Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

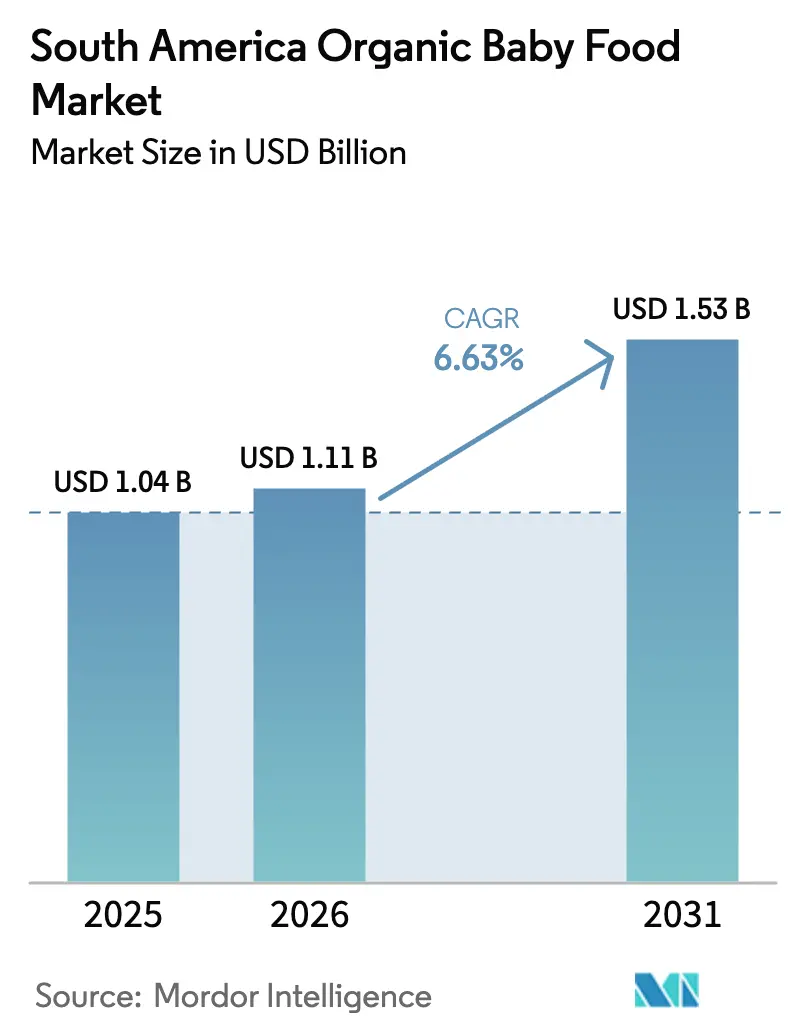

| Base Year Market Size (2025) | USD 1.04 Billion |

| Market Size (2026) | USD 1.11 Billion |

| Market Size (2031) | USD 1.53 Billion |

| Growth Rate (2026 - 2031) | 6.63% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Organic Baby Food Market Analysis by Mordor Intelligence

In 2025, the South American organic baby food market size is valued at USD 1.04 billion. The South American organic baby food market is expected to grow from USD 1.04 billion in 2025 to USD 1.11 billion in 2026 and is forecast to reach USD 1.53 billion by 2031 at 6.63% CAGR over 2026-2031. South America’s organic baby food market is shifting rapidly from niche to mainstream, led by a growing middle class, fast-paced urbanization, and new labeling laws in Brazil and Chile. To meet evolving consumer expectations, companies are blending local superfoods into their offerings while investing in better cold-chain systems and smoother e-commerce delivery networks across key cities. These moves cater to parents who prioritize premium quality and doorstep delivery. Although sourcing certified organic ingredients remains costly, major formula manufacturers are increasingly building vertically integrated supply models to secure a more reliable pipeline. These initiatives not only alleviate constraints but also assist local farmers in transitioning to organic methods. Consequently, the South American organic baby food market is becoming more resilient to currency fluctuations and supply disruptions. Furthermore, it's fostering consumer trust through traceability measures, including QR-code provenance checks.

Key Report Takeways

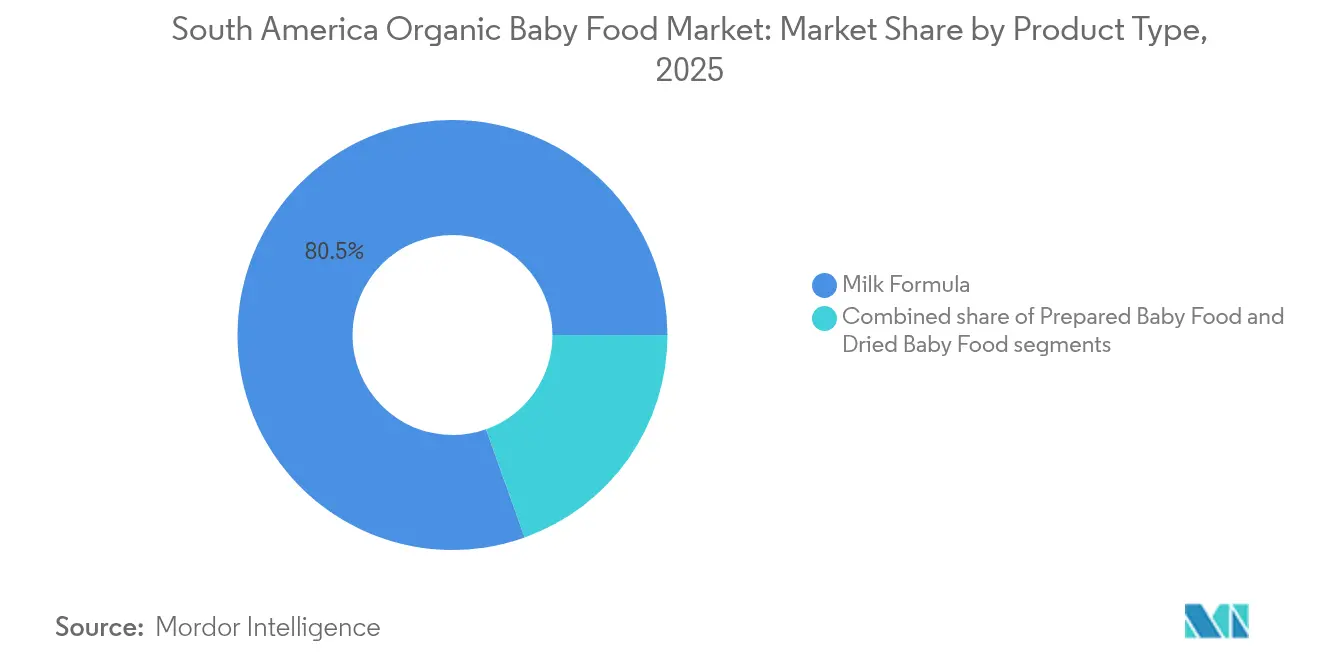

- By product type, milk formula led with 80.45% of the South American organic baby food market share in 2025, while prepared baby food is forecast to expand at a 7.02% CAGR to 2031.

- By age group, the 6-12 months segment captured 57.62% of the South American organic baby food market share in 2025; the 12-24 months cohort is projected to grow at a 7.69% CAGR through 2031.

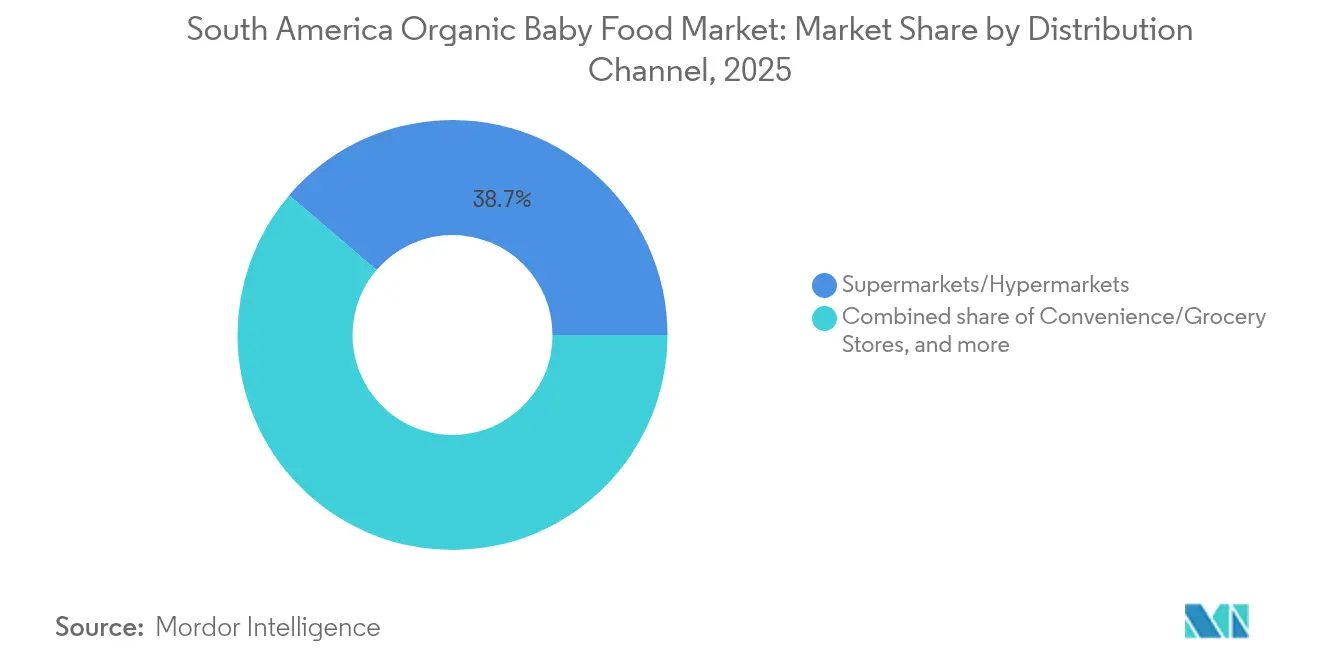

- By distribution channel, supermarkets and hypermarkets held 38.74% revenue share in 2025, while online retail stores recorded the highest projected CAGR at 7.66% for 2026-2031.

- By geography, Brazil dominated with a 46.88% share in 2025, and Argentina is poised for the quickest expansion at a 7.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Organic Baby Food Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising middle-class demand for clean-label infant nutrition | +4.2% | Brazil, Argentina, Chile, with spillover to Colombia and Peru | Medium term (2-4 years) |

| Awareness regarding nutrition labeling promoting demand | +3.1% | Brazil, Argentina, Chile | Short term (≤ 2 years) |

| Fast expansion of online baby specialty retailers | +2.8% | Brazil, Colombia, Chile, urban centers in Peru and Argentina | Short term (≤ 2 years) |

| Growing participation of women in workforce boosting demand for ready-to-eat organic purees | +2.1% | Brazil, Chile, Colombia | Medium term (2-4 years) |

| Growing popularity of plant-based diets influencing baby food choices. | +1.8% | Brazil, Chile, Argentina, urban centers across region | Medium term (2-4 years) |

| Rise in e-commerce platforms facilitating easy access to organic baby food. | +1.6% | Brazil, Colombia, Chile, Argentina | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising middle-class demand for clean-label infant nutrition

In Brazil and Argentina, the rapidly expanding middle class is driving a major shift in the organic baby food market. Parents are increasingly favoring products devoid of artificial ingredients, preservatives, and pesticides. As a result, there's a notable surge in demand for premium organic offerings. With rising incomes, middle-class families are more willing to spend on what they view as safer, higher-quality nutrition for their children. Parents are becoming more ingredient-savvy, prompting brands to simplify formulations and use familiar, transparent ingredients.Social media parenting groups are amplifying this shift, sharing tips and ingredient insights that help normalize organic choices across diverse income groups. Furthermore, government initiatives promoting organic farming and sustainable practices in both countries are expected to support the growth of the organic baby food market during the forecast period.

Awareness regarding nutrition labeling promoting demand

In South America, as parents sharpen their skills in deciphering ingredient lists and nutritional data, the organic baby food market is witnessing a surge. Stricter labeling regulations, particularly in Brazil and Chile, have fostered a more transparent marketplace, where the clear indication of products free from artificial additives and pesticide residues has become a key competitive advantage. Tighter labeling laws in Brazil and Chile are driving a new level of transparency, helping parents easily spot the differences between organic and conventional options. A 2024 study found that parents who understand nutrition labeling are nearly three times more likely to choose organic products for their babies. This trend is especially evident among first-time parents, who, with heightened vigilance towards allergens and contaminants, gravitate towards certified organic products boasting clear and thorough labeling. Additionally, the rising prevalence of health-conscious lifestyles and increasing disposable incomes in the region are further fueling the demand for organic baby food. Manufacturers are responding by going beyond basic compliance, providing greater visibility into how ingredients are sourced and processed a move that resonates strongly with today’s informed parents.

Fast expansion of online baby specialty retailers

In South America, online baby specialty retailers are revolutionizing how parents discover and buy organic baby food. Online baby stores are transforming how parents across South America buy organic baby food. These platforms make premium products easier to find and compare, offering detailed descriptions, honest reviews, and professional advice all in one place. World Bank data (2024) revealed that about 84% of Brazil’s population uses Internet [1]Source: International Telecommunication Union (ITU), “Individuals Using the Internet (% of Population),"data.worldbank.org.. This digital surge has empowered brands to connect with consumers in secondary cities, previously cut off from specialty retail. Time-pressed parents are embracing subscription and auto-refill options, ensuring a steady supply of trusted products without the hassle of repeat shopping. This trend not only guarantees manufacturers steady revenue but also fosters deeper brand loyalty. Furthermore, direct-to-consumer approaches enable smaller organic baby food brands to sidestep traditional retail hurdles. By selling directly to consumers, smaller brands save on retail costs and gain valuable insights into customer behavior, helping them tailor products and messaging more effectively.

Growing participation of women in workforce boosting demand for ready-to-eat organic purees

In South America, the increasing participation of women in the workforce is reshaping family dynamics and feeding practices, driving significant growth in the demand for convenient and nutritious organic baby food. Urban working mothers, who often face time constraints, are turning to ready-to-eat organic purees as a practical alternative. These products combine the nutritional benefits of homemade food with the convenience required by modern lifestyles. According to World Bank data, 53% of women in Brazil in 2024 are part of the labor force, highlighting the growing need for such solutions [2]Source: World Bank Group, "Labor force participation rate, female (% of female population ages 15+) Brazil,"data.worldbank.org. This trend is particularly prominent in Brazil and Chile, where improved childcare services are enabling more women to pursue employment. This shift not only supports women's economic empowerment but also directly contributes to the expanding market for organic baby food. In response, manufacturers are focusing on innovation, enhancing packaging designs and product formulations to emphasize convenience and the use of premium organic ingredients. These products are being marketed as essential tools for modern parenting, offering a balance between nutrition and practicality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited regional organic raw-material supply raising cogs for milks and cereals | -2.3% | Brazil, Argentina, Peru | Medium term (2-4 years) |

| Constrained cold-chain logistics in rural andes limiting shelf life of fresh purees | -1.7% | Peru, Colombia, Chile, rural areas of Argentina | Short term (≤ 2 years) |

| Shorter shelf life of organic products leading to potential wastage. | -1.4% | All countries, particularly rural and remote areas | Short term (≤ 2 years) |

| Regulatory hurdles and certifications can be time-consuming and costly for producers | -1.2% | Brazil, Argentina, Peru, Colombia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited regional organic raw-material supply raising cogs for milks and cereals

In South America, manufacturers of milk formulas and cereals grapple with rising costs, largely due to a persistent shortage of certified organic raw materials. While organic agriculture is on the rise in the region, it still falls short of meeting the surging demand. This shortfall compels producers to either turn to costly imports or navigate the intricate process of establishing local supply chains. Brazil and Argentina feel the brunt of this challenge, as the shift to organic farming faces hurdles like steep certification costs, a dearth of technical know-how, and insufficient policy backing. Some companies are turning to vertical integration by forging direct ties with farmers and offering technical support to bolster organic farming practices and work towards a steadier supply chain. However, these initiatives demand hefty upfront investments and patience, as immediate supply boosts aren't guaranteed. Consequently, manufacturers must balance short-term challenges with the promise of long-term gains in South America's shifting organic market landscape.

Constrained cold-chain logistics in rural andes limiting shelf life of fresh purees

In the rural Andean regions, a rudimentary cold chain infrastructure is hindering the distribution and shelf life of fresh organic purees. This shortcoming limits market penetration in crucial areas of Peru, Colombia, and Chile. The region's mountainous terrain and inadequate refrigerated transport and storage lead to temperature control issues, threatening the integrity and safety of products, particularly organic ones that lack preservatives. Local producers, often unable to invest in private cold chain solutions, find themselves at a competitive disadvantage. This scenario favors multinational corporations, which have established distribution networks and shelf-stable formulations. These market dynamics are driving innovations in alternative preservation methods and packaging technologies. These advancements seek to maintain nutritional integrity without the necessity for constant refrigeration. Yet, manufacturers grapple with challenges, as these solutions frequently involve trade-offs between shelf stability, nutritional value, and a clean-label positioning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Milk Formula Dominates Despite Ingredient Challenges

In 2025, the milk formula segment secures a commanding 80.45% share of the South American organic baby food market. Its prominence is anchored in its pivotal role in infant nutrition, especially for households unable to breastfeed. Established players, leveraging strong brand equity, have adeptly positioned organic formulations as premium, price-worthy alternatives. Manufacturers find themselves at a crossroads, balancing the scarce availability of organic dairy inputs with the imperative to provide comprehensive dietary profiles vital for infant growth. Recent innovations spotlight hypoallergenic organic formulations, a response to the surging food sensitivities in infants, birthing premium subsegments that boast elevated margins.

Though the prepared baby food segment currently holds a smaller share, it's poised to be the market's growth catalyst, eyeing a robust CAGR of 7.02% from 2026 to 2031. A rising maternal workforce and shifting feeding practices fuel this surge. Manufacturers are at the forefront of innovation, crafting organic purees that not only echo homemade textures and flavors but also infuse indigenous superfoods, resonating with health-conscious parents. The allure of convenience further propels the segment's momentum. As parents juggle busy schedules, the demand for nutritious, ready-to-eat options aligned with values of clean ingredients and sustainability has surged.

By Age Group: 6-12 Months Segment Captures Critical Weaning Transition

In 2025, the South American organic baby food market sees the 6-12 months age group commanding a dominant 57.62% share. This age bracket, pivotal in transitioning infants from exclusive milk feeding to solid foods, underscores the blend of nutritional complexity and heightened parental concern. As parents introduce solid foods, their heightened attention to premium organic offerings stems from promises of safety and optimal nutrition. Manufacturers, recognizing this critical juncture, craft stage-specific organic products that introduce varied textures and flavors while upholding stringent organic standards, fostering brand loyalty throughout the weaning process.

Meanwhile, the 12-24 months segment is on the rise, boasting a projected CAGR of 7.69% from 2026 to 2031. This growth highlights parents' preference for commercially prepared organic options before transitioning to family meals. Fueled by an awareness of specialized nutrition's importance during toddlerhood and the convenience of ready-to-serve organic meals, products in this segment feature sophisticated flavors and diverse textures, aiding palate development and eating skills. Brands are introducing organic finger foods and self-feeding options, aligning with contemporary feeding philosophies and maintaining a clean-label appeal for health-conscious parents.

By Distribution Channel: Supermarkets Lead While E-commerce Accelerates

In 2025, supermarkets and hypermarkets command a dominant 38.74% market share, capitalizing on their unmatched physical presence and the one-stop shopping convenience that resonates with busy parents. Strategic in-store placements strengthen their position in the organic baby food category by placing premium organic options alongside conventional ones for easy comparison. Dedicated baby sections further enhance the shopping experience. Leading supermarket chains across South America are expanding organic private label offerings, creating price-competitive alternatives that attract a broader consumer base. In 2023, Carrefour Comércio e Indústria Ltda boasted 1,188 food retail stores, securing its position as the second-largest player in Brazil, just behind AM/PM Comestíveis Ltda .

Online retail is soaring, with forecasts predicting a CAGR of 7.66% from 2026 to 2031. This boom is reshaping how South Americans find, evaluate, and buy organic baby food. The online channel thrives by offering detailed product information, honest customer reviews, and expert insights on organic benefits. Additionally, online platforms provide a crucial avenue for organic specialty brands, often overlooked in brick-and-mortar stores, to engage niche audiences with targeted messaging. Subscription models now suggest products based on a child's age and developmental milestones, ensuring steady revenue and simplifying the replenishment process for busy parents.

Geography Analysis

In 2025, Brazil commands a dominant 46.88% share of the South American organic baby food market, capitalizing on its vast population, a burgeoning middle class, and an increasing health consciousness among its urban dwellers. With the economy stabilizing and incomes rising, Brazilian families are willing to pay more for premium organic baby foods that emphasize safety and nutrition. However, ingredient sourcing remains a key challenge, as domestic organic farming still can’t keep pace with demand. New labeling regulations introduced by the Brazilian government have bolstered transparency and trust among consumers, fostering a conducive atmosphere for organic products that prioritize clean ingredients and nutritional value, as highlighted by the Global Organic Trade Association.

The market is buzzing with innovations, particularly in organic formulations that resonate locally, integrating indigenous Brazilian superfoods like açaí and cupuaçu, catering to parents desiring culturally authentic nutrition for their children. While Brazil's organic agriculture is on the rise, it struggles to satiate the surging demand. This shortfall opens the door for companies ready to invest in local supply networks, building long-term partnerships with farmers and supporting the region’s shift toward organic production.

Argentina is on the fast track, eyeing a robust CAGR of 7.15% from 2026 to 2031, albeit starting from a modest base. As the economy stabilizes, conditions are ripe for the premium category to flourish. The Argentine market shows a pronounced inclination towards milk formulas, a nod to cultural feeding traditions, and the dominance of multinational dairy firms with local production units. Danone stands tall in Argentina's specialized nutrition arena, with its brands, Aptamil and Nutrilon, making significant inroads in the organic infant formula segment. Urban centers, especially Buenos Aires, are witnessing a surge in demand for high-quality imported organic products among the affluent, even as economic fluctuations pose challenges to wider market penetration.

Competitive Landscape

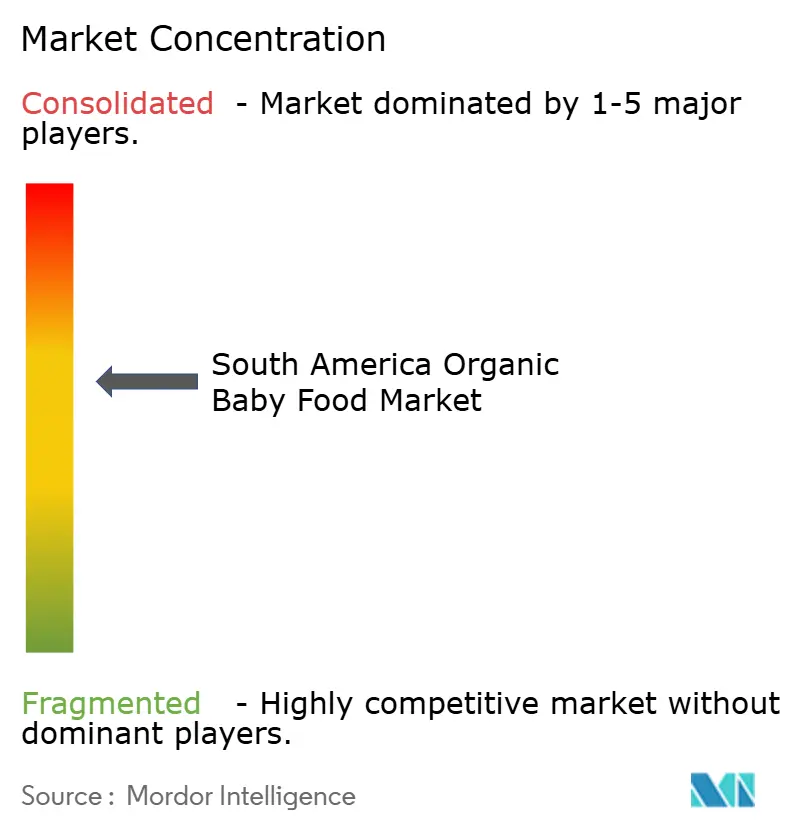

The South American organic baby food market is moderately consolidated with the presence of major players in the market, such as Nestlé S.A., The Hain Celestial Group, Inc., Abbott Laboratories, The Hero Group, Sun-Maid Growers of California, among others. In response to evolving consumer tastes and preferences, these key players, along with other active companies, have prioritized product innovation. Their strategy centers on offering diverse products with enhanced functionalities, complemented by essential certifications to bolster consumer trust.

A significant space exists between expensive international brands and low-cost conventional options, a space regional producers can target with affordable, locally made organic alternatives. By optimizing local supply chains, these players can craft cost-competitive organic products. Meanwhile, players like PachaMama Orgânicos from Brazil and Biorgánicos Chile SpA are carving a niche by spotlighting indigenous ingredients and cultural significance. Their approach directly challenges the "imported premium" image of multinationals, offering genuine local alternatives that align with a rising wave of nationalistic consumer sentiments.

Technology is emerging as a key differentiator. Major players are investing in blockchain-based traceability tools that give consumers greater confidence in certification and sourcing claims. These systems not only validate organic credentials and production methods but also tackle the increasing consumer skepticism surrounding certification claims. Regulatory frameworks can act as barriers to entry, potentially hindering both innovation and competition, as underscored by recent analyses of supply chain vulnerabilities.

South America Organic Baby Food Industry Leaders

-

The Hain Celestial Group, Inc

-

The Hero Group

-

Sun-Maid Growers of California

-

Abbott Laboratories

-

Nestle S.A

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Bobbie expanded its footprint by introducing its organic infant formulas in nearly 500 Whole Foods Market outlets. Both its Organic and Organic Gentle lines meet FDA and EU nutritional standards and are now available to South American consumers.

- October 2024: Babylife Organics, a new entrant in the baby food sector, launched a line of Regenerative Organic Certified products designed to mitigate toxic heavy metal contamination. The line, which includes various fruit and vegetable purees, is tested for arsenic, cadmium, lead and mercury at four critical points: soil, raw ingredients, prepared ingredients and the final product.

- January 2024: Nestlé invested BRL 6 billion (approx. USD 1.2 billion) in food and drink production in Brazil, with a series of payments between 2023 and 2025. According to the brand, the fund is primarily allocated to boost business growth, integrate new technologies in the industry, expand manufacturing facilities, transform its portfolio, and advance the sustainability agenda in Nestlé’s including baby food in Brazil.

South America Organic Baby Food Market Report Scope

Organic baby foods are grown or processed without synthetic fertilizers or pesticides. The organic baby food market is segmented by product type, age group, packaging type, distribution channel, and geography. By product type, the segmentation includes milk formula, prepared baby food, and dried baby food. By age group, the market is segmented into 0-6 months, 6-12 months, 12-24 months, and more than 24 months. By packaging type, the market is segmented into pouches, glass jars, tetra pak cartons, and others. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, baby specialty stores, pharmacies/drugstores, and online retail stores. By geography, the market is segmented into Brazil, Argentina, Chile, Colombia, Peru, and the Rest of South America.

For each segment, the market sizing and forecasts are done in value terms of USD million.

By Product Type

| Milk Formula |

| Prepared Baby Food |

| Dried Baby Food |

By Age Group

| 0 - 6 Months |

| 6 - 12 Months |

| 12 - 24 Months |

| More than 24 Months |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Baby Specialty Stores |

| Pharmacies/Drugstores |

| Online Retail Stores |

By Geography

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Product Type | Milk Formula |

| Prepared Baby Food | |

| Dried Baby Food | |

| By Age Group | 0 - 6 Months |

| 6 - 12 Months | |

| 12 - 24 Months | |

| More than 24 Months | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Baby Specialty Stores | |

| Pharmacies/Drugstores | |

| Online Retail Stores | |

| By Geography | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is the current size of the South America organic baby food market?

The market is valued at USD 1.11 billion in 2026 and is projected to reach USD 1.53 billion by 2031.

Which product segment leads the South America organic baby food market?

Milk formula leads with a 80.45% share in 2025, reflecting its essential role in infant nutrition.

Which channel is growing fastest for organic baby food sales in South America?

Online retail stores are expanding at a 7.66% CAGR, driven by specialty e-commerce platforms and subscription models.

Why is Argentina the fastest-growing national market in the region?

Economic stabilization and a strong dairy base support rapid uptake of organic milk formula, leading to a 7.15% forecast CAGR.

Page last updated on: