Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.75 Billion |

| Market Size (2031) | USD 13.41 Billion |

| Growth Rate (2026 - 2031) | 4.53% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

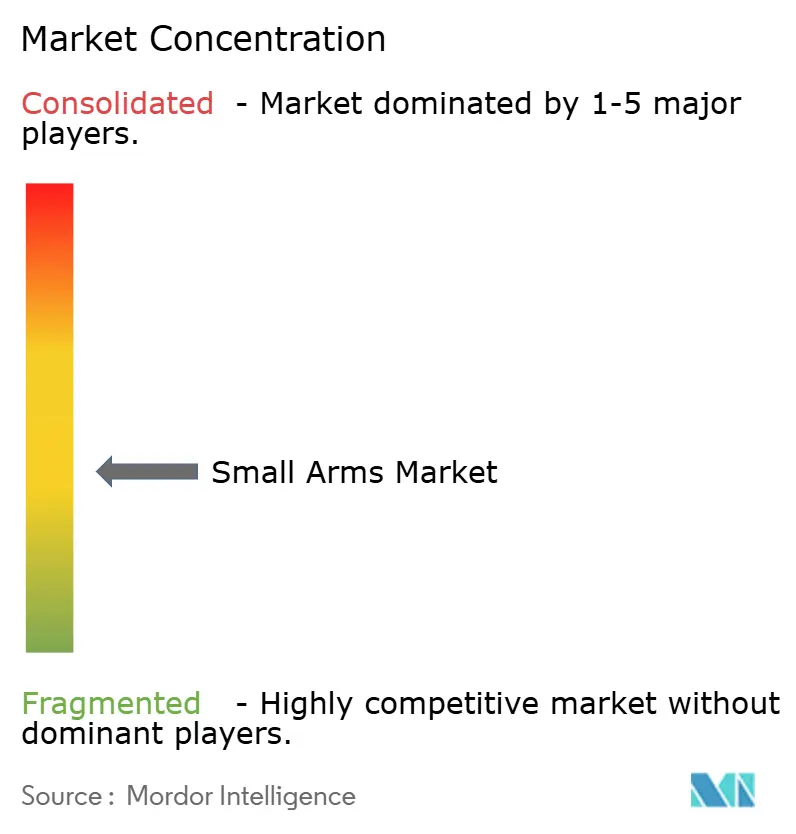

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Small Arms Market Analysis by Mordor Intelligence

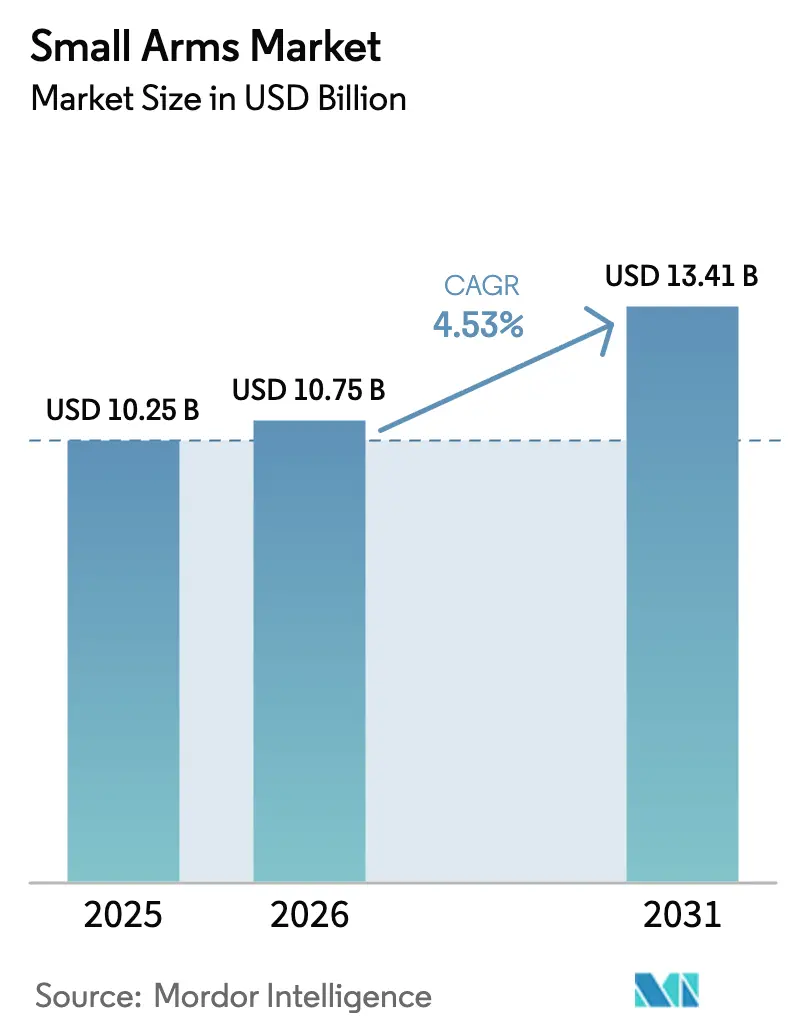

The small arms market size is expected to grow from USD 10.25 billion in 2025 to USD 10.75 billion in 2026, and is forecasted to reach USD 13.41 billion by 2031 at a 4.53% CAGR over 2026-2031. Defense modernization initiatives, consistent civilian demand for personal-protection firearms, and advancements in modular and smart weapon platforms drive this growth. Military programs, such as the US Army’s 10-year Next Generation Squad Weapon (NGSW) initiative valued at up to USD 4.7 billion, highlight the transition from legacy 5.56 mm weapons to advanced 6.8 mm systems designed to counter modern body armor. Civilian demand also remains strong, with the FBI reporting 518 million cumulative NICS checks by August 2025. Additionally, 29 US states adopted constitutional carry laws by 2024, reducing barriers to firearm ownership. In the Asia-Pacific region, defense corridors in countries like India and the Philippines emphasize domestic manufacturing and supply chain resilience, supported by regional capital investments and technology transfers. Meanwhile, ESG-driven divestment and stricter export controls are increasing compliance costs, prompting established manufacturers to adopt consolidation and regionalization strategies.

Key Report Takeaways

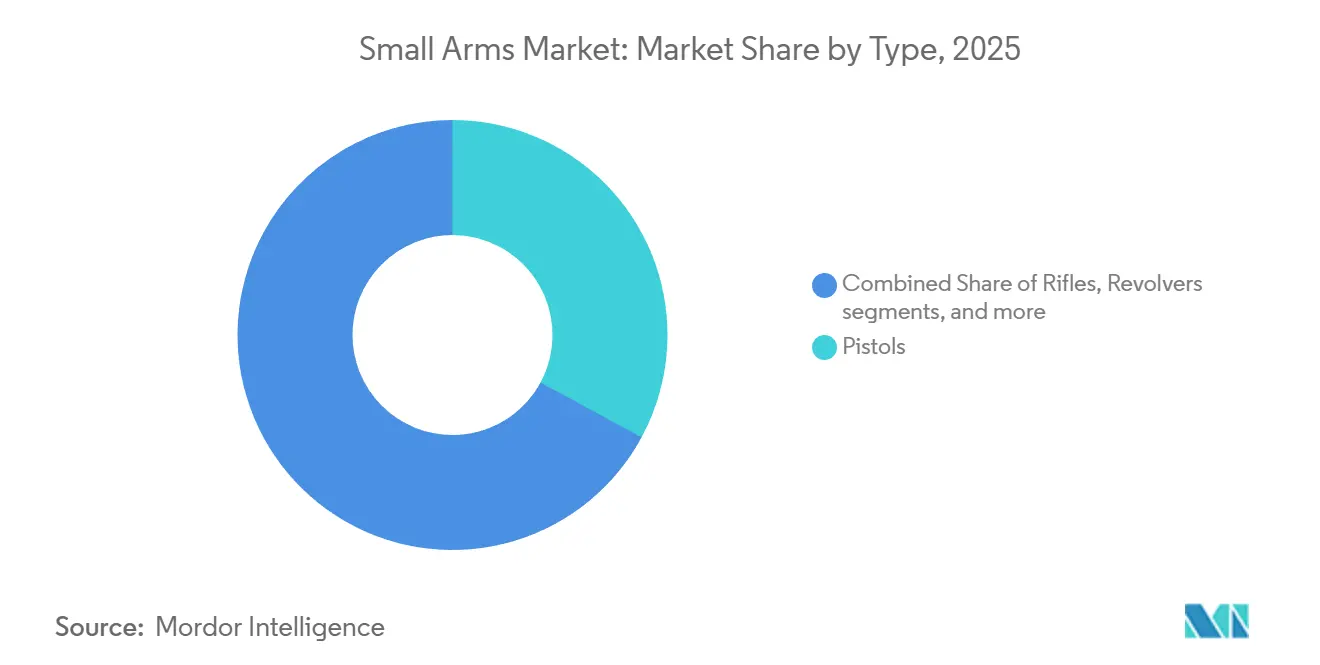

- By type, pistols accounted for 32.89% of the small arms market share in 2025, while assault rifles are projected to grow at a CAGR of 5.12% through 2031.

- By caliber, 9 mm rounds represented 27.64% of the small arms market size in 2025. Meanwhile, 6.8 mm rounds are expected to expand at a CAGR of 7.85% by 2031.

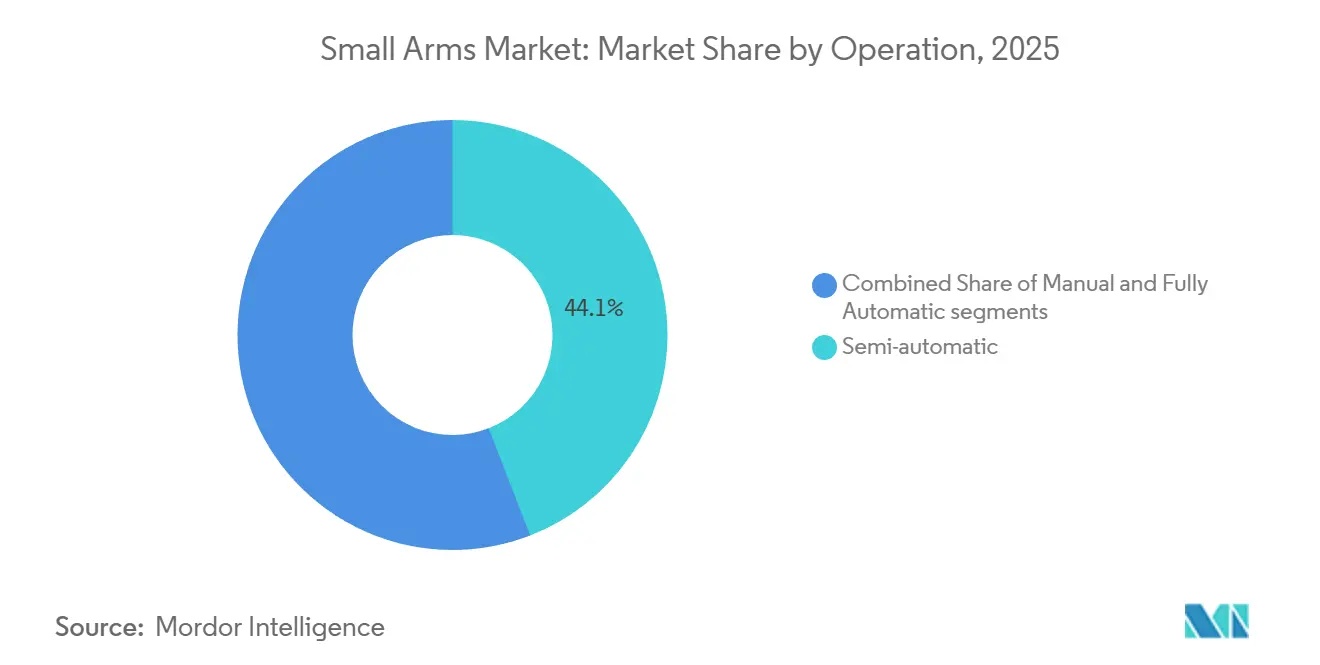

- By operation, semi-automatic systems held a 44.12% share of the small arms market size in 2025, with fully automatic platforms advancing at a CAGR of 5.48% through 2031.

- By end user, civil and law enforcement customers captured 57.96% of the small arms market size in 2025, while the military segment is anticipated to achieve the highest CAGR of 4.98% by 2031.

- By geography, North America maintained a 34.98% share of the small arms market in 2025, whereas the Asia-Pacific region is forecasted to grow at a CAGR of 5.38% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Small Arms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased defense procurement from modernization programs | +1.2% | Global, concentration in NATO and Asia-Pacific | Medium term (2-4 years) |

| Growing civilian demand for personal-protection firearms | +0.9% | North America, expanding to Europe and Asia-Pacific | Long term (≥ 4 years) |

| Increased focus on domestic manufacturing and supply chain resilience | +0.8% | US, Europe, India | Medium term (2-4 years) |

| Shift toward lightweight, modular firearm platforms | +0.7% | Global, led by NATO countries | Medium term (2-4 years) |

| Surge in competitive shooting and hunting sports memberships | +0.5% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Emerging adoption of biometric and smart-locking handguns in law enforcement | +0.3% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Defense Procurement from Modernization Programs

Global militaries are deploying next-generation platforms capable of defeating Level IV armor at ranges exceeding 600 meters, a capability beyond the reach of legacy 5.56 mm weapons. Canada has allocated up to CAD 1 billion (approximately USD 740 million) for 65,401 rifles under its Close Area Suppression Weapon and C7 programs, with deliveries scheduled to begin in 2026. In India, defense production for FY 2024-25 reached INR 1.54 lakh crore (approximately USD 18.5 billion), driven by the production of the AK-203 and 7.62 mm UGRAM rifles.[1]Press Information Bureau, “Defence Production Reaches Record INR 1.54 Lakh Crore,” pib.gov.in These large-scale contracts are accelerating the shift toward 6.8 mm and 7.62 mm calibers, indicating a structural change in demand. Follow-on procurement by NATO allies and Middle Eastern customers is anticipated as interoperability and lethality requirements align. This procurement pipeline ensures multi-year revenue visibility for prime contractors and their component suppliers.

Growing Civilian Demand for Personal-Protection Firearms

Concealed-carry permits reached 21.46 million in 2024, alongside 4.3 million first-time gun owners in 2023. While permit numbers declined as more states adopted constitutional carry laws, unit sales remained above pre-pandemic levels, reflecting sustained demand. Consumers are increasingly opting for compact, optics-ready pistols, such as the Glock 43X and SIG P365, which combine sub-compact frames with 10-to 15-round magazines. First-time gun owners are younger and more diverse, expanding the market for accessories and training services. This trend has led to higher sales of holsters, red-dot optics, and personal-defense ammunition. The civilian segment provides consistent cash flow, offsetting the cyclical nature of military budgets.

Surge in Competitive Shooting and Hunting Sports Memberships

The firearms industry supported 384,437 US jobs and generated USD 90.06 billion in total economic output in 2023. Excise taxes under the Pittman-Robertson Act contributed USD 944 million to conservation funding, which supports the development of new shooting ranges and encourages participation.[2]National Shooting Sports Foundation, “2024 Firearms and Ammunition Industry Economic Impact Report,” nssf.org Entry-level competitive events, such as the Precision Rifle Series, USPSA, and 3-Gun, charge match fees ranging from USD 50 to USD 150 and require equipment kits costing over USD 1,500. Younger participants often develop long-term brand loyalty, upgrading rifles, optics, and triggers as their skills improve. Investments in range infrastructure by the US Department of the Interior help alleviate capacity constraints. These factors collectively increase average transaction values and stabilize revenue for manufacturers and retailers.

Shift Toward Lightweight, Modular Firearm Platforms

Modular firearm platforms allow caliber changes within a single serialized receiver, reducing life-cycle costs for agencies and enthusiasts. For example, the Primary Weapons Systems UXR, priced at USD 2,650, enables users to switch between 5.56 mm, .300 BLK, and 6.5 Grendel barrels. Similarly, SIG Sauer’s MCX offers flexibility across .300 BLK, 5.56 mm, and 7.62 × 39 mm calibers, minimizing armory inventory. Beretta’s BRX1 Strata combines quick-change barrels with sub-MOA accuracy, catering to precision hunters. Innovations such as powered Picatinny rails, patented in 2019, centralize energy for optics and lasers, reducing weight and cable clutter. These design features are rapidly transitioning from special operations to civilian markets, driving upgrade cycles and boosting accessory sales.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ammunition supply chain disruptions from primer material shortages | -1.1% | Global, with acute impact on US and European manufacturers | Short term (≤ 2 years) |

| Stricter end-use monitoring and export control regulations | -0.9% | US and European exporters | Short term (≤ 2 years) |

| Reduced financing due to ESG-aligned divestment trends | -0.6% | North America and Europe | Medium term (2-4 years) |

| Technological substitution from gunshot detection and surveillance systems | -0.4% | North America and Europe, emerging in Asia-Pacific urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter End-Use Monitoring And Export Control Regulations

The US Directorate of Defense Trade Controls enforces ITAR licensing and Blue Lantern post-shipment checks, increasing compliance costs for exporters. SIG Sauer’s USD 11 million penalty for improper exports has heightened scrutiny, prompting companies to expand their legal and audit teams. The EU’s updated Common Position requires human rights and diversion risk assessments, adding administrative burdens. For smaller manufacturers, these overhead costs can represent several percentage points of revenue, effectively limiting their export opportunities. Delays in compliance processes can also jeopardize delivery timelines, undermining buyer confidence and opening the door to competing bids.

Reduced Financing Due To ESG-Aligned Divestment Trends

Institutional investors such as CalPERS and the New York State Common Retirement Fund have divested from firearms holdings, while Norway’s sovereign fund has excluded several manufacturers. Major banks now restrict lending unless clients adopt specific “best practices,” which increases borrowing costs and reduces the availability of credit. Smith & Wesson reported losing tens of millions of dollars in contracts due to ESG pressures, prompting the company to relocate from Massachusetts to Tennessee to maintain its manufacturing viability. Limited access to capital can delay R&D, constrain inventory, and deter potential acquisitions, driving consolidation among financially stronger players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Pistols Retain Lead While Assault Rifles Drive Growth

Pistols accounted for 32.89% of the small arms market share in 2025, driven by increased adoption for concealed carry and standardization as duty weapons among law enforcement agencies. Glock holds over 65% of US law enforcement contracts, while SIG Sauer's P320 Modular Handgun System, with its interchangeable grip modules and slide lengths, boosts aftermarket revenue. Revolvers continue to lose market share, and shotguns remain specialized for breaching and less-lethal applications. Assault rifles are expected to grow at a 5.12% CAGR, surpassing the overall small arms market, supported by programs such as India's AK-203 and the US's 6.8 mm XM7 rollout. Their higher unit value and volume potential position them as significant revenue drivers for prime contractors.

Upgrades to assault rifles also stimulate demand for optics, suppressors, and training kits, expanding the accessory ecosystem. Weapon-specific accessories often account for 20-30% of life-cycle costs, thereby reinforcing platform dependency. Law enforcement and military buyers standardize spare parts inventories and armorer certifications around selected models, increasing switching costs. As legacy fleets age, procurement cycles align, enhancing visibility of the order book through 2031. Marketing efforts emphasize modular rails and ambidextrous controls, which reduce training time and encourage broader adoption.

By Caliber: 9 mm Dominance Faces 6.8 mm Disruption

The 9 mm caliber held a 27.64% share of the small arms market in 2025, supported by NATO standardization and a large installed base. The FBI’s 2014 return to 9 mm validated improved terminal ballistics, prompting additional agency transitions. However, 6.8 mm rounds are projected to grow at a 7.85% CAGR, driven by the US Army’s adoption of 6.8 × 51 mm cartridges for the XM7 and XM250. If NATO adopts a common 6.8 mm standard, ammunition suppliers may face retooling costs but benefit from long-term demand visibility.

The transition to 6.8 mm introduces logistical challenges, including heavier cartridges that reduce soldier loadouts and increase costs by 30-40% compared to 5.56 mm. Interim dual-caliber inventories complicate training and maintenance. Despite these challenges, the performance advantages against advanced armor make 6.8 mm rounds appealing for frontline units. Civilian adoption remains limited due to higher ammunition costs, though precision-rifle enthusiasts show early interest, suggesting potential crossover as prices stabilize. Manufacturers with vertically integrated ammunition production are well-positioned to capture value as the caliber shift progresses.

By Operation: Semi-Automatic Prevalence Meets Full-Auto Uptrend

Semi-automatic firearms represented 44.12% of the small arms market in 2025, driven by AR-15-pattern rifles and striker-fired pistols. Over 24 million AR-15 variants are in civilian hands in the US, sustaining strong demand for spare parts and accessories. Fully automatic systems, restricted to military and select law enforcement use, are forecast to grow at a 5.48% CAGR, supported by the XM250 program and India’s ASMI machine pistol rollout.

Manual-operation firearms, such as bolt-action precision rifles and pump-action shotguns, remain relevant for hunting and sniper roles but contribute minimal growth. Semi-automatic platforms benefit from aftermarket customization, with features like optics-ready receivers and drop-in triggers increasing per-unit revenue. Fully automatic procurement cycles are less frequent but high in value, often bundled with advanced suppressors and thermal optics. OEMs offering comprehensive solutions gain an advantage in tenders that prioritize total system cost.

By End-User: Civil and Law Enforcement Hold Majority, Military Spending Accelerates

Civilian and law enforcement users accounted for 57.96% of the small arms market in 2025, driven by US consumer demand and agency replacements. The National Shooting Sports Foundation reported USD 90.058 billion in economic output, highlighting the sector’s contribution to employment and tax revenues. Military spending, however, is expected to grow faster at a 4.98% CAGR, fueled by NATO’s 2%-of-GDP defense spending commitment and urgent platform upgrades following the Russia-Ukraine conflict.[3]

Civilian purchases are split between affordability for first-time buyers and premium features for enthusiasts. Law enforcement procurement focuses on competitive tenders that emphasize life-cycle costs, warranty terms, and training services. Military modernization efforts often bundle small arms with suppressors, innovative optics, and data-fusion accessories, increasing average contract values. Vendors that localize production or partner with state-owned enterprises benefit from preferential offsets and expedited approval processes.

Geography Analysis

North America maintained a 34.98% share of the small arms market in 2025, supported by 518 million cumulative FBI background checks and 21.46 million active concealed-carry permits in 2024. Canada's CAD 1 billion (USD 0.73 billion) Close Area Suppression Weapon procurement and Mexico's restrictive civilian firearm laws highlight contrasting national approaches. In the US, constitutional carry statutes have reduced permitting revenues but increased unit sales, sustaining aftermarket demand despite ESG divestment pressures from funds such as CalPERS.

The Asia-Pacific region is expected to achieve a 5.38% CAGR through 2031. Key drivers include India's INR 1.54 lakh crore (USD 18.5 billion) defense production milestone, the Philippines' self-reliance legislation, and South Korea's expanding rifle exports. Japan's introduction of the Howa Type 20 and Australia's Thales EF88 Austeyr reflect efforts to enhance sovereign capabilities. Meanwhile, China's Type 191 upgrade advances domestic self-sufficiency but faces limited export opportunities due to geopolitical tensions.

Europe, South America, and the Middle East and Africa collectively account for the remaining market share. In Europe, the updated Firearms Directive has tightened civilian firearm regulations, while defense spending has increased as countries replenish stocks depleted by aid to Ukraine. In South America, Brazil's civilian firearm ownership increased by 100% between 2019 and 2022, although recent political changes have introduced uncertainty. Middle Eastern markets are heavily investing in local production, with Saudi Arabia's SAMI and the UAE's EDGE consolidating manufacturing under the mandates of Vision 2030. Israel Weapon Industries exports to over 30 countries, further strengthening its market presence in the region. In Africa, the market remains fragmented; South Africa's Denel faces financial challenges, while Egypt continues to operate AK-pattern assembly lines for domestic use.

Competitive Landscape

The competitive intensity in the small arms market is moderate, with key players such as Glock, SIG Sauer, Smith & Wesson, Sturm, Ruger & Co., Beretta, Heckler & Koch, and FN Herstal maintaining significant installed bases. Differentiation primarily revolves around modularity and intelligent integration. For instance, SIG Sauer’s MCX rifle and BDX 2.0 ballistic-data exchange system integrate sensors and optics, enabling shooters to automatically adjust holds. Similarly, Primary Weapons Systems’ UXR enhances platform utility by offering expanded caliber options through the Xchange system. In the emerging smart gun niche, Biofire has established a first-mover advantage by shipping consumer smart guns and obtaining certification in California.

Domestic manufacturing partnerships are fostering regional market traction. Examples include Indo-Russian Rifles producing AK-203s in India, the Philippines collaborating with South Korea on K2 rifles, and SAMI consolidating Saudi demand under a unified framework. Additionally, ESG-linked funding constraints are influencing market dynamics, encouraging private ownership structures or sovereign backing. This trend is exemplified by Smith & Wesson’s relocation to Tennessee and the impact of fund-exclusion lists on several of its competitors.

Technological advancements, such as the powered Picatinny rail, are streamlining power distribution for optics and lasers, making them particularly appealing to special operations budgets. While niche disruptors like Biofire operate with relatively low capital, raising USD 38 million compared to incumbents’ annual R&D budgets exceeding USD 100 million, regulatory challenges are delaying the widespread adoption of smart-gun mandates. This delay provides established players with time to develop comparable technologies or acquire innovative startups.

Small Arms Industry Leaders

SMITH & WESSON BRANDS, INC.

Sturm, Ruger & Co., Inc.

SIG SAUER, Inc.

GLOCK Gesellschaft m.b.H.

FN Browning Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The US Army officially granted Type Classification to SIG Sauer's XM7 rifle and XM250 automatic rifle, confirming their compliance with standards for widespread use. This approval solidified a USD 4.7 billion contract, representing a significant step in replacing the M4 and M249 with the new 6.8 × 51 mm weapons designed to enhance next-generation soldier lethality. Initial concerns regarding weight and fumes were addressed during the development process.

- April 2025: The Defence Research and Development Organisation (DRDO) introduced its prototype of a 6.8 x 43 mm assault rifle. This model includes a polymer 30-round magazine with metal inserts and a telescopic stock. It combines the stopping power of a 7.62x39 mm round with reduced weight, making it a potential standard-issue firearm for the Indian Army.

- January 2025: Kalashnikov Concern JSC delivered the initial batch of Model 2023 AK-12 rifles as part of government contracts scheduled for completion by 2025. The AK-12 is the primary automatic weapon for the Russian Armed Forces, with consistently high annual production volumes.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global small arms market as the yearly factory-gate value of newly produced, man-portable firearms up to 12.7 mm caliber, including pistols, revolvers, rifles, shotguns, sub-machine guns, and light machine guns, supplied to military, law-enforcement, and civilian users.

Scope Exclusions: Crew-served weapons above 12.7 mm, replica or deactivated guns, aftermarket parts, and accessories remain outside scope.

Segmentation Overview

- By Type

- Pistols

- Revolvers

- Rifles

- Assault Rifles

- Sniper Rifles

- Others

- Machine Guns

- Light Machine Guns

- Heavy Machine Guns

- Shotguns

- Other Types

- By Caliber

- 5.56 mm

- 6.8 mm

- 7.62 mm

- 9 mm

- 12.7 mm

- Other Calibers

- By Operation

- Manual

- Semi-automatic

- Fully Automatic

- By End User

- Civil and Law Enforcement

- Civilian Protection

- Hunting and Sporting

- Other End Users

- Military

- Civil and Law Enforcement

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews with procurement officers, wholesalers, range operators, and shooting-sport coaches across North America, Europe, Asia-Pacific, and the Middle East. These exchanges, recorded under Chatham House rules, clarified realistic transfer prices, informal gray-market flows, shipping lead times, and caliber migration plans, enabling us to close gaps left by desk research.

Desk Research

We first mine authoritative open data such as SIPRI defense-spending tables, UN Comtrade shipment codes, Small Arms Survey production tallies, Eurostat import logs, and ATF AFMER manufacturing files. We then layer in patent counts from Questel and contract headlines captured within Dow Jones Factiva. Our team also screens company 10-Ks through D&B Hoovers and policy releases from NATO and SAAMI, which lets us detect cyclical procurement spikes before crunching numbers. These examples illustrate the wider set of references reviewed; many more sources inform data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down production-plus-trade construct builds regional consumption pools that are stress-tested through sampled average-selling-price × volume snapshots from manufacturer roll-ups. Key variables like defense capital outlays, active-duty strength, new firearm permits, hunting-license counts, and caliber replacement rates feed a multivariate regression generating 2025-2030 projections. Where bottom-up inputs are thin, historic import ratios bridge gaps before final reconciliation. This is where Mordor Intelligence differentiates, because the model can stress-test alternative scenarios such as accelerated 6.8 mm adoption.

Data Validation & Update Cycle

Outputs face anomaly screens, ±7 percent variance checks, cross-model triangulation, and dual-analyst review. We refresh models each year; interim events, major tenders, export bans, and tariff shifts trigger unscheduled updates, after which a lead analyst signs off so clients receive the latest view.

Why Mordor's Small Arms Baseline Commands Reliability

Published estimates often diverge because firms vary scope focus, price year, and refresh cadence.

The benchmark below highlights 2025 differences.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.29 B (2025) | Mordor Intelligence | - |

| USD 8.90 B (2022) | Global Consultancy A | Excludes civilian sales; dated base year |

| USD 9.46 B (2024) | Industry Publisher B | Handgun-weighted scope |

| USD 8.92 B (2023) | Market Study C | Bundles light weapons with small arms |

The comparison shows that our live primary checks, clearly delimited scope, and annual refresh give decision-makers a transparent, dependable baseline traceable to verifiable drivers.

Key Questions Answered in the Report

What is the current global size of the small-arms sector and its projected growth to 2031?

The small arms market is valued at USD 10.75 billion in 2026 and is forecasted to reach USD 13.41 billion by 2031, registering a CAGR of 4.53% during the forecast period.

Which firearm type generates the largest share of global revenue today?

Pistols account for 32.89% of 2025 worldwide sales, reflecting law-enforcement preferences and sustained concealed-carry demand.

Why is 6.8 mm ammunition drawing heightened procurement interest?

US Army adoption of 6.8 × 51 mm weapons for improved body-armor penetration has spurred allied evaluations, pushing the caliber toward a 7.85% CAGR through 2031.

How large is civilian firearm ownership in the United States right now?

The FBI has processed 518 million cumulative NICS background checks as of August 2025, underscoring the depth of civilian holdings.

Which region is expected to expand fastest by 2031?

Asia-Pacific is projected to grow at a 5.38% CAGR, powered by India’s defense corridors and the Philippines’ self-reliant production policies.

How are ESG-driven divestments affecting firearm manufacturers?

Pension-fund and bank pullbacks raise borrowing costs; Smith & Wesson reported tens of millions in lost business due to ESG pressure.

Page last updated on: