Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.41 Billion |

| Market Size (2026) | USD 2.52 Billion |

| Market Size (2031) | USD 3.11 Billion |

| Growth Rate (2026 - 2031) | 4.36% CAGR |

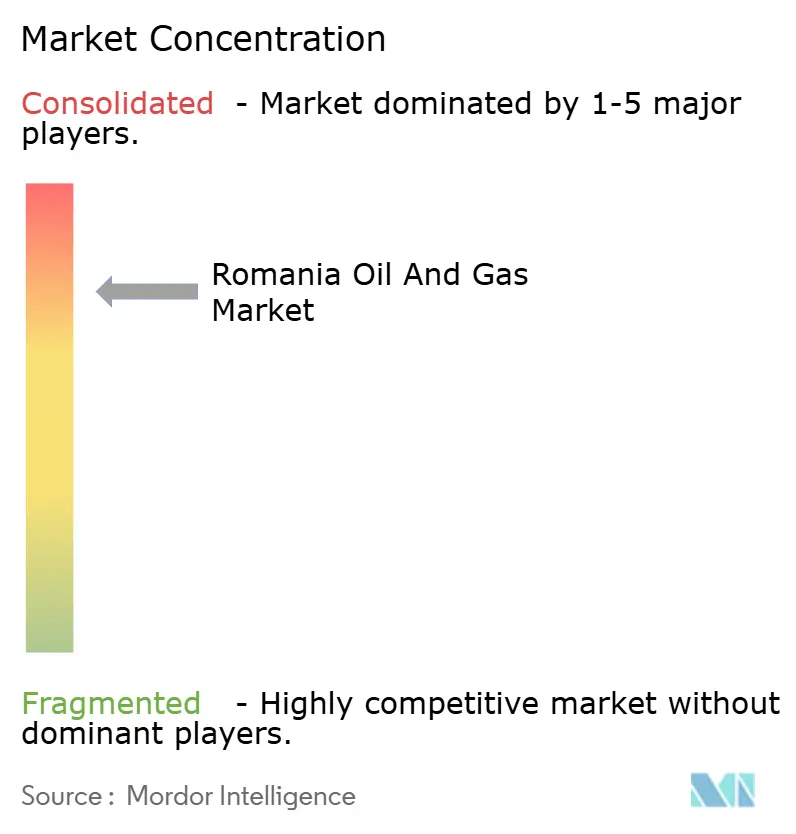

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Romania Oil And Gas Market Analysis by Mordor Intelligence

The Romania Oil And Gas Market size is expected to grow from USD 2.41 billion in 2025 to USD 2.52 billion in 2026 and is forecast to reach USD 3.11 billion by 2031 at 4.36% CAGR over 2026-2031.

Upstream investment anchored by the Neptun Deep project, fiscal reforms that accelerate depreciation of offshore assets, and steady pipeline modernization drive the most visible growth momentum. Black Sea discoveries, coupled with the capacity increases of the BRUA corridor, position Romania as a regional supply node at a time when EU buyers are rebalancing away from traditional routes. Digital transformation programs, ranging from artificial intelligence-assisted drilling to predictive maintenance, increase asset uptime and reduce costs, making even mature onshore wells economically viable. Emerging service lines, such as well abandonment and site remediation, respond to stricter environmental compliance norms and create new revenue streams.

Key Report Takeaways

- By sector, the upstream sector led with 71.42% of Romania's oil and gas market share in 2025, while the upstream segment is expected to advance at a 4.9% CAGR through 2031.

- By location, onshore assets captured 58.35% of Romania's oil and gas market size in 2025, whereas the offshore segment is expected to expand at a 7.2% CAGR to 2031.

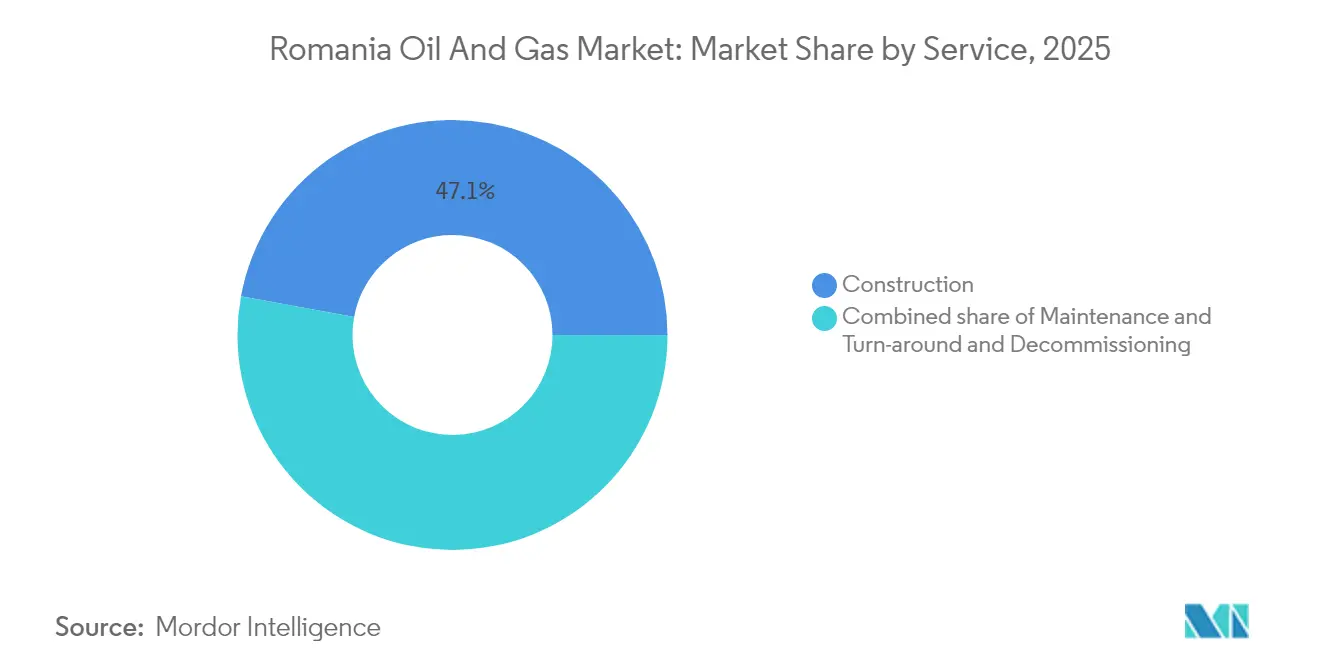

- By service, construction services accounted for 47.12% of Romania's oil and gas market size in 2025, and decommissioning services registered the highest 6.5% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Romania Oil And Gas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising domestic gas demand for power generation & industry | +1.20% | National, with concentration in Bucharest-Ilfov, Constanța industrial zones | Medium term (2-4 years) |

| Black Sea offshore gas discoveries & development | +1.80% | Black Sea offshore zones, coastal infrastructure in Constanța County | Long term (≥ 4 years) |

| Fiscal reforms incentivising upstream investment | +0.90% | National upstream operations, enhanced focus on offshore blocks | Short term (≤ 2 years) |

| Expansion of regional interconnectors (BRUA pipeline) | +0.70% | Regional, connecting Romania-Bulgaria-Austria-Hungary corridor | Medium term (2-4 years) |

| Digitisation & advanced analytics adoption in O&G operations | +0.50% | National, with early implementation in major upstream facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Domestic Gas Demand for Power Generation & Industry

Romania's thermal power fleet is increasingly relying on gas as coal-fired plants retire in line with EU climate directives, prompting utilities to secure long-term supply contracts.(1)Romanian Ministry of Energy, “National Energy Consumption Statistics 2024,” ENERGIE.GOV.RO Industrial gas use is climbing in chemicals and metallurgy, where operators must curb carbon intensity to keep EU market access. Domestic demand is forecast to reach 12-13 billion m³ annually by 2030, widening today's supply gap and strengthening the economic case for Neptun Deep. Cross-border sales grow in parallel; a May 2025 deal commits OMV Petrom to meet 25 % of Moldova's yearly needs, demonstrating how Romania's oil and gas market participants secure new offtake channels. The demand trend is therefore a structural, medium-term driver that sustains capacity additions onshore and offshore.

Black Sea Offshore Gas Discoveries & Development

Seismic campaigns highlight several prospects that could formally double Romania’s proven reserves within a decade, led by the 100 billion m³ Neptun Deep reservoir.(2)Romanian National Agency for Mineral Resources, “Black Sea Reserve Estimates Report,” ANRM.RO Investment structures totaling USD 4.4 billion include wells in water exceeding 1,000 meters, subsea tie-backs, and new gas processing terminals. At its 8 billion m³ plateau, the field alone would enable the country to switch from a net importer to a net exporter. The adoption of technology, particularly remote-operated vehicles and high-pressure subsea equipment, reduces unit lifting costs despite harsh deepwater conditions. Although the first gas is expected in 2027, long lead times lengthen the driver’s influence well beyond 2030.

Fiscal Reforms Incentivizing Upstream Investment

A 2024 ordinance reduced supplemental taxes, accelerated depreciation, and introduced ring-fencing for frontier plays, correcting earlier fiscal instability that had stalled wildcat drilling.(3)Romanian Ministry of Finance, “Fiscal Reforms for Upstream Investment Incentives,” MFINANTE.GOV.RO Capital budgeting now reflects higher post-tax returns, unlocking deferred portfolios in Midia and Trident blocks. The reforms lower payback thresholds for high-CAPEX deepwater projects, crowding in both domestic and international capital. Uncertainty has eased further since the creation of ANRMPSG, which integrates environmental and technical approvals under a single agency, thereby shortening timelines by approximately 15 months.

Expansion of Regional Interconnectors (BRUA Pipeline)

Phase 2 financing of EUR 93.5 million upgrades compressor stations, lifts reversible flow, and adds metering that allows Romanian producers to access hub pricing in Baumgarten, Austria.(4)European Investment Bank, “Romania Pipeline Infrastructure Financing Agreement,” EIB.ORGPost-2026, export optionality is expected to narrow basis differentials and raise achieved netbacks for Black Sea volumes. Flexible capacity supports seasonal arbitrage, enabling operators to optimize throughput during peak winter demand. Strategic value accelerated after the 2022 supply shock, when EU utilities started diversifying away from legacy sources.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX amid oil-price volatility | -1.10% | National upstream operations, concentrated in offshore developments | Medium term (2-4 years) |

| Regulatory uncertainty & frequent policy changes | -0.80% | National regulatory framework, affecting all market segments | Short term (≤ 2 years) |

| Skilled-labour shortages in offshore operations | -0.60% | Offshore Black Sea operations, specialized technical roles | Long term (≥ 4 years) |

| Public opposition & environmental litigation | -0.40% | Coastal areas, offshore drilling zones, urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX amid Oil-Price Volatility

Neptun Deep’s USD 4.4 billion price tag is nearly twice the size of the 2024 Romanian oil and gas market, leaving sponsors highly exposed to cyclical swings. Rig day-rates, steel procurement, and debt service costs correlate closely with Brent benchmarks, complicating budget discipline. Development lead times of up to seven years mean that price forecasts must remain credible across multiple cycles. Domestic firms have thinner balance sheets than international majors, which limits their ability to absorb shocks and strains on project finance structures.

Regulatory Uncertainty & Frequent Policy Changes

Between 2020 and 2024, Romania introduced three separate royalty schedules and amended supplementary taxes twice, sending mixed signals to investors. Although ANRMPSG consolidates oversight, environmental lawsuits continue to extend license approvals, with Greenpeace appeals adding precedent-setting delays.(5)Greenpeace Romania, “Environmental Impact Assessment Challenges,” GREENPEACE.ORG Operators must increase compliance budgets to navigate shifting rules, diverting resources from core drilling activities, and maintain redundant scenario plans that inflate overall project costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Upstream Drives Market Leadership

The upstream segment accounted for a dominant 71.42% share of Romania's oil and gas market in 2025, a position strengthened by investments in the Black Sea. Romania's oil and gas market size for the upstream sector is projected to expand at a 4.9% CAGR to 2031, driven by the development of 15 new offshore wells and digital upgrades in legacy fields. Streamlined fiscal terms enable faster depreciation, which, when combined with predictive analytics, enhances breakeven economics for marginal oil and gas reservoirs. Midstream expansion follows production growth: Transgaz is lengthening gathering systems and adding cryogenic processing to handle higher condensate yields. Downstream operations face margin compression due to EU carbon pricing and competition from Polish refineries, which limits growth prospects even as modernization continues.

Advanced techniques such as polymer flooding extend recovery rates in Carpathian onshore fields, damping natural declines and providing near-term barrels until offshore volumes peak. The government's Industrial Strategy 2024-2030 elevates upstream autonomy as a pillar of national security, underpining steady licensing rounds. New ANRMPSG guidelines require an environmental impact assessment in the planning phase, encouraging operators to adopt best-in-class waste management practices. Over the forecast period, upstream gains reinforce the value proposition that domestic molecules mitigate import exposure.

By Location: Offshore Acceleration Challenges Onshore Dominance

Onshore sites retained 58.35% of Romania's oil and gas market share in 2025, reflecting decades of existing wells, installed gathering lines, and a workforce familiar with the sector. However, offshore acreage posts the fastest expansion, with a 7.2% CAGR, led by deepwater blocks that open larger, contiguous resource bases. The shift amplifies capital intensity; a single subsea template offshore equals the drilling budget for multiple onshore infill campaigns. Romania's oil and gas market share may shift toward offshore by 2030, once Neptun Deep reaches its plateau; however, onshore remains strategic for cash flow and local employment.

Transgaz's EUR 93.5 million upgrade equips the BRUA corridor to evacuate incremental offshore gas, creating a fluid interface between locations.ISO 14001 certification harmonizes environmental controls, but offshore players face extra layers under the EU Marine Strategy directives. Service suppliers are pivoting to vessel leasing, remote monitoring, and dynamic positioning skills that command premium day rates. Onshore firms, by contrast, focus on cost discipline, horizontal sidetracks, and produced-water re-injection, reflecting different risk-reward profiles. The two settings thus coexist, each with its own tailored operating model and investment threshold.

By Service: Construction Leads as Decommissioning Emerges

Construction services captured 47.12% of Romania's oil and gas market share in 2025, closely correlated with platform fabrication, pipeline welding, and topside integration for Black Sea projects. High-value EPC contracts mobilize domestic yards in Constanța and global specialists for deepwater mooring systems. Romania's oil and gas market size is growing steadily in the construction sector, as long-lead items are ordered three to four years before the first gas production. Maintenance and turnaround services hold mid-cycle revenue streams centered on rotating equipment overhauls and integrity inspections.

Decommissioning is the fastest-growing service line, with a 6.5% CAGR, leveraging new rules that obligate asset retirement fund accrual during the productive life of assets. Over 600 onshore wells drilled before 1990 approach end-of-life status, requiring plug-and-abandon programs and soil restoration. Specialized contractors deploy cementing units, wellbore logging, and remediation chemicals tailored to Romanian geology. As mature assets sunset, the share of decommissioning in Romania's oil and gas market is expected to widen, creating a balanced service mix between growth-oriented construction and risk-mitigation-driven retirement work.

Geography Analysis

Romania's oil and gas market development exhibits clear spatial patterns rooted in geologic endowment, infrastructure availability, and regional demand centers. The Black Sea continental shelf represents the principal upside, hosting an estimated 200 billion m³ in contingent gas resources awaiting appraisal. Constanța County serves as an operational hub; its shipyards fabricate jackets, and its port handles heavy-lift modules, shortening logistics cycles for offshore campaigns. Inland, the Carpathian Basin continues to produce reliable output from mature sandstone reservoirs, where water flooding and polymer injection extend plateau phases.

Greater Bucharest sits at the heart of national demand, absorbing roughly 30 % of domestic gas for power plants such as Elcen South and for combined-heat-and-power systems in residential blocks. The BRUA corridor repositions western Romania as a strategic transit zone, enabling reverse flows toward Hungary during high-demand winters and feeding Austrian hubs under normal conditions. Southeastern counties near Bulgaria benefit from bidirectional compressors, which augment supply resilience following regional supply disruptions in 2022.

Environmental governance differs across zones. Coastal operations must comply with EU Marine Spatial Planning, leading to extended baseline monitoring for sea mammals and benthic habitats. Inland projects operate under terrestrial Natura 2000 constraints, especially near protected Carpathian forests. Workforce distribution also varies: offshore crews rotate from Constanța heliports, while onshore staff reside in small towns such as Ploiești and Târgu Mureș. Regional universities, including Ovidius University of Constanța, incorporate petroleum engineering electives to address skill gaps, thereby embedding human capital clusters in project hotspots.

Competitive Landscape

The Romanian oil and gas market exhibits moderate concentration, with OMV Petrom and Romgaz jointly controlling approximately 60% of the upstream output. Meanwhile, a handful of large service providers handle deepwater scopes. International majors, including TotalEnergies and ExxonMobil, continue to bid selectively for exploration blocks but are increasingly partnering with Romanian firms to mitigate regulatory risks. Competitive advantages hinge on operational efficiency, digital maturity, and compliance track record, factors that shape ANRMPSG approvals and access to strategic investment thresholds.

Technology adoption differentiates front-runners. OMV Petrom reports 15-20 % uptime gains from predictive maintenance systems, while Romgaz trials artificial-intelligence-assisted reservoir modeling to pinpoint infill well locations. Service contractors are diversifying into remote operations centers, which reduce offshore headcount, a critical edge amid skilled labor shortages. Decommissioning, still a nascent field, attracts specialized players such as Petrofac Romania, which applies North Sea learnings to Carpathian geology.

Capital strength remains a pivot. Transgaz raised EUR 93.5 million from the EIB, underscoring financiers’ appetite for transmission assets with stable rate-based returns. Equity markets likewise rewarded Romgaz’s EUR 385 million bond issuance, signaling investor confidence in monetizing Black Sea gas after first production in 2027. Conversely, smaller independent firms face funding constraints as lenders scrutinize their commodity exposure and regulatory uncertainty. The entry of renewable developers into corporate procurement pools challenges incumbents to prove competitive returns and transparent emissions management.

Romania Oil And Gas Industry Leaders

OMV Petrom SA

Serinus Energy Company

Exxon Mobil Corporation

Romgaz SA

Total S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: OMV Petrom and Romgaz have commenced drilling operations at the Neptun Deep project in the Black Sea, marking the start of Romania's most significant offshore gas development, with first production targeted for 2027.

- January 2025: Transgaz secured EUR 93.5 million in financing from the European Investment Bank for the expansion of the Black Sea-Podișor pipeline, enhancing Romania's gas evacuation capacity and regional interconnector capabilities.

- September 2024: OMV Petrom announced the discovery of Romania's largest oil field in decades, located in the Carpathian region, with estimated reserves exceeding 10 million barrels.

- June 2024: OMV Petrom announced the discovery of Romania's largest oil field in decades, located in the Carpathian region, with estimated reserves exceeding 10 million barrels.

- May 2024: Romgaz completed a EUR 385 million bond issuance to finance expansion projects and working capital requirements, demonstrating strong investor confidence in Romania's gas sector growth prospects.

Romania Oil And Gas Market Report Scope

The Romania oil and gas market report include:

By Sector

| Upstream |

| Midstream |

| Downstream |

By Location

| Onshore |

| Offshore |

By Service

| Construction |

| Maintenance and Turn-around |

| Decommissioning |

| By Sector | Upstream |

| Midstream | |

| Downstream | |

| By Location | Onshore |

| Offshore | |

| By Service | Construction |

| Maintenance and Turn-around | |

| Decommissioning |

Key Questions Answered in the Report

How large is the Romania oil and gas market today?

Romania oil and gas market size was USD 2.52 billion in 2026 and is projected to reach USD 3.11 billion by 2031 at a 4.36 % CAGR.

When will Neptun Deep start producing gas?

Operators target first gas from Neptun Deep in 2027, with plateau output forecast at 8 billion m³ annually.

Which segment grows fastest within Romanian services?

Decommissioning services show the quickest pace at 6.5 % CAGR due to stricter end-of-life rules for aging wells.

How does BRUA pipeline expansion affect Romania?

Additional compressor capacity lifts throughput to 4.4 billion m³ per year, enabling exporters to access Central European hubs.

What reforms make Romania attractive for upstream investors?

A 2024 fiscal package cut supplemental taxes and introduced accelerated depreciation for offshore assets, boosting post-tax returns.

Which companies dominate Romanian production?

OMV Petrom and Romgaz together provide roughly 60 % of national upstream volumes, underlining their leadership.

Page last updated on: