Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

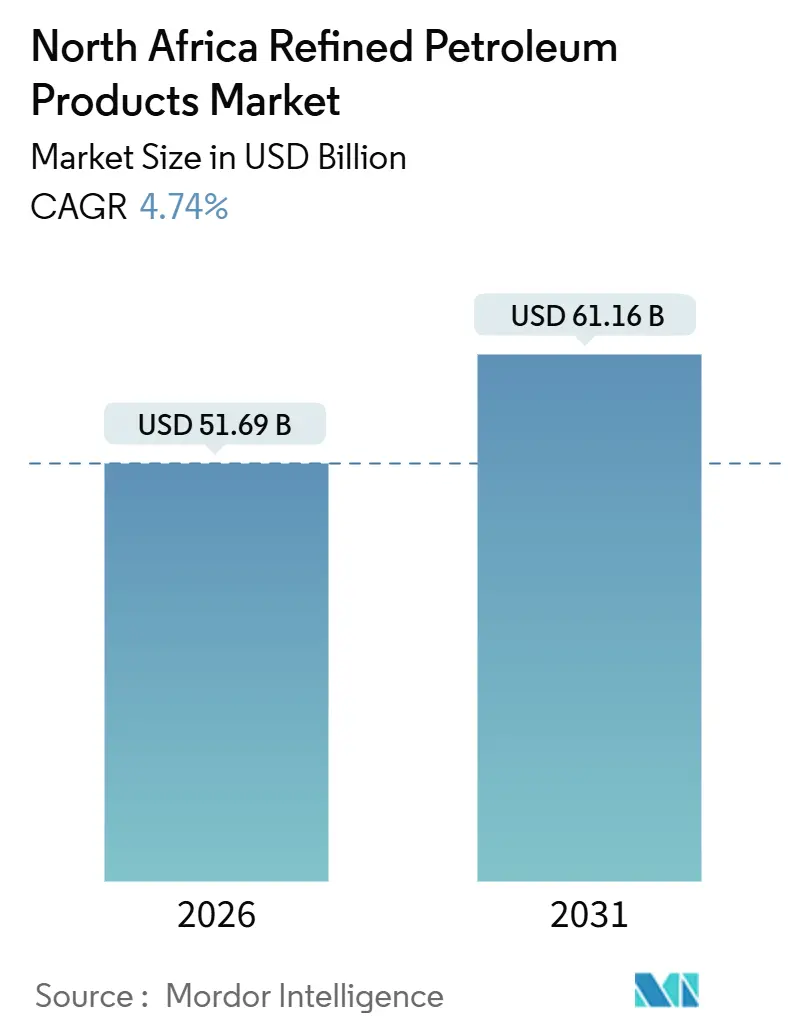

| Market Size (2026) | USD 51.69 Billion |

| Market Size (2031) | USD 61.16 Billion |

| Growth Rate (2026 - 2031) | 4.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North Africa Refined Petroleum Products Market Analysis by Mordor Intelligence

The North Africa Refined Petroleum Products Market size is estimated at USD 51.69 billion in 2026, and is expected to reach USD 61.16 billion by 2031, at a CAGR of 4.74% during the forecast period (2026-2031).

The expansion comes from refinery upgrades, subsidy reform, and new petrochemical offtake that re-route feedstock flows while cushioning upstream volatility. Egypt, Algeria, and Morocco are modernizing existing complexes, adopting Euro 5 standards, and positioning coastal ports as compliant bunkering hubs, moves that sustain demand for low-sulfur middle distillates. Aviation fuel is the fastest-growing product as passenger traffic rebounds across Cairo, Casablanca, and Marrakech airports, while diesel continues to dominate road freight and farm activity. Petrochemical integration is steadily lifting internal naphtha and LPG requirements. At the same time, rising EU and Middle-East exports keep regional pricing competitive, forcing local refiners to raise complexity and improve margin capture. Heightened geopolitical risk in Libya and deeper power-sector fuel switching to gas and renewables temper overall growth, but do not derail the upward trajectory of the North Africa refined petroleum products market.

Key Report Takeaways

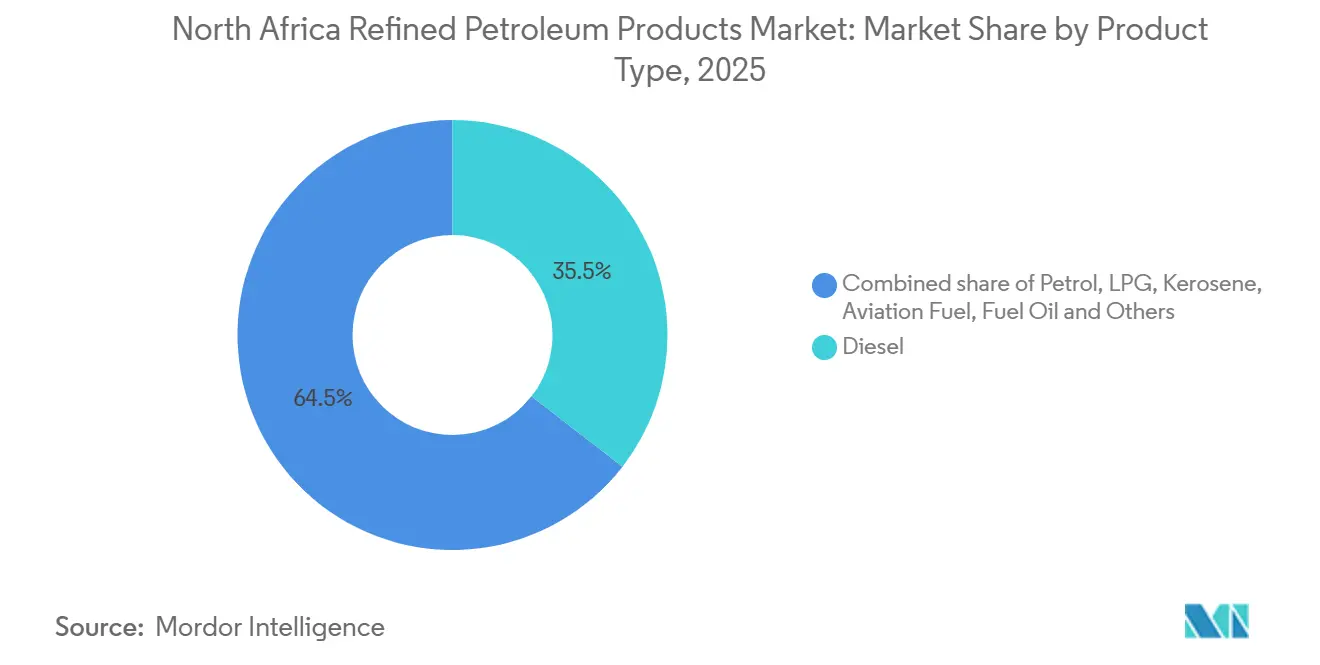

- By product type, diesel held 35.5% of the North Africa refined petroleum products market size in 2025; aviation fuel exhibits the highest projected CAGR at 6.5% to 2031.

- By sulfur content, low-sulfur grades captured 58.1% share of the North Africa refined petroleum products market size in 2025 and are advancing at a 5.3% CAGR to 2031.

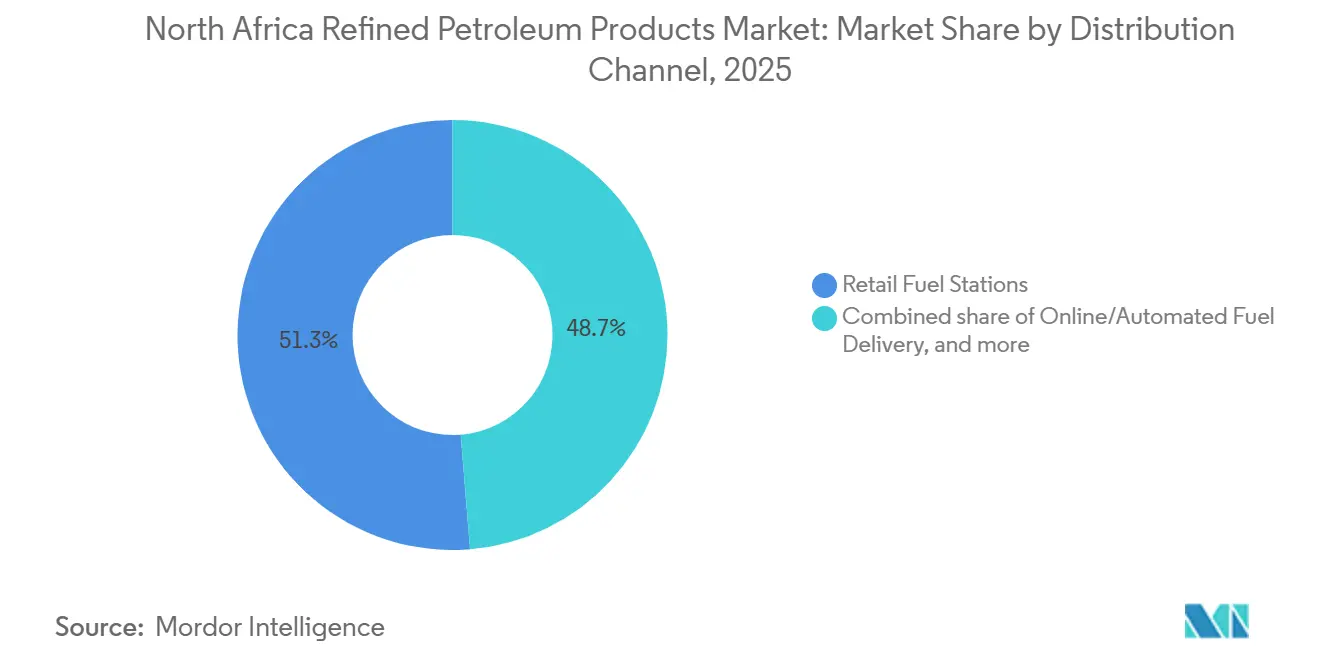

- By distribution channel, retail fuel stations controlled 51.3% of 2025 volume; online and automated delivery platforms are expanding at a 7.1% CAGR to 2031.

- By end-use sector, transportation accounted for a 55.9% share of the North Africa refined petroleum products market size in 2025, and petrochemicals are set to grow at a 6.8% CAGR through 2031.

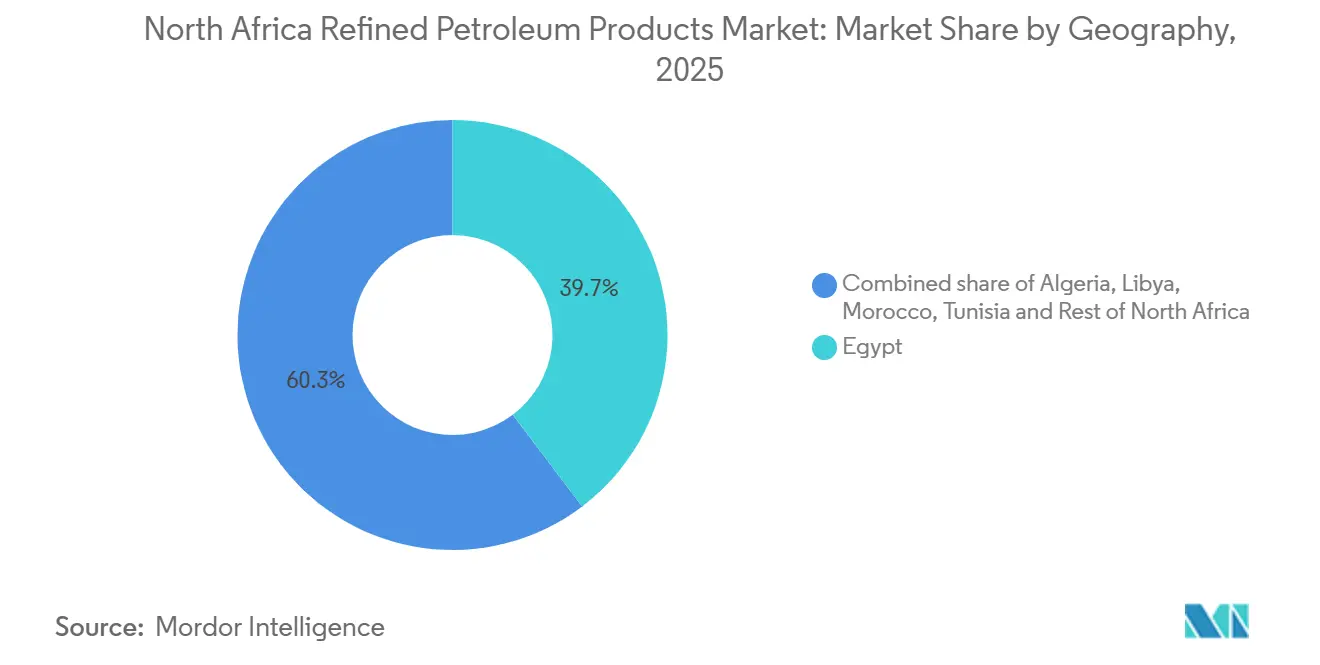

- By geography, Egypt led with a 39.7% North Africa refined petroleum products market share in 2025, while its own segment is forecast to expand at a 5.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North Africa Refined Petroleum Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vehicle-fleet growth boosts transport fuel demand | 1.2% | Egypt, Algeria, Morocco - urban corridors and cross-border freight routes | Medium term (2-4 years) |

| Refinery upgrades & capacity expansions (Egypt, Algeria) | 1.0% | Egypt (MIDOR, Assiut, Alexandria Petroleum), Algeria (Hassi Messaoud, Skikda) | Long term (≥ 4 years) |

| Gradual subsidy reform improving downstream economics | 0.8% | Egypt, Libya - fiscal consolidation under IMF programs | Medium term (2-4 years) |

| Port-led bunkering hub strategy post-Mediterranean ECA 0.1% S cap | 0.6% | Egypt (Alexandria, Suez, Port Said), Algeria (Oran, Skikda) | Short term (≤ 2 years) |

| New petrochemical complexes raising naphtha/LPG offtake | 0.7% | Egypt (Carbon Holdings, SIDPEC, Red Sea National Refining), Algeria (Sonatrach Arzew) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vehicle-Fleet Growth Boosts Transport Fuel Demand

Continued urbanization, stronger tourism flows, and expanding cross-border freight routes are lifting gasoline, diesel, and jet-fuel consumption. Egypt’s target of 30 million tourists by 2028 widens rental-car fleets and inter-city coach services, while Morocco’s aviation hubs posted double-digit traffic gains in 2024. Algeria’s Naftal distributed 13.3 million tonnes of fuels in 2024 and expects steady growth as it reorganizes products and channels. Fuel subsidies in Libya still absorb 35% of GDP, encouraging smuggling that artificially inflates regional demand statistics and keeps refinery throughputs elevated. Despite ongoing power fuel switching, transport remains resilient, reinforcing a positive volume outlook for the North Africa refined petroleum products market.

Refinery Upgrades and Capacity Expansions

Egypt invested roughly USD 8 billion in its downstream over the past decade, including MIDOR’s USD 2.7 billion expansion, Assiut’s USD 1.5–3 billion hydrocracker, and Alexandria Petroleum debottlenecking. Combined projects lift national capacity toward 900,000 barrels per day by 2027. Algeria’s 110,000-barrel-per-day Hassi Messaoud refinery broke ground in 2025 and complements Sonatrach’s revitalized Skikda and Arzew plants. Raised complexity boosts white-product yields and Euro 5 compliance, shrinking import dependence and setting the stage for export arbitrage within the North Africa refined petroleum products market.

Gradual Subsidy Reform Improving Downstream Economics

Egypt increased pump prices by up to 15% during 2024-25 and moved to cash transfers by mid-2025 under its IMF program. Narrower parity gaps lift refinery margins and attract private investment, such as Qalaa Holdings’ USD 200 million Mostorod Phase 2 expansion. Libya’s generous subsidy regime still distorts trade flows, while Algeria maintains low domestic prices to preserve social stability. The divergence channels capital toward Egypt and limits private initiatives elsewhere, shaping competitive dynamics in the North Africa refined petroleum products market.

Port-Led Bunkering Hub Strategy After Mediterranean 0.1% Sulfur Cap

IMO rules effective May 2025 require 0.1% sulfur marine fuel in the Mediterranean.[1]Arab Finance editors, “Egypt enforces Euro 5 diesel nationwide,” arabfinance.com Egypt enforced compliance at Alexandria, Suez, and Port Said, leveraging its Suez Canal traffic to capture incremental bunkering demand. Established storage and blending assets allow rapid scale-up of very-low-sulfur fuel oil and marine gasoil, diverting volumes from European ports and lifting the overall CAGR of the North Africa refined petroleum products market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Political-security disruptions curbing Libyan crude feedstock | -0.5% | Libya (Zawiya, Ras Lanuf refineries), regional crude export terminals | Short term (≤ 2 years) |

| Import competition from surplus EU & Middle-East products | -0.4% | Morocco, Tunisia, Libya - import-dependent markets | Medium term (2-4 years) |

| Power-sector fuel-switching to gas & renewables cuts FO/diesel demand | -0.3% | Egypt, Algeria - grid-connected generation and industrial captive power | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Political-Security Disruptions Curbing Libyan Crude Feedstock

Zawiya refinery halted operations in December 2024 after armed clashes destroyed storage tanks, mirroring previous outages that slashed national output by 63% in August 2024. Repeated force majeure erodes feedstock supply, forces higher imports, and pushes refiners in neighboring states to source costlier barrels, hindering the growth of the North Africa refined petroleum products market.

Import Competition from Surplus EU and Middle-East Products

EU exports worth USD 3.9 billion to Libya, USD 3.1 billion to Morocco, and USD 2.0 billion to Egypt in 2023 illustrate the scale of external inflows. Oversupply from European and Gulf mega-refineries depresses regional prices and limits local expansion viability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Aviation Fuel Outpaces Diesel Growth

Aviation fuel volume expands at a 6.5% CAGR between 2026 and 2031 as Cairo, Casablanca, and Marrakech airports add gates and carriers. Diesel retained the largest slice at 35.5% of the North Africa refined petroleum products market size in 2025, but its 4.5% growth trails jet fuel because power-generation displacement offsets freight gains. Petrol follows overall demand, LPG holds niche cooking and rural roles, and fuel oil contracts under emission curbs. Bitumen and naphtha rise with road building and petrochemical feedstock pull. The strategic trade-off pushes refiners to maximize middle distillates, underpinning profitability across the North Africa refined petroleum products market.

Egypt’s aim for 30 million tourists by 2028 implies roughly 1.5 million tonnes of incremental jet fuel that MIDOR and Assiut must meet, encouraging further hydrotreating investments. Premium jet margins and stable airline contracts make kerosene optimization a top priority within the North Africa refined petroleum products industry.

By Sulfur Content: Low-Sulfur Dominance Reflects Regulatory Tightening

Low-sulfur grades captured 58.1% share in 2025 and are projected to expand at a 5.3% CAGR through 2031 as Egypt and Morocco enforce Euro 5 standards.[2]Arab Finance editors, “Mediterranean ECA rules come into force,” arabfinance.com Algeria moves gradually yet plans full alignment post-2027, while Tunisia and Libya lag. High-sulfur fuels rise just 3.8% amid marine sulfur caps and shrinking power-sector usage. Complex refineries with hydrotreaters seize premium margins, whereas older topping plants risk stranded status unless modernized. This divergence drives technology uptake and capital flows across the North Africa refined petroleum products market.

By Distribution Channel: Digital Platforms Disrupt Retail Networks

Traditional stations still moved 51.3% of 2025 volumes, but online and automated delivery posts a 7.1% CAGR through 2031 as corporate fleets adopt cashless fuel cards and mobile apps. NaftalCard’s January 2025 launch exemplifies the shift, mirrored by pilots from Vivo Energy and TotalEnergies. Digital entrants capture data, reduce shrinkage, and rationalize logistics, eroding forecourt volumes in urban hubs. Retail operators add non-fuel conveniences and loyalty programs to defend their share in the North Africa refined petroleum products market.

By End-Use Sector: Petrochemicals Surge as Power Demand Wanes

Transportation absorbed 55.9% of 2025 demand and advances 4.8% yearly, but petrochemicals lead at 6.8% thanks to USD 14 billion of greenfield crackers in Egypt and Algeria. Power generation retreats at -1.0% CAGR as gas and renewables gain. Industrial, residential, and commercial segments post moderate 3–4% growth. Marine and bunkering climb 5.5% on ECA compliance, enhancing port revenues and consolidating Egypt’s role within the North Africa refined petroleum products market.

Geography Analysis

Egypt accounts for the largest slice of the North Africa refined petroleum products market and shows the fastest growth. Refinery capacity will reach 900,000 barrels per day by 2027 after modernization at MIDOR, Assiut, and Egyptian Refining Company.[3]MIDOR press release, “Capacity expansion completed,” midor.com Retail price alignment under subsidy rollback improves margins and crowds in private capital. Ports along the Suez Canal secure bunkering business after the 0.1% sulfur ceiling, boosting marine fuel throughput. Tourism and petrochemicals provide durable demand engines, giving Egypt a sustained 5.2% CAGR.

Algeria ranks second with roughly 28% of demand and a 4.5% CAGR. Sonatrach achieved refined-product self-sufficiency in 2023, freeing capacity for export once Hassi Messaoud starts up in 2027. Continued upstream investment by Eni and Sinopec safeguards crude supply, while inland plants extend coverage to the south. Low domestic pump prices maintain consumption, but delayed subsidy reform may restrain private downstream participation in the North Africa refined petroleum products market.

Libya contributes 18% yet rises only 3.5% annually due to chronic insecurity. Zawiya outages compel imports despite 380,000 barrels per day of nameplate capacity. The resulting reliance on European cargoes undercuts domestic margins and blunts growth prospects. Morocco holds a 10% share and grows 4.0% on tourism and mining, but the absence of refining keeps it vulnerable to global price swings. Tunisia and the rest of North Africa together account for about 6% and show sub-4% growth, given limited infrastructure and lower purchasing power.

Competitive Landscape

The North Africa refined petroleum products market is moderately concentrated. State-owned Sonatrach, Egyptian General Petroleum Corporation, and Libya National Oil Corporation dominate throughput and logistics, while TotalEnergies, Shell, and Eni emphasize upstream and selective downstream links. Upgrades at MIDOR and Assiut embed Honeywell UOP and TechnipFMC technology that raises complexity and assures Euro 5 output, amplifying competitive gaps against legacy skimming plants.[4]TechnipFMC corporate news, “MIDOR awards modernization contract,” technipfmc.com International majors channel capital toward integrated gas and petrochemical schemes, seeking higher margins than basic fuels. Niche challengers such as Qalaa Holdings and Shard Capital focus on refining-petrochemical hybrids offering flexibility and export optionality.

Retail distribution sees Vivo Energy, Puma Energy, and Naftal scale digital solutions for fleets. Morocco and Tunisia, lacking domestic refineries, are prime targets for import-terminal or greenfield complex proposals. Success hinges on political stability, feedstock security, and alignment with tightening environmental norms that underpin value accrual in the North Africa refined petroleum products market.

North Africa Refined Petroleum Products Industry Leaders

Sonatrach SPA

Royal Dutch Shell Plc

Egyptian General Petroleum Corporation

TotalEnergies SE

Exxon Mobil Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Driven by new expansion plans, Middle East Oil Refinery (MIDOR) has ramped up its operating capacity to 160,000 barrels per day (bbl/d), with the goal of bolstering local production and curbing import dependence.

- May 2025: Starting May 1, 2025, Egypt's Mediterranean ports, including Alexandria, will enforce a 0.1% sulfur marine fuel rule for ships. This move aligns with the Mediterranean Sea's designation as a Sulphur Oxides Emission Control Area (Med SOx ECA).

- February 2025: Shard Capital Partners, the project leader, announced that Egypt's ambitious USD 7 billion petrochemical complex in New Alamein City aims to churn out 3.1 million tonnes annually of "eight specialized" products.

- November 2024: Egyptian Refining Company (ERC), a subsidiary of EGX-listed Qalaa Holdings, has unveiled a USD 200 million investment for the second phase of its expansion. This move will boost ERC's refining capacity by an additional 600,000 tonnes per annum.

North Africa Refined Petroleum Products Market Report Scope

Crude oil undergoes industrial processes, chiefly {fractional distillation}, to yield refined petroleum products. These include not only the familiar fuels like gasoline, diesel, and jet fuel, but also heating oil and other crucial materials. Beyond these, the spectrum of refined products extends to LPG, asphalt, lubricants, waxes, petrochemical feedstocks, and petroleum coke, all of which play pivotal roles in fueling transportation, industry, and everyday life.

The North Africa refined petroleum products market is segmented by product type, sulfur content, distribution channel, end-use sector, and geography. By product type, the market is segmented into petrol, diesel, LPG, kerosene, aviation fuel, fuel oil, and others. By sulfur content, the market is segmented into low-sulfur and high-sulfur refined petroleum products. By distribution channel, the market is segmented into retail, bulk, direct, and online channels. By end-use sector, the market is segmented into transportation, power, industrial, petrochemicals, residential, marine, and agriculture. The report also covers the market size and forecasts for the West Africa refined petroleum products market across key countries in the region, including Algeria, Egypt, Libya, Morocco, Tunisia, Rest of North Africa. For each segment, the market sizing and forecasts have been conducted on the basis of value (USD).

By Product Type

| Petrol (Gasoline) |

| Diesel |

| LPG |

| Kerosene |

| Aviation Fuel |

| Fuel Oil (HSFO, VLSFO) |

| Others (Bitumen, Naphtha) |

By Sulfur Content

| Low-Sulfur (Up to 10 ppm) |

| High-Sulfur (Above 10 ppm) |

By Distribution Channel

| Retail Fuel Stations |

| Commercial Bulk Sales |

| Direct Supply Contracts |

| Online/Automated Fuel Delivery |

By End-Use Sector

| Transportation |

| Power Generation |

| Industrial Manufacturing |

| Petrochemicals |

| Residential and Commercial |

| Marine and Bunkering |

| Agriculture and Mining |

By Geography

| Algeria |

| Egypt |

| Libya |

| Morocco |

| Tunisia |

| Rest of North Africa |

| By Product Type | Petrol (Gasoline) |

| Diesel | |

| LPG | |

| Kerosene | |

| Aviation Fuel | |

| Fuel Oil (HSFO, VLSFO) | |

| Others (Bitumen, Naphtha) | |

| By Sulfur Content | Low-Sulfur (Up to 10 ppm) |

| High-Sulfur (Above 10 ppm) | |

| By Distribution Channel | Retail Fuel Stations |

| Commercial Bulk Sales | |

| Direct Supply Contracts | |

| Online/Automated Fuel Delivery | |

| By End-Use Sector | Transportation |

| Power Generation | |

| Industrial Manufacturing | |

| Petrochemicals | |

| Residential and Commercial | |

| Marine and Bunkering | |

| Agriculture and Mining | |

| By Geography | Algeria |

| Egypt | |

| Libya | |

| Morocco | |

| Tunisia | |

| Rest of North Africa |

Key Questions Answered in the Report

What is the current value of the North Africa refined petroleum products market?

The market is valued at USD 51.69 billion in 2026 and is projected to reach USD 61.16 billion by 2031.

Which country leads demand in North Africa for refined products?

Egypt dominates with 39.7% regional demand in 2025 and posts the fastest growth at a 5.2% CAGR through 2031.

Which product segment grows the fastest?

Aviation fuel records a 6.5% CAGR from 2026 to 2031 as airport expansions and tourism lift jet-fuel demand.

How is the sulfur cap affecting marine fuels in the region?

A 0.1% sulfur limit effective May 2025 shifts bunkering to compliant ports such as Alexandria, Suez and Port Said, raising demand for very-low-sulfur grades.

What role do digital platforms play in distribution?

Online and automated channels, led by programs like NaftalCard, grow 7.1% yearly by streamlining fleet transactions and reducing cash handling.

Page last updated on: