Bed Head Panel Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

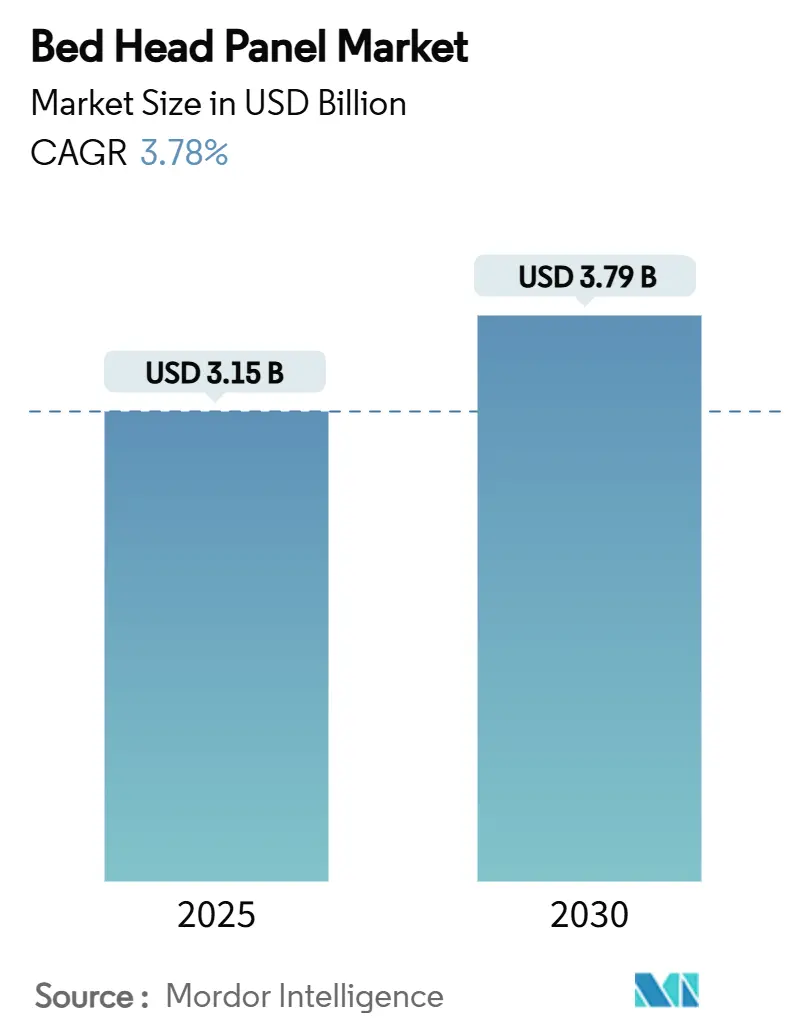

| Market Size (2025) | USD 3.15 Billion |

| Market Size (2030) | USD 3.79 Billion |

| Growth Rate (2025 - 2030) | 3.78% CAGR |

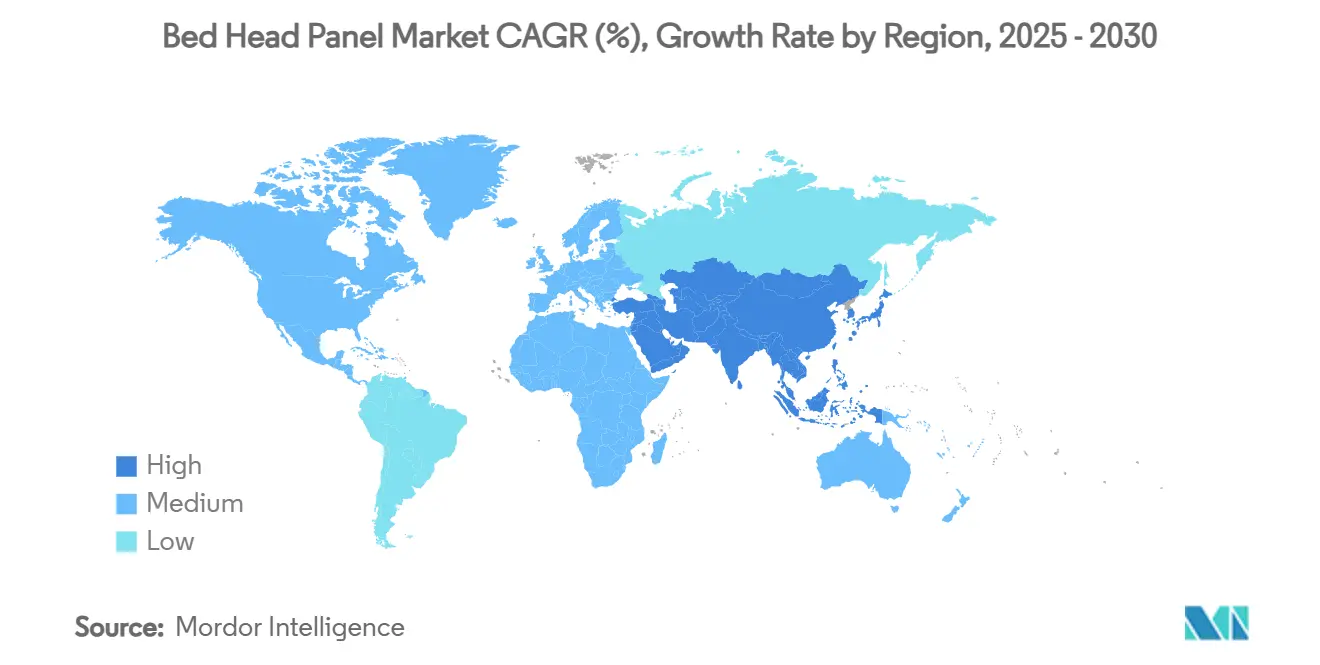

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bed Head Panel Market Analysis by Mordor Intelligence

The bed head panel market size stands at USD 3.15 billion in 2025 and is forecast to reach USD 3.79 billion by 2030, reflecting a 3.78% CAGR during the period. Smart hospital programs, rising compliance standards, and aging-population demand are steering the bed head panel market beyond its traditional role as a conduit for medical gases into the core of connected patient-room ecosystems. Hospitals now specify panels that bundle medical gas, electrical power, data ports, and IoT sensors, turning the product into a strategic infrastructure element. Capital spending aimed at ICU upgrades, pediatric expansions, and modular ward conversions is sustaining steady volume growth despite thinning replacement cycles in mature regions. Competitive intensity remains moderate as certification hurdles, installation know-how, and after-sales networks deter new entrants, while incumbents differentiate through turnkey offerings that pair hardware with software analytics. North America leads on code-driven retrofits, but Asia-Pacific’s pace of hospital construction delivers the fastest unit growth.

Key Report Takeaways

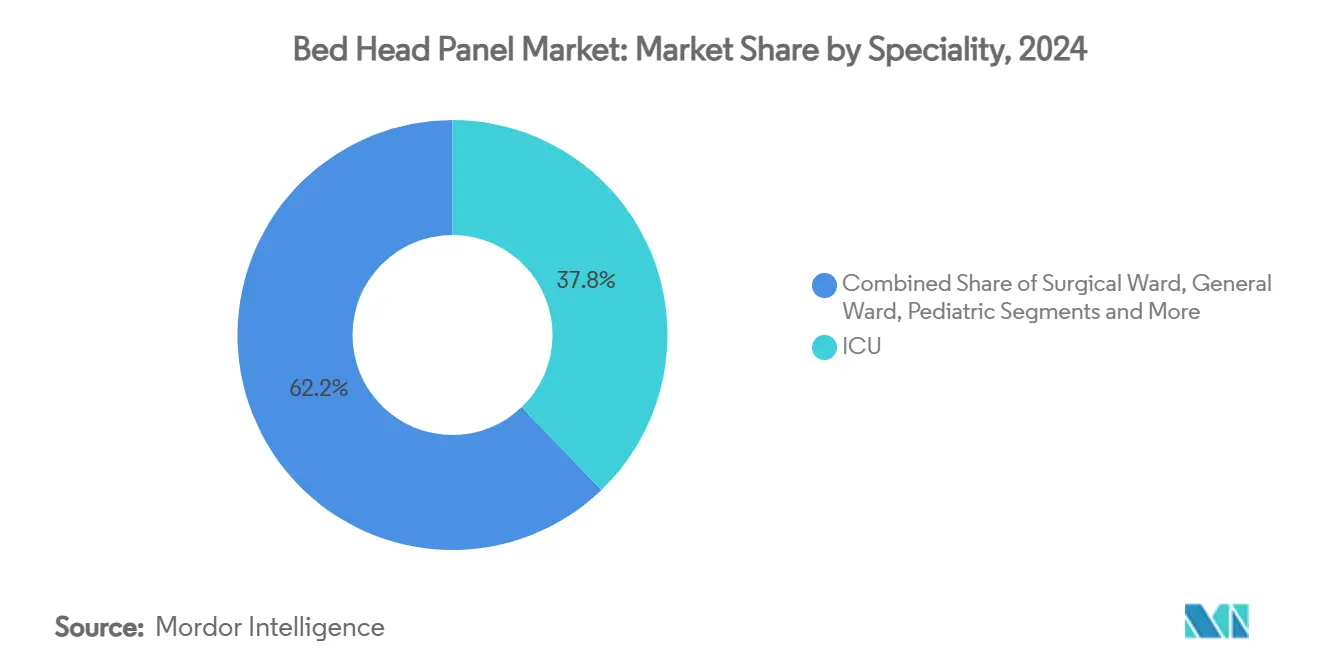

- By specialty, ICU led with 37.81% of bed head panel market share in 2024; pediatric applications are forecast to expand at a 5.68% CAGR through 2030.

- By orientation, horizontal panels held 66% of bed head panel market share in 2024, while pendant/ceiling-boom configurations are advancing at a 6.44% CAGR to 2030.

- By material, aluminum captured 70% share of the bed head panel market size in 2024, whereas composite substrates are projected to grow at a 6.89% CAGR between 2025-2030.

- By technology-integration level, basic analog units accounted for 52% share of the bed head panel market size in 2024; smart IoT-enabled panels are pacing ahead at a 7.56% CAGR through 2030.

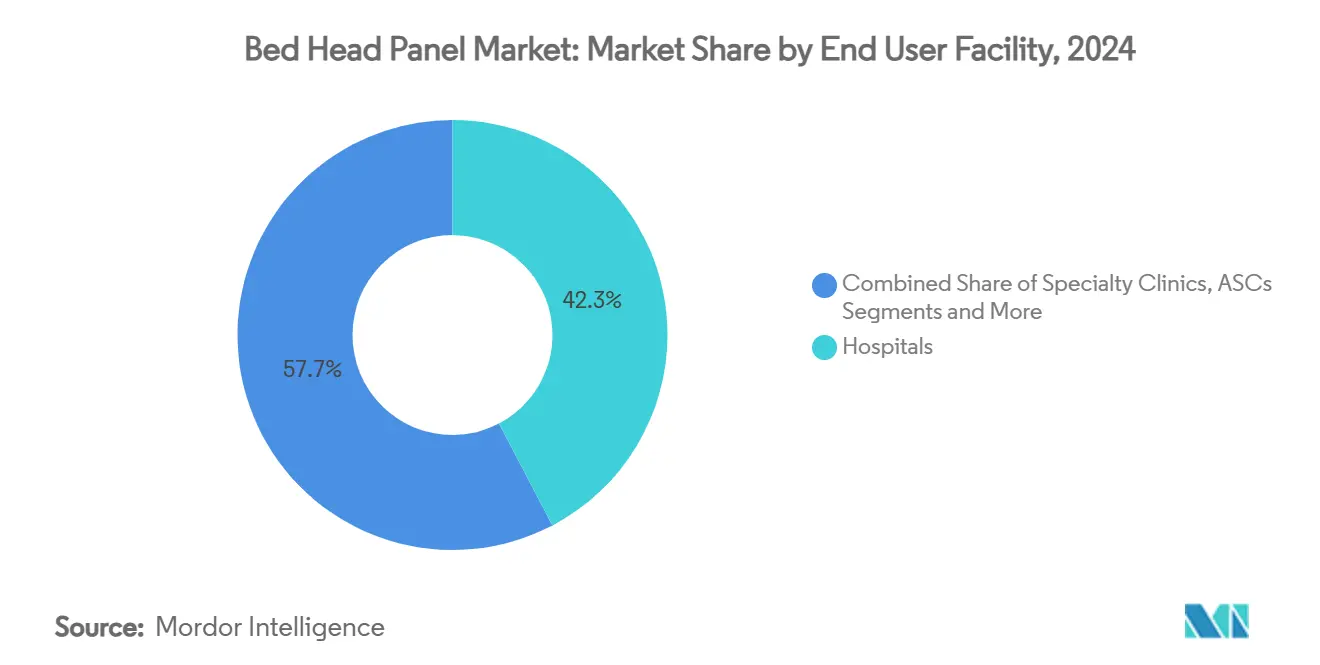

- By end-use facility, hospitals commanded 42.31% of bed head panel market share in 2024, whereas home healthcare settings are poised to record a 7.34% CAGR over the forecast period.

- By geography, North America led with 34.53% of bed head panel market share in 2024, while Asia-Pacific is set to post the fastest growth at a 5.93% CAGR through 2030.

Market Trends and Insights

Drivers Impact Analysis of Bed Head Panel Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing & Chronic-Care Population Swell | +0.8% | North America, Europe, East Asia | Long term (≥ 4 years) |

| Expanding Hospital Infrastructure Outlays | +0.9% | Asia-Pacific, Middle East | Medium term (2-4 years) |

| Compliance Pressure for Integrated Med-Gas & Electrical Safety | +0.6% | Global | Medium term (2-4 years) |

| Modular Hospital Builds Favor Pre-Fabricated Aluminium Panels | +0.5% | Global | Medium term (2-4 years) |

| Adoption of Smart Patient-Room IoT Interfaces | +0.7% | North America, Asia-Pacific | Long term (≥ 4 years) |

| Demand for Antimicrobial Powder-Coated Finishes | +0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ageing & Chronic-Care Population Swell

Increasing life expectancy and a higher prevalence of long-term conditions are lifting demand for high-acuity beds in ICUs and step-down units. The American Hospital Association anticipates adults aged 65+ will exceed 20% of the U.S. population by 2030, triggering a need for 31 million annual inpatient discharges.[1]American Hospital Association, “AHA’s 2025 Environmental Scan Reports Key Trends Shaping the Future of Healthcare,” neohospitals.orgEquivalent demographic pressure is visible in China, where projected health expenditure could climb to USD 33.4 trillion by 2060 as the cohort of seniors grows.[2]Mark Heffernan, “Forecast of Total Health Expenditure on China’s Ageing Population: A System Dynamics Model,” BMC Health Services Research, biomedcentral.com Hospitals are consequently installing smart panels that integrate oxygen, vacuum, electrical circuits, and networked sensors able to support ventilators, infusion pumps, and continuous monitoring. In parallel, secondary facilities are converting into senior-care centers, prompting specialized panel formats that combine acute and residential functionality. The resulting uplift in unit orders gives the bed head panel market a dependable long-run volume baseline.

Expanding Hospital Infrastructure Outlays

Governments and private operators continue to green-light multi-billion-dollar expansion projects. China has surpassed 12,000 public hospitals, each adopting standardized panel specifications to simplify maintenance across campuses. In the United States, certificates of need for 1,700 construction projects underscore a steady retrofit pipeline. Even with inflation and labor bottlenecks, 47% of projects finished on schedule in 2024, demonstrating resilient procurement for core headwall components. Asia-Pacific financial institutions, including the Asian Infrastructure Investment Bank, are funding rural clinics and trauma centers that require code-compliant panels to meet safety benchmarks. The cumulative effect is a medium-term boost of almost one percentage point to the global CAGR.

Compliance Pressure for Integrated Med-Gas & Electrical Safety

Updates to NFPA 99 and IEC 60601-1 extend performance obligations from pipework to the terminal outlet, compelling healthcare facilities to upgrade legacy headwalls. The 2024 NFPA 99 edition introduces stricter carbon-monoxide monitoring and automatic shutdown valves that must reside inside the panel chassis.[3]National Fire Protection Association, “Help Ensure Compliance with the Health Care Facility Code,” nfpa.org The International Electrotechnical Commission’s latest amendment similarly demands proof of essential performance under single-fault conditions. Compliance audits attached to federal reimbursements have accelerated replacement programs, adding specialised features such as gas-quality sensors, circuit separation, and warning beacons. This regulation-led refresh cycle feeds directly into the bed head panel market.

Modular Hospital Builds Favor Pre-Fabricated Aluminium Panels

Off-site construction contracts now specify complete wall modules equipped with aluminium panels that slot into the building envelope. Facilities adopting 80-90% prefab ratios shave months from project schedules and reduce on-site skilled-trade requirements. Aluminium’s light weight, corrosion resistance, and compatibility with antimicrobial powder coatings make it the default substrate for these factory-built headwalls. Specialist vendors deliver plug-and-play assemblies where gas lines, receptacles, and nurse-call circuits are factory-tested before shipment, shortening commissioning time while offering hospitals a predictable cost profile.

Restraints Impact Analysis of Bed Head Panel Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight Capital Budgets in Public Hospitals | -0.5% | Europe, Emerging Markets | Medium term (2-4 years) |

| Aluminium Price Volatility | -0.3% | Asia-Pacific Supply Chain | Short term (≤ 2 years) |

| Space-Saving Power Columns Cannibalising Horizontal Panels | -0.4% | North America, Europe | Long term (≥ 4 years) |

| Local-Content Mandates Hindering Foreign Suppliers | -0.2% | Select Asia-Pacific & Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tight Capital Budgets in Public Hospitals

Deferred maintenance across European public systems reached an estimated USD 243 billion in 2024, forcing administrators to triage infrastructure spending and prolong replacement intervals for bed head panels. Physician-executives often prioritize basic analog models over smart variants to protect clinical budgets. Funding shortfalls slow penetration of IoT headwalls outside flagship projects, shaving half a percentage point off the forecast CAGR.

Aluminium Price Volatility

Rapid swings in LME aluminium contracts inject uncertainty into bill-of-materials costs, complicating long-term quotes for hospital groups negotiating multi-year construction phases. Tier-2 suppliers, heavily concentrated in Asia, run on thinner margins and may delay production until raw-material prices stabilize, extending lead times and creating risk of project delays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Bed Head Panel Market Segment Analysis

By Specialty:

ICU Dominance Drives Technical ComplexityICUs represented the largest slice of the bed head panel market size in 2024 as lifesaving equipment relies on fault-tolerant oxygen, vacuum, and power circuits. High-acuity protocols necessitate integrated alarm systems, redundant gas outlets, and shielded data cabling within the panel chassis. Surgical wards follow with multi-gas needs for anesthesia and post-operative care, while general-ward panels are migrating toward ICU-grade specs to enable surge flexibility. Pediatric care, although smaller in absolute value, is the fastest-expanding niche at a 5.68% CAGR thanks to specialized safety locks, color coding, and child-friendly aesthetics. Emergency departments demand quick-connect configurations that withstand heavy turnover, and neonatal ICUs stipulate ultra-precise flow regulators. The resulting product diversity enlarges the total addressable universe for headwall suppliers, sustaining the broader bed head panel market.

Rising pediatric facility investment introduces design complexity but also premium margins. Panels in children’s wards embed tamper-proof outlets, low-brightness night lighting, and interactive displays that soothe young patients. The higher bill of materials per unit offsets lower volumes, safeguarding revenue growth. ICU refresh cycles lengthen to eight-plus years, so vendors increasingly bundle long-term maintenance contracts, locking in aftermarket cash flows that underpin profitability in the bed head panel industry.

By Orientation:

Horizontal Panels Face Vertical ChallengeHorizontal headwalls still accounted for 66% of bed head panel market share in 2024, a testament to decades-old facility standards and clinician familiarity. Their extended footprint accommodates multiple gas outlets, double electrical circuits, and nurse-call terminals at eye level. Yet pendant booms are winning projects where ceiling infrastructure can shoulder the load, delivering unobstructed wall space for monitors and family seating. Vertical headwalls, while niche, serve retrofit sites where structural elements block long horizontal runs. Architects balance infection-control goals with ergonomic convenience, nudging demand toward hybrid rooms that combine a compact horizontal strip with a ceiling pendant. This blended approach preserves unit sales even as spatial economics shift.

Ceiling-mounted systems also align with clean-room airflow paths, boosting their take-up in isolation rooms and pandemic-preparedness wards. However, the higher capital cost and maintenance complexity of articulated booms prevent rapid displacement of conventional strips, cushioning volume erosion within the bed head panel market over the forecast window.

By Material:

Aluminum Dominance Meets Composite InnovationAluminum panels held 69.8% of the bed head panel market size in 2024 due to ease of machining, corrosion resistance, and compatibility with antimicrobial coatings. Their high strength-to-weight ratio simplifies installation in prefab modules, and intrinsic conductivity enables reliable earthing of electrical circuits. Steel retains a foothold in radiology suites that demand attenuation of stray electromagnetic fields. Composites, led by antimicrobial laminates, are scaling quickly on the back of infection-control mandates. These fibre-reinforced resin panels embed copper or silver micro-particles, delivering continuous biocidal action without compromising structural integrity.

Wood-laminate variants decorate VIP and maternity suites but remain a small share because maintenance crews must respect strict cleaning chemistries. Composite platforms naturally host embedded antennae and BLE beacons used for RTLS, supporting future smart-hospital upgrades. Material innovation therefore pivots the competition from pure metals toward hybrid substrates that marry mechanical durability with digital readiness.

By End-Use Facility:

Hospital Dominance Challenged by Home CareHospitals generated 42.3% of global revenue in 2024, driven by intensive renovation programs and greenfield tertiary complexes that demand thousands of identical panels for economies of scale. Specialty clinics, including dialysis and oncology centers, purchase procedure-room headwalls optimized for single-gas setups, creating a price-sensitive but steady sub-segment.

Home healthcare is the standout growth pocket, expanding 7.34% annually as insurers reimburse remote oxygen therapy and chronic-care monitoring. Vendors miniaturize gas manifolds and integrate Wi-Fi modules to fit residential settings, opening a parallel channel distinct from hospital contractors. Ambulatory surgery centers value compact recovery-bay strips that combine oxygen, suction, and tablet docks for immediate post-anesthetic surveillance. The proliferation of these sites across suburban locations widens geographic dispersion of demand, reinforcing volume stability for the bed head panel market.

By Technology Integration Level:

Smart Systems Gain TractionConventional analog panels still comprise 52.3% of shipments because cost-constrained hospitals favour proven technology with minimal IT overhead. Yet smart IoT-enabled models are the clear growth lever at a 7.56% CAGR, embedding edge processors, FHIR-compatible data gateways, and device charging ports. Intermediate nurse-call-plus-data variants act as a bridge, allowing staged upgrades that reuse existing wiring harnesses.

Major OEMs now bundle cybersecurity hardening and HL7 interfaces, charging subscription fees for cloud dashboards that visualise outlet status and predictive maintenance alerts. The twin revenue streams—hardware and software—raise switching costs, anchoring client relationships and enhancing the competitive moat inside the bed head panel industry.

Geography Analysis

North America Bed Head Panel Market

North America retained 34.5% of global revenue in 2024 thanks to NFPA-driven upgrade cycles and medical-real-estate build-outs. U.S. outpatient buildings averaged 25,000 sq ft in new starts, each requiring headwalls conforming to local fire-code zone separation. Canada’s single-payer system adds periodic block tenders that favour panel assemblies pre-listed to CSA standards.

APAC, Europe and Middle East Bed Head Panel Market

Asia-Pacific is adding acute-care beds at the fastest clip, translating into 5.93% regional CAGR. China plans 2 million institutional elderly-care beds equipped with medical-gas utilities, while Indian hospital chains push into tier-II cities with multi-specialty campuses that standardize on aluminium panels for logistical simplicity. Funding from the AIIB for rural clinics further amplifies uptake in Southeast Asia. Europe exhibits modest growth tied to sustainability retrofits that prioritise low-energy lighting and recyclable materials inside headwalls. The Middle East allocates capital to medical-tourism hubs, often specifying luxury finishes that command premium unit prices. Collectively these trends anchor global growth even as North American replacement cycles mature.

Competitive Landscape

Industry concentration sits in the mid-range. The top five manufacturers collectively hold good share of global revenue, a share high enough to influence pricing but low enough to permit regional specialists. Certification complexity around med-gas welding, electrical isolation, and antibacterial coatings restricts casual entry. Incumbents deepen moats through factory-to-site services that include BIM design, installation supervision, and 10-year maintenance plans.

Digital differentiation is widening. Firms embed proprietary IoT stacks, partner with cloud vendors, or acquire sensor start-ups to offer SaaS dashboards. GE HealthCare’s alliance with AWS on generative AI illustrates a move to pair imaging and headwall data for predictive workflows. Siemens integrates panels into building-automation suites, permitting unified control of lighting, HVAC, and outlet alarms. Price competition remains limited to commoditized analog strips, while smart variants command a 25-30% ASP premium. Market entry barriers are therefore rising even as overall growth remains steady.

Bed Head Panel Industry Leaders

Baxter

Stryker Corporation

Getinge AB

LINET Group SE

Precision UK Ltd

- *Disclaimer: Major Players sorted in no particular order

Bed Head Panel Market Companies Covered in this Report

- Baxter

- Stryker

- Getinge

- LINET Group

- Precision UK Ltd

- Novair Medical

- Tedisel Medical

- Silbermann Technologies

- Paramount Bed Holdings Co.

- Modular Hospitech Pvt. Ltd.

- Medline Industries

- Joerns Healthcare

- Stiegelmeyer

- Pukang Medical

- CR Medisystems Pvt. Ltd.

- Amcaremed Technology Co. Ltd.

- BeaconMedæs (Atlas Copco)

- Dragerwerk

- Shanghai Huifeng Medical

Recent Industry Developments in Bed Head Panel Market

- July 2025: Teleflex completed its EUR 760 million acquisition of BIOTRONIK’s vascular intervention business, broadening its presence in cardiac-care environments where premium bed head panels integrate hemodynamic monitoring ports.

- July 2025: The European Union approved EUR 403 million to accelerate medical-device innovation, part of a funding track that also underwrites connected headwall prototypes.

- March 2025: GE HealthCare and NVIDIA launched an initiative to develop autonomous imaging, reliant on high-bandwidth headwall data channels for ultrasound and X-ray workflows.

Global Bed Head Panel Market Report Scope

Segmentation Overview

| ICU |

| Surgical Ward |

| General Ward |

| Pediatric |

| Emergency |

| Horizontal |

| Vertical |

| Pendant / Ceiling-boom |

| Aluminium |

| Steel |

| Composite |

| Wood-laminate |

| Hospitals |

| Specialty Clinics |

| Ambulatory Surgical Centres |

| Home Healthcare Settings |

| Basic Analog Panels |

| Integrated Nurse-Call & Data Panels |

| Smart IoT-Enabled Panels |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Specialty | ICU | |

| Surgical Ward | ||

| General Ward | ||

| Pediatric | ||

| Emergency | ||

| By Orientation | Horizontal | |

| Vertical | ||

| Pendant / Ceiling-boom | ||

| By Material | Aluminium | |

| Steel | ||

| Composite | ||

| Wood-laminate | ||

| By End-Use Facility | Hospitals | |

| Specialty Clinics | ||

| Ambulatory Surgical Centres | ||

| Home Healthcare Settings | ||

| By Technology Integration Level | Basic Analog Panels | |

| Integrated Nurse-Call & Data Panels | ||

| Smart IoT-Enabled Panels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the bed head panel market?

The bed head panel market is valued at USD 3.15 billion in 2025 and is projected to reach USD 3.79 billion by 2030.

Which segment holds the largest bed head panel market share?

ICU applications lead with 37.81% of global revenue in 2024.

How quickly are smart IoT-enabled panels growing?

Smart panels are advancing at a 7.56% CAGR, the fastest among technology tiers.

Why is Asia-Pacific the fastest-growing region?

Rapid hospital construction, adoption of international safety codes, and senior-care expansion yield a 5.93% regional CAGR.

What material dominates bed head panel construction?

Aluminium accounts for about 70% of global volume thanks to modular-build compatibility and antimicrobial coating adherence.

How will compliance regulations influence future demand?

Stricter NFPA 99 and IEC 60601-1 updates require integrated safety features, driving retrofit purchases of advanced headwalls.

Page last updated on: