Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

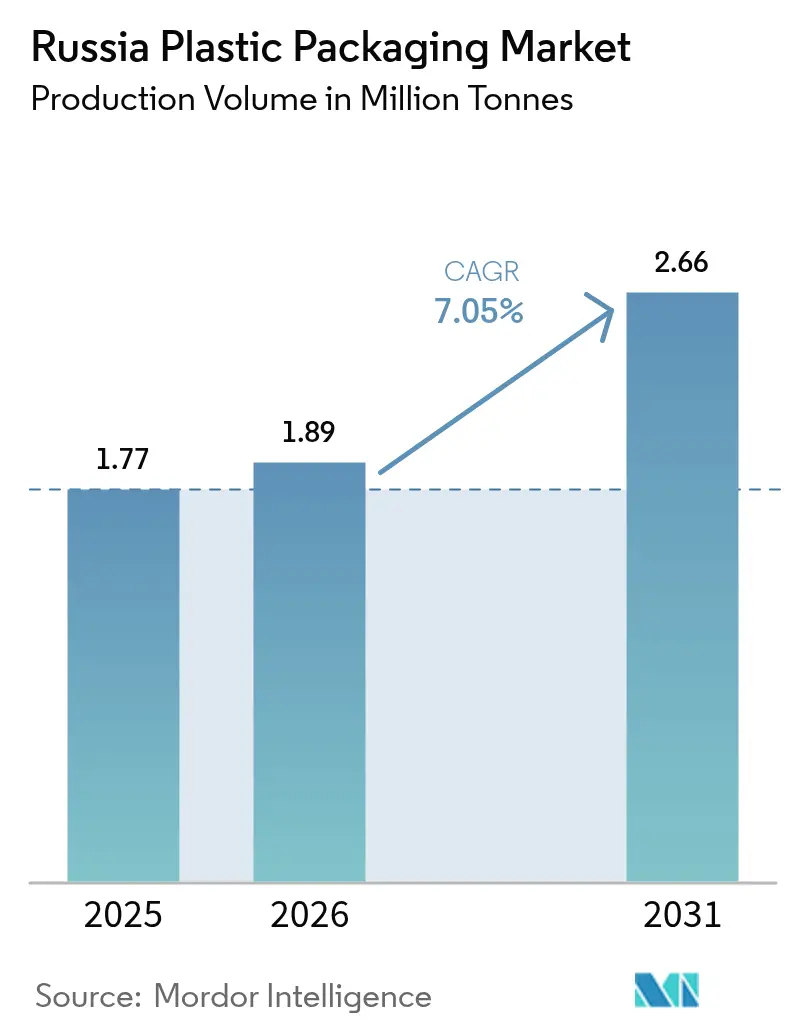

| Base Year Market Size (2025) | 1.77 Million tonnes |

| Market Volume (2026) | 1.89 Million tonnes |

| Market Volume (2031) | 2.66 Million tonnes |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

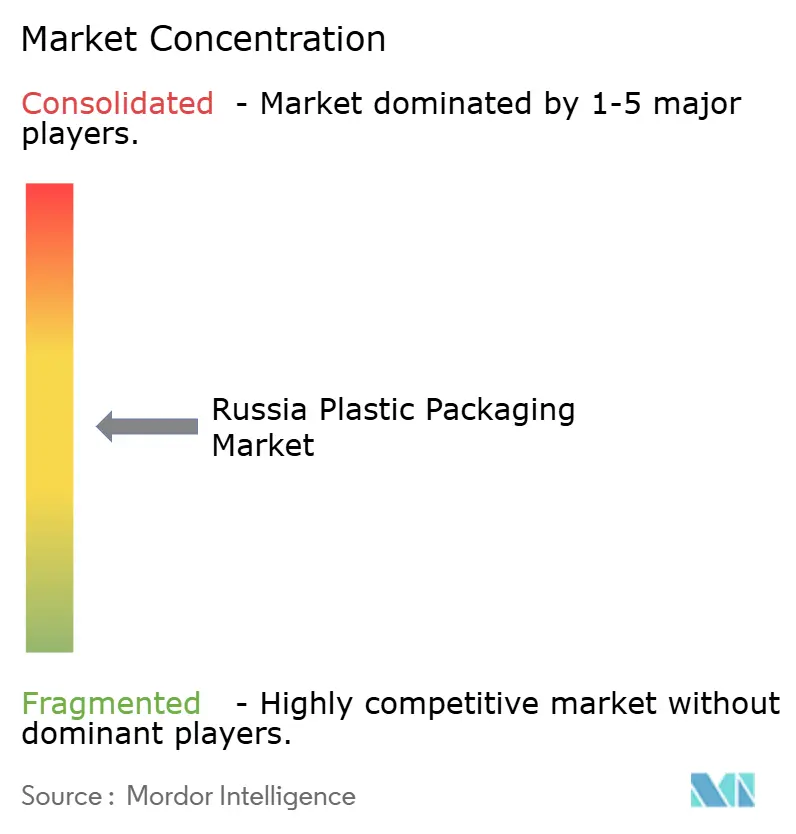

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Plastic Packaging Market Analysis by Mordor Intelligence

The Russia plastic packaging market size in 2026 is estimated at 1.89 million tonnes, growing from 2025 value of 1.77 million tonnes with 2031 projections showing 2.66 million tonnes, growing at 7.05% CAGR over 2026-2031. Accelerated domestic polymer capacity additions, a 45% surge in e-commerce sales to RUB 19.9 trillion (USD 0.23 trillion) in 2024, and rising investments in automated filling and sealing lines are expanding demand for barrier films, pouches, and lightweight rigid containers. Regulatory moves that restrict single-use items are redirecting material selection toward compostable films and recycled-content resins, while SIBUR’s 71%-complete Amur Gas Chemical Complex underpins future feedstock security. Meanwhile, logistics hurdles across 11 time zones favor durable, temperature-resistant packaging that can handle long-haul transit and automated parcel lockers. These dynamics together reinforce a shift from import-heavy supply chains toward a more self-sufficient Russia plastic packaging market.

Key Report Takeaways

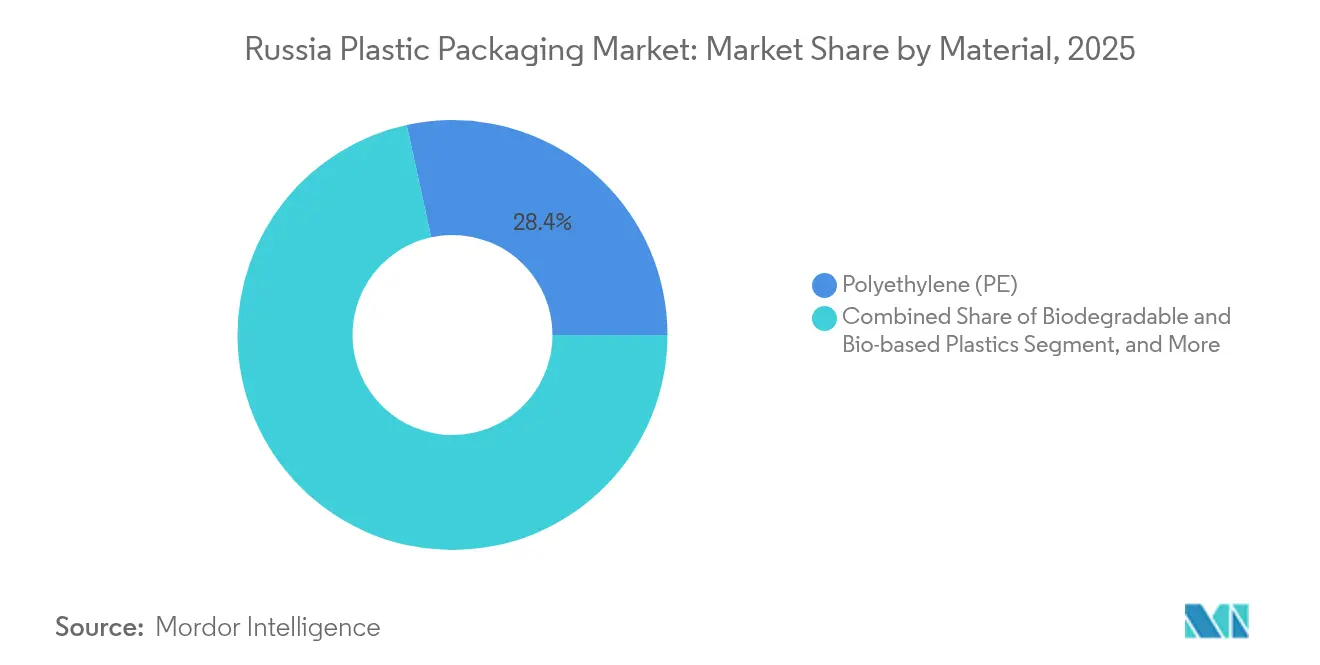

- By material, polyethylene led with 28.42% Russia plastic packaging market share in 2025, while biodegradable and bio-based plastics registering the fastest 8.74% CAGR to 2031.

- By type, flexible formats captured 54.43% of the Russia plastic packaging market size and are advancing at an 7.76% CAGR through 2031.

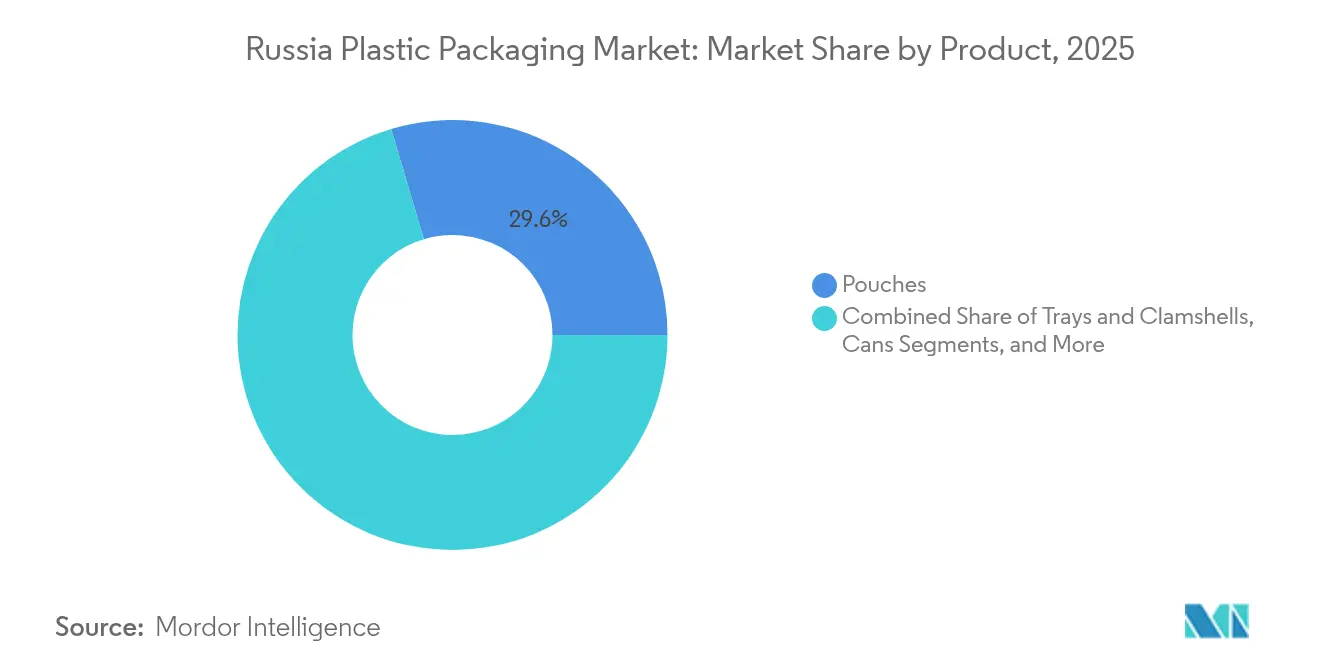

- By product, pouches accounted for 29.61% of the Russia plastic packaging market size in 2025, and registering the fastest 8.05% CAGR to 2031.

- By end-user, food applications controlled 29.43% of the Russia plastic packaging market size in 2025; personal-care and household lines are set for the highest 9.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in demand for packaged FMCG products | +1.8% | Major urban regions | Medium term (2-4 years) |

| Growth of e-commerce and home-delivery logistics | +1.5% | Nationwide | Short term (≤ 2 years) |

| Increasing adoption of lightweight, cost-effective packaging | +1.2% | Manufacturing clusters | Medium term (2-4 years) |

| Expansion of Russian food export markets | +0.9% | Export-oriented south and Black Sea | Long term (≥ 4 years) |

| Government incentives for domestic processing investments | +0.8% | Priority industrial regions | Long term (≥ 4 years) |

| Logistics challenges across vast territory | +0.6% | Far East and Siberia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise in Demand for Packaged FMCG Products

Rising single-person households and busier urban lifestyles boosted ready-meal sales 13% in 2024, prompting converters to supply more multi-layer pouches, thermoformed trays, and flow-wrap films that extend shelf life. Potato processing hit 1.5 million tonnes with a 25% jump in frozen categories, multiplying primary, secondary, and tertiary pack demand. Snack output climbed to 717 000 tonnes, stimulating orders for high-barrier metallized films that balance oxygen and moisture protection. Equipment producers responded; packaging and bottling machinery represented 35% of RUB 128 billion in 2023 food-equipment spending, signaling a virtuous cycle of automated filling lines driving film consumption. As factory throughput rises, the Russia plastic packaging market gains resilience against import disruptions.

Growth of E-Commerce and Home-Delivery Logistics

A RUB 19.9 trillion (USD 0.23 trillion) e-retail sector in 2024 fostered unprecedented volumes of mailer bags, stretch-wrap, and tamper-evident pouches for four dominant platforms that now handle 81% of online orders. Fulfillment spending near RUB 94 billion (USD 1.13 billion) drove automation, while 50,000 pick-up points required parcel-ready formats with drop-safe seals. Because the cross-border share of orders plunged to 3% in 2023, local converters captured more line-side demand, reinforcing domestic polymer flows. In the Far East and North Caucasus, longer lead times spur thicker cushioning films and co-extruded liners to tackle sub-zero rail transits. These factors together lift volume and value across the Russia plastic packaging market.

Increasing Adoption of Lightweight, Cost-Effective Packaging

Freight costs climbed 17% in 2024, so brand owners prioritized thinner bottles and downgauged shrink films that save transport fuel without compromising integrity. SIBUR’s customer-centric polymer grades enable 5–7% wall-thickness cuts, validated by ALPLA plants converting 50 000 tonnes of PET annually with lightweight neck finishes. High-speed overwrappers running 100 cycles per minute minimize trim waste, translating to lower carbon intensity per packed unit. As line operators adopt inline gravimetric controls, consistent gauge reduction becomes the norm, broadening the Russia plastic packaging industry’s cost edge against imported finished packs.

Expansion of Russian Food Export Markets

Confectionery exports rose 8% to 700 000 tonnes in 2024, led by chocolate blocks heading to China and Gulf markets that demand premium print aesthetics and heat-stable laminates. Government freight-rebate schemes and permanent retail pavilions in six key countries lower upfront risk, encouraging exporters to specify higher-barrier foils and desiccant sachets. Greenhouse vegetable acreage expanded 2.1%, pushing modified-atmosphere bags with laser-micro-perforation into mainstream use. As trade lanes tilt toward humid climates, pouch films must withstand 40 °C holds without seal failure, propelling R&D in ethylene-vinyl-alcohol-based structures. These shifts cement overseas volume as a structural pillar for the Russia plastic packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent government regulation on single-use plastics | -1.4% | Nationwide | Short term (≤ 2 years) |

| Volatility in polymer raw-material prices | -1.1% | Import-dependent converters | Medium term (2-4 years) |

| Growing consumer environmental concerns | -0.8% | Tier-1 cities | Long term (≥ 4 years) |

| Limited recycling infrastructure and collection gaps | -0.6% | Remote regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Government Regulation on Single-Use Plastics

Russia’s phased bans on 28 disposable items, plus tougher extended-producer-responsibility (EPR) fees introduced in 2025, compel converters to redesign lids, caps, and opaque PET bottles while funding recovery schemes. Non-compliant packs face market withdrawal, so brand owners fast-track switchovers to recyclable mono-material films. TR CU 005/2011 heightens migration testing, especially for infant food jars, adding certification lead time and tooling cost. Collectively, these rules slow short-term tonnage growth, yet they also open premium niches for bio-based grades.

Volatility in Polymer Raw-Material Prices

Imported resins worth USD 14 billion in 2024 exposed converters to foreign exchange swings; PVC spot prices alone rose 2.8% in early 2025, compressing margins. European demand weakness kept polypropylene values soft, but freight bottlenecks at Black Sea ports added unexpected surcharges. SIBUR’s Amur Gas Chemical Complex will eventually ease supply risk, yet until ramp-up finishes, buyers employ shorter contracts and inventory buffers that raise working-capital needs. Such unpredictability restrains near-term investment appetites in the Russia plastic packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Sustainable Alternatives Challenge Polyethylene’s Lead

Polyethylene held 28.42% Russia plastic packaging market share in 2025, supported by domestic cracker capacity and well-established extrusion lines . Yet biodegradable and bio-based resins are advancing at 8.74% CAGR as brand owners chase EPR credits and retail chains pilot compostable ready-meal trays. Policell’s ramp-up to 15 000 tonnes of PLA demonstrates supply readiness, while SIBUR’s catalyst unit targets novel metallocene grades that permit thinner films at equal stiffness . Demand for food-contact safety under TR CU 005/2011 keeps PET and PP relevant in hot-fill and retort pouches. PVC and polystyrene now serve niche closures and medical items.

Circular-economy pilots, including retailer take-back of PET salad bowls, are spurring investment in food-grade recycling lines that feed back into thermoform sheets. As a result, the Russia plastic packaging market size for recycled polyethylene is forecast to rise 9.84% annually between 2026–2031. Domestic feedstock improves pricing visibility and limits currency exposure, offering converters a hedge against imported resin volatility. Collectively, material mix diversification underpins the sustainability narrative while maintaining volume growth.

By Type: Flexible Formats Capture Efficiency Gains

Flexible products commanded 54.43% of the Russia plastic packaging market size in 2025 and are expanding at an 7.76% CAGR, propelled by e-commerce mailers and high-barrier snack films that cut weight versus rigid jars. Laminated stand-up pouches with laser scoring now replace metal cans in baby purée and wet-pet-food aisles. Meanwhile, rigid options retain share in carbonated drinks and bulk chemicals where drop resistance is paramount. Growth of lightweight thermoformed cups with in-mold labels further narrows the divide, offering 18% lower material usage versus injection-molded counterparts.

Converters investing in high-output blown-film lines can switch between LDPE, LLDPE, and bio-resins, aligning with regulatory trajectories. Across remote Siberian routes, flexible pallet hoods withstand –30 °C, reinforcing their logistics value. This cost-to-performance advantage secures flexible packaging’s role as the volume engine for the Russia plastic packaging market. Rigid suppliers are countering with PCR-rich bottles and returnable crates to preserve relevance.

By Product: Pouches Extend Beyond Snacks

Pouches held 29.61% Russia plastic packaging market share in 2025 and will post an 8.05% CAGR through 2031 as fitments, spouts, and retort films widen their use in soup concentrates, household gels, and motor oils. Pillow pouches processed at 600 bags-per-minute now dominate powdered milk exports, while quad-seal coffee packs with degassing valves appeal to specialty roasters. Bottles and jars still anchor 1 L dairy products and cooking oil but face thinner neck finishes to cut resin. Trays for ready-meals gain traction as microwave-safe grades extend convenience.

Compostable pouch laminates using PLA and starch offer 40% lower cradle-to-gate greenhouse emissions, attracting eco-centric brands. In response, blown-film lines add five-layer capability to incorporate bio-barrier resins without sacrificing machinability. Consumer acceptance of tear-off laser score lines and easy-open zippers fuels repeat purchases. Thus, pouches remain a focal point for innovation inside the Russia plastic packaging market.

By End-User Industry: Food Retains Primacy, Personal Care Accelerates

Food applications held 29.43% of the Russia plastic packaging market size in 2025, anchored by chilled dairy, confectionery, and frozen potato exports . Automated MAP lines improve shelf life for greenhouse cucumbers, while portion-controlled snack bags address single-adult households. Beverage categories stay steady as sports-cap PET bottles offset softness in carbonated drinks. Medical and pharma volumes gain from pre-fillable syringes molded under ISO 7 cleanrooms.

Personal-care and household goods will grow 9.08% annually to 2031, aided by switch to 60% PCR bottles that cut virgin resin by 1 200 tonnes per year. E-supermarkets bundle detergents with refill pouches, lowering logistics cost and landfill footprint. Industry collaboration on drop-test protocols ensures lightweight containers survive courier networks. These trends reinforce diversified demand within the Russia plastic packaging industry.

Geography Analysis

Central Federal District houses Moscow’s dense converter cluster and 28 supplier sites, giving it logistical reach and immediate access to Russia plastic packaging market demand hotspots. St. Petersburg and Leningrad Oblast follow, where Gotek Group’s buy-out of Mondi’s assets created a three-player oligopoly in corrugate and flexible rolls . The presence of skilled labor and multi-modal transport links underpins these hubs.

Yekaterinburg anchors the Urals, serving as a PP and PE redistribution center through Polimaks’ 3 500 m² warehouse that feeds converters across CIS nations. Siberia’s Novosibirsk leverages proximity to feedstock and Asian corridors; 2 550 exporters tapped state support programs worth USD 1.56 billion in 2023, lifting pack exports to China and Mongolia. Southern Krasnodar blends greenhouse vegetables with rising sweet-confection exports, driving specialized breathable films.

Far-East border congestion at Zabaikalsk forces three-week truck queues, so shippers favor reusable crates that stack efficiently during empty returns. Arctic zones mandate –40 °C-tolerant films, while subtropical Stavropol demands UV-stabilized clamshells. National digital freight-tracking pilots promise better lane visibility, offering converters data to optimize material choice and inventory turns within the Russia plastic packaging market.

Regulatory Landscape

Regulation of plastic packaging in Russia is increasingly shaped by extended producer responsibility (EPR) under Federal Law No. 451-FZ (amendments to Federal Law No. 89-FZ on waste), with obligations and reporting tied to packaging volumes and recycling fulfillment or payment of an environmental fee. Reporting for the prior calendar year is due by April 15 (for example, 2025 reporting submitted by April 15, 2026) via the EFGIS UOIT platform. Russia is also continuing phased restrictions on disposable items and has introduced tighter EPR fees in 2025, which pressures brand owners and converters to redesign packaging toward recyclable structures.

On the technical compliance side, polymer packaging used for food and other regulated applications is governed through GOST and EAEU technical regulations, including TR CU 005/2011 for packaging safety and referenced GOST requirements (such as GOST 33837-2022 for packaging). Recycling targets and eco-fee parameters have been updated through the EPR reform cycle, with transitional recycling rates cited at 55% for 2025 and 75% for 2026. Federal Law No. 495-FZ, enacted on December 31, 2025, postponed certain environmental fee reform rules for importers until January 1, 2028, which adds additional timing considerations for import-dependent packaging inputs.

Value Chain Analysis

The value chain begins upstream with resin and additive supply, led by domestic polymer producers such as SIBUR, and extends through compounding and masterbatching, film extrusion and sheet production, conversion (printing, laminating, thermoforming, injection and compression molding), and then distribution to end-users including food, beverage, personal care and household, healthcare, industrial manufacturing, and retail and e-commerce. Russia's push for feedstock security is visible in large petrochemical investments such as the Amur complex, while converters and packers are increasingly prioritizing barrier performance, downgauging, and compatibility with high-speed filling and sealing lines to serve FMCG, ready meals, and parcel logistics.

Midstream, trade associations such as the Association of Plastic Processors (APP/SPP) act as an industry coordinator with the Ministry of Industry and Trade on technical standards and trade measures. Industry forums have addressed constraints including the risk that anti-dumping duties on imported inputs can tighten supply during periods of limited local availability. Downstream, e-commerce and long-haul distribution across Russia's geography increase demand for durable flexible packaging, while bank-supported modernization and localized capability upgrades are emerging, including the June 2026 launch of mass production of barrier skin packaging at the Desnogorsk Polymer Plant supported by VTB financing, which improves access to higher-value formats within the country.

Competitive Landscape

Domestic champions such as SIBUR secure feedstock through vertical integration and now add 1 000 tonnes of local catalysts to deepen supply sovereignty.[1]ChemAnalyst, “SIBUR’s Catalyst Leap,” ChemAnalyst, chemanalyst.com Gotek’s RUB 1.6 billion acquisition expanded capacity in sacks, film, and corrugated trays, elevating it into the top three pack suppliers. International firms respond with selective divestments; Amcor exited direct operations in early 2025 but maintains technology-licensing arrangements, ensuring its multilayer know-how circulates through Russian partnerships.[2]Amcor, “Q2 2025 Press Release,” Amcor, amcor.com

Technology adoption sets new competitive benchmarks. High-speed counting-and-crating systems now process 600 cases hourly, slashing labor costs and giving early movers a 2–3 ppt margin edge . 2024 switch from divisional to end-market business units speeds co-development of custom resins for flexible sachets and rigid closures. On the sustainability front, Amcor’s tie-up with Kolon for chemically recycled PET supplies future PCR laminate inputs .

Mid-tier challengers exploit export white-space. Atlantis-Pak showcases barrier casings at Asian expos, positioning itself as a one-stop OEM for halal and ready-meal brands.[3]Atlantis-Pak, “News,” Atlantis-Pak, atlantis-pak.top Equipment makers delivering gravimetric dosing and automated reel splicing further tighten quality variance. Taken together, these maneuvers reinforce moderate consolidation inside the Russia plastic packaging market.

Russia Plastic Packaging Industry Leaders

Valmapak, LLC

Mirpack Company, LLC

SIBUR Holding PJSC

AptarGroup, Inc.

ALPLA Werke Alwin Lehner GmbH and Co KG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

EPR reform and higher recycling obligations are expanding whitespace for packaging redesign and compliance services, particularly mono-material flexible structures, recycled-content resins, and traceable documentation workflows around eco-fee reporting. Regulatory anchors in 2026 include the 75% packaging recycling mass requirement referenced for 2026, alongside tighter reporting discipline, with April 15 submissions via EFGIS UOIT. This combination supports demand for converters that can supply compliant packaging specifications and help customers with documentation and recyclability claims.

Capacity additions and localization projects are also creating near-term investment and partnership openings across films and high-barrier formats. In March 2026, YamburgPromInvest Plast announced construction of a new film and plastics sheeting plant in the Ust-Luga Special Economic Zone (Leningrad Oblast) with a RUB 5 billion investment, highlighting active build-out in film supply near a major logistics node. On materials and verification, the March 2026 launch of the National Certification System for Sustainable Development and Carbon Neutrality (SURIUN) and the adoption of GOST R 72006-2025 introduce a new pathway for packaging producers to differentiate sustainability performance. Industry dialogue at RosUpack 2026 also highlighted practical shifts toward Asian technology partnerships and recyclable mono-material adoption, reinforcing a market environment where converters that can localize equipment, qualify new polymer grades, and certify claims gain share with FMCG and e-commerce customers.

Recent Industry Developments

- June 2026: SIBUR developed a new bimodal HDPE grade (HD21550 CC) for 38-mm beverage caps used in dairy, juice, and tea closures, designed for both injection and compression molding. The grade is intended to support consistent processing and performance in high-throughput cap manufacturing, enabling domestic substitution for closure resin demand.

- April 2025: SIBUR Khimprom installed two reactors for DOT plasticizer production, expanding local availability of key additives used across plastics processing. This supports converters dealing with import friction on formulation inputs and improves resilience for domestic packaging production.

- January 2024: Russia's e-commerce turnover reached RUB 19.9 trillion in 2024, accelerating demand for mailer bags, stretch wrap, and tamper-evident flexible packaging used across fulfillment networks. The scale-up in parcel flows reinforced investment in automated packing lines and higher-performance films suited for long-distance distribution.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers plastic packaging used in Russia across rigid and flexible formats, measured as the quantity of packaging shipped into end uses like food, beverage, retail, healthcare, and industrial applications.

Scope exclusions: Paper, metal, and glass packaging are excluded, and packaging machinery and packaging services are also not counted.

Segmentation Overview

- By Material

- Polyethylene Terephthalate (PET)

- Polyethylene (PE)

- High-Density Polyethylene (HDPE)

- Low-Density and Linear-LDPE

- Linear Low-Density Polyethylene (LLDPE)

- Polypropylene (PP)

- Biodegradable and Bio-based Plastics

- Other Materials

- By Type

- Rigid Plastic

- Flexible Plastic

- By Product

- Bottles and Jars

- Cans

- Pouches

- Trays and Clamshells

- Caps and Closures

- Other Products

- By End-User Industry

- Food

- Beverage

- Healthcare and Pharmaceuticals

- Retail and E-commerce

- Industrial Manufacturing

- Personal Care and Household

- Other End-User Industries

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to build the structure of the market, anchor the historical direction, and set realistic input ranges before we modeled volumes. We relied on public statistics and standards documents such as national statistics releases, customs and trade data, packaging and plastics association publications, polymer and materials data from intergovernmental bodies, and peer reviewed technical papers on resin use and recyclability.

To make the numbers usable for a market model, these sources were connected to practical signals like polymer availability, packaging conversion activity, and end market demand indicators. We also reviewed company presentations, annual disclosures, plant announcements, and reputable news to track capacity additions, shutdowns, and shifts toward recycled content and compliant formats. Where needed, we supplemented public information with paid subscriptions that provide company financials and intelligence, news and financials, patent databases, and an import export shipment level database to reduce blind spots. The sources listed here are illustrative only, and many other references were checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating how much packaging is actually being shipped and which end uses are expanding faster, since public data is often reported in broader plastics or packaging totals. We spoke with a mix of resin suppliers, packaging converters, brand owners, and distribution linked stakeholders across Russia so our assumptions on format mix, substitution, and demand seasonality could be tested and corrected.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | APAC: 45% |

| Mid tier: 54% | Functional/Unit leaders: 39% | EMEA: 30% |

| Smaller Players: 15% | Managers: 48% | Americas: 25% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up combination. We reconstructed national packaging demand from end-use consumption and conversion activity, then cross-checked with supplier and converter level approximations. In practice, the top-down layer starts with demand pools in food and beverage, retail and e-commerce shipping needs, healthcare packaging use, and industrial consumption, which are then translated into packaging format demand using penetration and pack rate logic.

The model was made sensitive to market fingerprints that typically move plastic packaging volumes in Russia, such as polymer supply additions and availability (PET, PE, PP), format shifts between rigid and flexible packaging, growth in pouches and caps and closures, substitution trends toward recycled or bio-based grades, and changes in packaged food and beverage throughput. To keep the sizing realistic, we also ran bottom-up checks like sampled converter capacity utilization, channel discussions on order patterns, and price per kg ranges to test whether implied volume and value relationships looked sensible. Where there were gaps, we used conservative ranges first, and then narrowed them after interviews.

For forecasting, scenario analysis was used so we could reflect different outcomes for consumer demand, trade conditions, and regulatory pressure on single-use items and recycled content. The final forecast path was selected only after primary respondents confirmed the likely direction for format mix, resin availability, and the pace at which compliant structures are being adopted.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, then checked for variance by packaging type, resin mix, and key end-use demand patterns, so one strong assumption could not distort the total. When an input created an unusual jump, the driver was traced to a specific data point. We then ran a second analyst review and, where needed, re-checked the point with a relevant interviewee.

Before sign-off, the model totals are compared against external indicators like polymer conversion trends, trade movement signals, and observable capacity changes, and then the full logic chain is reviewed for internal consistency. Reports are refreshed annually. Interim updates are triggered by material events such as major capacity additions, policy changes, or sharp shifts in resin supply, and we run a final pre-delivery pass so the published view stays current.

Mordor Intelligence's Russia Plastic Packaging Market Size Compared With Other Published Estimates

Published market sizes for Russia plastic packaging often differ because the unit of measure is not the same, the included materials and formats are not consistent, and the conversion from volume to value depends heavily on price assumptions. Variations also come from how firms handle import dependence, recycled content shifts, and whether they refresh key inputs after sudden changes in resin availability.

Glass, metal, and paper packaging sit outside Mordor Intelligence's scope, which is one reason some broader packaging figures look larger even when they describe similar end markets. Another driver is the measurement basis, where our reported baseline is in tonnes, while some public estimates publish a USD value that can swing based on which price series is used for polymers and converted packaging, and what currency timing is applied.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.77 M (2025) | |

| Global Consultancy A | USD 8.00 B (2024) | Uses a value-based definition that can embed converter pricing and inflation assumptions, and the scope description does not clearly separate plastic packaging from broader packaging activity in all end uses. |

| Regional Consultancy B | USD 6.80 B (2026) | Publishes a future-year value point and then applies a long-horizon CAGR, which can under or overstate near-term shifts in resin mix, import availability, and format substitution between rigid and flexible. |

The table shows that most of the spread is explained by unit choice and scope breadth, followed by how prices and currency timing are treated when converting packaging demand into USD. By keeping the model tied to observable packaging volumes and then testing implied value with realistic price ranges, we get a repeatable number that clients can reconcile back to clear market drivers.

Key Questions Answered in the Report

How large is the Russia plastic packaging market in 2026?

The Russia plastic packaging market size stands at 1.89 million tonnes in 2026 and is projected to grow at 7.05% CAGR to 2031.

Which material leads demand in Russian plastic packs?

Polyethylene remains the leading material, accounting for 28.42% of volume in 2025.

Why are flexible formats gaining share in Russia?

Flexible films and pouches deliver weight savings, lower freight costs, and fit automated e-commerce fulfilment, driving their 7.76% CAGR through 2031.

What is the fastest-growing end-use segment?

Personal-care and household goods packaging is expected to expand 9.08% per year thanks to brand premiumization and higher PCR content targets.

How will new domestic petrochemical capacity affect pricing?

When the Amur Gas Chemical Complex comes online, local PE and PP supply should temper import reliance and reduce raw-material price volatility for converters.

Page last updated on: