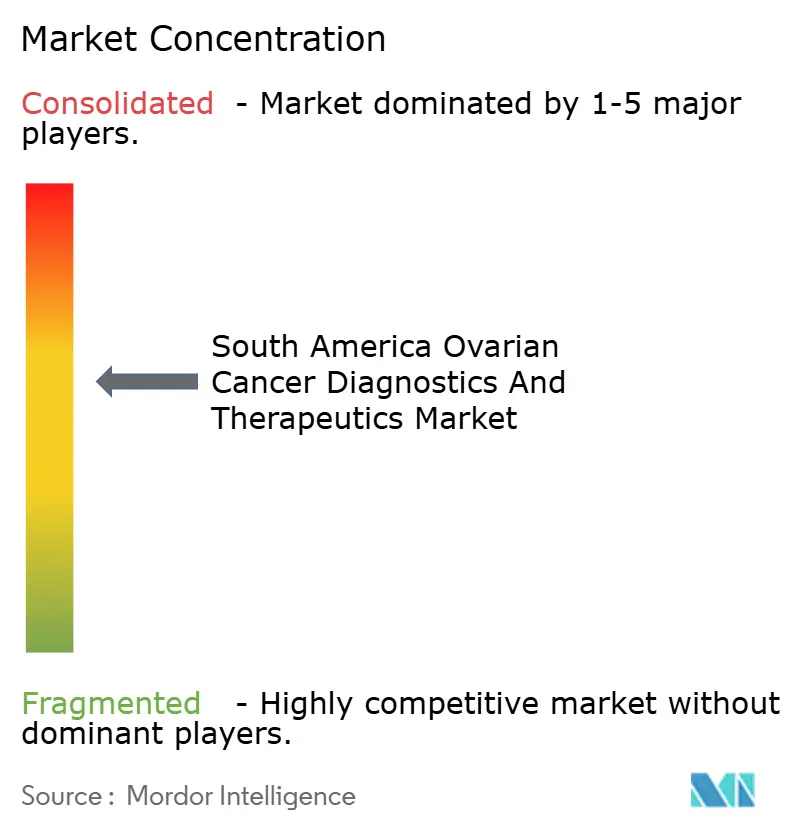

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Ovarian Cancer Diagnostics And Therapeutics Market Analysis by Mordor Intelligence

The South America Ovarian Cancer Diagnostics And Therapeutics Market size is projected to expand from USD 4.45 billion in 2025 and USD 4.86 billion in 2026 to USD 7.55 billion by 2031, registering a CAGR of 9.22% between 2026 to 2031.

The increasing number of newly diagnosed patients, expanding insurance mandates, and localized production of active pharmaceutical ingredients are driving revenue growth in the region. Ovarian cancer deaths are projected to rise significantly, from 206,956 in 2022 to over 350,000 by 2050, with late-stage cases dominating and reinforcing the reliance on chemotherapy and targeted therapies.[1]International Agency for Research on Cancer, “GLOBOCAN 2022,” gco.iarc.frRegulatory bodies are fast-tracking approvals, with Brazil’s ANVISA approving multiple targeted therapies and a liquid biopsy assay within 8 months of U.S. clearance. Multinational companies are leveraging regional real-world evidence registries to accelerate reimbursements, intensifying competition. Meanwhile, policymakers are allocating oncology budgets to address tariff-driven drug price inflation. These factors collectively establish a strong growth trajectory for South America's ovarian cancer diagnostics and therapeutics market over the next five years.

Key Report Takeaways

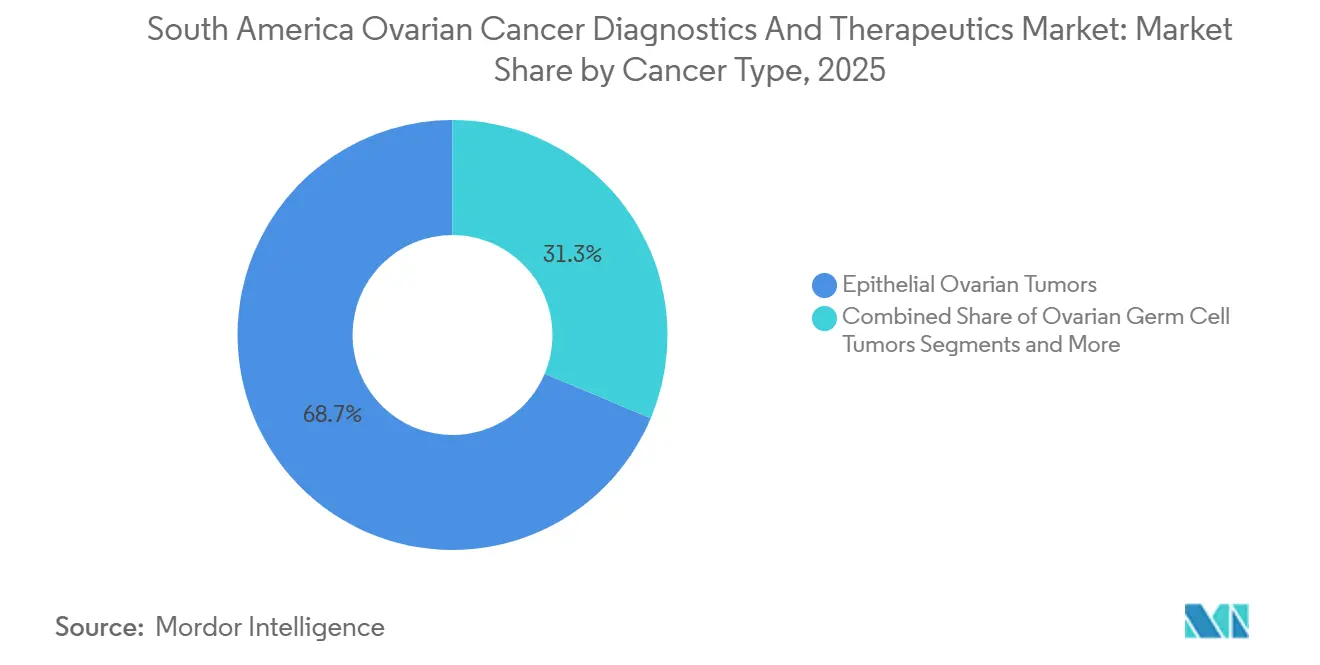

- By cancer type, epithelial tumors accounted for 68.67% of revenue in 2025, while germ-cell and stromal tumors grew at a subdued pace.

- By diagnostic modality, blood tests captured 34.45% of the South American ovarian cancer diagnostics and therapeutics market share in 2025; liquid biopsy platforms are advancing at a 12.80% CAGR through 2031.

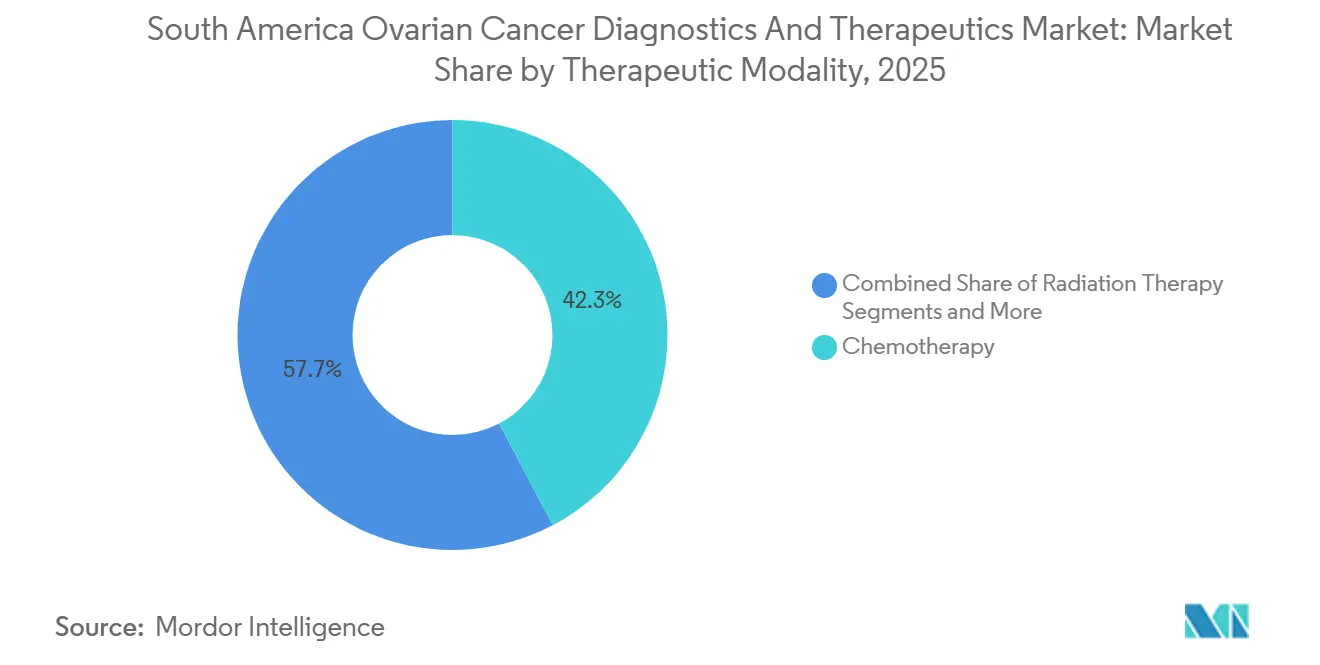

- By therapeutic modality, chemotherapy retained 42.27% of the South America ovarian cancer diagnostics and therapeutics market in 2025; targeted therapies are projected to expand at a 14.64% CAGR through 2031.

- By end user, hospitals accounted for 62.09% of spending in 2025, while ambulatory surgical centers are forecast to record an 11.85% CAGR through 2031.

- Brazil captured 47.34% of South America ovarian cancer diagnostics and therapeutics market revenue in 2025; Peru is expected to post the fastest-growing national CAGR at 10.35% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Ovarian Cancer Diagnostics And Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing incidences of ovarian cancer | +1.8% | Brazil, Argentina, Peru | Medium term (2-4 years) |

| Rising geriatric female population | +1.5% | Brazil, Argentina, Chile | Long term (≥4 years) |

| Growing healthcare expenditure & insurance coverage | +2.1% | Brazil, Peru, Colombia | Short term (≤2 years) |

| Rapid uptake of parp inhibitors & other targeted therapies | +2.3% | Brazil, Argentina, Chile | Short term (≤2 years) |

| Expansion of BRCA/HRD testing reimbursement programs | +1.2% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| On-shoring of oncology API manufacturing | +0.9% | Brazil, Argentina | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Increasing Incidences of Ovarian Cancer

In Andean nations, age-standardized incidence rates of ovarian cancer are rising at an annual rate between 2.1% and 2.7%, surpassing the global average. In 2022, Brazil reported 7,710 new ovarian cancer diagnoses and anticipates a 9% yearly increase through 2030.[2]World Health Organization, “Cancer Fact Sheet,” who.int This projection is driven by the continued adoption of opportunistic rather than systematic screening approaches. Over 60% of diagnosed cases remain at FIGO stages III or IV, limiting overall survival to 32 months. This late-stage diagnosis has significantly increased the demand for platinum-based chemotherapy and first-line PARP inhibitor maintenance treatments. To address this, health ministries are piloting risk-stratified screening programs. For instance, Chile’s hereditary registry now connects BRCA carriers directly to prophylactic surgeries.[3]Chilean Ministry of Health, “Programa Nacional de Cáncer,” minsal.cl Pharmaceutical companies are prioritizing the region for drug launches, as evidenced by the eight-month approval lead for olaparib in Brazil compared to the United States.

Rising Geriatric Female Population

By 2035, the percentage of South American women aged 65 and older is projected to rise from 8.1% in 2025 to 11.3%. Since the risk of ovarian cancer peaks between ages 55 and 74, this growing elderly demographic is expected to increase both the number of incident cases and the duration of maintenance therapy. In response, tertiary centers are establishing geriatric oncology units to address challenges like polypharmacy and frailty, favoring oral targeted agents and outpatient infusions over traditional inpatient chemotherapy. With longer life expectancies, there is also a rise in surveillance testing. Serial CA-125 assays and liquid biopsies are now reimbursed, enabling earlier detection of biochemical recurrences before they progress to imaging.

Growing Healthcare Expenditure & Insurance Coverage

In 2024, Brazil allocated approximately USD 28 billion to healthcare, with over half directed toward hospital and outpatient services. Additionally, Brazil expanded its essential medicines list by incorporating 14 new oncology drugs. Peru invested USD 120 million to upgrade 22 regional oncology centers, successfully reducing the median time-to-treatment from 47 days in 2023 to a targeted 29 days in 2025. In Chile, the national health fund now covers 78% of the population and recently included bevacizumab-paclitaxel in its guaranteed benefits package, resulting in an 81% reduction in average first-line out-of-pocket expenses. These initiatives are streamlining patient access to evidence-based treatment pathways.

Rapid Uptake of PARP Inhibitors & Other Targeted Therapies

Following promising results from the OCEANIA registry, which involved 1,240 patients, both olaparib and niraparib have made significant inroads into maintenance therapy across Brazil, Argentina, and Chile. This figure aligns with the nation's willingness-to-pay benchmark. Meanwhile, mirvetuximab soravtansine, an antibody-drug conjugate targeting folate receptor alpha, received approval in 2024 and is currently under review by regulatory authorities. Early-access data showcase a promising 32% objective response rate in patients with platinum-resistant conditions.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Low Awareness Leading to Late-Stage Diagnosis | -1.4% | Peru, Colombia, northern Brazil | Medium term (2-4 years) |

| High Cost of Targeted Drugs & Companion Diagnostics | -1.1% | Argentina, Peru, Colombia | Short term (≤2 years) |

| Pathology Workforce Shortages Causing Biomarker Test Delays | -0.8% | Tier-2 cities, rural areas | Long term (≥4 years) |

| Fragmented Reimbursement for Companion Diagnostics vs Drugs | -0.7% | Argentina, Colombia, Brazil | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low Awareness Leading to Late-Stage Diagnosis

In rural Peru and Colombia, symptom-awareness campaigns reach fewer than 35% of women. This limited reach results in a median diagnostic delay of 7.2 months, more than double that observed in metropolitan São Paulo and Buenos Aires. Patients diagnosed at Stage IV are often ineligible for cytoreductive surgery and face treatment costs that are 2.8 times higher, primarily due to extended chemotherapy and palliative care. While Chile’s pilot program utilizing community health workers shows potential, the issue of sustainable funding remains unresolved.

High Cost of Targeted Drugs & Companion Diagnostics

In Argentina, Olaparib is priced at ARS 1.2 million (USD 3,400) per month. This cost, which is four times the median household income, leads 38% of patients to discontinue therapy within six months. Germline BRCA testing, available in private labs, costs between USD 800 and 1,200. However, the reimbursement authorization process can take 90 to 120 days, delaying precision medicine decisions. In Peru, EsSalud has set an annual cap of USD 30,000 on PARP spending. This threshold is exceeded by two-thirds of recipients, forcing them to switch to generic chemotherapy or rely on manufacturer assistance programs. Advocacy groups are advocating for performance-based contracts that ensure reimbursement only when a biomarker-defined response is documented, following the example of Chile’s 2024 pembrolizumab model.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cancer Type: Epithelial Tumors Widen Their Lead

Epithelial tumors accounted for 68.67% of South America's ovarian cancer diagnostics and therapeutics market revenue in 2025, with an anticipated growth rate of 11.5% CAGR through 2031. High-grade serous carcinoma, representing over half of all epithelial diagnoses, demonstrates the highest prevalence of BRCA and HRD, driving the adoption of PARP inhibitors. Local trials for PI3K and AKT inhibitors are gaining momentum, particularly for clear-cell and endometrioid variants, with alpelisib currently in a phase II study in Brazil involving 180 patients.

Ongoing molecular segmentation is expected to further refine treatment algorithms. The increasing adoption of comprehensive genomic profiling enables oncologists to identify actionable mutations such as PIK3CA, ARID1A, and PTEN, creating opportunities for targeted therapy combinations. Advocacy groups are actively promoting subtype-specific clinical-trial enrollment criteria to accelerate access to experimental treatments.

By Diagnostic Modality: Liquid Biopsy Accelerates Genomic Insight

Blood-based CA-125 assays remain a cornerstone of diagnostic workflows, contributing 34.45% of 2025's revenue. However, their dominance is diminishing as liquid-biopsy assays gain traction, growing at a 12.80% CAGR following the approval of Guardant360 CDx, the first comprehensive ctDNA test for ovarian cancer. The market for liquid-biopsy platforms in South America is projected to approach USD 950 million by 2031, driven by their ability to detect resistance mutations without the need for invasive tissue re-biopsies.

Laboratory networks are consolidating to scale next-generation sequencing capabilities, with major players deploying advanced systems in key locations such as São Paulo and Buenos Aires. Additionally, payers are increasingly bundling reimbursements for molecular testing with companion therapeutics, facilitating broader adoption.

By Therapeutic Modality: Targeted Agents Redefine Maintenance

In 2025, chemotherapy retained a 42.27% revenue share, primarily supported by cost-effective carboplatin-paclitaxel doublets supplied by regional generics. However, targeted therapies are experiencing the fastest growth, with a 14.64% CAGR through 2031. Drugs such as olaparib, niraparib, and rucaparib are gaining significant traction in first-line maintenance for BRCA-mutated and HRD-positive patients. The market share of targeted agents is expected to exceed 35% by 2031, supported by the anticipated approval of mirvetuximab soravtansine in Brazil.

Price reductions are becoming evident, with biosimilars of bevacizumab significantly lowering per-cycle costs by over 50% in 2024, thereby improving accessibility within Brazil’s public health system. Additionally, value-based contracts for PARP inhibitors, which offer refunds for non-responsive patients, are under active negotiation.

By End User: Ambulatory Migration Gains Speed

Hospitals accounted for 62.09% of spending in 2025, driven by their role in cytoreductive surgeries and high-acuity chemotherapy infusions. However, ambulatory surgical centers are expanding rapidly, with an 11.85% CAGR, supported by minimally invasive laparoscopy and same-day discharge protocols that reduce per-case costs by 40% compared to inpatient care. Rede D’Or has opened seven oncology-focused ambulatory units between 2024 and 2025, targeting an 85% same-day discharge rate.

Diagnostic laboratories are also consolidating, with key players merging select sequencing operations to enhance purchasing power for genomic reagents. This consolidation supports standardized reporting and faster turnaround times, which are critical for timely maintenance-therapy decisions.

Geography Analysis

In 2025, Brazil accounted for 47.34% of South America's ovarian cancer diagnostics and therapeutics market revenue. This leadership was driven by its 108 million women of reproductive age and a universal public insurance system reimbursing over 75% of medical visits. Global pharmaceutical companies, including AstraZeneca and Roche, have established trial coordination hubs in São Paulo to leverage extensive patient pools and expedite enrollment processes.

Argentina held a 22% revenue share in 2025, supported by PAMI's coverage of 5.2 million retirees, the highest-risk demographic. Economic instability has led to the adoption of risk-sharing models, where manufacturers reimburse payers if predefined clinical outcomes are not achieved.

Peru is experiencing the fastest growth, with the market projected to expand at a 10.35% CAGR through 2031. EsSalud's insurance expansion now includes 1.8 million informal-sector workers, while significant investments in oncology centers have reduced treatment delays and improved early diagnosis rates. Chile's hereditary registry sets a benchmark for BRCA-carrier management, with Uruguay exploring a similar initiative. Bolivia and Ecuador, facing rising incidence rates, continue to rely on cross-border referrals to advanced centers in Brazil and Argentina.

Competitive Landscape

Market concentration is moderate, with the top five pharmaceutical companies controlling approximately 58% of therapeutic revenue in 2025. Diagnostics remain fragmented, divided between global platform providers and regional lab networks. Key strategic priorities include accelerating reimbursements, bundling companion diagnostics, and increasing local API production to mitigate the impact of 2025 tariff hikes.

AstraZeneca’s Lynparza achieved Brazilian approval eight months after its U.S. clearance, supported by strong local real-world evidence. Roche is integrating Guardant360 ctDNA results into tumor-board workflows via its NAVIFY cloud, reducing treatment decision timelines by up to five days. GSK is addressing enrollment disparities through a decentralized trial model, recruiting patients from 55 satellite centers across urban and rural areas.

Diagnostic companies are focusing on urban referral centers for high-throughput sequencing systems, while rural clinics benefit from point-of-care ultrasound and rapid CA-125 kits under a World Bank oncology-equity grant. Brazilian contract manufacturers, such as Eurofarma, are scaling up PARP inhibitor production to shorten lead times and manage currency volatility effectively.

South America Ovarian Cancer Diagnostics And Therapeutics Industry Leaders

AstraZeneca plc

F. Hoffman-La Roche Ltd

Siemens Healthineers AG

Johnson & Johnson Services, Inc.

GSK plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Henlius Biotech secured marketing authorization from Bolivia's AGEMED for Longiva, its bevacizumab biosimilar, marking the company's fourth international approval.

- January 2025: AstraZeneca announced a USD 45 million investment to expand its oncology trial hub in São Paulo, with plans to enroll 800 ovarian cancer patients from the region by 2027.

South America Ovarian Cancer Diagnostics And Therapeutics Market Report Scope

As per the scope of the report, Ovarian cancer is a type of cancer that begins in the ovaries. There are several types of ovarian cancer, among which Epithelial ovarian cancer is the most common type of ovarian cancer. The report covers various diagnostic and therapeutic approaches used in the treatment of ovarian cancer.

The South America ovarian cancer diagnostics and therapeutics market is segmented by cancer type, diagnostic modality, therapeutic modality, end user, and geography. By cancer type, the market is segmented into epithelial ovarian tumors, ovarian germ cell tumors, and others. By diagnostic modality, the market is segmented into biopsy, blood tests, ultrasound, PET, CT scan, MRI, liquid biopsy (ctDNA), and other diagnostics. By therapeutic modality, the market is segmented into chemotherapy, radiation therapy, targeted therapy, immunotherapy, hormonal therapy, and others. By end user, the market is segmented into hospitals, cancer specialty centers, diagnostic laboratories, ambulatory surgical centers, and research institutes. By geography, the market is segmented into Brazil, Argentina, Colombia, Chile, Peru, and the rest of South America. The report offers market size and forecasts in value (USD) for the above segments.

By Cancer Type

| Epithelial Ovarian Tumors |

| Ovarian Germ Cell Tumors |

| Others |

By Diagnostic Modality

| Biopsy |

| Blood Tests |

| Ultrasound |

| PET |

| CT Scan |

| MRI |

| Liquid Biopsy (ctDNA) |

| Other Diagnostics |

By Therapeutic Modality

| Chemotherapy |

| Radiation Therapy |

| Targeted Therapy |

| Immunotherapy |

| Hormonal Therapy |

| Others |

By End User

| Hospitals |

| Cancer Specialty Centers |

| Diagnostic Laboratories |

| Ambulatory Surgical Centers |

| Research Institutes |

By Geography

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Cancer Type | Epithelial Ovarian Tumors |

| Ovarian Germ Cell Tumors | |

| Others | |

| By Diagnostic Modality | Biopsy |

| Blood Tests | |

| Ultrasound | |

| PET | |

| CT Scan | |

| MRI | |

| Liquid Biopsy (ctDNA) | |

| Other Diagnostics | |

| By Therapeutic Modality | Chemotherapy |

| Radiation Therapy | |

| Targeted Therapy | |

| Immunotherapy | |

| Hormonal Therapy | |

| Others | |

| By End User | Hospitals |

| Cancer Specialty Centers | |

| Diagnostic Laboratories | |

| Ambulatory Surgical Centers | |

| Research Institutes | |

| By Geography | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

How large will spending on ovarian-cancer diagnostics and drugs become in South America by 2031?

Combined revenue is projected to reach USD 7.55 billion, advancing at a 9.2% CAGR from 2026 to 2031.

Which treatment category is growing fastest across the region?

Targeted therapies, particularly PARP inhibitors, are expected to post a 14.6% CAGR through 2031 as reimbursement expands.

Why is Peru the quickest-expanding national market?

Insurance reforms, a USD 120 million oncology-center upgrade program, and a rising insured workforce push Perus CAGR to 10.35%.

What share do epithelial tumors hold within regional therapeutic revenue?

Epithelial tumors commanded 68.67% of revenue in 2025 and will maintain leadership through 2031.

How are payers addressing the high cost of genomic testing?

Countries such as Chile and Brazil are bundling BRCA or HRD testing reimbursement with the cost of maintenance therapies, easing patient access.

Which diagnostic technology is most likely to displace tissue biopsy?

Liquid-biopsy assays like Guardant360 CDx are seeing 12.8% CAGR growth because they detect resistance mutations from a routine blood draw.

Page last updated on: