South America Data Center Networking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

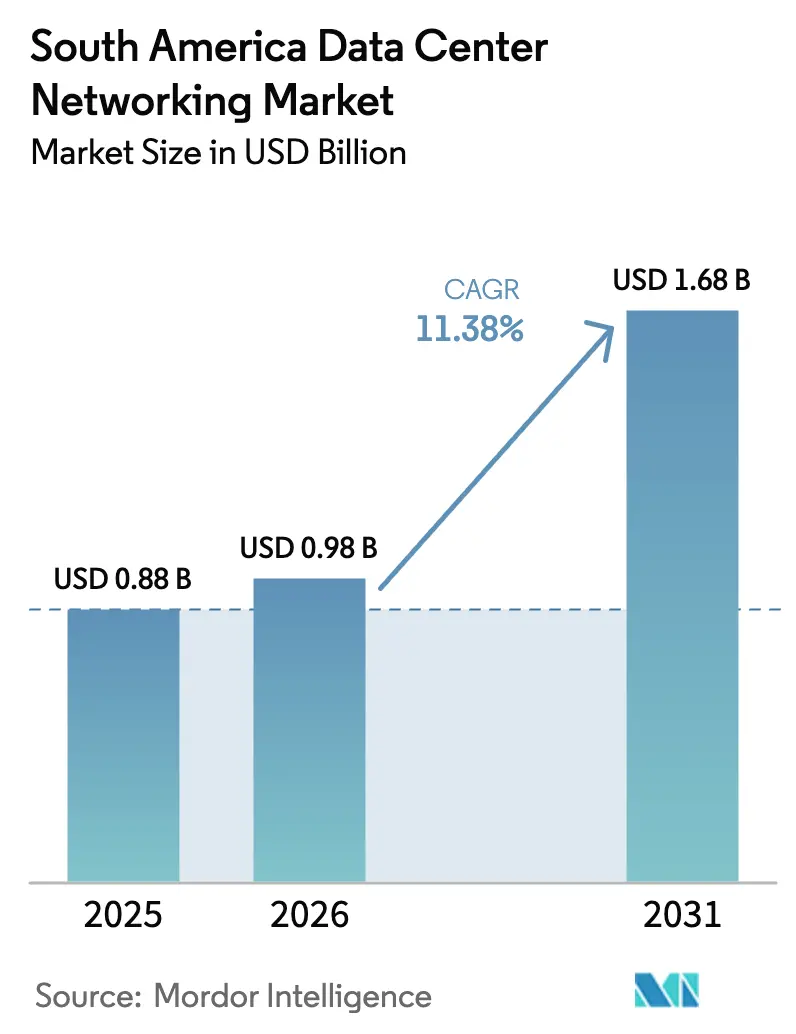

| Base Year Market Size (2025) | USD 0.88 Billion |

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 1.68 Billion |

| Growth Rate (2026 - 2031) | 11.38% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Data Center Networking Market Analysis by Mordor Intelligence

The South America data center networking market size is expected to grow from USD 0.88 billion in 2025 to USD 0.98 billion in 2026 and is forecast to reach USD 1.68 billion by 2031 at 11.38% CAGR over 2026-2031. Robust capital flows from hyperscale cloud providers, national incentives for renewable-powered facilities, and rapid enterprise adoption of hybrid and multi-cloud architectures fuel this sustained growth. Submarine-cable additions along the Atlantic and Pacific coasts strengthen international connectivity, while open-networking ecosystems based on white-box switches and SONiC software drive cost efficiency. Vendors compete intensely around high-bandwidth optical interconnects, intent-based network automation, and integrated security appliances as Latin American organizations modernize data centers to run AI-driven workloads. Supply-chain‐friendly policies such as Brazil’s ex-tariff regime ease import duties on advanced ICT gear, offsetting pricing pressure from regional currency volatility and tariff structures.

Key Report Takeaways

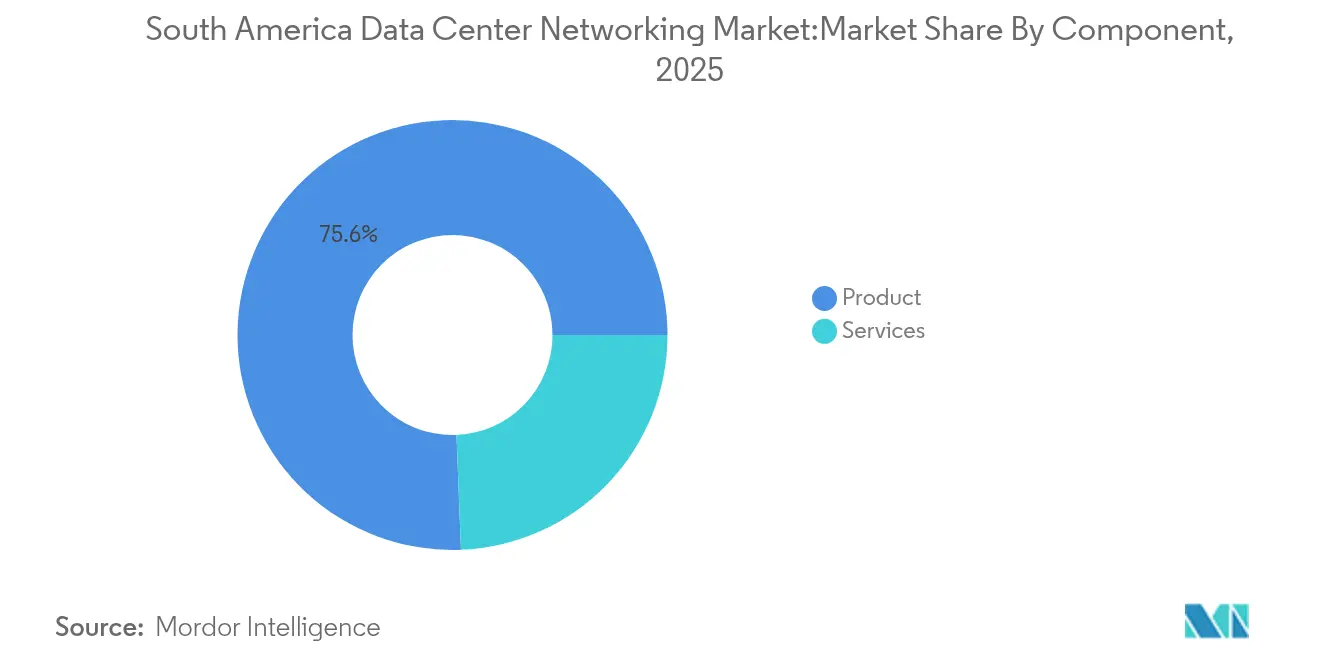

- By component, Products retained 75.63% of 2025 revenue, while Services are projected to expand at an 11.49% CAGR to 2031.

- By end-user, IT & Telecommunications accounted for 36.89% of 2025 revenue; Manufacturing & Industrial is poised for the fastest 11.88% CAGR through 2031.

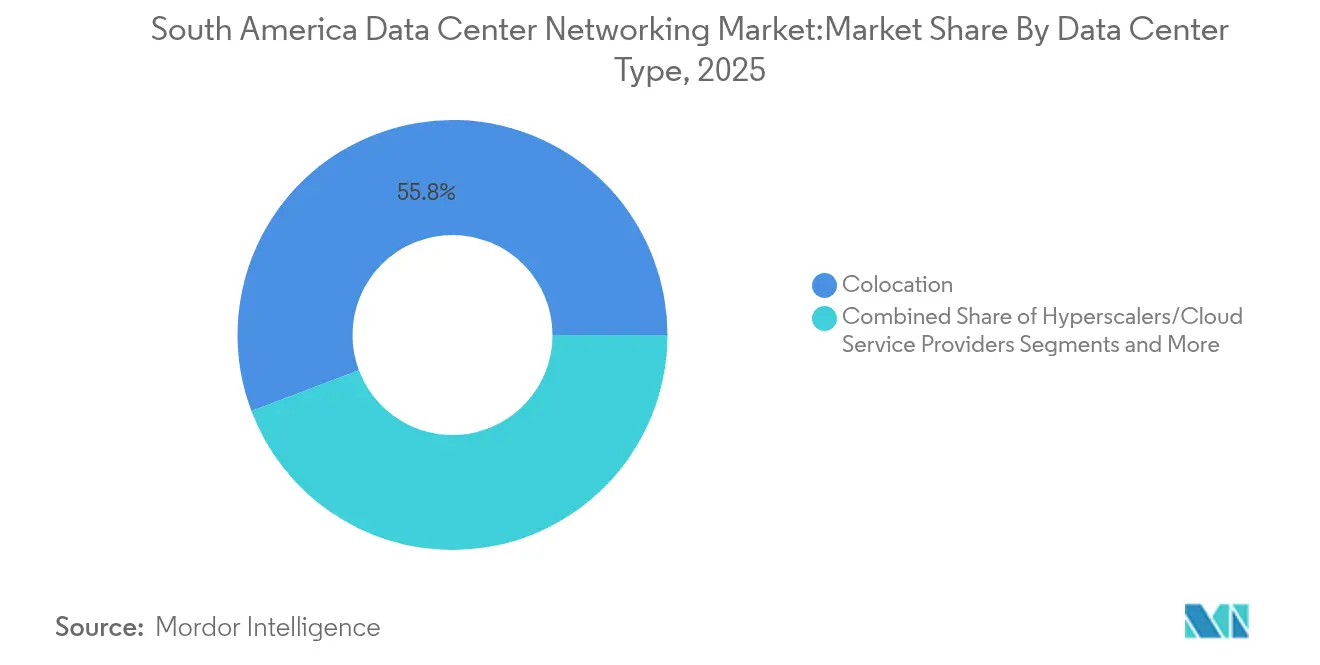

- By data-center type, Colocation sites held 55.75% of 2025 capacity; Hyperscalers & Cloud Service Providers lead growth at a 13.12% CAGR to 2031.

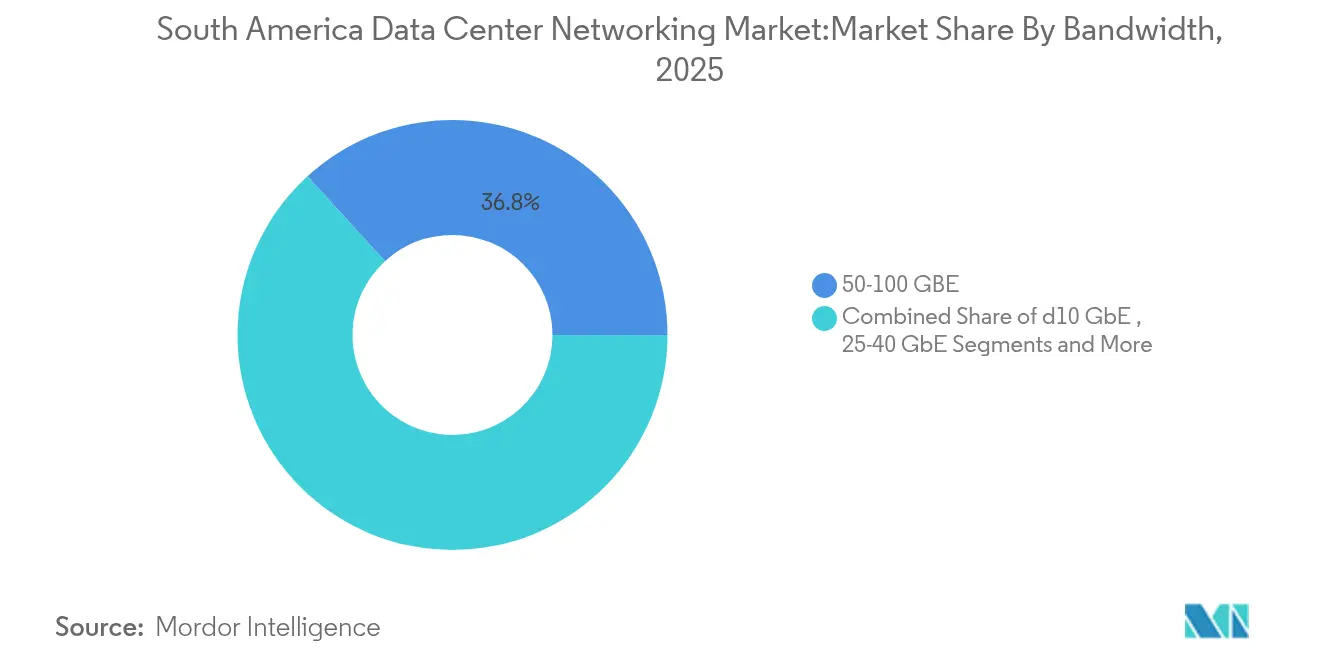

- By bandwidth, 50-100 GbE led with 36.78% of the South America data center networking market share in 2025, whereas greater than 100 GbE is forecast to post a 12.32% CAGR through 2031.

- By Country, Brazil led with 25.08 % of the South America data center networking market share in 2025, whereas Argentina is forecast to post a 11.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Competitive positioning in South america includes both locally based firms and those operating across multiple regions. The market landscape in the global data center networking industry research shows how these players are arranged internationally.

South America Data Center Networking Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing need for cloud storage and reliable application performance | +2.8% | Brazil, Chile, Colombia, Argentina | Medium term (2-4 years) |

| Rising cyber-attacks among enterprises | +2.1% | Brazil & Argentina financial centers | Short term (≤ 2 years) |

| Proliferation of hyperscale data-center builds by global cloud providers | +3.2% | Brazil primary, Chile secondary | Medium term (2-4 years) |

| Surge in submarine-cable landings enabling low-latency coastal hubs | +1.8% | Brazil, Chile, Argentina | Long term (≥ 4 years) |

| Brazil’s renewable-energy incentives for green networking upgrades | +1.1% | National, early São Paulo clusters | Long term (≥ 4 years) |

| Adoption of open networking (white-box + SONiC) cutting CAPEX | +1.5% | Brazil, Chile | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing need for cloud storage and reliable application performance

Enterprises are shifting mission-critical workloads to cloud platforms, which raises throughput and latency requirements inside regional facilities. Banco Itaú’s program to move all core systems to the cloud by 2028 typifies the demand spike, prompting carriers to light new 400G and 800G links. Cirion Technologies has already demonstrated a 1.6 Tb/s single-carrier wavelength between São Paulo and Santiago, proving that optical backbones can stay ahead of AI-era traffic.[1]StockTitan, “Cirion Completes 1.6 Tb/s Trial,” stocktitan.net Storage performance is equally vital for hybrid deployments that synchronize on-premises and cloud repositories in real time.

Rising cyber-attacks among enterprises

Latin-American companies now record 2,569 attacks per week—40% above the global average—pushing CISOs to buy next-generation firewalls, secure SD-WAN, and AI-augmented threat analytics. Mutual Ser EPS, a Colombian insurer, adopted Fortinet’s FortiGate appliances to harden more than 50 branch locations that run multi-cloud applications.[2]Fortinet, “Mutual Ser EPS Secures Multi-Cloud,” fortinet.com Budgets are shifting fast; half of regional firms allocate between USD 10 million and USD 49 million annually to cybersecurity controls

Proliferation of hyperscale data-center builds by global cloud providers

Amazon is placing USD 4 billion in a new Chilean cloud region that comes online in 2026, while AWS and Microsoft combined invested USD 4.5 billion in Brazilian expansions during 2024.[3]BNamericas, “Banco Itaú Cloud Migration Roadmap,” bnamericas.comEach deployment requires leaf-spine fabrics using 25–100 GbE links for general compute and >100 GbE for AI clusters, triggering multi-year hardware refresh cycles at carrier hotels and metro backbones

Surge in submarine-cable landings enabling low-latency coastal hubs

Google’s trans-Pacific cable and Cirion’s SAC2 system are elevating Valparaíso and Fortaleza into latency-sensitive exchange points. Fortaleza now hosts 16 live cables, letting operators deliver sub-60 ms round-trip times to Miami, Luanda, and Lisbon. These facilities deploy dense optical cross-connects and automated fiber monitoring to handle traffic peaks during live-stream events and gaming launches.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing network complexity | −1.8% | Brazil & Chile enterprises | Short term (≤ 2 years) |

| High import tariffs and CAPEX for advanced equipment | −2.3% | Argentina, Colombia | Medium term (2-4 years) |

| Shortage of automation-skilled network engineers | −1.6% | Region-wide | Medium term (2-4 years) |

| Fragmented data-sovereignty regulations | −1.4% | Multinationals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing network complexity

Hybrid-cloud overlays, east-west microsegmentation, and edge bursts expose skill gaps. Enterprises deploying intent-based controllers face multi-vendor API sprawl that strains thin NOC teams. Lack of trained staff delays 400G adoption schedules, inflates consulting reliance, and limits achievable automation depth.

High import tariffs & CAPEX for advanced equipment

Tariffs pushing costs 8–20% higher for routers and leaf switches persuade smaller operators to extend life cycles rather than embrace 800G optics. Brazil’s ex-tariff program counters part of this penalty by exempting 1,495 ICT SKUs from duties, accelerating availability of AI-optimized NICs that are not manufactured domestically.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Accelerate Despite Hardware Dominance

Products anchored 75.63% of 2025 revenue, reflecting heavy outlays on switches, routers, optical transponders, and security appliances that form the bedrock of every data center networking market deployment. Ethernet leaf–spine upgrade cycles shift from 25G/100G toward 400G class, while modular routers integrate SR-MPLS for simplified underlay automation. Vendors synchronize switch ASIC roadmaps with merchant-silicon breakthroughs to meet latency budgets of AI clusters running RDMA over Converged Ethernet.Services expand at an 11.49% CAGR, fueled by managed SDN controllers, lifecycle automation, and white-glove zero-trust overlays for enterprises lacking in-house skill sets. Consulting arms of OEMs bundle network-as-code blueprints plus DevNet-style training that compress deployment lead times. Regional MSPs carve niches by delivering multicloud connectivity hand-offs and ISO 27001-aligned managed detection and response, ensuring compliance across heterogeneous domiciles.

By End-User: Manufacturing Disrupts Traditional IT Leadership

IT & Telecommunications kept a 36.89% revenue lead in 2025 as telco clouds virtualized core network slices and OTT video platforms cached near-edge nodes. Banking retained multi-region active–active data stores to satisfy instant-payment directives, lifting demand for encrypted 100G MAC-sec ports. Yet Manufacturing & Industrial registers the fastest 11.88% CAGR as Industry 4.0 retrofits call for deterministic Ethernet, Time-Sensitive Networking, and private 5G gateways linking PLCs to fog servers. Mining consortia run tele-remote haulage over Cisco URWB links under 10 ms RTT, demonstrating ruggedized optical rings that survive high-vibration pits. Automotive plants spearhead open networking pilots that enforce vendor-agnostic telemetry on CAN-bus digital twins feeding cloud AI quality-control engines.

By Data-Center Type: Hyperscalers Reshape Market Dynamics

Colocation halls comprised 55.75% of live footprint in 2025 and remain pivotal for latency-sensitive metro peering. Neutral facilities diversify with renewable PPAs and sovereign-cloud enclaves to shield regulated customer data. Still, hyperscalers log a 13.12% CAGR as Amazon, Microsoft, and Google pour more than USD 10 billion into South American regions between 2024-2025, architecting multistorey campuses wired at 25/50 kV feeds. The data center networking market share for hyperscalers will approach 40.60% by 2031 as tenants chase predictable cloud availability zones.Scala Data Centers’ planned 4.7 GW AI City in Porto Alegre will rely on fabric switches delivering 64 x 800G ports per chassis for NVLink mesh backplanes that host LLM inference farms. Edge and micro-modular sites spring up along cable landing beaches, where <1 MW pods terminate 800G coherent optics into coastal IPoDWDM supernodes.

By Bandwidth: High-Speed Connectivity Drives Innovation

Ports above 100 GbE exhibit a 12.32% CAGR as training clusters traverse 1.6 Tb/s trunks over 800G DR4+ optics. Conversely, 50-100 GbE continues as the largest slice at 36.78% given its balance of price-per-gig and backward compatibility. The data center networking market size for >100 GbE ports is forecast to hit USD 624.37 million in 2031, underscoring AI and HPC momentum. RoCE v2 acceleration and PFC-free transport shape topological decisions, while IPoDWDM collapses gray optics to curb power envelopes.Legacy ≤10 GbE links linger in branch DCs and archival backup segments that tolerate higher oversubscription. Mid-tier 25-40 GbE lines underpin edge deployments where workloads burst unpredictably yet remain smaller than core-DC AI jobs.

Geography Analysis

Brazil led with 25.08 % of the South America data center networking market share in 2025. São Paulo state concentrates 427.5 MW live draw and another 672 MW in build or planning, propelled by USD 2.7 billion from Microsoft and USD 1.8 billion from AWS. Brazil’s tax-exempt ex-tariff roster accelerates uptake of switch ASICs otherwise unavailable domestically, giving the data center networking market a cost buffer during currency swings. Fortaleza’s 16 cable landings transform Ceará into a continental traffic exchange, reducing round-trip latency to Miami below 55 ms.

Chile rises as a Pacific data-hub candidate backed by December 2024’s National Data Centers Plan, pledging USD 2.5 billion in incentives plus expedited environmental approvals. Amazon’s USD 4 billion Santiago cloud region, slated to go live in 2026, will couple with Google’s trans-Pacific Topaz cable to anchor latency-sensitive trade between Latin America and Asia. Equinix’s USD 130 million Santiago IBX further diversifies operator choices and fosters neutral caching clusters atop 100% renewable power.Argentina is forecast to post a 11.02% CAGR through 2031. Argentina’s national digital-health grid on Red Hat OpenShift scaled transaction volumes 15× in under two years, showcasing demand for scalable underlay fabrics Red Hat. Colombia’s fintech surge and submarine-fiber additions spur adoption of AES-256 MAC-sec for compliance, even as peso volatility and tariff overhead dilute smaller ISPs’ capex budgets. Both nations work on harmonizing cybersecurity statutes to lure multinational tenants wary of fragmented oversight.

Mordor Intelligence tracks the data center networking market across other major regions such as Asia, Europe, and Africa, with additional country-level coverage spanning Chile, Brazil, Italy, Germany, Norway, and Netherlands, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Market concentration remains moderate as entrenched global vendors face white-box commoditization pressures. Cisco, Juniper, and Arista dominate leaf-spine orders, yet Arista’s 27.6% revenue jump to USD 2.005 billion in Q1 2025 underscores demand for its AI-centric 800G platforms. Juniper expands Apstra intent-based fabric blueprints for multi-vendor SONiC estates, while Cisco integrates line-rate AES-256 MAC-sec on 51.2T ASICs and reports USD 8.252 billion Americas revenue in Q1 FY25.

Dell Technologies wins share through open-networking bundles pairing PowerSwitch with SONiC, highlighted by SKY Brazil’s deployment that cut provisioning cycles by 60%. Fortinet leverages regional threat upticks by converging NGFW, SD-WAN, and zero-trust network-access into ASIC-accelerated appliances such as the FortiGate 70G launched in February 2025. HPE couples Cray Slingshot interconnects with NVIDIA Blackwell GPUs in its June 2025 AI Factory blueprint for turnkey liquid-cooled clusters.

South America Data Center Networking Industry Leaders

Cisco Systems Inc.

Huawei Technologies Co. Ltd.

Juniper Networks Inc.

Hewlett Packard Enterprise Development LP

Arista Networks Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: HPE unveiled AI Factory systems built on NVIDIA Blackwell GPUs and new Private Cloud AI platforms, adding turnkey liquid cooling and observability.

- June 2025: Fortinet launched AI-powered Workspace Security suite extending FortiMail protection to browsers and collaboration apps.

- May 2025: Arista Networks posted record USD 2.005 billion Q1 2025 revenue (+27.6% YoY) and introduced Cluster Load Balancing in EOS.

- April 2025: Patria invested USD 1 billion to build a pan-Latin data-center platform.

South America Data Center Networking Market Report Scope

Data center networking refers to the set of technologies, protocols, and hardware used to connect physical and network-based devices and manage the network infrastructure, storage, and processing of application and data. Data center networking is very critical for 100% uptime of data centers. In the current web-connected world, business workloads are executed on single computers, hence leading to the need for data center networking. Networks provide servers, clients, applications, and middleware with a standard plan to stage the execution of workloads and also to manage access to the data produced.

The South American data center networking market is segmented by component type (product (ethernet switches, router, storage area network (SAN), application delivery controller (ADC), and other networking equipment) and services (installation & integration, training & consulting, and support & maintenance)), end-user (IT & telecommunication, BFSI, government, media & entertainment, and other end-users), and country (Chile, Brazil, and the Rest of South America).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Products | Ethernet Switches |

| Routers | |

| Storage Area Network (SAN) | |

| Application Delivery Controllers (ADC) | |

| Network Security Appliances | |

| Software-Defined Networking (SDN) Controllers | |

| Optical Interconnects | |

| Services | Installation and Integration |

| Training and Consulting | |

| Support and Maintenance | |

| Managed Network Services |

| IT and Telecommunications |

| Banking, Financial Services and Insurance (BFSI) |

| Government and Defense |

| Media and Entertainment |

| Healthcare and Life Sciences |

| Manufacturing and Industrial |

| Other End-Users |

| Colocation |

| Hyperscalers/Cloud Service Providers |

| Edge/Micro Data Centers |

| Less than or Equal to 10 GbE |

| 25-40 GbE |

| 50-100 GbE |

| Greater than 100 GbE |

| Brazil |

| Mexico |

| Argentina |

| Rest of South America |

| By Component | Products | Ethernet Switches |

| Routers | ||

| Storage Area Network (SAN) | ||

| Application Delivery Controllers (ADC) | ||

| Network Security Appliances | ||

| Software-Defined Networking (SDN) Controllers | ||

| Optical Interconnects | ||

| Services | Installation and Integration | |

| Training and Consulting | ||

| Support and Maintenance | ||

| Managed Network Services | ||

| By End-User | IT and Telecommunications | |

| Banking, Financial Services and Insurance (BFSI) | ||

| Government and Defense | ||

| Media and Entertainment | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial | ||

| Other End-Users | ||

| By Data-Center Type | Colocation | |

| Hyperscalers/Cloud Service Providers | ||

| Edge/Micro Data Centers | ||

| By Bandwidth | Less than or Equal to 10 GbE | |

| 25-40 GbE | ||

| 50-100 GbE | ||

| Greater than 100 GbE | ||

| By Country | Brazil | |

| Mexico | ||

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the South America data center networking market?

The market is valued at USD 0.98 billion in 2026 and is projected to reach USD 1.68 billion by 2031.

Which component segment is growing fastest?

Services are expanding at an 11.49% CAGR, driven by managed SDN, automation consulting, and skill-gap outsourcing.

Why are Manufacturing & Industrial users adopting data center networking solutions rapidly?

Industry 4.0 initiatives, ultra-low-latency control loops, and private 5G deployments push Manufacturing & Industrial toward a forecast 11.88% CAGR.

Which bandwidth tier is expected to dominate by 2031?

Links above 100 GbE, tied to AI and HPC workloads, will post a 12.32% CAGR, although 50-100 GbE remains the largest share through the forecast horizon.

Page last updated on: