Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 43.10 Billion |

| Market Size (2026) | USD 45.01 Billion |

| Market Size (2031) | USD 54.89 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Fuel Station Market Analysis by Mordor Intelligence

The Saudi Arabia Fuel Station Market size is projected to be USD 43.10 billion in 2025, USD 45.01 billion in 2026, and reach USD 54.89 billion by 2031, growing at a CAGR of 4.05% from 2026 to 2031.

Momentum rests on three parallel forces: a 16.8% surge in 2024 new-vehicle registrations that expanded the national parc to 15.8 million units, the diesel-price doubling that tested price elasticity yet widened retail spreads, and Vision 2030 mandates that funnel private capital into multi-energy forecourts able to dispense gasoline, diesel, electricity, and hydrogen. While gasoline retains transactional primacy, alternative fuels are scaling at a 25.3% growth, providing a hedge against looming efficiency norms and the Saudi Green Initiative. Station operators are racing to re-balance economics as Aramco’s monthly price caps leave only 5–8 halalas per-liter gross margin, tilting profit pools toward convenience retail, quick-service restaurants, and fintech-enabled loyalty programs. Foreign incumbents such as ADNOC Distribution, ENOC, and OOMCO have entered to replicate high-margin non-fuel blueprints honed in the UAE and Oman, intensifying network upgrades and accelerating consolidation across the Saudi Arabia fuel station market.

Key Report Takeaways

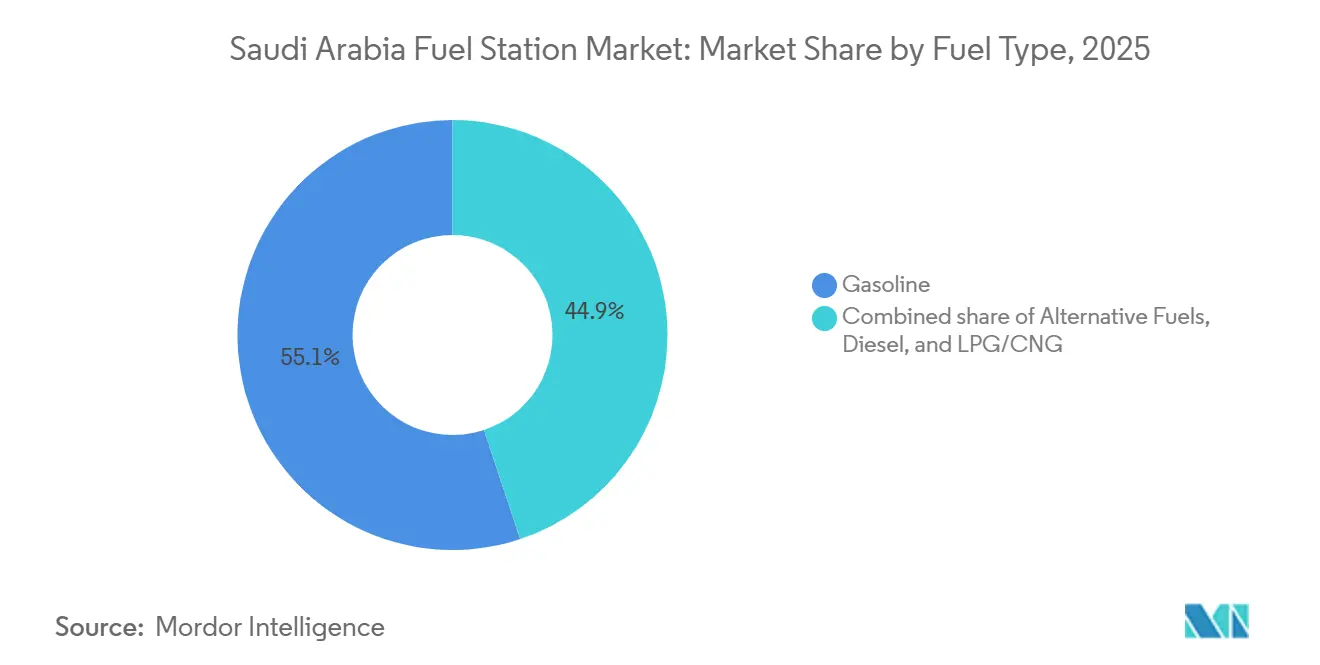

- By fuel type, gasoline led with 55.1% of the Saudi Arabian fuel station market share in 2025, whereas alternative fuels are projected to post a 25.3% CAGR through 2031.

- By service offering, fuel-and-convenience-store formats captured 51.5% revenue in 2025; multi-energy hubs integrating EV and hydrogen dispensing are forecast to grow at a 20.7% CAGR to 2031.

- By station format, traditional full-service sites held a 49.9% share in 2025, while highway service plazas are set to expand at a 6.2% CAGR over 2026-2031.

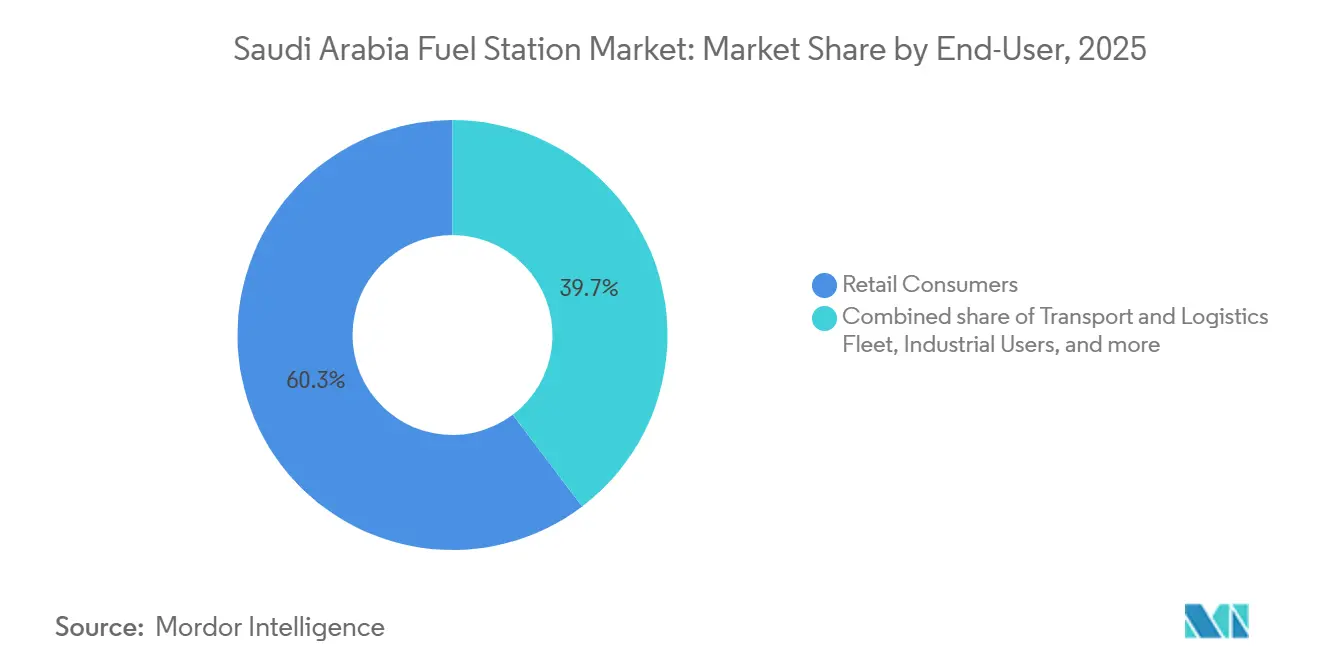

- By end user, retail motorists accounted for 60.3% demand in 2025 and transport-and-logistics fleets represent the fastest-growing cohort at 6.9% CAGR to 2031.

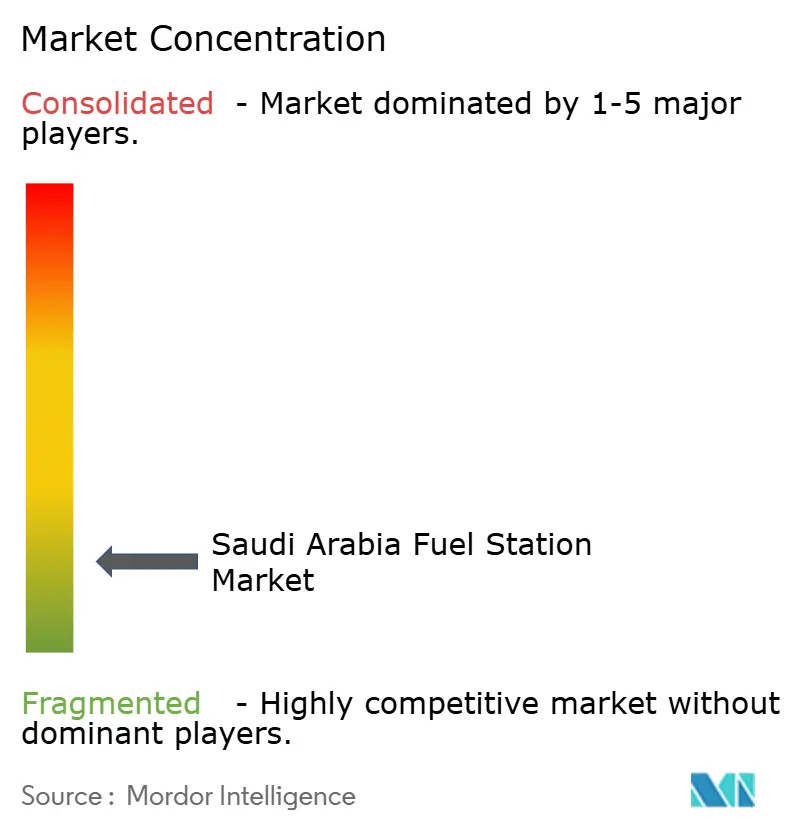

- SASCO, Aldrees, Petromin, the Aramco–TotalEnergies Sahel venture, and NAFT (now folded into SASCO) collectively controlled roughly 25–30% of the Saudi Arabia fuel station market in 2025, underscoring a moderately fragmented competitive field.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Fuel Station Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising light-vehicle parc post-COVID rebound | +0.9% | Riyadh, Jeddah, Dammam metros | Short term (≤ 2 years) |

| Acceleration of giga-projects (NEOM, Qiddiya, Red Sea) | +0.7% | Western & Central corridors | Medium term (2-4 years) |

| Fuel-price liberalization attracting private capex | +0.6% | Nationwide urban nodes | Medium term (2-4 years) |

| Modern convenience-retail formats boosting forecourt revenue | +0.5% | Major cities | Short term (≤ 2 years) |

| RFID / mobile pay fueling experience upgrades | +0.3% | National | Short term (≤ 2 years) |

| Uniform-design mandate forcing network modernization | +0.4% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Light-Vehicle Parc Post-COVID Rebound

New-vehicle registrations jumped 16.8% in 2024, lifting the parc to 15.8 million units and directly raising throughput at the average Saudi Arabian fuel station market forecourt.[1]Saudi Gazette, “Saudi Arabia Vehicle Registration Statistics 2024,” SAUDIGAZETTE.COM.SA Passenger-car demand rebounded as consumer credit loosened and Vision 2030 construction reopened, prompting chains to retrofit legacy sites with automated dispensers that add 15–20% pump productivity at peak times. SASCO alone automated 292 stations in 2023 and introduced self-fueling at 56 sites, a move that compressed labor cost per liter while pushing volume per nozzle higher.[2]Saudi Automotive Services Company, “Annual Report 2023,” SASCO.COM.SA Fleet composition favors SUVs and crossovers that consume 10–15% more fuel per kilometer than sedans, cushioning gasoline demand against forthcoming CAFÉ standards. Higher utilization also enhances the addressable base for ancillary services such as oil-change bays and tire centers that lift non-fuel revenue.

Acceleration of Giga-Projects (NEOM, Qiddiya, Red Sea)

Megaprojects valued above USD 1 trillion are converting previously remote stretches into high-traffic corridors, creating micro-markets within the broader Saudi Arabia fuel station market. NEOM’s USD 8.5 billion green-hydrogen plant goes live in 2026, and Petromin has already opened a prototype site that dispenses gasoline, diesel, electricity, and hydrogen in one forecourt.[3]Arab News, “SASCO Opens Al-Jazeera 1 Highway Service Plaza,” ARABNEWS.COM Highway service plazas such as SASCO’s Al-Jazeera 1 on the Riyadh–Dammam route anchor giga-project logistics, spanning 280,000 square meters and integrating QSRs, prayer halls, and rest areas to extend dwell time beyond 20 minutes. These destination-style formats justify the capex of USD 6.7–10.7 million per site and capture tourism-linked demand that Vision 2030 places at 100 million annual visits by 2030.

Fuel-Price Liberalization Attracting Private Capex

Aramco’s monthly pricing lifted diesel from SAR 0.80 to SAR 1.60 per liter in January 2024 and nudged gasoline 91 to SAR 2.37 by December 2024, eroding the subsidy-era barriers that had deterred private entrants. Gross fuel spreads of 5–8 halalas per liter now suffice when paired with 30–40% margins from convenience retail. Circle K’s alliance with the Alsulaiman Group targets 300 stores within five years, relying on higher price transparency and faster pump payback periods to justify investment. ADNOC Distribution opened 25 Saudi sites by December 2025, transplanting its ADNOC Oasis blueprint that sources up to 50% of gross profit from non-fuel lines.

Modern Convenience-Retail Formats Boosting Forecourt Revenue

As the Saudi Arabia fuel station market transitions toward thinner per-liter economics, c-stores, cafés, and QSRs supply the bulk of incremental profit. SASCO’s Palm network reached 128 outlets in 2023 and plans 60 more in 2026, accounting for 30–40% of station-level profit. The Aramco–TotalEnergies Sahel venture runs 270 mixed-energy sites that leverage Bonjour and Fai café formats to lift average tickets 20–30% above fuel-only peers. PwC research shows 62% of Saudis seek health-forward food and 40% prefer tech such as self-checkout, aligning with Circle K’s introduction of cashier-less kiosks in July 2025.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV & hybrid adoption targets for 2030 | -0.5% | Riyadh, Jeddah, NEOM | Long term (≥ 4 years) |

| CAFÉ efficiency standards & ride-sharing penetration | -0.3% | Urban centers | Medium term (2-4 years) |

| Retail margin squeeze from monthly price cap | -0.2% | Nationwide | Short term (≤ 2 years) |

| Rising UST-leak compliance CAPEX | -0.1% | Legacy districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EV & Hybrid Adoption Targets for 2030

The Saudi Green Initiative mandates 30% of new-vehicle sales be electric or plug-in hybrid by 2030, a policy reinforced by fleet-procurement rules for public agencies. Lucid delivered 6,200 units in 2025, triple its 2024 tally, while Ceer shipped its first 150 vehicles in September 2025, securing government-fleet contracts. Public charging points surpassed 1,000 in 2024, with another 1,000 under tender, yet utilization averages below 15%, raising questions about near-term ROI for chargers that cost SAR 150,000–250,000 each. A typical 50 kWh charge yields only SAR 75 at current tariffs, half the revenue of a gasoline fill, squeezing forecourt economics and lengthening payback periods unless bundled with high-margin retail offers.

CAFÉ Efficiency Standards & Ride-Sharing Penetration

SASO 2864:2022 phases fuel-economy rules to 20 km/L for cars by 2030, implying a 15–20% cut in per-vehicle gasoline demand. Simultaneously, ride-hailing hit USD 2.5 billion in 2023 and is growing 12% annually, with Uber, Careem, and Bolt intensifying urban competition. Higher vehicle utilization reduces the total cars needed, capping parc expansion. Fleet drivers refuel more often yet chase the cheapest pump, diluting brand loyalty and ancillary purchases. Station chains are countering with volume-discount lanes, but per-transaction profit remains 20–30% below retail norms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Alternative Fuels Surge Amid Gasoline Dominance

Gasoline generated 55.1% of the Saudi Arabian fuel station market in 2025, underpinned by the 15.8 million-vehicle parc and persistent internal-combustion reliance. Diesel followed, yet its January 2024 price leap to SAR 1.60 prompted freight operators to upgrade fleets, moderating volume gains. Liquefied and compressed gases stay niche, limited by sparse dispensing points. Alternative fuels, hydrogen, and EV charging will expand at a 25.3% CAGR through 2031, buoyed by the USD 8.5 billion NEOM hydrogen plant and a 30% EV-sales mandate.[4]Air Products, “Agreement for USD 5 Billion NEOM Hydrogen Facility,” AIRPRODUCTS.COM The Saudi Arabia fuel station market size for alternative fuels is set to outpace overall growth, yet remains a cash-consumer until charger utilization climbs above breakeven mid-decade.

Despite thin margins, operators position infrastructure early to anchor brand equity and capture first-mover data. SASCO’s fast-charger rollout begins in 2024, betting Lucid and Ceer volume will exceed 150,000 units annually by 2028. Hydrogen pumping costs run SAR 2–3 million per station, but giga-project corridors offer captive demand from construction fleets. Gasoline cash flows, therefore, cross-subsidize the transition, keeping the Saudi Arabian fuel station market resilient during the energy mix shift.

By Service Offering: Multi-Energy Hubs Redefine Forecourt Economics

Fuel-and-c-store designs delivered 51.5% revenue in 2025 and will remain the Saudi Arabia fuel station market workhorse through 2031. Palm, Bonjour, Fai, and ADNOC Oasis concepts have demonstrated 20–30% ticket uplifts over fuel-only peers. Multi-energy hubs that pair liquid fuels with EV and hydrogen dispense points grow fastest at 20.7% CAGR, riding Vision 2030 mandates.

The Saudi Arabia fuel station market size for multi-energy hubs remains small yet strategic. Operators view electrons and hydrogen as traffic magnets that lengthen dwell times and stimulate retail baskets. Circle K’s North American planograms, health-led assortments, and self-checkout serve PwC findings on consumer preference, raising non-fuel gross margins to 35–40%. However, low electricity tariffs cap charging spreads at 10–15%, making cross-selling essential for economic viability.

By Station Format: Highway Plazas Capture Corridor Traffic

Traditional full-service sites retained 49.9% of 2025 volume, but highway plazas will post a 6.2% CAGR out to 2031 as giga-project logistics and domestic tourism scale. The Saudi Arabia fuel station market size allocated to plaza developments is rising because each project funnels USD 6.7–10.7 million into large-format sites every 150–200 km.

Al-Jazeera 1 sets the blueprint: 280,000 square meters, integrated QSRs, prayer halls, and ample truck parking. Average dwell hits 25 minutes, tripling in-store spend relative to city stations. Capex intensity limits competition to well-capitalized chains, accelerating consolidation while offering insurers and regulators uniform-design compliance that reduces operational risk.

By End User: Transport Fleets Accelerate Electrification

Retail motorists supplied 60.3% of 2025 demand, but logistics and ride-hailing fleets will expand at a 6.9% CAGR to 2031, propelled by e-commerce and Vision 2030 trade-hub ambitions. The Saudi Arabia fuel station market size for fleet fueling is poised to enlarge as fleet vehicles log 40,000–60,000 km annually, raising per-vehicle throughput.

Government decrees require 30% EV adoption in public fleets, nudging bulk buyers toward electrified vans and sedans starting in 2025. Chains respond with high-amp charging lanes, RFID pumps, and fleet-discount programs to protect share. Yet fleet customers bargain hard on price, yielding margins 20–30% beneath retail averages and pressuring operators to monetize data analytics and ancillary maintenance offers.

Geography Analysis

Riyadh, Jeddah, and Dammam house more than 60% of the country’s vehicle base, siphoning the lion’s share of Saudi Arabia's fuel station market throughput and non-fuel revenue. SASCO concentrates its 540 stations in these metros, where prime sites pump 3–5 million liters monthly. The Western Province’s NEOM and Red Sea tourism corridors show the fastest network build-out; Petromin’s NEOM hub embeds hydrogen and EV lines that regional planners intend to replicate near pilgrimage centers in Mecca and Medina.

Central provinces exploit inter-city highways. SASCO’s Al-Jazeera 1 plaza on the Riyadh–Dammam axis captures both commuter and long-haul freight, illustrating how high-capex formats unlock rural spending previously lost to informal truck stops. Eastern industrial belts centered on Dammam sustain diesel-heavy volumes but trail in EV uptake due to depot-to-port haul lengths that exceed current battery ranges. Northern and southern regions remain underserved; modular stations with two to four pumps and limited retail can carve local monopolies, yet longer payback horizons deter fast expansion.

Uniform-design enforcement intensifies in metros, pressing independents to retrofit or exit. Rural areas experience looser oversight, but subsidy removal equalizes pump prices nationwide, driving urban consumers to price-shop within 1–2 halalas spreads and sharpening competitive pressure in dense catchments.

Competitive Landscape

The Saudi Arabia fuel station industry hosts a moderately fragmented roster: the top five operators control roughly 25–30% of national volume. SASCO leads with about a 5.5% share and a 540-station footprint, followed by Aldrees, Petromin, and the Aramco–TotalEnergies Sahel network. Gulf entrants import playbooks that hinge on diversified revenue: ADNOC Distribution’s Oasis stores, ENOC’s ZOOM outlets, and OOMCO’s Quick Shop formats replicate UAE and Omani success in extracting 50% of gross profit from non-fuel lines.

Circle K’s alliance with the Alsulaiman Group aims for 300 stores by 2030 and employs North American category management to optimize planograms and loyalty analytics. Technology is a decisive wedge: SASCO’s app enables pump reservation and in-car payment, trimming transaction times by 30–40 seconds and capturing purchase data for personalized offers. Aramco’s NFC windshield tags let fleet drivers refuel without PIN entry, feeding real-time analytics that fine-tune promotions.

Compliance costs accelerate consolidation. Uniform-design retrofits run SAR 100,000–300,000 per legacy site, prompting small independents to divest networks rather than invest. Large chains exploit scale economies in procurement, IT, and marketing, pushing the Saudi Arabia fuel station market toward a more structured oligopoly while still leaving room for regional specialists in compact or rural formats.

Saudi Arabia Fuel Station Industry Leaders

Aldrees Petroleum & Transport Services Co. (Aldrees)

SASCO

Petromin Corporation

Aramco/Total Sahel JV

NAFT Services Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Saudi Aramco has introduced 98-octane gasoline at select fuel stations in Riyadh, Jeddah, Dammam, and connecting highways. This premium fuel option caters to high-performance vehicles while maintaining the availability of existing 91 and 95-octane supplies. Over 130 stations now offer the new fuel, enhancing consumer choice and meeting market demand for specialized petrol options.

- November 2025: The Ministry of Energy tendered 500 new public EV chargers across Riyadh, Jeddah, and Mecca for installation by Q3 2026.

- May 2025: Saudi Arabia initiated a nationwide fuel station inspection campaign ahead of Hajj and Eid to assess compliance, quality, licensing, and standards at petrol outlets across 23 cities. The campaign involves over 300 inspectors and includes sampling of gasoline, diesel, and oils to ensure regulatory adherence.

- July 2024: Circle K and Alsulaiman Group opened their 50th Saudi store, incorporating self-checkout kiosks.

Saudi Arabia Fuel Station Market Report Scope

A fuel station, also known as a petrol station or gas station, is a facility that sells fuel and engine lubricants for motor vehicles. Fuel dispensers are used to pump gasoline and diesel into the tanks within vehicles and calculate the financial cost of the fuel transferred to the vehicle.

The Saudi Arabia fuel station market report is segmented into fuel type, service offering, station format, end-user, and geography. By fuel type, the market is divided into gasoline, diesel, LPG/CNG, and alternative fuels. By service offering, the market is segmented into fuel only, fuel and convenience store, fuel/c-store/QSR, and multi-energy hubs. By station format, the market is segregated into traditional full-service, compact/micro-stations, and others. By end-user, the market is divided into retail consumers, commercial fleets, industrial users, transport/logistics fleets, and air/marine transport. The market sizing and forecasts for each segment are based on the revenue generated (in USD).

By Fuel Type

| Gasoline |

| Diesel |

| Liquified Petroleum Gas (LPG)/Compressed Natural Gas (CNG) |

| Alternative Fuels (Hydrogen, EV Charging) |

By Service Offering

| Fuel Only |

| Fuel and Convenience Store |

| Fuel, C-Store, and Quick-Serve Restaurant |

| Multi-Energy Hubs (Fuel + EV/H₂) |

By Station Format

| Traditional Full-Service |

| Compact/Micro-stations |

| Highway Service Plazas |

By End-User

| Retail Consumers |

| Commercial Fleets |

| Industrial Users |

| Transport and Logistics Fleets |

| Air/Marine Transport |

| By Fuel Type | Gasoline |

| Diesel | |

| Liquified Petroleum Gas (LPG)/Compressed Natural Gas (CNG) | |

| Alternative Fuels (Hydrogen, EV Charging) | |

| By Service Offering | Fuel Only |

| Fuel and Convenience Store | |

| Fuel, C-Store, and Quick-Serve Restaurant | |

| Multi-Energy Hubs (Fuel + EV/H₂) | |

| By Station Format | Traditional Full-Service |

| Compact/Micro-stations | |

| Highway Service Plazas | |

| By End-User | Retail Consumers |

| Commercial Fleets | |

| Industrial Users | |

| Transport and Logistics Fleets | |

| Air/Marine Transport |

Key Questions Answered in the Report

What is the current value of the Saudi Arabia fuel station market?

The Saudi Arabia fuel station market size reached USD 45.01 billion in 2026 and is projected to climb to USD 54.89 billion by 2031.

How fast is the Saudi Arabia fuel station market expected to grow?

The market is forecast to register a 4.05% CAGR between 2026 and 2031, supported by vehicle-parc growth and convenience-retail expansion.

Which fuel type is expanding the quickest in Saudi filling stations?

Alternative fuels, namely hydrogen and EV charging, are poised to rise at a 25.3% CAGR through 2031 despite a small starting base.

Who are the leading players in Saudi fuel retail?

SASCO, Aldrees, Petromin, the Aramco-TotalEnergies Sahel venture, and NAFT (now integrated into SASCO) head the operator rankings with roughly 25-30% combined share.

How are convenience stores influencing station profitability?

Non-fuel lines such as cafés and c-stores contribute 30-40% of station-level profit, offsetting thin fuel margins capped at 5-8 halalas per liter.

What role will hydrogen play in Saudi forecourts?

Hydrogen pumps will initially anchor giga-project corridors like NEOM, with infrastructure spending front-loaded ahead of fuel-cell vehicle adoption expected post-2027.

Page last updated on: