Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 8.62 Billion |

| Market Size (2026) | USD 9.17 Billion |

| Market Size (2031) | USD 11.91 Billion |

| Growth Rate (2026 - 2031) | 5.37% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peru Road Freight Transport Market Analysis by Mordor Intelligence

The Peru Road Freight Transport Market size was valued at USD 8.62 billion in 2025 and is estimated to grow from USD 9.17 billion in 2026 to reach USD 11.91 billion by 2031, at a CAGR of 5.37% during the forecast period (2026-2031).

Investment in cold-chain assets for premium agro-exports, 5G-enabled telematics, and carbon-credit financing for electric trucks jointly lift service quality ceilings and formalize capacity across the Peru road freight transport market. At the same time, recurrent civil-unrest blockades, green-emissions toll surcharges on pre-Euro IV rigs, rising cargo theft along Amazon corridors, and tight domestic credit continue to test operator resilience. The competitive field, therefore, pivots on technology adoption, regulatory compliance, and balance-sheet breadth rather than on low-price bidding alone, encouraging mid-sized carriers to seek alliances or digital-platform partnerships that lift fleet utilization and working-capital velocity.

Key Report Takeaways

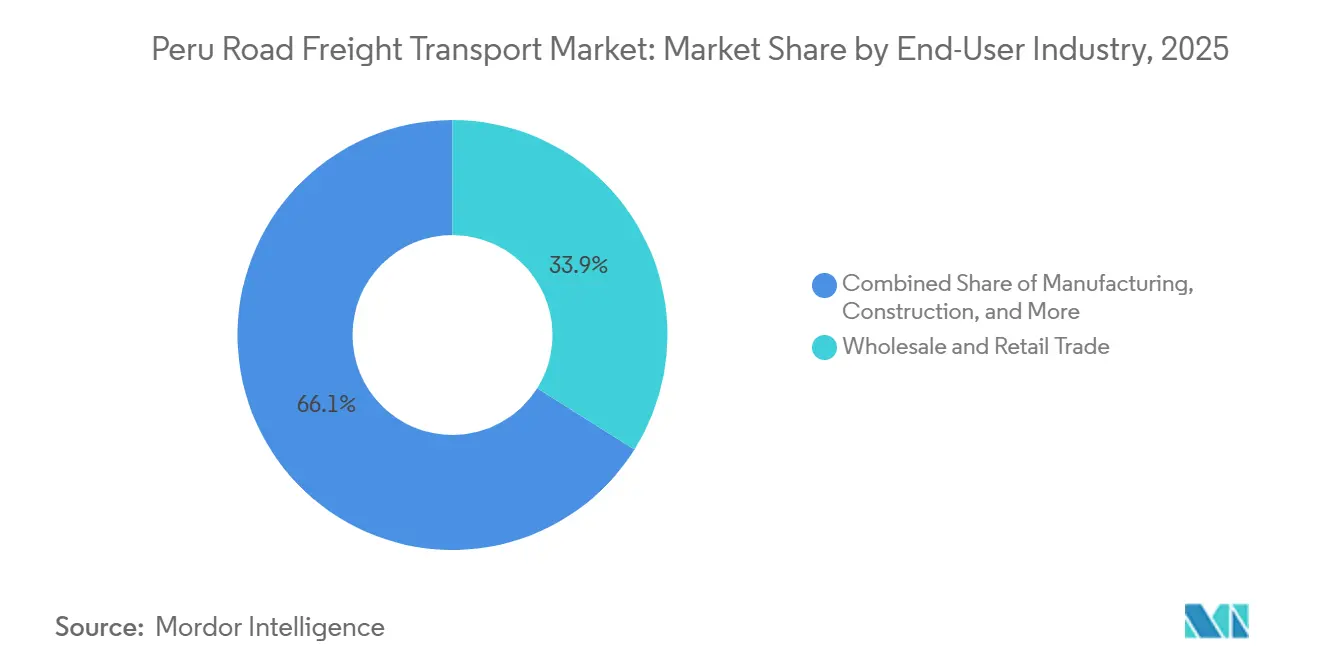

- By end-user industry, wholesale and retail trade led with 33.94% of Peru road freight transport market share in 2025 and is forecast to expand at a 6.17% CAGR to 2031.

- By destination, domestic services commanded 62.07% share of the Peru road freight transport market size in 2025, while international freight is projected to advance at a 6.21% CAGR through 2031.

- By truckload specification, full-truck-load operations captured 78.71% share of Peru road freight transport market, whereas less-than-truckload is the fastest-growing sub-segment at 6.01% CAGR to 2031.

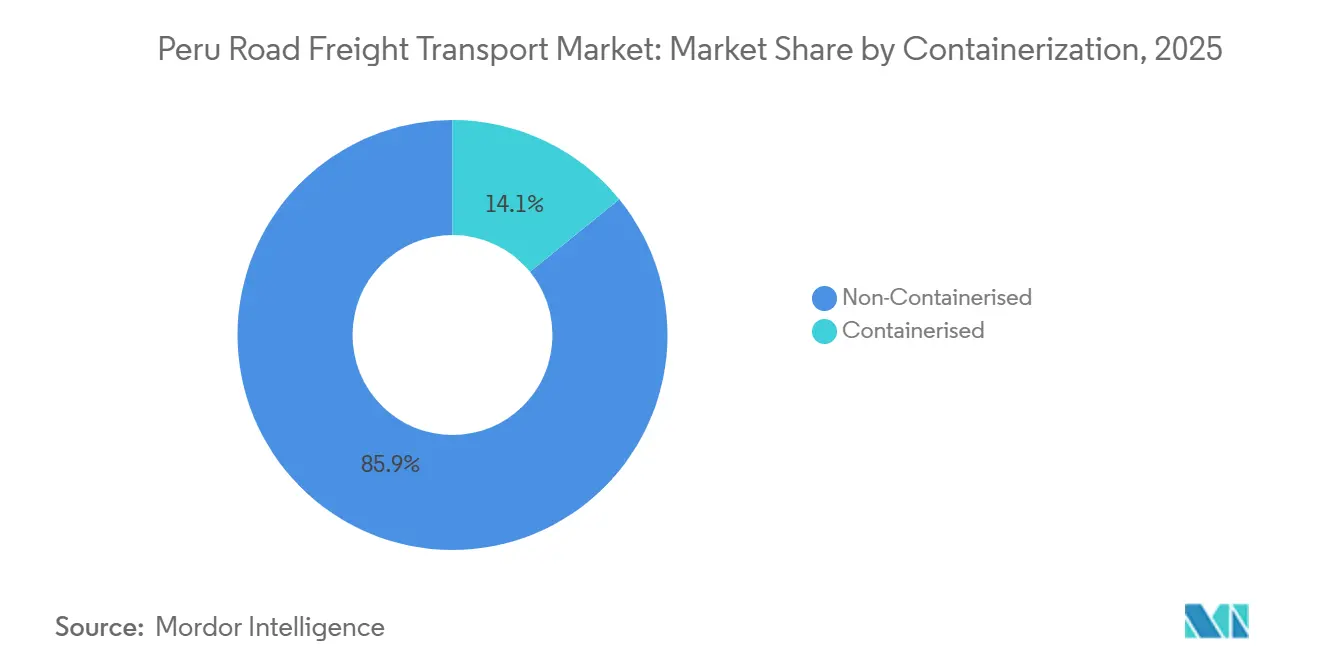

- By containerization, non-containerized freight held 85.88% share of Peru road freight transport market, and containerized movements are forecast to grow at a 5.47% CAGR over 2026-2031.

- By distance band, long-haul lanes represented 73.99% of total value in 2025, while short-haul routes will post the higher 5.52% CAGR during the outlook period.

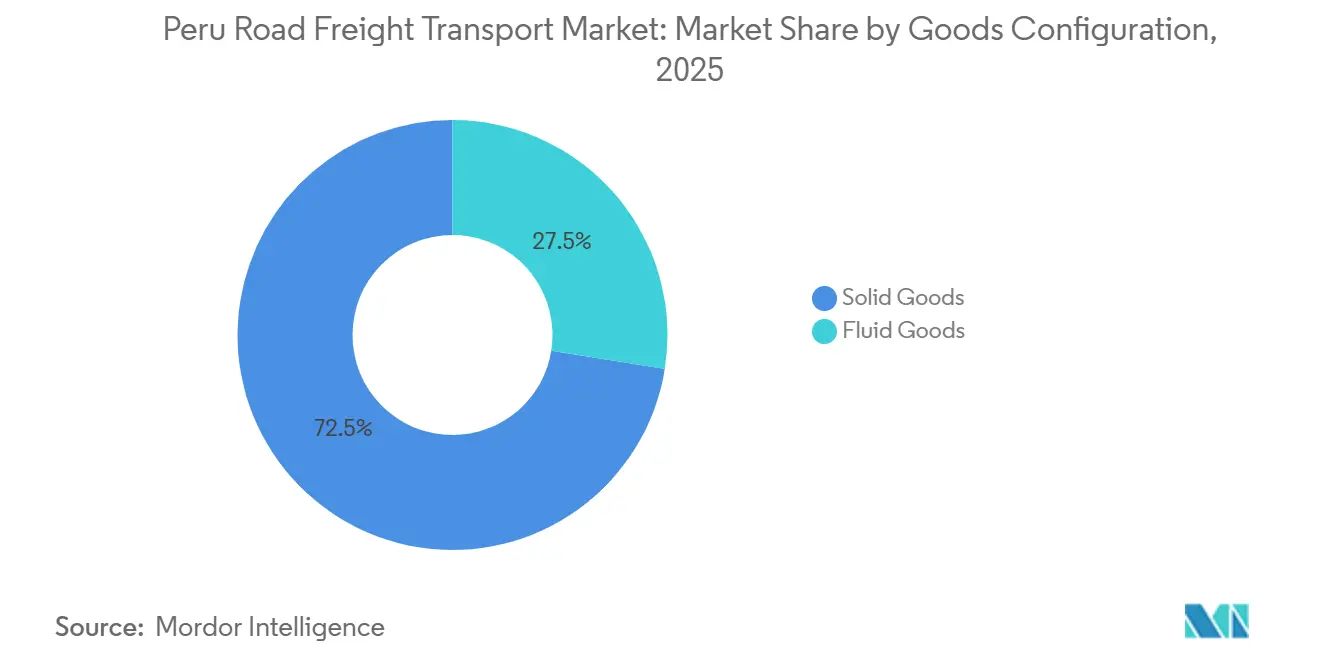

- By goods configuration, solid cargo retained a 72.49% of Peru road freight transport market, fluid goods are set to increase the fastest at a 5.78% CAGR through 2031.

- By temperature control, non-temperature controlled moves accounted for 94.63% of 2025 value and temperature-controlled transport will accelerate at a 5.90% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Peru Road Freight Transport Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nearshoring-led manufacturing influx | +0.9% | Lima-Callao industrial belt | Medium term (2-4 years) |

| SUNAT electronic-invoicing mandate | +0.6% | National, urban-centric | Short term (≤ 2 years) |

| Cold-chain expansion for high-value exports | +0.7% | Coastal Ica-Lima-Piura | Medium term (2-4 years) |

| 5G logistics corridors and platooning pilots | +0.3% | Lima, Arequipa-Cusco | Long term (≥ 4 years) |

| Carbon-credit financing for e-trucks | +0.4% | Lima metro, port approaches | Medium term (2-4 years) |

| Longitudinal de la Sierra highway concession | +0.5% | Central Andean mining belt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nearshoring-Led Manufacturing Influx Boosting Domestic Freight Volumes

Foreign direct investment in Peruvian manufacturing rose 23% year-over-year in 2025, concentrated in Lima-Callao industrial parks, where proximity to ports and United States trade preferences shorten supply chains for automotive parts and consumer-electronics assemblers. Recurring inbound raw-material and outbound finished-goods flows lower demand volatility for carriers active in the Peru road freight transport market. Shipments feature higher average values, encouraging shippers to specify real-time tracking, cargo-integrity sensors, and contractual service-level agreements. Larger operators win multi-year deals that stabilize fleet-deployment plans and improve bargaining power with equipment suppliers. Consequently, domestic legs for near-shore production now underpin backhaul loads previously subject to empty-return risk, nudging overall asset-utilization ratios upward[1]Inter-American Development Bank, “Carbon Credit Financing for Transport,” iadb.org.

SUNAT Electronic-Invoicing Mandate Lowering Compliance Friction

Universal e-invoicing since January 2025 has shaved typical payment cycles from 45-60 days to 15-30 days, freeing working capital and trimming reliance on factoring lines costing 18-24% annually. Automated reconciliation between delivery proof and tax documentation cuts administrative overheads, leveling the field for smaller fleets that lacked dedicated back-office staff. Formalization deepens as shippers insist on e-invoice capability, pressuring informal haulers to upgrade or exit. The Peru road freight transport market, therefore, shifts toward transparent pricing and documented service performance, a prerequisite for multinational procurement audits. Over the medium term, consistent cash-flow visibility eases collateral requirements for bank loans, gently widening the credit funnel for compliant SME carriers.

Cold-Chain Expansion for High-Value Agro-Exports Fueling Reefer Demand

Blueberries and avocados generated USD 3 billion in export receipts during 2025, all of which require temperature ranges between 0 °C and 8 °C throughout inland transit. Freight rates for refrigerated trucks stand 40-60% above dry-van equivalents, justifying the extra capital tied up in reefers and telematics-enabled temperature loggers. Specialized operators in the Peru road freight transport market differentiate via multi-temperature trailers that mix produce lots without risking load rejection. Customs brokers increasingly demand IoT-based integrity certificates before issuing phytosanitary clearance, embedding digital cold-chain datapoints into export documentation workflows. Reefer fleet growth is thus tethered to horticulture acreage expansion and to stringent buyer protocols in North America and Asia[2]UNCTAD, “Foreign Direct Investment Trends Latin America 2025,” unctad.org.

5G Logistics Corridors Enabling Real-Time Telematics & Platooning

Commercial 5G along the Lima-Arequipa spine unlocks sub-second latency, supporting predictive-maintenance analytics that have trimmed unscheduled downtime by roughly 30% for early adopters. Truck-platooning pilots deliver 8-12% fuel savings by maintaining tight inter-vehicle gaps under coordinated braking logic. These efficiency gains arrive as diesel prices remain volatile, cushioning operating-cost exposure for fleets with connected rigs. However, the capex burden and cybersecurity requirements deter small players, accelerating M&A prospects in the Peru road freight transport market. Regulatory sandboxes for autonomous convoys are set to widen after 2028, potentially recasting driver-rostering norms and insurance frameworks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Civil-unrest blockades on Panamericana Sur | -0.7% | Arequipa-Cusco-Puno | Short term (≤ 2 years) |

| Green-Emissions toll surcharges on Euro III rigs | -0.5% | National toll network | Medium term (2-4 years) |

| Rising cargo theft in Amazon corridor | -0.4% | Ucayali-San Martín | Medium term (2-4 years) |

| Tight credit cycle for SME fleet renewal | -0.6% | Nationwide, acute among independents | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Civil-Unrest Blockades Along Panamericana Sur

Forty-seven days of protest-induced road closures in 2024 interrupted mineral supply chains linking southern mines to Lima smelters and ports, inflating safety-stock needs by 15-20%. Insurers loaded corridor-specific surcharges of 200-300 bps on cargo over USD 100,000, a non-trivial uptick in total landed cost. Larger fleets in the Peru road freight transport market deploy real-time route-monitoring dashboards and remote liaisons with community leaders to secure advance warnings, yet spontaneous flashpoints remain unmitigable. The unpredictability compels shippers to commission dual-routing clauses and pay premiums for carriers maintaining rail or coastal-shipping fallback, ultimately embedding systemic slack that drags on effective capacity.

2025 Green-Emissions Law Introducing Euro-III Toll Penalties

From July 2026, trucks below Euro IV standards will need to pay 50-100% higher tolls, amounting to USD 800-1,200 annually per vehicle on the Lima-Callao expressway. About 40% of Peru’s active fleet falls within the penalty slab, forcing small operators either to absorb the margin hit or to pass costs along, risking customer churn. Credit constraints slow replacement cycles, widening cost gaps between modern fleets and legacy rigs within the Peru road freight transport market. Fleet aggregators eye distressed asset purchases to accelerate consolidation, betting on residual-value arbitrage as outdated equipment is scrapped[3]Congreso de la República, “Green-Emissions Law 2025,” congreso.gob.pe.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Retail Consolidation Reshapes Demand

Wholesale and retail trade generated 33.94% of the Peru road freight transport market size in 2025. Over 2026-2031, the segment is forecast to grow at 6.17% CAGR, adding capacity for last-mile drops and reverse-logistics loops that capture returns management. Because retailers tender predictable soft-goods volumes, carriers can justify installing route-optimization software and micro-fulfillment hubs that lower empty-mile incidence.

Manufacturing ranks second but posts a slower trajectory as installed near-shoring capacity stabilizes after the initial investment burst. Nevertheless, automotive and consumer-electronics assemblers issue just-in-time schedules that demand 98-99% on-time performance, incentivizing carriers in the Peru road freight transport market to deploy dual-driver shifts and cross-dock nodes. Oil, gas, and mining continue to rely on heavy-haul specialists, whereas agriculture and forestry underpin temperature-controlled growth through premium berry and avocado shipments. Construction freight remains cyclical, rising in tandem with public-works outlays such as port hinterland roads and toll-way resurfacing programs.

By Destination: Export Corridors Drive International Growth

Domestic lanes accounted for 62.07% of the Peru road freight transport market in 2025, yet international flows to Chile, Ecuador, and Asian maritime routes are projected to eclipse domestic growth at a 6.21% CAGR to 2031. The Chancay mega-port gives exporters a direct Pacific gateway to Shanghai, trimming ocean transit by 10-12 days and lifting demand for drayage and customs-bonded trucking. Carriers equipped with customs brokerage, ATA Carnet processing, and bilingual driver documentation gain a competitive edge.

Rising middle-class demand prompts network redesigns that favor hub-and-spoke models capable of same-day replenishment, cementing the Peru road freight transport market as a critical artery for perishable and fast-moving consumer goods. Shippers increasingly split inventory across regional DCs to hedge blockade risk, boosting inter-regional haul lengths even within domestic borders.

By Truckload Specification: Shipment Fragmentation Accelerates

Full-truck-load retained 78.71% of the Peru road freight transport market share during 2025, thanks to bulk mineral and agro-commodity moves. Yet, less-than-truckload is expanding at 6.01% CAGR through 2031, fueled by e-commerce parcelization and retailers' push for lower inventory carry. LTL network economics depend on terminal density; therefore, the top-five carriers are doubling dock doors in Lima, Arequipa, and Trujillo.

Advanced consolidation algorithms in digital freight marketplaces reduce deadhead miles by 18-20% compared with manual dispatch, bolstering LTL margin resilience. The Peru road freight transport market witnesses carriers bundling technology subscriptions with line-haul contracts, effectively monetizing data analytics as a service. FTL will remain indispensable for single-consignee commodity runs, but its share is expected to erode modestly as supply chains tilt toward agility over scale.

By Containerization: Intermodal Standards Gain Traction

By containerization, non-containerized freight held 85.88% of Peru road freight transport market, and containerized movements are forecast to grow at a 5.47% CAGR over 2026-2031. Visibility tools like blockchain-anchored seals provide immutable handover records, a must-have for food-safety audits in destination markets.

Non-containerized freight still enjoys economies of scale in mining and fishmeal exports, and its operational simplicity appeals to carriers with limited chassis pools. Over the outlook horizon, container availability during peak horticulture season will dictate premium spot rates, while digital container-exchange markets aim to curb imbalance surcharges within the Peru road freight transport market.

By Distance: Short-Haul Urbanization

Long-haul trips captured 73.99% of Peru's road freight transport market share, yet short-haul segments are forecast to log a 5.52% CAGR as urban consumer spending balloons. Last-mile circuit density improves when retailers and e-tailers invest in spoke satellites around Lima’s periphery, allowing 30-minute delivery windows that command premium tariffs.

Long-haul margins hinge on obtaining backhauls out of mining regions, a task complicated by directional traffic imbalances. Carriers experiment with milk-run models that aggregate multiple partials for return trips, mitigating empty-load costs within the Peru road freight transport market. Government bypass projects around congested city centers cut idling times, indirectly stretching driver hours-of-service envelopes and boosting effective kilometer yields.

By Goods Configuration: Specialized Liquid Transport Expands

Solid commodities still dominate at 72.49% share, but fluid goods, including fuels, chemicals, and food-grade oils, are advancing at 5.78% CAGR. Hazardous-material haulers invest in double-shell tankers and inert-gas blanketing systems to meet stricter safety codes, raising capital barriers for entrants.

Meanwhile, LNG and CNG distribution networks radiating from the Camisea field create new lanes for cryogenic tank trucks. Food-grade tanker demand rises on the back of edible oil refining along the northern coast. These dynamics widen service differentiation inside the Peru road freight transport market, as only compliant carriers can tap higher-yield liquid cargoes.

By Temperature Control: Cold Chain Premiumization

Non-temperature-controlled loads accounted for 94.63% of Peru's road freight transport market share, but the temperature-controlled sub-segment is racing ahead at a 5.90% CAGR. Multi-zone reefers capable of holding 0 °C produce and 15 °C pharmaceuticals simultaneously command even higher rates.

Fleet operators in the Peru road freight transport market pair IoT thermologgers with blockchain certificates that satisfy foreign buyers’ proof-of-integrity requests. Urban cold-stores near Jorge Chávez International Airport have doubled capacity since 2024, cutting dwell times and spoilage incidence. Industry observers expect the temperature-controlled share to surpass 8% by 2031 as domestic chilled-food consumption climbs.

Geography Analysis

Lima-Callao alone generated about 45% of the Peru road freight transport market value in 2025, courtesy of its role as both consumption nexus and maritime gateway. Coastal corridors from Ica to Piura leverage flat topography and irrigated export farming to feed northbound berry and asparagus consignments into Callao and Pisco ports. Highlands such as Cajamarca and Arequipa remain mineral powerhouses, dispatching concentrate convoys but suffering empty backhauls due to sparse local demand, which inflates directional rate spreads.

Amazon-frontier cities like Pucallpa depend on road-to-river trans-loading, adding modal complexity and raising insurance costs tied to cargo-theft risk. Seasonal downpours and El Nino events wash out unpaved segments, prompting emergency freight surcharges that ripple through consumer-goods pricing in jungle provinces. Northern regions' coffee and cacao booms enjoy new paved spurs funded under the National Infrastructure Plan, shortening farm-to-port runs by up to four hours.

Infrastructure disparity shapes carrier strategy; nationwide players focus on trunk roads with 24/7 weigh-station coverage, while regional specialists exploit local knowledge to navigate secondary trails and bilingual paperwork. Climate-resilient roadway upgrades, especially along landslide-prone stretches, will be critical to sustaining CAGR projections for the Peru road freight transport market beyond 2030. Finally, city-bypass investments around Trujillo and Chiclayo cut urban congestion, unlocking same-day regional delivery promises that retailers now feature in advertising.

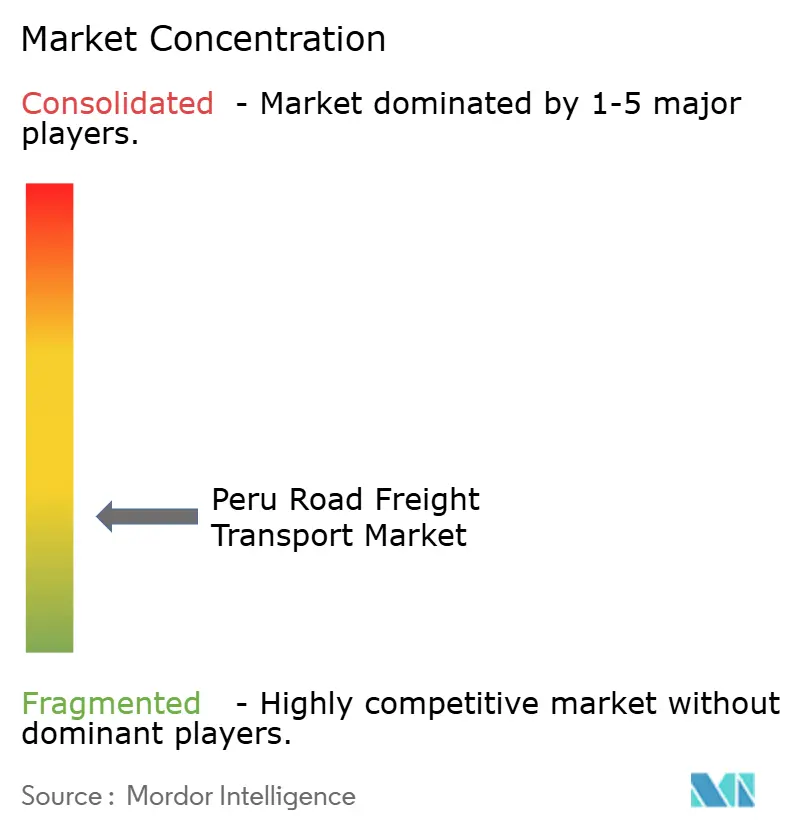

Competitive Landscape

The Peru road freight transport market remains moderately fragmented; the top five operators together hold roughly 35-40% revenue, leaving space for niche specialists. DSV’s EUR 14.3 billion (USD 16.47 billion) buyout of DB Schenker instantly entrenched the acquirer in chemical and retail verticals and signaled growing appetite among globals for Latin American density. Kuehne+Nagel’s USD 12 million cold-chain campus in Lima and DHL’s USD 18 million multi-client DC show that multinationals are shifting from asset-light forwarding to asset-heavy distribution, a pivot driven by shippers’ demand for integrated visibility across modes.

Regional champions such as SAVAR Corporacion and Peru Logistic SAC counter by embedding AI route-optimization and pharma GDP certifications, respectively, to retain key accounts. Digital freight marketplaces, pioneered by SAVAR’s 2024 launch, compress brokerage spreads and uplift asset utilization, but face trust hurdles among smaller fleets uncomfortable with smartphone-based work allocation. Security-centric providers operating armed-escort and fortified-yard services extract premiums from electronics consignors navigating Amazon corridors, carving out defensible positions despite limited fleet size.

Strategic partnerships proliferate: CEVA’s pact with a copper consortium bundles project cargo, heavy-haul, and supply-chain analytics into a one-stop service. JAS Worldwide’s local forwarder acquisition adds hinterland offices that global integrators often overlook[4]JAS Worldwide, “Peru Expansion via Acquisition 2024,” jasworldwide.com . Finally, carbon-neutral offerings from Geodis resonate with exporters seeking Scope 3 abatement. Across all tiers, telematics adoption, driver-safety programs, and predictive maintenance investments differentiate bids and shape contract renewals.

Peru Road Freight Transport Industry Leaders

DHL

DSV

SAVAR Corporación Logística

CMA CGFM

Ransa Comercial

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: DHL Group announced expansion of data center logistics network with 10 new warehouses and over 7 million ft² capacity.

- November 2025: CEVA Logistics signed an agreement with Iveco Group to operate a new distribution center, expanding its regional logistics footprint and strengthening automotive supply chain capabilities in Latin America.

- May 2025: CEVA Logistics expanded its deep-sea vehicle logistics network connecting the Far East with Central and South America, strengthening automotive logistics flows into the region.

- March 2025: DHL Group announced the acquisition of pharma logistics firm Cryopdp to strengthen its life sciences supply chain capabilities.

Peru Road Freight Transport Market Report Scope

By Destination

| Domestic |

| International |

By End-User Industry

| Manufacturing |

| Oil, Gas, Mining & Quarrying |

| Agriculture, Fishing & Forestry |

| Construction |

| Wholesale and Retail Trade |

| Other End-Users |

By Truckload Specification

| Full Truckload (FTL) |

| Less-than-Truckload (LTL) |

By Containerization

| Containerised |

| Non-Containerised |

By Distance

| Long Haul |

| Short Haul |

By Goods Configuration

| Fluid Goods |

| Solid Goods |

By Temperature Control

| Non-Temperatured Controlled |

| Temperatured Controlled |

| By Destination | Domestic |

| International | |

| By End-User Industry | Manufacturing |

| Oil, Gas, Mining & Quarrying | |

| Agriculture, Fishing & Forestry | |

| Construction | |

| Wholesale and Retail Trade | |

| Other End-Users | |

| By Truckload Specification | Full Truckload (FTL) |

| Less-than-Truckload (LTL) | |

| By Containerization | Containerised |

| Non-Containerised | |

| By Distance | Long Haul |

| Short Haul | |

| By Goods Configuration | Fluid Goods |

| Solid Goods | |

| By Temperature Control | Non-Temperatured Controlled |

| Temperatured Controlled |

Key Questions Answered in the Report

What is the current value of the Peru road freight transport market?

The Peru road freight transport market size reached USD 9.17 billion in 2026.

How fast will Peru’s road freight sector grow through 2031?

Aggregate value is forecast to climb to USD 11.91 billion, a 5.37% CAGR over 2026-2031.

Which end-user group generates the most freight revenue?

Wholesale and retail trade leads with 33.94% of 2025 turnover and is also the fastef9s

What lane type is expanding the quickest?

International corridors are projected to grow at 6.21% CAGR, outpacing domestic hauls.

How are sustainability policies affecting fleet investment?

A 2026 toll surcharge on Euro III trucks and carbon-credit financing for electric vehicles are accelerating fleet modernization, especially in Lima.

Which technology trends are most transformative?

Mandatory e-invoicing, 5G telematics, blockchain documentation, and AI route optimization are all reshaping pricing power and service quality.

Page last updated on: