Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

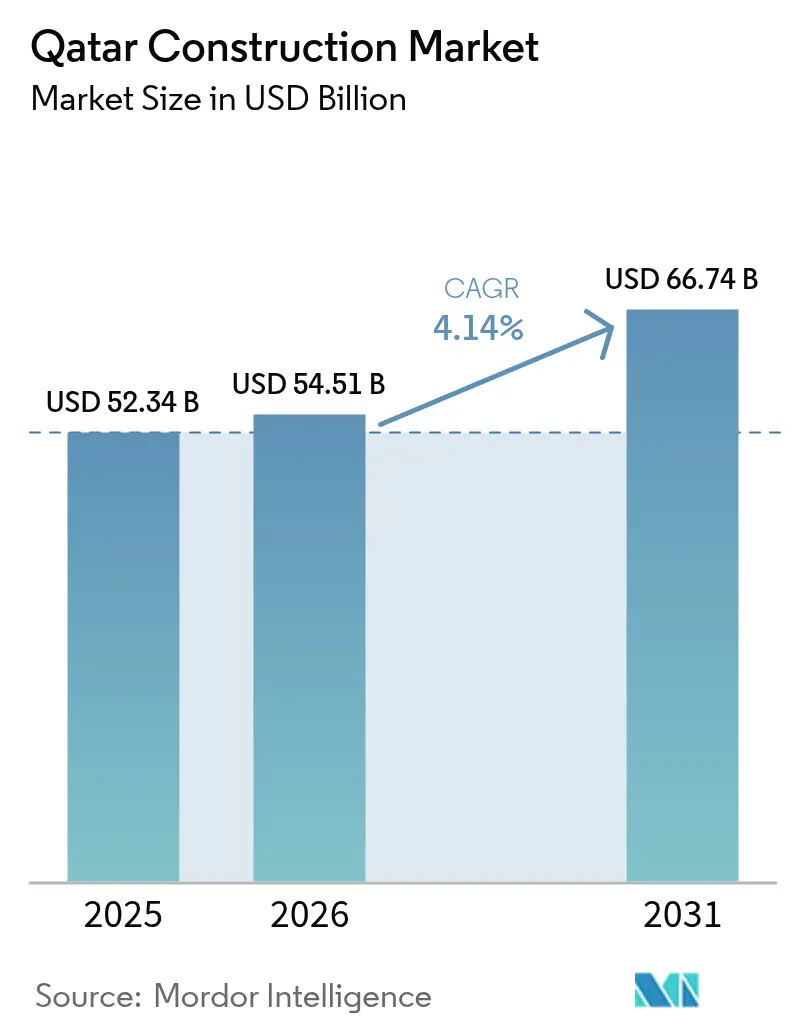

| Base Year Market Size (2025) | USD 52.34 Billion |

| Market Size (2026) | USD 54.51 Billion |

| Market Size (2031) | USD 66.74 Billion |

| Growth Rate (2026 - 2031) | 4.14% CAGR |

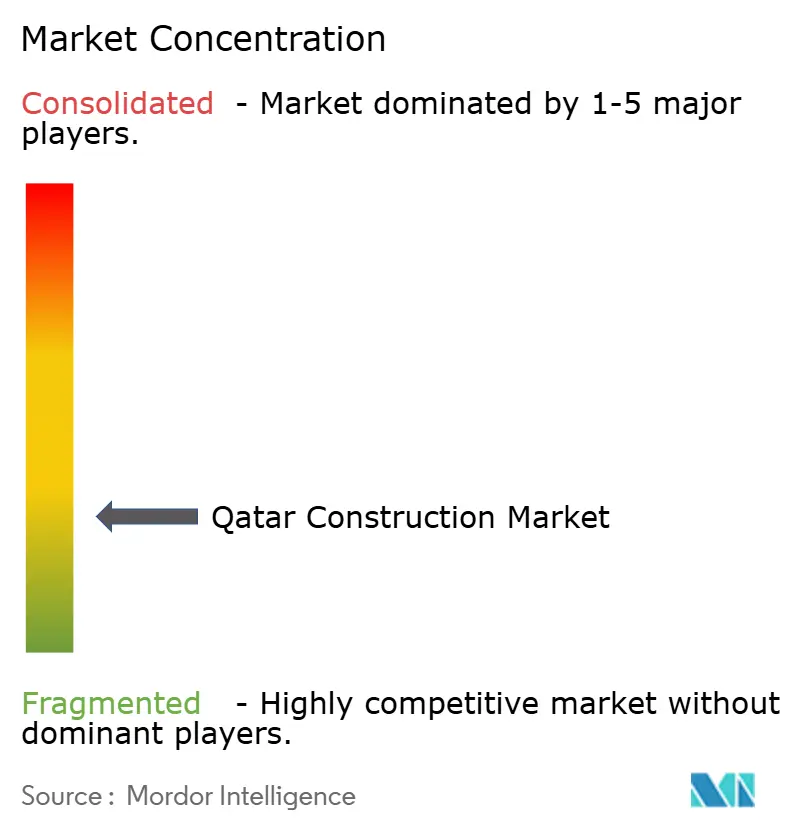

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Construction Market Analysis by Mordor Intelligence

The Qatar Construction Market size was valued at USD 52.34 billion in 2025 and estimated to grow from USD 54.51 billion in 2026 to reach USD 66.74 billion by 2031, at a CAGR of 4.14% during the forecast period (2026-2031). This steady expansion is anchored in the nation’s long-term economic diversification agenda under Qatar National Vision 2030, large-scale public spending on transport and energy infrastructure, and an accelerating pipeline of liquefied natural-gas (LNG) projects spearheaded by QatarEnergy. Progressive adoption of modular construction, heightened private-sector participation through newly formalized public-private-partnership (PPP) frameworks, and resilient demand for renovation of post-World-Cup assets further reinforce the growth trajectory of the Qatar construction market. Meanwhile, climate-resilient design requirements, rising digital-twin adoption, and a deepening focus on lifecycle asset management are reshaping bidding criteria and contractor capabilities across the construction value chain. Competitive intensity has intensified as global engineering, procurement, and construction (EPC) majors enter consortia with local firms to capture multi-billion-dollar contracts linked to the North Field LNG expansion, the Doha metro build-out, and smart-city projects such as Lusail.

Key Report Takeaways

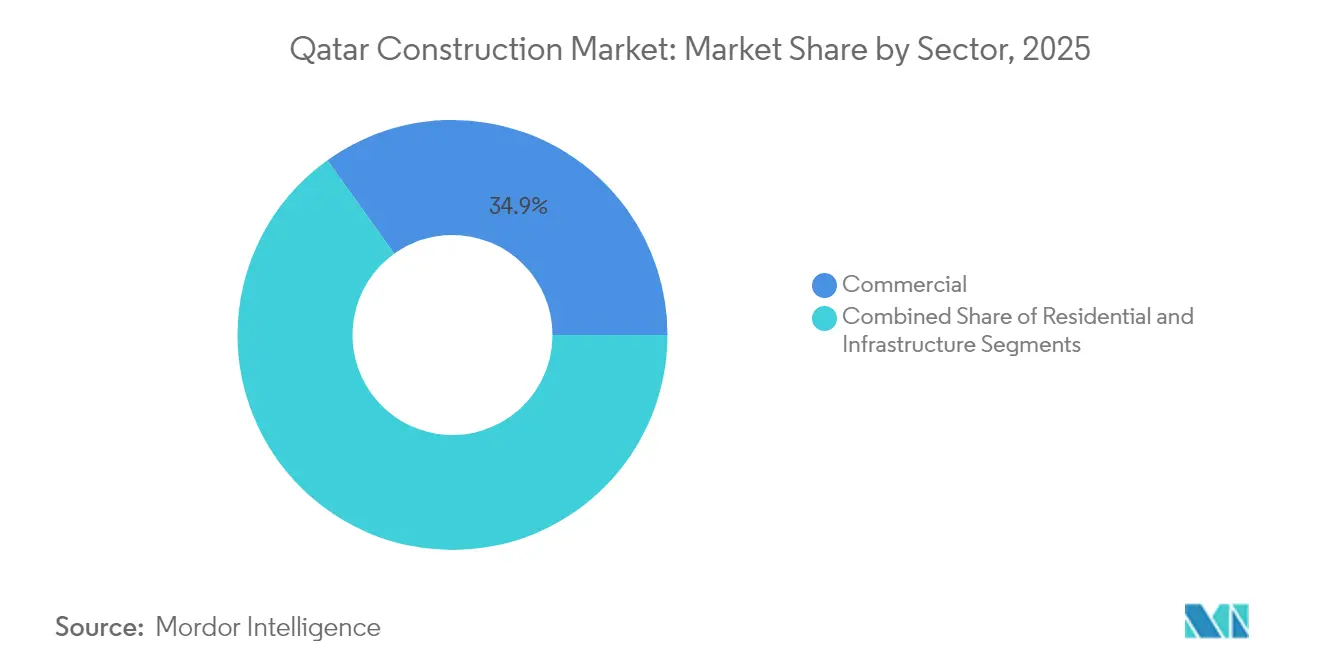

- By sector, the commercial segment led with 34.89% revenue share in 2025; infrastructure is projected to advance at a 4.87% CAGR through 2031.

- By construction type, new construction accounted for 74.25% of the Qatar construction market share in 2025, while renovation is forecast to grow at 6.08% CAGR to 2031.

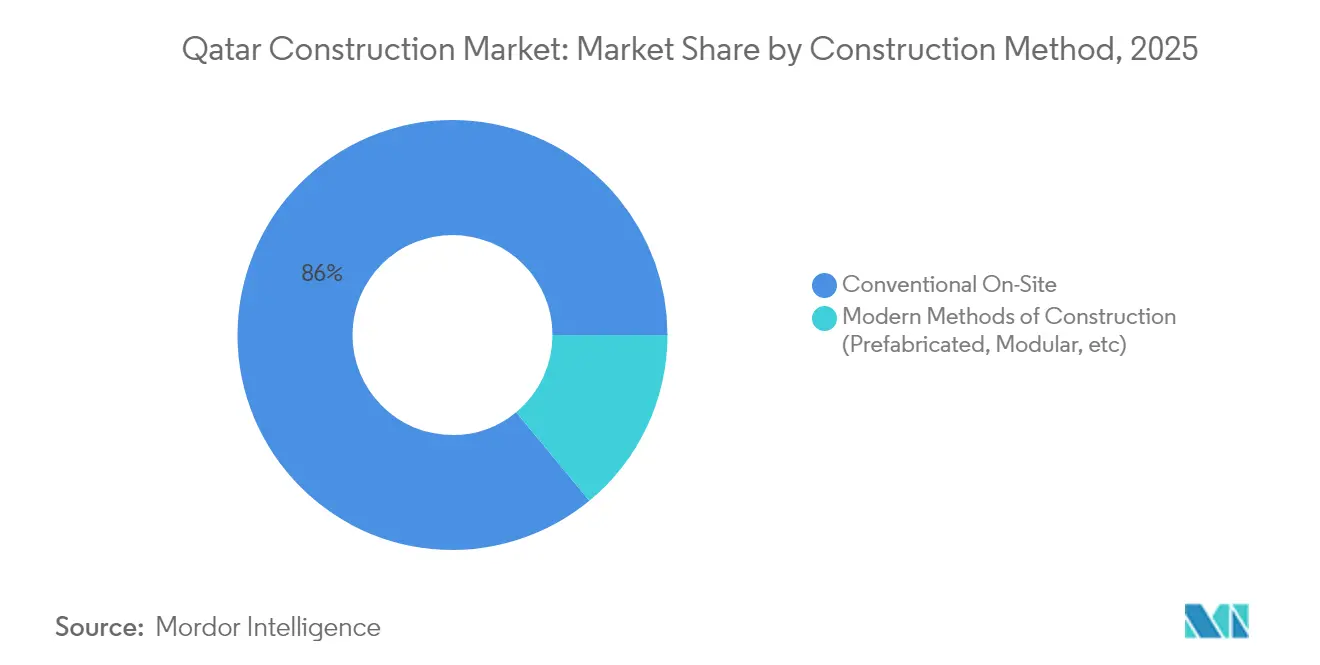

- By construction method, conventional on-site techniques dominated with an 85.98% share in 2025; modern modular approaches are set to expand at a 6.29% CAGR through 2031.

- By investment source, public funding sustained 77.95% of overall activity in 2025; private participation is rising at 6.02% CAGR under the evolving PPP law.

- By Geography, Doha captured 63.05% of 2025 spending; secondary hubs such as Al Wakrah are pacing ahead at 6.38% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| North Field LNG & transport mega-projects | +1.8% | Ras Laffan, Mesaieed | Medium term (2-4 years) |

| Government mega-investment pipeline | +1.2% | Doha, Lusail | Long term (≥ 4 years) |

| Rapid urbanization & population growth | +0.7% | Doha metro area | Long term (≥ 4 years) |

| Adoption of modular/off-site construction | +0.3% | Nationwide | Medium term (2-4 years) |

| AI & data-center infrastructure boom | +0.2% | Doha tech zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

North Field LNG Expansion Catalyzes Industrial Construction Boom

The North Field East, South, and West phases exceed USD 50 billion in combined outlays, expanding LNG output from 77 mtpa to 142 mtpa by 2030. Each phase integrates carbon-capture technology expected to cut project emissions by 25%, demanding specialized green-construction materials and engineering solutions. Peak onsite workforce is set at 45,000 workers, and over 600,000 m³ of concrete will be poured, strengthening order books for regional ready-mix manufacturers. Contracts awarded to Saipem, McDermott, Technip Energies, and Larsen & Toubro underscore the project’s global pull and position Qatar as a reference for mega-scale LNG construction excellence. Its mid-term completion schedule underpins robust civil, marine-jetty, and mechanical-erection activity across the Qatar construction market.

Government Mega-Investment Pipeline Drives Long-Term Infrastructure Transformation

Qatar’s Third National Development Strategy allocates USD 85 billion to infrastructure through 2030, catalyzing continuous demand across transport, sanitation, and public-facility segments. Ashghal’s Major Expressway Programme alone covers 45 km of sewer tunnels and 70 km of interceptor sewers, boosting opportunities in tunneling, geotechnical, and smart-maintenance services. Procurement frameworks increasingly mandate lifecycle asset-management provisions, nudging contractors toward digital-twin platforms and predictive maintenance offerings. Outsourced programme-management partnerships with global firms such as Parsons and AECOM ensure international best practices while upskilling local talent. Overall, the sustained pipeline supports capacity utilization for domestic materials suppliers and secures multi-year visibility for the Qatar construction market[1]International Trade Administration, “Qatar Construction Sector Overview,” trade.gov.

Rapid Urbanization Intensifies Infrastructure Demand and Design Complexity

Doha’s built-up footprint expanded 777% between 1984 and 2020, now hosting 85% of Qatar’s population. This demographic concentration has increased storm-runoff by 422%, prompting city planners to specify advanced drainage and flood-resilient road sub-grades for new districts. Mixed-use icons such as Pearl-Qatar, with USD 15 billion invested to deliver housing for 45,000 residents at 93% occupancy, reveal pent-up appetite for high-density waterfront developments. Transit-oriented projects around Doha Metro stations accelerate vertical residential demand, while older neighborhoods like Al Sadd pivot toward regeneration schemes that merge heritage façades with smarter utilities. Collectively, these trends heighten demand for civil engineering, MEP retrofits, and landscape-urbanism services in the Qatar construction market.

Modular Construction Adoption Accelerates Through Government Support and Efficiency Demands

Design for Manufacturing and Assembly principles are gaining traction as heat-stress constraints and skilled-labor limits push builders toward controlled factory settings. Ashghal’s pilot tenders for prefabricated utility corridors and schools have demonstrated 20% schedule savings and 15% waste reduction, validating the model for broader rollout. Joint ventures between Qatari developers and European modular specialists now supply volumetric units for Lusail’s mid-rise towers, with domestic fabrication plants scaling capacity to 10,000 units annually. Financial institutions increasingly view modular pipelines as lower-risk assets because of predictable cash-flow timing and quality assurance. As cost curves improve, modular penetration is poised to rise across hospitality, worker-accommodation, and data-center projects, lifting efficiency benchmarks within the Qatar construction market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile construction-material prices | -0.8% | Nationwide | Short term (≤ 2 years) |

| Post-World-Cup real-estate correction | -0.6% | Doha, major cities | Medium term (2-4 years) |

| Skilled-labor gap for advanced methods | -0.5% | Nationwide | Medium term (2-4 years) |

| Slow PPP-framework implementation | -0.3% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Construction-Material Prices Create Cost-Management Challenges

Qatar remains reliant on imported cement clinker, steel rebar, and specialty façades, exposing contractors to freight swings and foreign-exchange risks. Aggregate demand is partially mitigated by Qatar Primary Materials Company’s berth expansion to 30 million t annual capacity by 2026, yet local sand reserves may deplete within five years. Commodity-price spikes triggered 6.5% consumer-price inflation in December 2021, inflating transport costs by 10.2% year-on-year before easing to a projected 2.4% band in 2025. Contractors are adopting hedging and indexed contract clauses, but margin pressure persists, trimming near-term growth in the Qatar construction market.

Post-World-Cup Real-Estate Correction Dampens Commercial Construction Demand

Following the 2022 FIFA World Cup, residential values in Doha declined 10% and prime rents slid 20%, prompting banks to restructure project-finance exposures. State-backed lenders now evaluate phased funding to mitigate unsold inventory risks in Lusail and West Bay. The Real Estate Regulatory Authority’s reforms, including escrow-account requirements and stricter pre-sale thresholds, aim to stabilize investor sentiment but lengthen approval timelines. Developers pivot toward adaptive reuse and branded residences to reposition oversupplied stock, tempering fresh ground-breaks in the Qatar construction market over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Commercial Leadership Drives Infrastructure Acceleration

Commercial construction commanded a 34.89% share of the Qatar construction market in 2025, underscored by landmark office towers and mixed-use hubs like Lusail Financial District. Energy-linked infrastructure, however, is the fastest-growing sector at 4.87% CAGR through 2031, buoyed by the North Field LNG build-out. Leading developers Qatari Diar and United Development Company anchor pipeline visibility, while international EPC players collaborate on mega-retail and hospitality programs. The sector’s resilience is aided by robust sovereign wealth inflows and the government’s push to brand Doha as a regional finance center.

Demand for industrial and logistics space continues to surge alongside the New Hamad Port’s cargo uptick. Data-center and fintech campuses entering design stages indicate future diversification within the commercial slice of the Qatar construction market. Conversely, hospitality projects are shifting focus from stadium-adjacent supply toward all-inclusive desert resorts and medical-tourism facilities, maintaining momentum as post-event traffic normalizes.

By Construction Type: Renovation Gains Momentum as New Construction Matures

New construction dominated with a 74.25% stake in 2025, yet renovation is accelerating at 6.08% CAGR, reflecting systematic upgrades of early-2000s stock and post-World-Cup assets. Major stadiums are converting into multi-purpose venues, demanding specialized façade retrofits and MEP reconfigurations. Commercial towers erected before 2010 now integrate smart building-management systems, improving energy metrics to align with the Global Sustainability Assessment System.

Renovation contractors leverage digital twins to minimize downtime, using laser scans to pre-fabricate replacement components. Facilities such as Hamad International Airport’s Terminal 1 are phasing in process-improvement works during off-peak windows, evidencing the complexity of brownfield execution. The burgeoning retrofit niche diversifies revenue streams and lifts overall quality benchmarks across the Qatar construction market.

By Construction Method: Modern Methods Gain Traction Despite Conventional Dominance

Conventional on-site work retained 85.98% of activity in 2025, yet modular volumetric units now populate worker camps, hotel wings, and data-hall shells at a 6.29% CAGR. Builders like HBK Contracting partner with European fabricators to localize module assembly, cutting on-site labor by 30%. Government pilot schools delivered within nine months validate the speed advantage of off-site integration.

Despite higher up-front design costs and supply-chain adjustments, modular adoption is climbing as lenders reward reduced schedule risk with favorable debt terms. Regulatory guidelines for transport and lifting logistics are in drafting, smoothing pathways for wider application. This shift will incrementally shrink project delivery cycles and boost productivity for the Qatar construction market.

By Investment Source: Private-Sector Participation Accelerates Through PPP Framework

Public expenditure accounted for 77.95% of total outlays in 2025, anchored by sovereign-funded expressways and energy infrastructure. Private investment is expanding at 6.02% CAGR as PPP concessions in schools, car parks, and wastewater treatment plants progress toward close. Qatar Investment Authority’s USD 300 billion portfolio crowds in foreign co-investors seeking long-dated, inflation-linked returns.

International funds targeting logistics and data-center assets are partnering with local developers to navigate land-lease structures and labor compliance. Structured-finance deals now embed green-loan tranches, incentivizing LEED-Gold and GSAS 4-Star certifications. As regulatory clarity improves, the Qatar construction market expects a richer mix of funding channels and risk-sharing models.

Geography Analysis

Doha remains the undisputed epicenter of the Qatar construction market, holding 63.05% share in 2025 and benefiting from steady tenant demand across finance, energy, and technology verticals. Projects such as Lusail Towers and Doha Metro Phase 2 continue to draw top-tier EPC consortia, while older districts like Al Sadd pivot toward mixed-use regeneration that respects heritage aesthetics yet meets smart-city specifications. High urban density coupled with a 422% increase in runoff spurs mandates for permeable paving, green roofs, and upgraded drainage systems, placing environmental engineering at the project forefront.

Moving north, Lusail exemplifies Qatar’s flagship smart-city vision. Carbon-neutral transportation networks, district cooling, and LEED-Gold public buildings set new performance benchmarks that ripple into surrounding municipalities. Strong pre-lease uptake for the city’s office clusters signals confidence among multinational tenants seeking regional headquarters. Construction momentum here underpins positive sentiment for the broader Qatar construction market through the decade.

Secondary nodes such as Al Wakrah and Mesaieed capitalize on spillover growth as Doha’s land premiums rise. The USD 7.4 billion New Port Project anchors logistics and light-manufacturing zones, attracting modular warehouse developers and value-added distributors. Planned rail spurs linking industrial estates to the main metro trunk will elevate multimodal connectivity, further scattering construction opportunities across the peninsula.

Competitive Landscape

Qatar's construction market is moderately fragmented, with Saipem, McDermott, Technip Energies, Larsen & Toubro, and Qatari Diar Construction collectively holding a 48% share of cumulative project billings in 2024. International giants leverage digital project-management suites and advanced fabrication yards to secure mega-scale LNG and marine-infrastructure contracts, while partnering with local Grade-A firms to satisfy Qatarization quotas.

Strategic alliances dominate bidding for publicly funded transport and civic projects. For example, a joint venture between PORR and HBK delivered sections of the Doha Metro’s Green Line using semi-autonomous tunnel-boring machines, trimming schedule float by 12%. Contractors increasingly embed sustainability key-performance indicators in bid submissions as agencies weigh carbon impacts alongside cost[3]Journal of Petroleum Technology, “North Field Pipeline Contract,” jpt.spe.org.

White-space opportunities are emerging in operation-and-maintenance concessions, as facilities such as expressways and district-cooling plants shift toward long-term performance-based contracts. Niche specialists in predictive analytics, façade-cleaning robotics, and energy-retrofit services are gaining ground, enhancing the competitive fabric of the Qatar construction market.

Qatar Construction Industry Leaders

Al Ali Engineering Co. W.L.L

Al Balagh Trading and Contracting

Arabian Construction Company

Al Darwish Engineering Co.

AL Huda Engineering Works

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Larsen & Toubro secured a USD 1.8 billion EPC contract for offshore compression complexes under the North Field Production Sustainability program.

- January 2025: QNB Group partnered with Qatari Diar on strategic land purchases in Lusail City, expanding a sustainable-finance portfolio exceeding USD 9 billion.

- January 2025: Zachry Group filed for Chapter 11 bankruptcy amid overruns at the Golden Pass LNG terminal co-owned by QatarEnergy and ExxonMobil, with McDermott and Chiyoda assuming project completion.

- October 2024: McDermott won an EPCI package for 250 km of pipelines connecting new offshore platforms to onshore LNG trains under North Field South.

Qatar Construction Market Report Scope

The construction market includes a wide range of activities that cover upcoming, ongoing, and growing construction projects in different sectors, which include but are not limited to geotechnical (underground structures) and superstructures in residential, commercial, and industrial structures, as well as infrastructure construction (like roads, railways, and airports) and power generation and transmission related infrastructure.

The report offers a complete background analysis of the construction sector, including an assessment and contribution of the sector to the economy, a market overview, market size estimation for key segments, emerging trends in the market segments, market dynamics, etc. The report also covers the impact of the COVID-19 pandemic on the market.

The Qatar construction market is segmented by type (commercial construction, residential construction, industrial construction, infrastructure (transportation) construction, and energy and utilities construction).

The report offers market size and forecasts for the Qatar construction market in terms of value (USD) for all the above segments.

By Sector

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By Geography

| Doha |

| Lusail |

| Al Wakrah |

| Rest of Qatar |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | Doha | |

| Lusail | ||

| Al Wakrah | ||

| Rest of Qatar | ||

Key Questions Answered in the Report

What is the current value of the Qatar construction market?

The sector is worth USD 54.51 billion in 2026 and is projected to hit USD 66.74 billion by 2031.

How fast is construction expected to grow in Qatar?

Industry revenue is forecast to increase at a 4.14% CAGR through 2031, led by infrastructure and LNG mega-projects.

Which sector holds the largest share of activity?

Commercial projects dominate with 34.89% of 2025 spending, while infrastructure is the fastest-growing segment.

Where is most construction taking place?

Doha commands 63.05% of national spending, but Al Wakrah and Lusail are catching up rapidly.

How big is the role of private investment?

Public funds still drive 77.95% of 2025 work, yet private participation is rising at 6.02% CAGR under new PPP laws.

What hampers growth in the near term?

Volatile material prices, a post-World-Cup real estate correction, and skilled-labor shortages act as key restraints.

Page last updated on: