Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

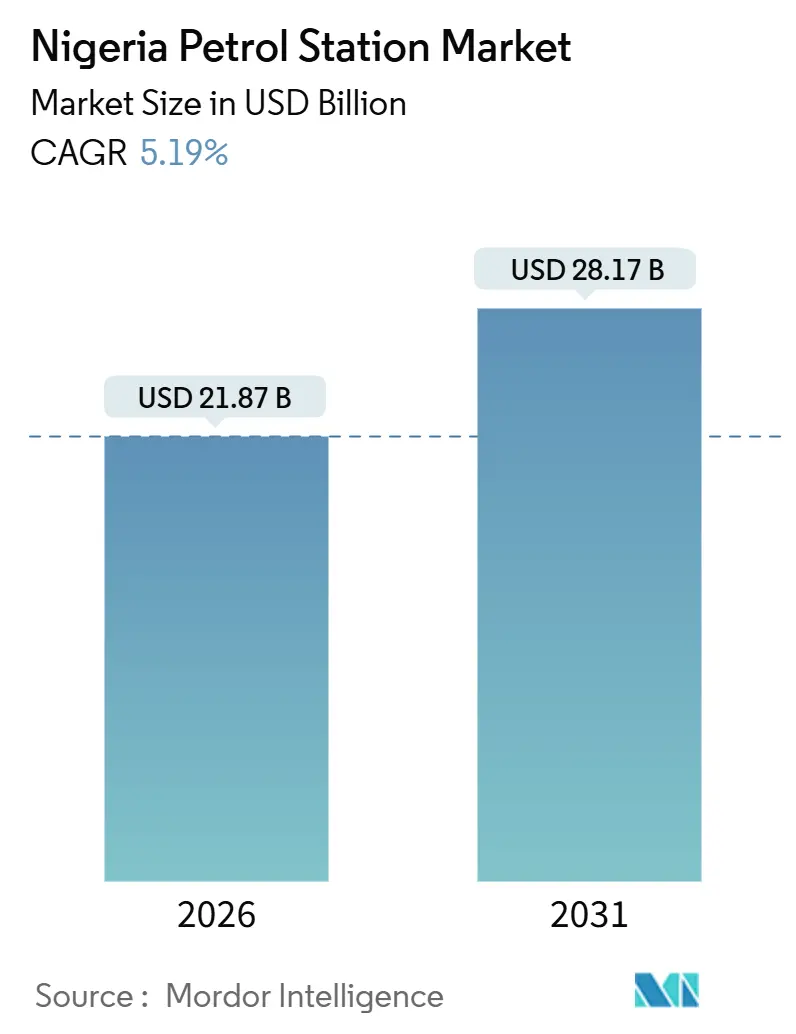

| Market Size (2026) | USD 21.87 Billion |

| Market Size (2031) | USD 28.17 Billion |

| Growth Rate (2026 - 2031) | 5.19% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Petrol Station Market Analysis by Mordor Intelligence

The Nigeria Petrol Station Market size is estimated at USD 21.87 billion in 2026, and is expected to reach USD 28.17 billion by 2031, at a CAGR of 5.19% during the forecast period (2026-2031).

Deregulated pump prices, the September 2024 start-up of the 650,000 bpd Dangote Refinery, and expanding multi-fuel infrastructure underpin the growth trajectory of the Nigeria petrol station market.[1]Dangote Industries, “Retail Roll-Out at 650,000 bpd Lekki Refinery,” dangote.com Capital is flowing toward compressed natural gas (CNG) and liquefied petroleum gas (LPG) dispensing, digital payments, and food-service co-location as operators defend margins in the post-subsidy era. FX-driven cost volatility, urban e-mobility adoption, and policy uncertainty around fuel tariffs temper momentum yet have accelerated portfolio diversification. Operators that secure long-term supply contracts with domestic refiners, embed retail technology, and prioritize underserved highway and northern corridors are positioned to outperform within the Nigeria petrol station market.

Key Report Takeaways

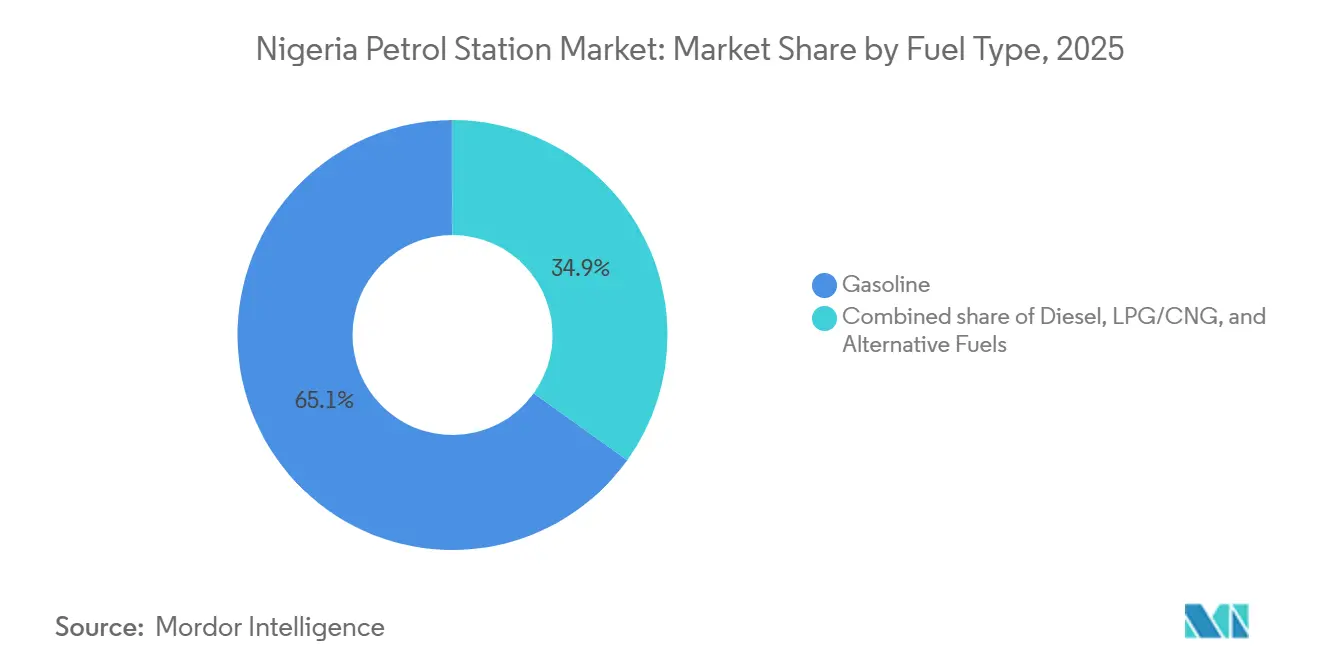

- By fuel type, gasoline led with 65.1% of the Nigeria petrol station market share in 2025; LPG/CNG installations are forecast to expand at a 23.8% CAGR through 2031.

- By service offering, fuel-only formats accounted for 50.5% of the Nigeria petrol station market size in 2025, while multi-energy hubs are advancing at a 26.2% CAGR to 2031.

- By station format, traditional full-service outlets held 63.3% of the Nigeria petrol station market share in 2025; highway service plazas are projected to grow at a 7.5% CAGR between 2026 and 2031.

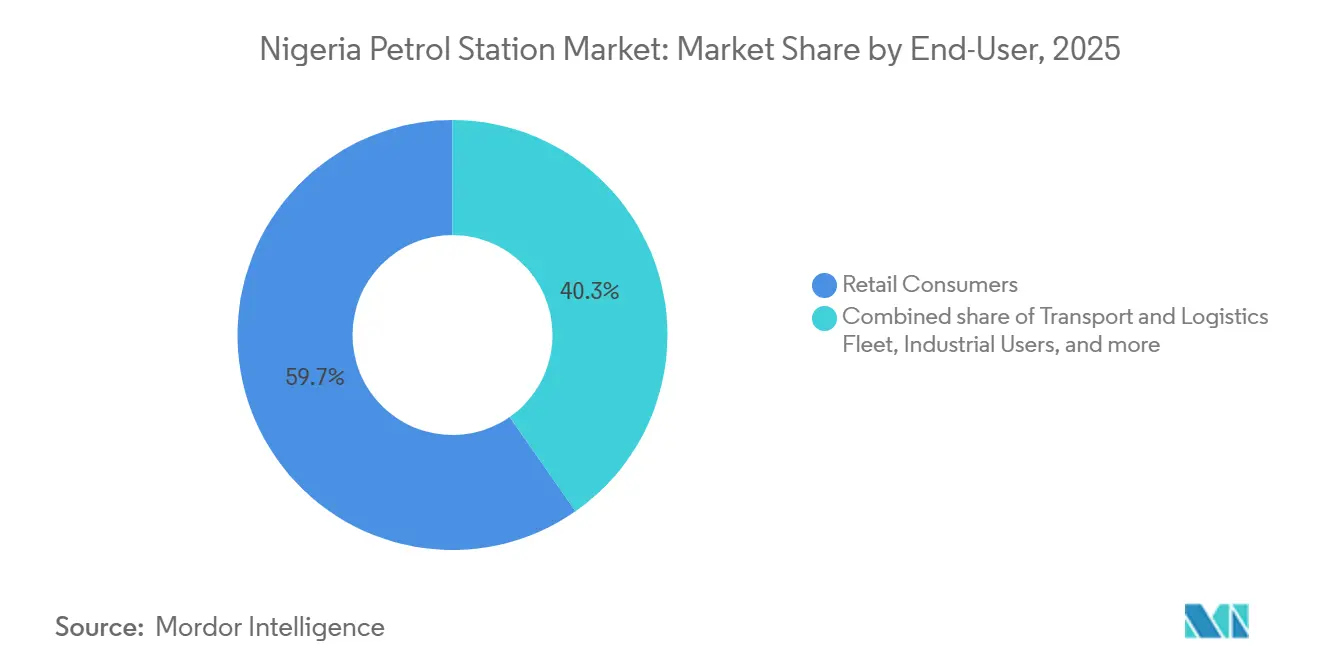

- By end-user, retail consumers represented 59.7% of the Nigeria petrol station market size in 2025, and transport-logistics fleets are expanding at a 6.9% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Nigeria Petrol Station Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vehicle ownership & middle-class growth | +1.2% | Lagos, Abuja, Port Harcourt | Medium term (2-4 years) |

| Fuel-price deregulation attracting private capital | +1.5% | National | Short term (≤ 2 years) |

| Expansion of road infrastructure | +0.8% | Lagos-Ibadan, Abuja-Kaduna, Niger Delta | Long term (≥ 4 years) |

| Co-location with QSR & fintech services boosts non-fuel revenue | +0.6% | Lagos, Abuja, Kano, Port Harcourt | Medium term (2-4 years) |

| National Gas Expansion Programme driving LPG/CNG pumps | +1.8% | Lagos, Abuja, nationwide depots | Short term (≤ 2 years) |

| Modular refineries ensuring localized supply | +0.5% | Imo, Edo, Rivers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle Ownership & Middle-Class Growth

Nigeria’s registered vehicle fleet exceeded 11.6 million units in 2024, yet per-capita ownership sits below 60 vehicles per 1,000 people, indicating headroom for expansion as consumer credit and disposable income rise. Household final-consumption expenditure grew 3.8% year-on-year in Q3 2024, supporting personal-mobility spending even with inflation near 30%.[2]Nigerian National Petroleum Company, “Downstream Facts & Figures,” nnpcgroup.com Lagos captures roughly 25% of national vehicle registrations, but tier-2 cities such as Ibadan, Benin City, and Kaduna offer higher growth potential due to lower station density and improving road networks. Operators focusing on land-banking in these secondary metros within the Nigeria petrol station market can secure favorable urban-planning approvals before land values adjust upward. As financing models mature, motorization in northern states is expected to converge with southern levels, broadening the addressable base for the Nigeria petrol station market.

Fuel-Price Deregulation Attracting Private Capital

The May 2023 subsidy removal eliminated an NGN 4 trillion annual fiscal burden and allowed pump prices to float with Brent and naira exchange rates, enabling transparent margins for the first time in decades. Pension funds and private equity subsequently financed roll-outs and acquisitions, exemplified by NNPC Retail’s December 2024 purchase of 380 Oando outlets that lifted its network above 1,000 stations. Dangote Refinery’s December 2025 move into direct retail at NGN 739 per liter undercut import parity by roughly 8%, forcing legacy importers to cede share. The October 2025 introduction of a 15% refined-product tariff highlighted regulatory volatility, yet operators are hedging risk through long-term offtake agreements with domestic refiners. Rapid capital deployment positions integrated players to capture volume and non-fuel spend within the Nigeria petrol station market.

Expansion of Road Infrastructure

Completion of the 127 km Lagos-Ibadan Expressway and Abuja-Kaduna upgrades reduced travel times by up to 40% and created demand for highway plazas offering fuel, food, parking, and EV charging. Service plazas can command margins 30% higher than standalone pumps by monetizing captive traffic and diversified revenue streams. The Second Niger Bridge has likewise spurred station development in Anambra and Delta, capitalizing on freight traffic doubling between Lagos and the east. Build-operate-transfer concessions approved by the Infrastructure Concession Regulatory Commission allow 25-year tenures, improving bankability for green-field highway assets. Operators that align site selection with toll-plaza locations and weigh-station nodes gain throughput advantages that reinforce the Nigeria petrol station market footprint.

Co-Location with QSR & Fintech Services Boosts Non-Fuel Revenue

TotalEnergies Marketing Nigeria’s integration of Café Bonjour, KFC, and Chicken Republic across 577 stations lifted food-service income to as much as 20% of site revenue in 2025. Digital payments, led by Flutterwave and Paystack, captured 43% of transactions, reducing cash-handling losses and enabling loyalty analytics. Non-fuel services carry gross margins of 20-25%, compared with 8-12% for fuel, cushioning stations against wholesale-price swings. Urban sites with daily throughput above 500 vehicles justify the capital intensity of kitchens and fintech kiosks, while rural outlets remain fuel-centric. The Nigeria petrol station industry increasingly treats forecourts as omnichannel retail hubs, blending fuel, food, and financial services to amplify wallet share.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FX shortages & import dependence create supply volatility | -1.5% | National | Short term (≤ 2 years) |

| Policy flip-flops on fuel subsidies | -0.8% | National | Short term (≤ 2 years) |

| Urban e-motorcycle adoption trims petrol demand | -0.4% | Lagos, Ogun, Abuja | Medium term (2-4 years) |

| Pipeline vandalism & fuel theft disrupt logistics | -0.6% | Niger Delta, Lagos-Ibadan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

FX Shortages & Import Dependence Create Supply Volatility

The naira slid from NGN 460/USD in early 2023 to beyond NGN 1,700/USD by late 2025, inflating landed fuel costs more than 250% and tightening supply whenever marketers could not secure forex from the central bank. Oando’s 9-month 2025 refined-product volume fell 56% year-on-year, reflecting a pause in petrol imports once Dangote came onstream. Although domestic refining eases FX pressure, gasoline remained tight into Q1 2026 as Dangote prioritized diesel and jet fuel. Import tariffs imposed in October 2025 exacerbated scarcity, forcing retailers to carry 7-10 days of inventory versus the global norm of 3-5 days, tying up working capital within the Nigeria petrol station market.

Policy Flip-Flops on Fuel Subsidies

The May 2023 subsidy removal tripled pump prices to NGN 540 per liter, yet tariff hikes and state-level caps in 2025 exposed the reversibility of deregulation. Temporary ceilings squeezed retailer margins below breakeven for six weeks, undermining confidence in payback periods required for station construction. Although the Petroleum Industry Act vests price oversight in NMDPRA, political override remains plausible, elevating cost-of-capital hurdles for investors considering the Nigeria petrol station market.

Segment Analysis

By Fuel Type: CNG Installations Outpace Gasoline Growth

Gasoline retained 65.1% revenue share in 2025, yet LPG/CNG dispensing is advancing at a 23.8% CAGR to 2031 as fleets chase 60-70% fuel-cost savings.[3]Nigerian National Petroleum Company, “Downstream Facts & Figures,” nnpcgroup.com The Nigeria petrol station market size for LPG/CNG is forecast to swell as NNPC targets more than 100 CNG outlets by 2026. Diesel remains indispensable for heavy freight, but early electric-truck pilots and the 2025 zero-emission mandate for urban logistics challenge its long-term dominance.[4]Energy Commission of Nigeria, “Electric Vehicle Transition and Green Mobility Bill 2025,” energy.gov.ng

Momentum favors gas and electricity. Lagos's genset electrification and growing EV penetration slow gasoline growth, while vehicle-conversion costs bottleneck CNG uptake. Urban LPG adoption is brisk thanks to cylinder distribution, whereas rural penetration lags. Hydrogen and fast charging remain nascent yet benefit from the presidential target of 10,000 chargers by 2028. Collectively, these shifts push operators to adopt multi-fuel forecourts, embedding resilience in the Nigeria petrol station market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Service Offering: Multi-Energy Hubs Lead Format Innovation

Fuel-only stores still generated 50.5% of 2025 revenue, but their share is shrinking as multi-energy hubs notch a 26.2% CAGR, propelled by mandated EV-charger installation. Fuel-and-convenience-store formats are ubiquitous in cities, while fuel-c-store-QSR layouts dominate highway corridors where captive demand justifies kitchen investment.

Service diversification lifts margins: food and retail yield up to 25% gross margins, cushioning deregulation-induced fuel volatility. Digital payments streamline loyalty schemes and inventory turns. Rural locations, with lower vehicle counts, retain fuel-centric models yet will gradually add CNG dispensers once conversion financing expands. The evolution underscores how non-fuel revenue secures profitability for the Nigeria petrol station market.

By Station Format: Highway Plazas Capture Infrastructure Spend

Traditional full-service stations held a 63.3% share in 2025, but highway plazas are racing ahead at a 7.5% CAGR as expressway upgrades finalize. Integrated rest stops embed fuel, QSR, parking, and EV charging, extracting higher spend per stop.

Compact and micro-stations thrive in densely populated Lagos zones where land exceeds NGN 500 million per hectare. Skid-mounted LPG modules require one-third the footprint of conventional sites, enabling infill growth. Self-service dispensers emerge in cities to cut labor costs, while attendant service endures in rural regions. Supply-chain economics favor sites within 50 km of depots or refineries, reinforcing location as a differentiator in the Nigeria petrol station market.

By End-User: Fleet Conversions Drive Commercial Segment

Retail consumers contributed 59.7% of the 2025 value, yet transport-logistics fleets, growing at a 6.9% CAGR, are adopting CNG and EV technology for cost predictability. Fleets unlock two-year paybacks on conversions, accelerating volume migration from petrol.

Industrial users pivot toward grid power and solar hybrids to curb diesel genset reliance, trimming bulk-fuel demand. Government and public-sector fleets are increasingly sourcing through retail networks under framework agreements, adding a stable off-take segment. Diverse end-user needs necessitate flexible dispensing options, anchoring a multi-energy strategy across the Nigeria petrol station market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Nigeria’s 31,220 retail stations are distributed unevenly: 12,950 in the north, 11,193 in the west, and 7,077 in the east. Lagos houses 3,000 sites yet posts lower per-station throughput, 40,000-50,000 liters/month, due to saturation, versus 80,000-100,000 liters in Abuja and Port Harcourt. Landlocked Kano and Kaduna pay NGN 50-80 more per liter than coastal Lagos as long-haul trucking inflates costs, encouraging cross-border smuggling to Niger and Cameroon.

Southern states benefit from refining capacity and port access. Dangote’s Lekki terminal supplies Lagos and adjoining corridors at logistics savings of 20-30%. Modular refineries in Imo and Edo feed depots within 50 km, modestly easing Delta and southeast pricing but covering less than 2% of national demand. Highway upgrades shift development toward expressway nodes, and Infrastructure-Concession concessions de-risk private investment in plazas.

CNG infrastructure clusters in Lagos and Abuja, leaving northern and southeastern states underserved; expanding conversion centers there is essential to democratize benefits. EV-charging mandates will burden rural forecourts in Borno and Zamfara, where power reliability and demand remain weak. Regional divergence implies that operators tailoring formats to local economies will gain share in the Nigeria petrol station market.

Competitive Landscape

Despite NNPC Retail’s leap to 1,000-plus stations after acquiring Oando outlets, independent marketers still operate roughly 60% of Nigeria’s network, keeping the field fragmented. TotalEnergies runs 577 solarized sites, posted NGN 1.04 trillion revenue in 2024, and leverages QSR tie-ins for differentiation. Rainoil controls 200 stations and three depots holding 50 million liters, reporting USD 696 million revenue for 2025. Ardova, Conoil, MRS, and 11 Plc each manage 100-300 sites, largely in the south and west.

Technology uptake is variable. NNPC’s fiber-optic pipelines cut theft by 40% in pilots, while LiveEO’s satellite analytics prevented USD 800,000 per connection in vandal losses. Digital payments at 43% of transactions reduce cash shrinkage and inform dynamic pricing. Fintech-fuel integrations, modular refineries supplying regional depots, and EV-charging developers are emerging disruptors poised to reshape the Nigeria petrol station market.

Consolidation pressure will intensify as scale advantages in procurement, financing, and non-fuel cross-sell widen profitability gaps. Operators balancing domestic supply contracts, retail-tech investment, and multi-energy capability will defend and grow share.

Nigeria Petrol Station Industry Leaders

NNPC Retail Ltd.

TotalEnergies Marketing Nigeria Plc

Conoil Plc

Ardova Plc

11 Plc (Ex-Mobil)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2026: TotalEnergies has agreed to sell its 10% stake in Nigeria’s onshore SPDC assets, which are part of broader operations that include approximately 540 petrol stations across the country. The sale to Vaaris Resources follows a previously blocked transaction and is intended to refocus on other energy assets while divesting from mature onshore operations within Nigeria’s oil industry.

- December 2025: Dangote Refinery began nationwide retail sales at NGN 739 per liter, underselling import parity by 8% and reshaping wholesale economics.

- October 2025: The federal government levied a 15% import tariff on refined products, pushing pump prices above NGN 1,000 and igniting protests.

- July 2025: Oando upsized its Afreximbank reserve-based loan to USD 375 million to pivot from imports to domestic supply.

Nigeria Petrol Station Market Report Scope

A fuel station, also known as a petrol station or gas station, is a facility that sells fuel and engine lubricants for motor vehicles. Fuel dispensers are used to pump gasoline and diesel into the tanks within vehicles and calculate the financial cost of the fuel transferred to the vehicle.

The Nigeria fuel station market report is segmented into fuel type, service offering, station format, end-user, and geography. By fuel type, the market is divided into gasoline, diesel, LPG/CNG, and alternative fuels. By service offering, the market is segmented into fuel only, fuel and convenience store, fuel/c-store/QSR, and multi-energy hubs. By station format, the market is segregated into traditional full-service, compact/micro-stations, and others. By end-user, the market is divided into retail consumers, commercial fleets, industrial users, transport/logistics fleets, and air/marine transport. The market sizing and forecasts for each segment are based on the revenue generated (in USD).

By Fuel Type

| Gasoline |

| Diesel |

| Liquified Petroleum Gas (LPG)/Compressed Natural Gas (CNG) |

| Alternative Fuels (Hydrogen, EV Charging) |

By Service Offering

| Fuel Only |

| Fuel and Convenience Store |

| Fuel, C-Store, and Quick-Serve Restaurant |

| Multi-Energy Hubs (Fuel + EV/H₂) |

By Station Format

| Traditional Full-Service |

| Compact/Micro-stations |

| Highway Service Plazas |

By End-User

| Retail Consumers |

| Commercial Fleets |

| Industrial Users |

| Transport and Logistics Fleets |

| Air/Marine Transport |

| By Fuel Type | Gasoline |

| Diesel | |

| Liquified Petroleum Gas (LPG)/Compressed Natural Gas (CNG) | |

| Alternative Fuels (Hydrogen, EV Charging) | |

| By Service Offering | Fuel Only |

| Fuel and Convenience Store | |

| Fuel, C-Store, and Quick-Serve Restaurant | |

| Multi-Energy Hubs (Fuel + EV/H₂) | |

| By Station Format | Traditional Full-Service |

| Compact/Micro-stations | |

| Highway Service Plazas | |

| By End-User | Retail Consumers |

| Commercial Fleets | |

| Industrial Users | |

| Transport and Logistics Fleets | |

| Air/Marine Transport |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value and projected size of the Nigeria petrol stations market?

The Nigeria petrol stations market size was USD 21.87 billion in 2026 and is forecast to reach USD 28.17 billion by 2031, reflecting a 5.19% CAGR.

How did Dangote Refinery change retail fuel economics?

By starting retail sales at NGN 739 per liter in December 2025, Dangote undercut import-parity prices by about 8% and reduced marketers forex exposure.

Which fuel type is growing fastest at Nigerian forecourts?

LPG/CNG dispensing is expanding at a 23.8% CAGR through 2031, driven by the NGN 250 billion National Gas Expansion Programme.

Why are multi-energy hubs gaining share?

Mandated EV-charger installation, higher non-fuel margins, and rising digital-payment penetration have propelled multi-energy hubs at a 26.2% CAGR.

What risks could slow market growth?

FX shortages, potential subsidy reinstatement, pipeline vandalism, and urban e-mobility adoption each erode growth, with FX volatility shaving an estimated 1.5 percentage points off forecast CAGR.

Which regions offer the highest throughput per station?

Abuja and Port Harcourt average 80,000-100,000 liters per month, double the saturated Lagos average of 40,000-50,000 liters.