Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

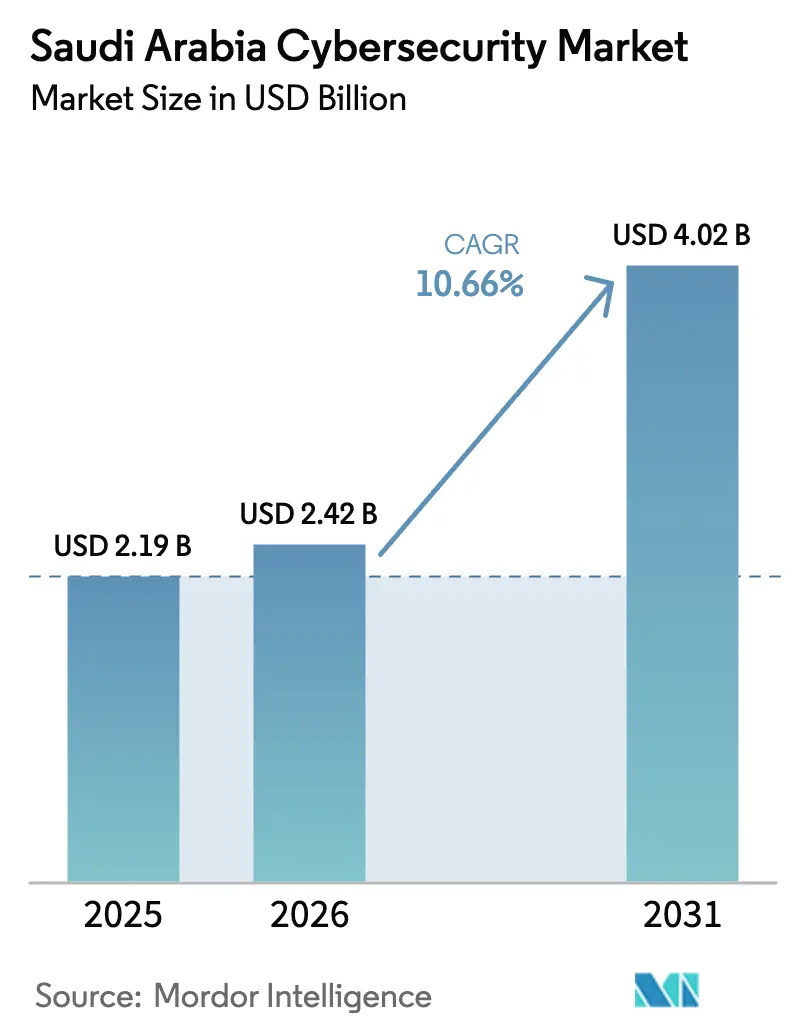

| Base Year Market Size (2025) | USD 2.19 Billion |

| Market Size (2026) | USD 2.42 Billion |

| Market Size (2031) | USD 4.02 Billion |

| Growth Rate (2026 - 2031) | 10.66% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Cybersecurity Market Analysis by Mordor Intelligence

Saudi Arabia cybersecurity market size in 2026 is estimated at USD 2.42 billion, growing from 2025 value of USD 2.19 billion with 2031 projections showing USD 4.02 billion, growing at 10.66% CAGR over 2026-2031. Strong public-sector spending, mandatory national controls, and rapid cloud migration are the foremost catalysts, while skills shortages and fragmented procurement processes temper overall momentum. Localization mandates are reshaping vendor strategies, with global and local players building joint offerings that blend international technology with Saudi compliance expertise. Government directives around Vision 2030 mega-projects, OT–IT convergence in energy assets, and sovereign cloud initiatives continue to widen the addressable opportunity for advanced threat detection, zero-trust frameworks, and managed security services. Simultaneously, a persistent lack of Saudi nationals with tier-3/4 incident-response expertise is accelerating the shift toward automation and outsourced operations.

Key Report Takeaways

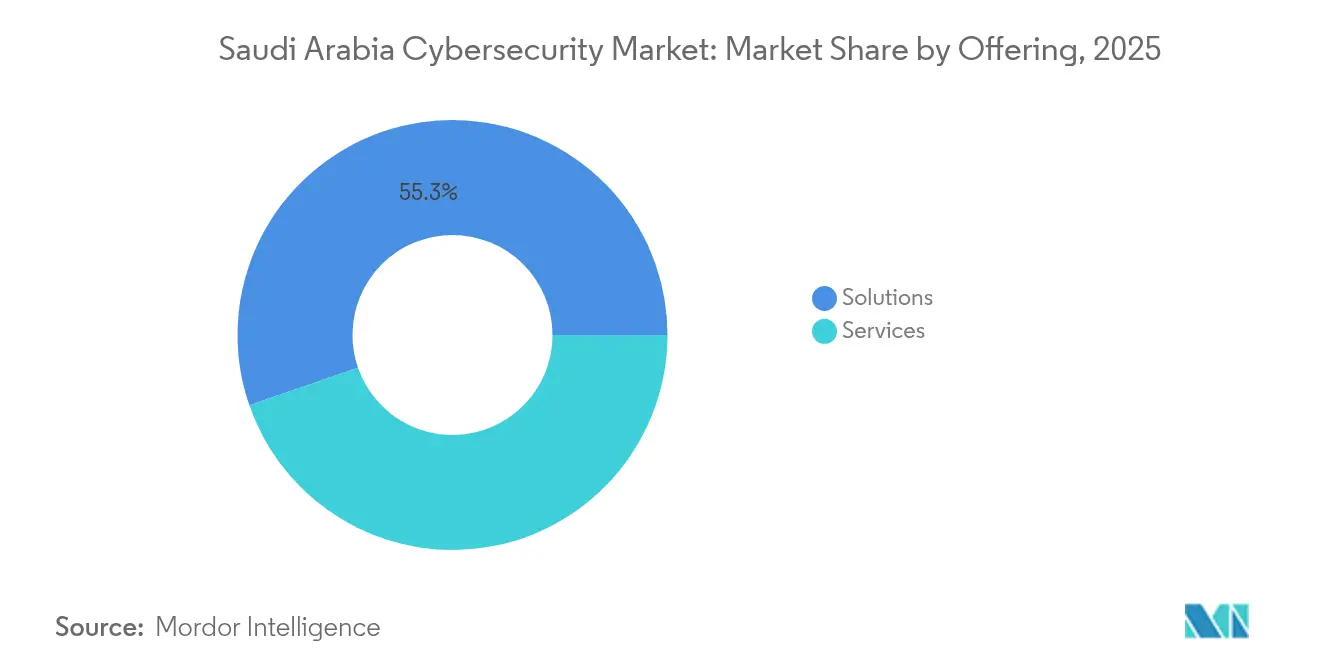

- By offering, Solutions led with 55.30% revenue share in 2025; Services are projected to grow at an 11.53% CAGR through 2031.

- By deployment mode, On-premise held 70.85% of the Saudi Arabia cybersecurity market share in 2025, while Cloud deployments are advancing at a 14.15% CAGR to 2031.

- By end-user industry, Government and Defense commanded 29.55% share of the Saudi Arabia cybersecurity market size in 2025; Healthcare is forecast to expand at a 13.03% CAGR between 2026-2031.

- By end-user enterprise size, Large enterprises accounted for 75.10% of the Saudi Arabia cybersecurity market size in 2025, yet SMEs record the fastest growth at a 14.28% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Cybersecurity Strategy Accelerating Large-Scale SOC and SIEM Deployments | +2.1% | Riyadh, Jeddah, Eastern Province | Medium term (2-4 years) |

| Mandatory Compliance with NCA Essential Cybersecurity Controls Driving Spending in Critical Sectors | +1.8% | Nationwide critical-infrastructure operators | Short term (≤ 2 years) |

| Hyper-digitisation of Vision 2030 Mega-Projects Creating New Attack Surfaces | +1.3% | NEOM, Red Sea, Qiddiya project zones | Long term (≥ 4 years) |

| Rapid Cloud Migration Post-SDAIA Policy Enabling Saudi-Hosted Public Clouds | +1.1% | Government and financial-services hubs | Medium term (2-4 years) |

| OT–ICS Convergence Elevating Security Requirements in Oil and Gas Facilities | +0.9% | Eastern Province refineries, national utilities | Medium term (2-4 years) |

| Growing Home-grown Talent Pool Strengthening Indigenous Cyber Capabilities | +0.6% | Major urban centers (Riyadh, Jeddah, Dammam) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

National Cybersecurity Strategy Accelerating Large-Scale SOC and SIEM Deployments

Saudi Arabia’s National Cybersecurity Strategy has unlocked record spending on fully staffed security operations centers and enterprise-grade SIEM platforms across ministries and critical agencies. Forty-nine federal bodies now integrate AI into threat-detection workflows, making the Kingdom the regional benchmark for coordinated cyber governance. Standardized procurement under this program enables volume discounts that favor platform vendors offering end-to-end analytics and incident-response orchestration. Private-sector operators in energy and finance are mirroring these frameworks to remain aligned with federal benchmarks. As a result, AI-enabled monitoring is expected to penetrate 94% of large organizations by 2026, cementing a demand cycle that supports long-term managed-detection-and-response growth.

Mandatory Compliance with NCA Essential Cybersecurity Controls Driving Spending

The updated ECC-2-2024 framework widens mandatory coverage to every entity handling national infrastructure and imposes fixed deadlines for adherence across five governance domains [1]National Cybersecurity Authority, “Essential Cybersecurity Controls 2024,” nca.gov.sa. Procurement timelines have compressed, forcing boards to allocate incremental capital for automated compliance reporting, continuous monitoring, and third-party risk management. Vendors bundling policy templates, control-mapping libraries, and audit-ready dashboards win early contracts, while services revenue accelerates as organizations outsource Governance-Risk-Compliance and red-team assessments.

Hyper-digitization of Vision 2030 Mega-Projects Creating New Attack Surfaces

Flagship projects such as NEOM’s USD 5 billion net-zero AI factory are fusing OT and IT networks at unprecedented scale, multiplying exposed endpoints and attracting higher-order adversaries. Smart-city grids, autonomous mobility corridors, and connected medical complexes require zero-trust segmentation, secure data-lake architectures, and AI-driven anomaly detection. The national importance of these corridors escalates the threat profile, incentivizing proactive investment in next-generation endpoint protection and industrial-grade encryption.

Rapid Cloud Migration Post-SDAIA Policy Enabling Saudi-Hosted Public Clouds

SDAIA’s cloud-first mandate obliges 80% of government workloads to reside in local clouds by 2030 and has already propelled a 16.8% annual expansion of domestic cloud capacity [2]Saudi Data and Artificial Intelligence Authority, “Cloud-First Policy Framework,” sdaia.gov.sa. Sovereign cloud regions operated by stc, SCCC, and global partners now host sensitive workloads that previously stalled in datacenters. Misconfiguration risk balloons in parallel, making cloud-security-posture-management, identity governance, and workload micro-segmentation top procurement items. Cloud-delivered security tools now record double-digit gains, eclipsing on-premise growth in every audited fiscal quarter since 2024.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Saudi-Nationals with Advanced Skills | -1.4% | Nationwide cyber operations centers | Medium term (2-4 years) |

| Fragmented Procurement across Semi-Government Entities | -1.1% | Semi-autonomous public bodies | Short term (≤ 2 years) |

| High Up-front Cost of Zero-Trust Re-architecture | -0.8% | Legacy ministries | Medium term (2-4 years) |

| Dependence on Foreign Encryption IP | -0.5% | Defense and utilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Saudi-Nationals with Tier-3/4 Incident-Response Skills

Despite scholarships and new cyber-academies, demand for forensic talent outstrips supply, lifting salaries by 30-40% in one year and pushing total cost of ownership beyond internal budgets. Enterprises pivot toward managed detection services, AI-augmented triage, and low-code security playbooks to offset the deficit, but knowledge transfer remains an unresolved challenge.

Fragmented Procurement across Semi-Government Entities Slowing Decision Cycles

More than 300 semi-government bodies run disjointed tendering processes; extended approval chains lengthen sales cycles by up to 60% relative to private deals. The absence of pooled contracts prevents volume savings and perpetuates tool sprawl, diluting defense-in-depth maturity across interconnected agencies. Although ECC alignment is slowly harmonizing baseline requirements, near-term purchasing friction continues to dampen aggregate spending velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Accelerate Despite Solutions Dominance

Solutions remained the cornerstone of the Saudi Arabia cybersecurity market with a 55.30% revenue contribution in 2025, reflecting mandatory basic-control deployment across ministries and regulated industries. Network firewalls, IAM suites, and endpoint detection platforms formed the bulk of purchases as zero-trust roadmaps matured. Conversely, the Services segment is forecast to expand at an 11.53% CAGR, well above the Saudi Arabia cybersecurity market average of 10.66%. Shortfalls in domestic talent propel outsourcing to managed-security service providers, particularly for 24/7 SOC monitoring and incident response. Professional-services demand also climbs as enterprises seek specialized guidance for ECC audits and OT security architecture.

The paradigm shift toward services is most visible in financial institutions and oil-and-gas operators, where compliance and continuous monitoring are mission-critical. Managed detection and response packages now incorporate AI-driven triage and automated compliance documentation to align with ECC-2-2024 timelines. Vendors offering bundled SOC-as-a-Service with threat-intelligence feeds are capturing mid-market share, while global integrators partner with local firms to address Arabic-language phishing and culturally specific social-engineering vectors.

By Deployment Mode: Cloud Security Transformation Accelerates

On-premise deployments held 70.85% of the Saudi Arabia cybersecurity market share in 2025 due to entrenched data-sovereignty preferences and strict residency clauses governing classified workloads. Ministries and refiners continue to favor local appliance-based firewalls and hardened datacenter SIEMs for sensitive applications.

Mission-critical workloads remain on-premise, while analytics, collaboration, and citizen-facing portals migrate to public or community clouds. This duality drives demand for unified-visibility platforms that correlate telemetry across mixed environments. The Saudi Cloud Computing Company’s geographically distributed nodes now deliver integrated WAF, DDoS protection, and workload-encryption services, easing sovereign-cloud adoption for regulated entities and SMEs alike.

By End-User Industry: Healthcare Emerges as Growth Leader

Government and Defense accounted for 29.55% of the Saudi Arabia cybersecurity market size in 2025, anchored by the National Cybersecurity Strategy and ECC mandates requiring continuous monitoring, threat intelligence sharing, and hardened identity controls. Collective procurement frameworks grant preferred pricing to certified vendors, fostering platform consolidation while raising entry barriers for unaccredited providers.

Healthcare is set to deliver the fastest growth at a 13.03% CAGR to 2031, aided by digital-medical-record rollouts, telehealth expansion, and the PDPL’s strict data-protection clauses. Clinics, research centers, and smart-hospital projects embedded in Vision 2030 developments are procuring endpoint encryption, secure PACS, and medical-device micro-segmentation. Security-by-design mandates within new hospital construction contracts are awarding wins to vendors that integrate compliance reporting and multi-factor authentication in medical workflows.

By End-user Enterprise Size: SMEs Accelerate Security Adoption

Large enterprises retained 75.10% of the Saudi Arabia cybersecurity market share in 2025, driven by compliance exposure and larger attack surfaces across banking, hydrocarbons, and telecom domains. These entities prioritize AI-assisted threat hunting, SOAR, and insider-risk analytics, often running federated SOC environments across multiple business units.

SMEs represent the most dynamic cohort, with spending projected to climb at a 14.28% CAGR. Subscription-based bundles that combine email security, endpoint protection, and vulnerability management in a single portal lower barriers to entry. The ECC’s extension to critical-supply-chain contractors compels smaller firms to document security posture before bidding on state-linked projects, triggering first-time investment in encryption, authentication, and managed backup services.

Geography Analysis

Riyadh anchors roughly 59.40% of national cybersecurity spending in 2025 as it hosts federal ministries, the central bank, and most enterprise headquarters. High-value state services and a growing cluster of international technology providers make the capital a prime target for advanced persistent threats, spurring continuous SOC expansion and AI-based anomaly detection. Government-backed innovation zones such as Digital City support start-ups focusing on Arabic-language threat feeds, bolstering local supply.

The Eastern Province forms the second-largest node of the Saudi Arabia cybersecurity market, dominated by energy-sector investments in SCADA and pipeline monitoring defenses. Saudi Aramco’s Third-Party Cybersecurity Compliance Certificate program obliges every vendor to maintain audited security baselines, propagating best practices across the supply chain. As OT–IT convergence advances within refineries and petrochemical complexes, layered segmentation, anomaly-based intrusion detection, and safety-integrity-level mapping become mandatory.

Western Saudi Arabia, centered on Jeddah and the holy cities, blends commercial logistics with religious-tourism surges. SDAIA’s biometric-verification platforms process millions of pilgrim entries each season, necessitating real-time encryption, network isolation, and rapid-scaling cloud controls. Expansion of King Abdullah Port and adjacent free zones intensifies supply-chain-security requirements, while new private healthcare clusters supporting medical tourism adopt endpoint hardening and data-loss-prevention suites to satisfy international patient-data standards.

Competitive Landscape

The Saudi Arabia cybersecurity market supports a fragmented field where multinational vendors, regional specialists, and emerging local champions vie for project-based wins. IBM, Cisco, and Palo Alto Networks leverage broad portfolios and global threat-intel labs to meet enterprise scalability demands, whereas sirar by stc and Taqnia Cyber pivot on deep knowledge of Saudi regulatory nuances and Arabic content filtering.

Strategic alliances dominate go-to-market motion. SCCC pairs Alibaba Cloud’s analytics engines with stc’s sovereign data centers to deliver government-grade cloud security, while industrial OEMs integrate with local MSSPs to protect refinery automation. Joint ventures frequently embed local-hosting clauses and Arabic support centers to satisfy ECC localization thresholds, shifting competitive parameters from pure feature parity to compliance readiness.

Niche innovators target white spaces such as supply-chain visibility, OT anomaly detection, and AI model security. Cipher’s USD 13.3 million funding round underscores investor appetite for Saudi-born MSSPs specializing in sector-specific playbooks for energy and logistics [3]Cipher, “Series A Funding Announcement,” cipher-ksa.com. Market entry barriers remain moderate, yet scale requires ECC accreditation, Arabic interface localization, and on-shore Tier-4 datacenter presence, factors that collectively reward firms willing to co-invest with Saudi partners.

Saudi Arabia Cybersecurity Industry Leaders

IBM Corporation

Broadcom Inc.

Cisco Systems Inc.

Palo Alto Networks, Inc.

Fortinet Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Mastercard opened the Middle East Cyber Resilience Center in Riyadh in collaboration with Riyad Bank to enhance regional defense capabilities.

- January 2025: SEALSQ and WISeKey introduced quantum-resistant IoT security initiatives supporting national digital-transformation goals.

- December 2024: The Saudi Cloud Computing Company announced geographic expansion beyond Riyadh to meet rising sovereign-cloud demand in line with the national Cloud-First Policy.

- November 2024: Cipher secured USD 13.3 million in pre-IPO financing from Impact 46 to scale managed-security services for regulated sectors.

Saudi Arabia Cybersecurity Market Report Scope

The Saudi Arabian cybersecurity market is defined based on the revenues generated from the solutions and services that are being used by various end-user industries across the country. The scope of the study does not include physical security solutions and industrial control systems. The analysis is based on the market insights captured through secondary research and the primaries. The report also covers the major factors impacting the growth of the market in terms of drivers and restraints.

The Saudi Arabia cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End-point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| Cloud |

| On-Premise |

By End-user Industry

| BFSI |

| Healthcare |

| IT and Telecom |

| Government and Defense |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Others |

By End-user Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End-point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By End-user Industry | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Government and Defense | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

| By End-user Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

What is the current size of the Saudi Arabia cybersecurity market?

The market stands at USD 2.42 billion in 2026.

How fast is the market expected to grow?

Revenue is projected to rise to USD 4.02 billion by 2031, reflecting an 10.66% CAGR.

Which end-user vertical is growing the quickest?

Healthcare leads with a 13.03% CAGR thanks to electronic-health-record rollouts and telemedicine expansion.

Why are cloud-security solutions gaining momentum?

SDAIA’s cloud-first mandate and sovereign cloud regions are pushing organizations to adopt cloud-native controls, resulting in a 14.15% CAGR for cloud deployments.

Page last updated on: