Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

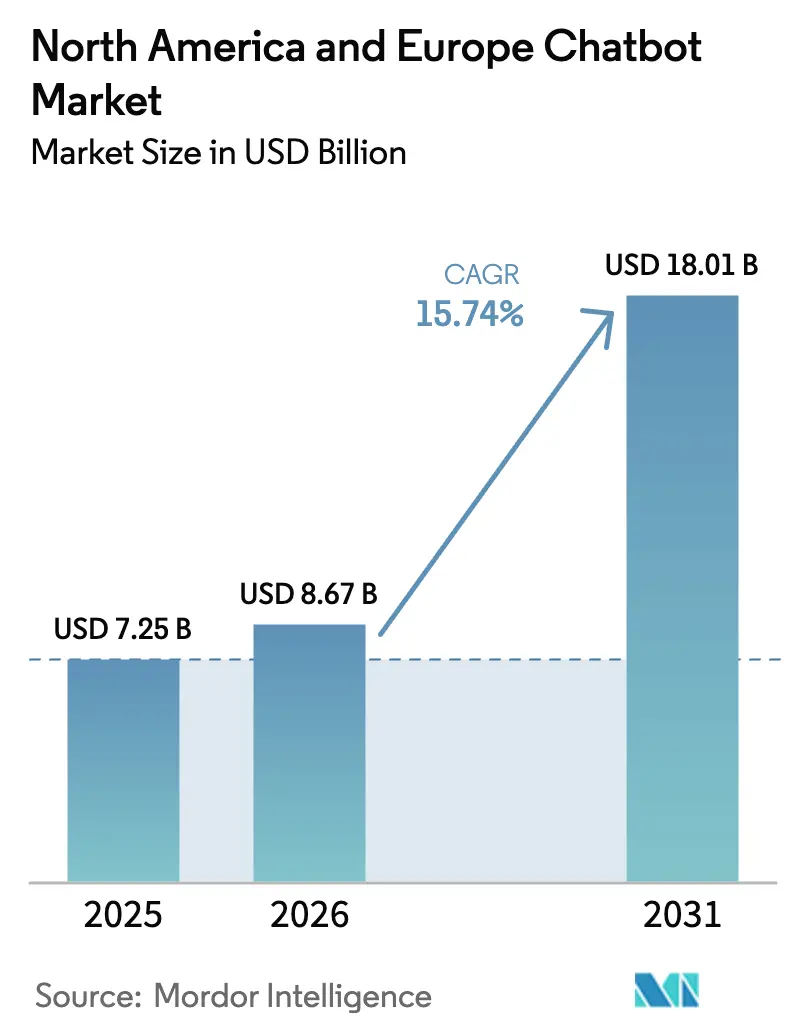

| Base Year Market Size (2025) | USD 7.25 Billion |

| Market Size (2026) | USD 8.67 Billion |

| Market Size (2031) | USD 18.01 Billion |

| Growth Rate (2026 - 2031) | 15.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America And Europe Chatbot Market Analysis by Mordor Intelligence

The North America and Europe Chatbot Market size was valued at USD 7.25 billion in 2025 and is estimated to grow from USD 8.67 billion in 2026 to reach USD 18.01 billion by 2031, at a CAGR of 15.74% during the forecast period (2026-2031). Demand is shifting from rule-based automation toward generative-AI architectures that blend retrieval-augmented generation with multimodal reasoning, enabling richer customer experiences while easing regulatory compliance obligations. The 24/7 digital-support rules under the European Union Digital Services Act, together with contact-center labor shortages documented by the Federal Reserve Bank of St. Louis, are steering budgets toward conversational agents that deflect tier-1 inquiries without human escalation. Cloud deployment remains the default, yet on-premises rollouts are rising in regulated verticals that must comply with data-residency mandates. Hyperscalers bundle chatbots into enterprise software suites, while specialist vendors focus on vertical workflows and hybrid deployment options, sustaining a moderately concentrated competitive landscape. Cost volatility tied to per-token API pricing and fragmented messaging-platform policies temper near-term adoption, but low-code tools and 5G-enabled edge inference expand the addressable user base, especially among small and medium enterprises.

Key Report Takeaways

- By deployment model, cloud accounted for 64.94% of the North America and Europe chatbot market share in 2025, while on-premise implementations are projected to post a 17.22% CAGR through 2031.

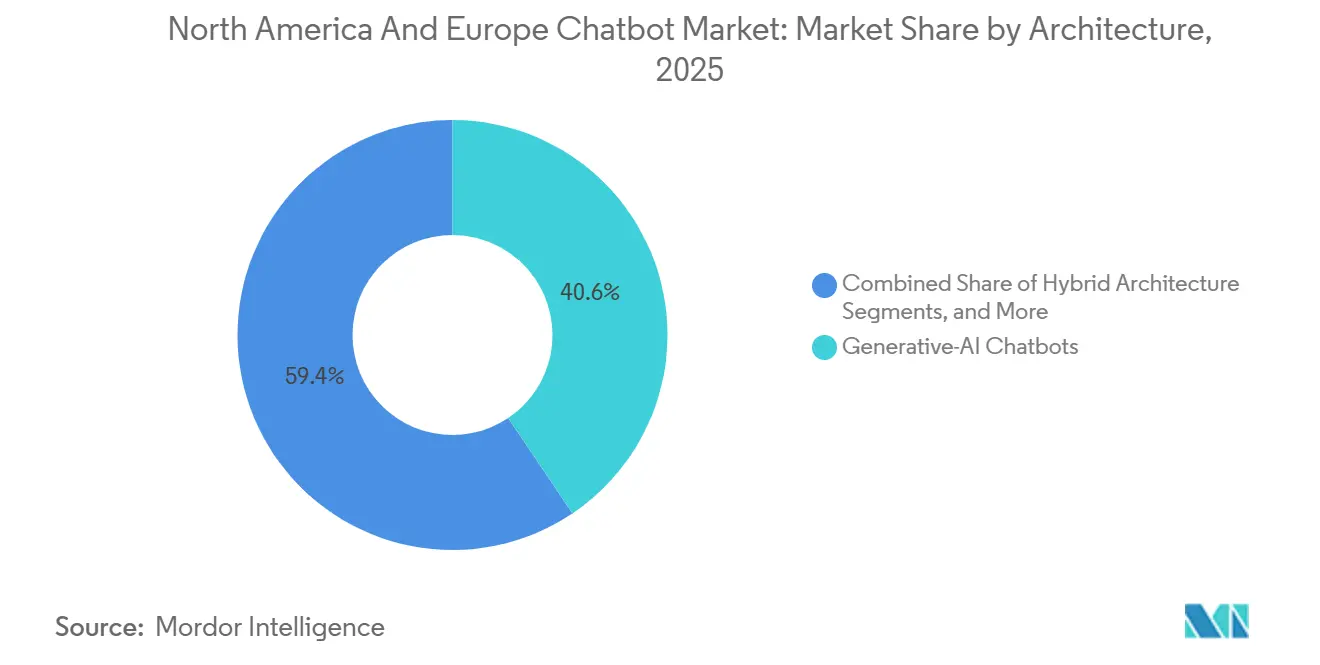

- By architecture, generative-AI chatbots captured 40.58% of the North America and Europe chatbot market size in 2025 and are forecast to grow at 17.83% CAGR to 2031.

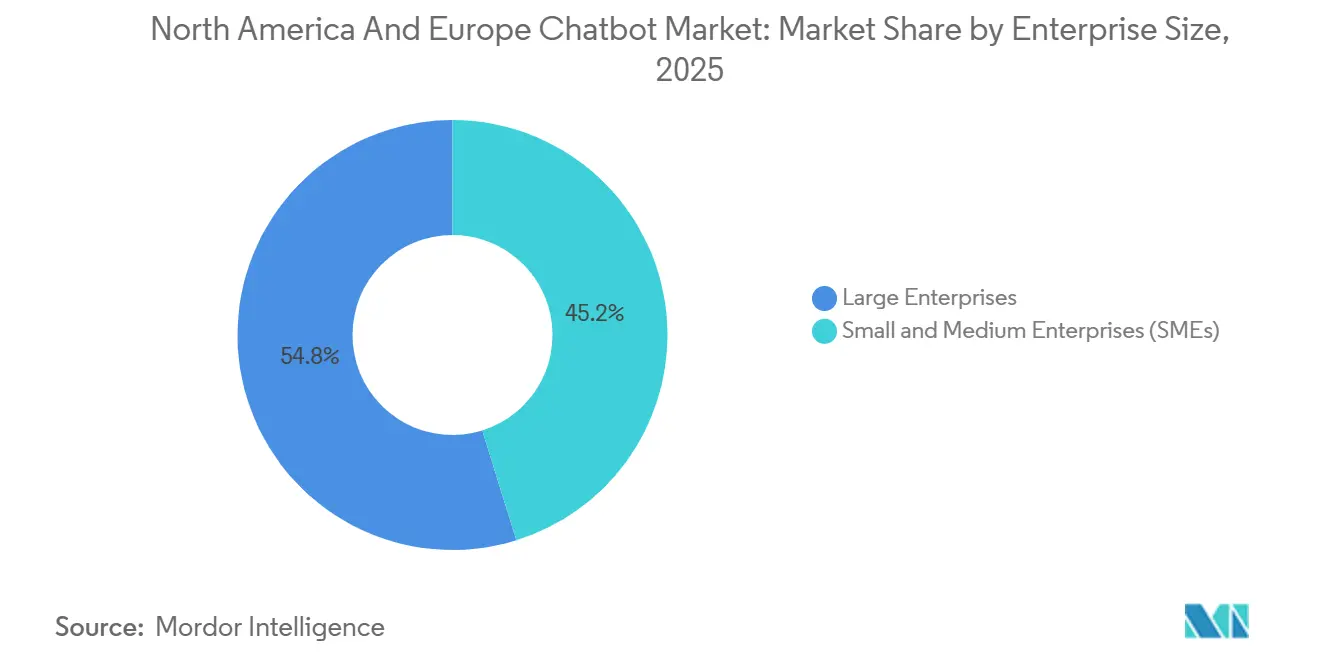

- By enterprise size, large enterprises led with 54.81% market share in 2025; small and medium enterprises are expected to expand at a faster 16.06% CAGR during 2026–2031.

- By end-user vertical, BFSI held 28.63% revenue share in 2025, whereas healthcare is projected to register a 15.93% CAGR through 2031.

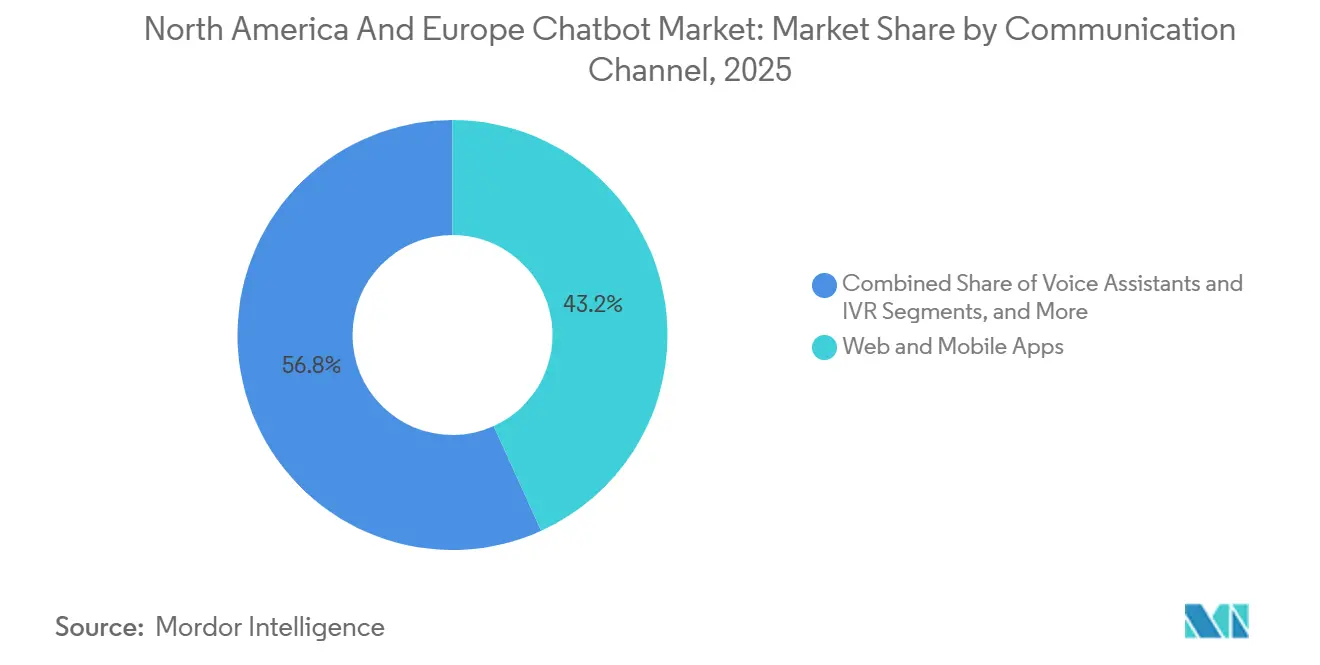

- By communication channel, web and mobile apps represented 43.22% of 2025 revenue, yet voice assistants and IVR integrations are advancing at 16.67% CAGR.

- By geography, the United States generated 46.06% of 2025 revenue; Italy is anticipated to be the fastest-growing country at 16.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America And Europe Chatbot Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CX Personalization via Retrieval-Augmented Generation (RAG) | +3.2% | North America and Europe, with early adoption in United States, Germany, United Kingdom | Medium term (2-4 years) |

| EU Digital Services Act (DSA) 24/7 Digital-Support Mandate | +2.8% | European Union member states, particularly Germany, France, Italy, Netherlands | Short term (≤ 2 years) |

| SaaS Ecosystem Embedding of ChatGPT and Claude APIs | +3.5% | North America and Europe, concentrated in United States, Canada, United Kingdom | Medium term (2-4 years) |

| Contact-Center Labor Shortages Push Automation | +2.6% | United States, Canada, United Kingdom, with spillover to Western Europe | Short term (≤ 2 years) |

| Rise of Low-Code / No-Code Bot Builders | +1.9% | Global, with strong uptake in North America SME segment and Southern Europe | Medium term (2-4 years) |

| 5G and Edge-Cloud Roll-outs Enable Real-Time Multimodal Bots | +1.4% | North America and Western Europe, led by United States, Germany, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

CX Personalization Via Retrieval-Augmented Generation (RAG)

RAG lets chatbots query proprietary knowledge bases in real time, grounding answers in enterprise data instead of generic model weights. NVIDIA showed that adding vector databases cut factual errors by 68% in pilot projects. Microsoft enabled Azure AI Search indices inside Copilot Studio in mid-2025, which United Wholesale Mortgage uses to process 14,000 loan files monthly with limited human review. GDPR pushes European banks toward on-premise RAG stacks, boosting demand for vendors that deliver hybrid-cloud architectures. Accuracy and auditability now outrank sheer fluency, reshaping product roadmaps across the North America and Europe chatbot market.

EU Digital Services Act 24/7 Digital-Support Mandate

The Digital Services Act, fully enforceable for very large online platforms since February 2024, obliges continuous multilingual support, prompting platforms to deploy chatbots across 24 official EU languages.[1]European Commission, “The Digital Services Act Package,” ec.europa.eu Germany’s cybersecurity authority required that automated support systems log every interaction, favoring chatbot suites with compliance dashboards. U.S. firms serving EU users are adopting compliant architectures globally, exporting European standards across the North America and Europe chatbot market.

SaaS Ecosystem Embedding of ChatGPT and Claude APIs

Salesforce, Oracle, and SAP embedded foundation-model APIs into CRM and ERP suites in 2025, turning chatbots into native modules rather than standalone tools. Oracle’s August 2025 pact with Google lets Oracle Cloud customers invoke Gemini models without workload migration, lowering procurement friction. Microsoft prices Copilot Studio at EUR 200 per month for 25,000 conversational credits, bundling chatbot capacity into broader enterprise agreements and reshaping purchasing authority toward line-of-business leaders.

Contact-Center Labor Shortages Push Automation

The U.S. Bureau of Labor Statistics recorded an 18% gap between openings and hires for customer-service roles in 2024. Turnover hit 45% annually, double pre-pandemic norms, motivating automation of tier-1 inquiries. McKinsey found 68% of surveyed contact centers plan to automate within two years, citing staffing deficits over cost savings.[2]McKinsey and Company, “Contact Center Automation Survey,” mckinsey.com Similar shortages in Canada and negotiated compromises with German labor unions further accelerate chatbot rollouts across the North America and Europe chatbot market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Token-Based API-Pricing Volatility | -1.8% | North America and Europe, particularly affecting high-volume retail and telecom deployments | Short term (≤ 2 years) |

| Fragmented Messaging-Platform Policies | -1.3% | Global, with acute impact in Europe where WhatsApp penetration exceeds 80% | Short term (≤ 2 years) |

| Edge-Device Privacy Constraints for On-Device Inference | -0.9% | European Union, driven by GDPR data-minimization requirements | Medium term (2-4 years) |

| Cultural Pushback on Bot-Led Mental-Health and Sensitive Services | -0.7% | North America and Northern Europe, particularly affecting healthcare and social-services sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Token-Based API-Pricing Volatility

OpenAI raised ChatGPT-4 API fees by 15% in March 2025, while Anthropic shifted to tiered pricing, raising budgeting uncertainty for high-volume users. A European telecom disclosed tripled API spending year over year, prompting reviews of on-premise language-model deployment. Microsoft’s credit-based pricing shows burn rates fluctuating by 300% depending on query length, pushing enterprises toward hybrid or open-source options to cap costs.

Fragmented Messaging-Platform Policies

Meta barred general-purpose chatbots on WhatsApp Business API effective January 15, 2026, limiting automation to transactional messages and user-initiated conversations. Brands reliant on WhatsApp in Southern Europe must now pivot to proprietary channels, while Telegram’s inconsistent moderation and Apple’s closed iMessage ecosystem complicate omnichannel strategies. Vendors offering unified interfaces across disparate APIs gain importance in the North America and Europe chatbot market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Enterprise Size: SMEs Gain Speed as Low-Code Tools Democratize Adoption

Large enterprises contributed 54.81% revenue in 2025, underscoring their resources for deep CRM integration and multilingual support across the North America and Europe chatbot market size. Yet SMEs are forecast to grow 16.06% CAGR through 2031, fueled by low-code builders that cut launch times from weeks to hours. Microsoft noted that 40% of the 160,000 Copilot Studio tenants have fewer than 250 staff, signaling that business units, not IT teams, now champion conversational projects.[3]Microsoft, “New Copilot Studio Capabilities Make Building and Managing Copilots Easier Than Ever,” microsoft.com Italy’s PNRR grants and similar subsidies in Spain and Portugal further close the adoption gap, reinforcing SMEs as a priority growth segment within the North America and Europe chatbot market.

SMEs pursue pre-built templates for order tracking and appointment scheduling, while large enterprises retain on-premise and hybrid rollouts to meet GDPR or HIPAA mandates. This bifurcation means platform providers must balance ease of use with enterprise-grade governance, offering scalable pricing tiers that evolve as customers mature.

By End-User Vertical: Healthcare Accelerates While BFSI Levels Off

BFSI retained 28.63% share in 2025, but growth is leveling as most tier-1 use cases mature. Healthcare, in contrast, is predicted to post a 15.93% CAGR, propelled by expanded telehealth reimbursement and FDA guidance that exempts administrative chatbots from pre-market approval. A 2025 JAMA study found no-show rates fell 22% when chatbots handled reminders and intake, fortifying the case for rapid scaling.

Health systems favor on-premise deployments to safeguard sensitive data, whereas retail leverages chatbots for conversational commerce, exemplified by Shopify’s Gemini-powered product discovery that boosted conversions 18%. Segment-specific compliance and ROI drivers will continue to dictate vendor positioning across the North America and Europe chatbot market.

By Architecture: Generative AI Gains Momentum but Hybrid Prevails in Regulated Use Cases

Generative-AI chatbots captured 40.58% of the North America and Europe chatbot market share in 2025 and are projected to expand at a 17.83% CAGR through 2031 as enterprises pursue natural dialog, sentiment detection, and contextual reasoning. These bots excel at cross-selling, multilingual support, and knowledge-base summarization capabilities embedded in Gemini Live on Vertex AI and Microsoft Copilot Studio. Finance and healthcare regulators, however, continue to demand explainable logic, so large institutions combine deterministic natural-language-understanding engines for routine intents with generative models for edge-case queries. This orchestration trims token usage and stabilizes inference costs even after OpenAI raised ChatGPT-4 prices by 15% in March 2025.

European lenders piloting hybrid stacks reported per-conversation spending 22% lower than fully generative approaches while maintaining a 95% containment rate for tier-1 tasks. IBM’s watsonx Assistant achieved a 75% automatic-resolution score in its 133,000-employee IT-support rollout by routing authentication, hardware, and software issues through distinct resolver paths. These outcomes validate configurable architectures across the North America and Europe chatbot market size. Vendors are expected to expose stricter governance controls, including token caps, model-switch thresholds, and audit logs, to help risk teams meet the AI-model validation guidelines anticipated under the EU Artificial Intelligence Act.

By Deployment Model: Cloud Dominates but Sovereign Requirements Sustain On-Premise Growth

Cloud deployments accounted for 64.94% of 2025 revenue and remain the default choice for greenfield projects, thanks to elastic scaling, geographically redundant availability zones, and rapid feature roll-outs across the North America and Europe chatbot market size. Hyperscalers guarantee 99.95% uptime and sub-100-millisecond round-trip latency, enabling retailers and airlines to support flash sales or seasonal demand spikes without capital expenditure. Yet data-sovereignty laws- such as Germany’s 2025 BSI guidance for public-sector workloads- are propelling on-premise and private-cloud growth, particularly in BFSI and healthcare.

Oracle’s August 2025 partnership with Google allows enterprises to run Gemini models inside Oracle Cloud Infrastructure, sidestepping migration fears and aligning with GDPR’s data-localization ethos. European health systems deploy Kubernetes-based sovereign clouds that never leave national borders, while U.S. defense contractors opt for “air-gapped” clusters managed under FedRAMP High controls. This equilibrium means vendors must instrument a single observability layer that unifies logging, version control, and usage analytics across mixed topologies. As a result, both cloud and on-premise segments will grow simultaneously rather than cannibalize each other, expanding the overall North America and Europe chatbot market share.

By Communication Channel: Voice Assistants Replace Touch-Tone IVR

Web and mobile apps captured 43.22% of 2025 revenue, reflecting their ubiquity in e-commerce, fintech, and SaaS workflows that already operate inside graphical user interfaces. However, voice assistants and modern IVR integrations are forecast to grow 16.67% CAGR through 2031 as contact centers retire keypad menus in favor of open-ended natural-language dialog. Deloitte’s 2025 survey showed 58% of North American and European help desks budgeting to phase out touch-tone IVR within two years. Gemini Live’s sub-50-millisecond latency on edge nodes allows mid-conversation clarifications, letting bots handle complex airline re-booking and insurance first-notice-of-loss calls without human intervention.

Meanwhile, Meta’s January 2026 ban on general-purpose chatbots within WhatsApp Business API forces brands to shift self-service flows into proprietary mobile apps, SMS, or RCS, fragmenting user journeys but increasing first-party data control. In-product widgets embedded via SDKs are rising as an alternative, giving SaaS vendors full control over telemetry and UI. Enterprises now layer speech analytics on top of voice bots to feed coaching prompts to human agents in real time, proving that bots complement rather than replace live staff. This channel diversification obliges platform providers to abstract channel-specific APIs into a unified orchestration layer, ensuring consistent persona, context-handoff, and analytics regardless of the end-user touchpoint across the North America and Europe chatbot market.

Geography Analysis

In 2025, the United States produced 46.06% of total revenue within the North America and Europe chatbot market, driven by hyperscaler ecosystems and acute labor shortages that turn automation into a staffing imperative. Canadian SMEs confront similar hiring gaps, translating into brisk uptake of low-code platforms. Mexico benefits from nearshoring, using bilingual chatbots to cover English-Spanish requests that previously demanded human agents.

Across Europe, Italy leads growth at 16.11% CAGR through 2031, underpinned by EUR 6.7 billion in PNRR funds for digital-skills programs. Germany, France, and the United Kingdom advance steadily but grapple with GDPR-driven preferences for on-premise deployments and transparency obligations under the AI Act. Southern and Eastern European markets close the gap thanks to lower labor costs and EU cohesion-policy grants that make chatbot ROI more compelling.

Regulatory heterogeneity shapes deployment choices: U.S. firms lean into cloud-hosted generative models, whereas European enterprises often hybridize to satisfy data-sovereignty mandates. Despite these differences, both regions converge on omnichannel strategies and hybrid architectures, reinforcing the leadership position of the North America and Europe chatbot market worldwide.

Competitive Landscape

The North America and Europe chatbot market is moderately concentrated, with Microsoft, Google, and IBM jointly holding roughly a 35%-40% share through deeply integrated offerings. Microsoft leverages its productivity stack, signing 160,000 Copilot Studio tenants by mid-2025. Google extends Gemini reach via Salesforce and Oracle partnerships, bypassing typical migration barriers. IBM targets regulated sectors with watsonx Agents that automate tier-2 workflows.

Mid-tier vendors consolidate to keep pace: Zendesk bought Ultimate in November 2025, following its earlier shift to outcome-based billing. Ada Support and Cognigy secure niches through vertical templates and GDPR-native deployments. Competitive intensity is set to rise as open-source LLMs lower entry barriers, yet hyperscalers’ bundling power and channel reach sustain their leadership in the North America and Europe chatbot market.

Emerging disruptors such as Anthropic and Forethought capitalize on safety-aligned models and customer-service specialization, respectively. Success will hinge on pairing domain depth with deployment flexibility, as end users demand hybrid topologies that balance performance, cost, and compliance.

North America And Europe Chatbot Industry Leaders

Microsoft Corporation

IBM Corporation

Google LLC (Alphabet Inc.)

Zendesk, Inc.

LivePerson, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Meta enforced a ban on general-purpose chatbots across WhatsApp Business API, confining automation to transactional or user-initiated messages.

- December 2025: Google’s Gemini Live API entered general availability on Vertex AI, delivering real-time multimodal conversations that early pilots cut handle time by 20%.

- November 2025: Zendesk acquired Ultimate, adding generative-AI automation to its customer-service suite.

- October 2025: Zendesk reported GPT-5-powered agents lowered human-transfer rates 20% during enterprise pilots.

- September 2025: Microsoft rolled out five new AI agents for Teams, extending Copilot Studio into collaboration workflows.

North America And Europe Chatbot Market Report Scope

The North America and Europe Chatbot Market Report is Segmented by Enterprise Size (Large Enterprises, Small and Medium Enterprises), End-User Vertical (BFSI, Retail, Healthcare, IT and Telecom, Travel and Hospitality, Other End-User Verticals), Architecture (Rule-based/NLU Chatbots, Generative-AI Chatbots, Hybrid Architectures), Deployment Model (Cloud-based, On-Premise/Private Cloud), Communication Channel (Web and Mobile Apps, Social Media/Messaging Apps, Voice Assistants and IVR, In-Product Widgets/SDKs), and Geography (North America, Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

By End-User Vertical

| BFSI |

| Retail |

| Healthcare |

| IT and Telecom |

| Travel and Hospitality |

| Other End-User Verticals |

By Architecture

| Rule-based/NLU Chatbots |

| Generative-AI Chatbots |

| Hybrid Architectures |

By Deployment Model

| Cloud-based |

| On-Premise/Private Cloud |

By Communication Channel

| Web and Mobile Apps |

| Social Media/Messaging Apps |

| Voice Assistants and IVR |

| In-Product Widgets/SDKs |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe |

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By End-User Vertical | BFSI | |

| Retail | ||

| Healthcare | ||

| IT and Telecom | ||

| Travel and Hospitality | ||

| Other End-User Verticals | ||

| By Architecture | Rule-based/NLU Chatbots | |

| Generative-AI Chatbots | ||

| Hybrid Architectures | ||

| By Deployment Model | Cloud-based | |

| On-Premise/Private Cloud | ||

| By Communication Channel | Web and Mobile Apps | |

| Social Media/Messaging Apps | ||

| Voice Assistants and IVR | ||

| In-Product Widgets/SDKs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How fast will generative-AI chatbots grow in North America and Europe through 2031?

The generative-AI segment is forecast to expand at 17.83% CAGR, the quickest pace among architectural categories.

Which end-user vertical is expected to add the most new spending by 2031?

Healthcare shows the strongest momentum, projected to grow at 15.93% CAGR as telehealth reimbursement and patient-engagement mandates widen.

Why are small and medium enterprises adopting chatbots more quickly now?

Low-code builders and subscription pricing reduce launch complexity, enabling SMEs to deploy within days and driving a 16.06% CAGR for the segment.

How are token-based API-pricing changes affecting enterprise budgets?

A 15% increase in ChatGPT-4 fees and tiered pricing from other providers introduce cost uncertainty, prompting some companies to explore hybrid or self-hosted models.

What role does the EU Digital Services Act play in chatbot deployment?

The DSA requires 24/7 multilingual digital support, making conversational AI the most economical way for large platforms to stay compliant across the bloc.

Page last updated on: