Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

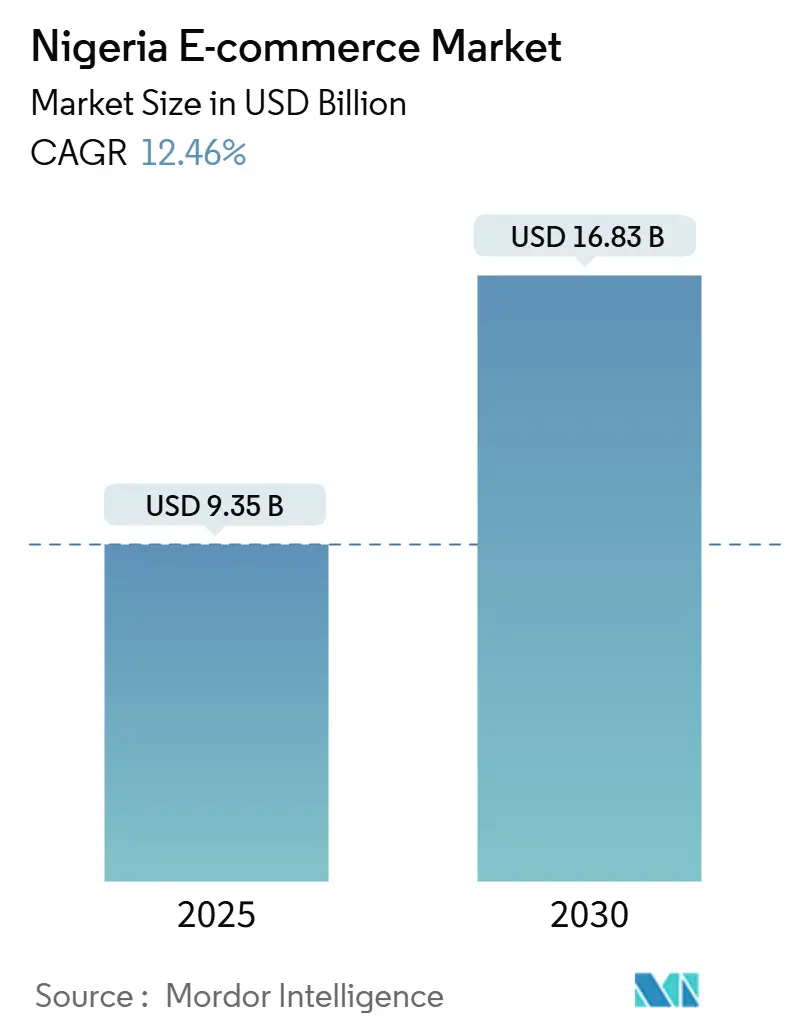

| Market Size (2025) | USD 9.35 Billion |

| Market Size (2030) | USD 16.83 Billion |

| Growth Rate (2025 - 2030) | 12.46% CAGR |

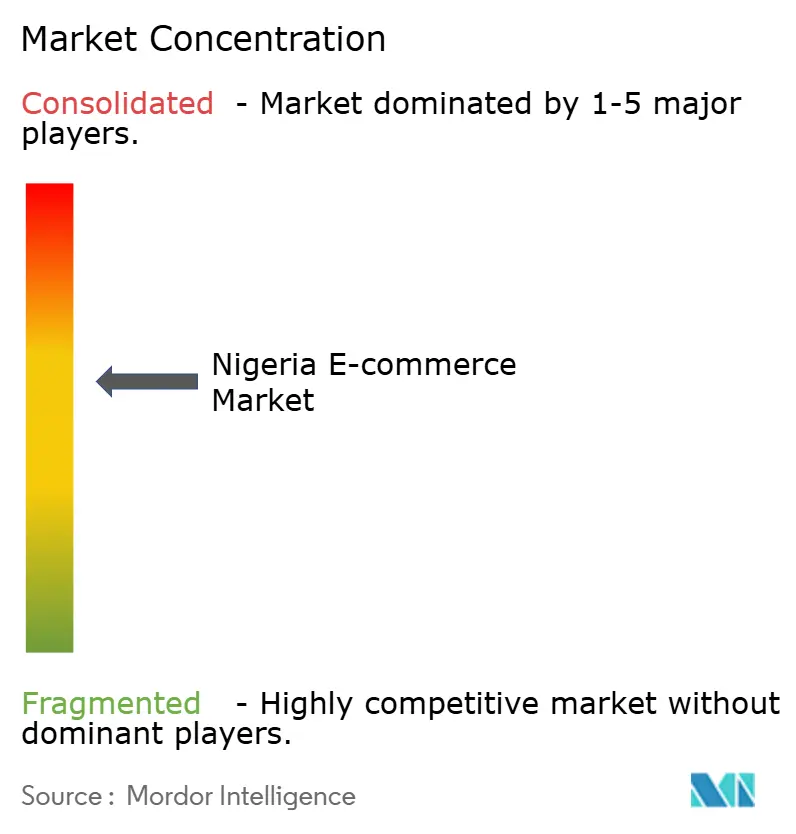

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Nigeria E-commerce Market Analysis by Mordor Intelligence

The Nigeria e-commerce market reached a Nigeria e-commerce market size of USD 9.35 billion in 2025 and is forecast to post USD 16.83 billion by 2030, reflecting a 12.46% CAGR. Rapid smartphone adoption, stronger payment rails and a wider logistics footprint continue to expand digital retail penetration in both urban and semi-urban centres. Mobile commerce now accounts for more than four-fifths of online orders, while social platforms have become critical discovery and checkout venues. Intensifying competition among local and foreign platforms is encouraging investments in same-day fulfilment, embedded finance and richer SKU depth. At the same time, margin management remains a central theme because of Naira volatility, higher last-mile costs and an evolving tax regime for non-resident digital sellers. Market participants that secure dependable logistics partners, diversify currency exposure and leverage data-driven merchandising are best positioned to capture upside within the Nigeria e-commerce market.[1]Federal Ministry of Communications and Digital Economy, “Nigerian National Broadband Plan 2020–2025,” digitalrightslawyers.org

Key Report Takeaways

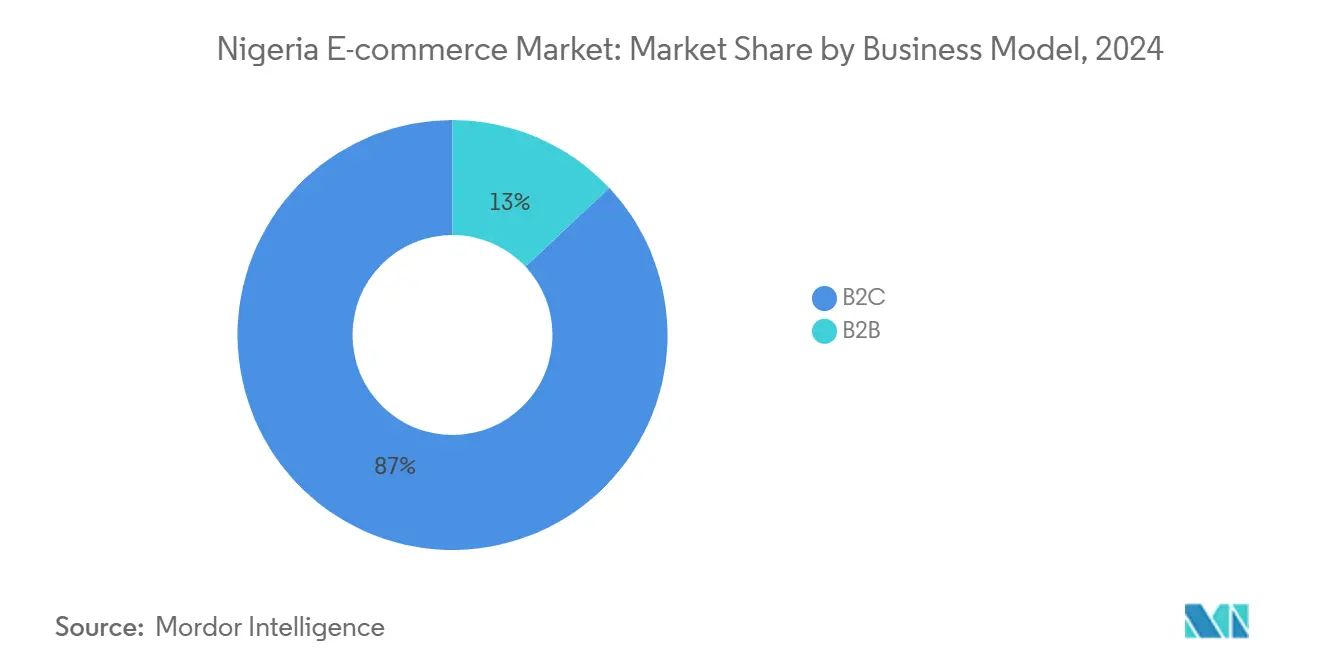

- By business model, the B2C segment held 87% Nigeria e-commerce market share in 2024, while B2B is set to expand at an 18.5% CAGR through 2030.

- By device, smartphones captured 82% of transactions in 2024; desktop-led purchases are forecast to grow at a modest 4.2% CAGR to 2030.

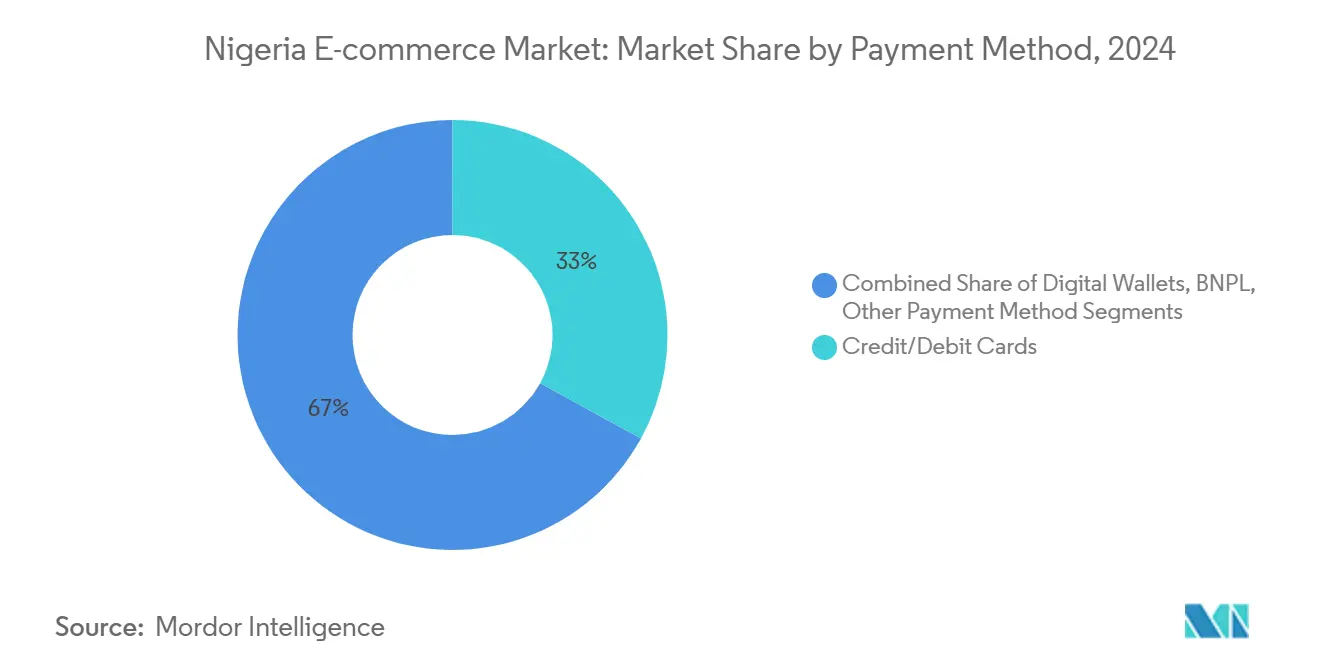

- By payment method, credit/debit cards contributed 33% of transaction value in 2024, whereas BNPL solutions are projected to rise at a 29.4% CAGR between 2025 and 2030.

- By B2C product category, consumer electronics commanded 28% of revenue in 2024; beauty and personal care is advancing at a 16.8% CAGR to 2030.

Nigeria E-commerce Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Social Commerce Adoption via WhatsApp & Instagram | +1.9% | National, with higher impact in Lagos, Abuja, and Port Harcourt | Short term (≤ 2 years) |

| Rapid Expansion of Mobile-Money Agent Network for Pay-on-Delivery Conversion | +1.5% | National, with emphasis on semi-urban and rural areas | Medium term (2-4 years) |

| Government National Broadband Plan Targeting 70% Coverage by 2025 | +2.2% | National, with initial focus on urban centers | Medium term (2-4 years) |

| Logistics Tech Start-ups Enabling Same-Day Fulfilment in Lagos & Abuja | +1.7% | Lagos and Abuja, with gradual expansion to secondary cities | Short term (≤ 2 years) |

| Cross-border Marketplace Integrations Boosting SKU Depth | +1.4% | National, with higher impact in urban centers | Medium term (2-4 years) |

| Rising Adoption of Buy-Now-Pay-Later Increasing Average Basket Size | +2.1% | National, with concentration in middle-income urban areas | Short term (≤ 2 years) |

Source: Mordor Intelligence

Surge in Social Commerce Adoption via WhatsApp & Instagram

Social shopping has shifted from a supplementary marketing tool into a priority sales engine for merchants in the Nigeria e-commerce market. Roughly 36.8 million social users dedicate close to four hours daily to platforms that now embed frictionless checkout. Businesses exploit these high-engagement venues to shorten conversion paths, increase order frequency and reduce reliance on formal storefronts. Real-time messaging builds consumer trust by enabling product verification before purchase. As a result, social commerce transaction value is projected to nearly double from USD 2.04 billion in 2025 to USD 3.96 billion in 2030, outpacing overall market growth. Platforms are also opening monetisation avenues for content creators, adding a community-led influence layer that supports cross-selling.

Rapid Expansion of Mobile-Money Agent Network for Pay-on-Delivery Conversion

Agent banking has evolved into an essential last-mile enabler for online retail, especially beyond tier-one cities. National initiatives targeting an eight-fold increase in female agents are widening consumer touchpoints for digital transactions. Agents convert cash-on-delivery orders into electronic settlements, lowering fraud risk and accelerating cash cycles for merchants. Larger corporates are introducing “agent-as-a-service” models, providing e-commerce platforms with on-demand distribution capacity. With cash still representing 55% of point-of-sale value, these networks help migrate shoppers into formal digital rails, ultimately enlarging addressable demand for the Nigeria e-commerce market.[3]CGAP, “Empowering Small Giants: Inclusive Embedded Finance for Micro Retailers,” cgap.org

Government National Broadband Plan Targeting 70% Coverage by 2025

The broadband roadmap mandates download speeds of 25 Mbps in cities and 10 Mbps in rural zones, aiming to connect at least 90% of the population.[2]Central Bank of Nigeria, “The CBN Economic Report January 2025,” cbn.gov.ng Every 10-point rise in broadband penetration is linked to up to 3.8% incremental GDP, reinforcing political commitment to infrastructure roll-outs. While a USD 461 million funding gap risks delay, public-private co-investment and a recently announced US-Nigeria technology dialogue are catalysing fibre deployment. Greater capacity unlocks richer media experiences, faster page loads and secure payment flows, broadening the customer base and supporting higher-value categories within the Nigeria e-commerce market.

Logistics Tech Start-ups Enabling Same-Day Fulfilment in Lagos & Abuja

More than 370 logistics tech ventures now operate in Nigeria, with funded players introducing AI-based route optimisation, real-time parcel visibility and micro-hub models. Same-day delivery, once aspirational, is becoming viable across key districts, elevating customer satisfaction and repeat orders. Asset-light orchestration platforms aggregate third-party vehicles and riders, cutting fixed costs while scaling capacity for peak events. As logistics reliability improves, retailers can confidently list perishable or fragile items, adding SKU diversity that deepens the Nigeria e-commerce market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban Congestion & Poor Address Systems Inflate Last-Mile Costs | -1.1% | Major urban centers, particularly Lagos and Abuja | Medium term (2-4 years) |

| High Card-Not-Present Fraud & Charge-backs Escalate Merchant Costs | -1.0% | National, with higher impact in urban areas | Short term (≤ 2 years) |

| Naira Volatility Compressing Import-Heavy Category Margins | -1.4% | National | Medium term (2-4 years) |

| Uncertain Digital Services Tax Framework for Foreign Sellers | -0.9% | National, with higher impact on international platforms | Medium term (2-4 years) |

Source: Mordor Intelligence

Urban Congestion & Poor Address Systems Inflate Last-Mile Costs

Traffic bottlenecks lengthen delivery windows by several hours and raise fulfilment charges by up to 30% versus structured markets. Informal addressing leads to failed drops and costly re-routes. Operators are piloting address validation APIs, geo-tagged pick-up lockers and community delivery agents to cut mis-delivery. Micro-fulfilment centres closer to demand clusters reduce travel distance but push up fixed overheads, limiting adoption by smaller vendors. Collaboration between state authorities and postal services aims to standardise addressing, which would materially unlock efficiency across the Nigeria e-commerce market.

High Card-Not-Present Fraud & Charge-backs Escalate Merchant Costs

Fraudulent transactions erode merchant profitability and damage consumer trust. Multi-factor authentication, one-time passwords and tokenisation have lowered attack vectors, yet fraud rates remain above global averages. Payment gateways are investing in behavioural analytics to flag anomalies in real time. Cost-sharing arrangements between issuers and acquirers help absorb charge-back exposure, but smaller sellers still face processing fee penalties that discourage card acceptance.

Segment Analysis

By Business Model: B2B Platforms Unlock Supply-Chain Efficiency

The B2C arm dominates current value flows, holding 87% Nigeria e-commerce market share in 2024. Even so, the B2B channel is scaling at an 18.5% CAGR as wholesalers and informal retailers digitise procurement. Leading start-ups process hundreds of millions of USD in annual transactions, leveraging embedded credit to improve stock rotation for corner shops that still drive most consumer purchases. Service expansion into inventory analytics, demand forecasting and supplier financing makes these platforms integral to the fast-moving consumer goods chain.

Digitalisation compresses procurement costs by roughly one-fifth and cuts delivery lead times from days to hours. As mobile penetration deepens, rural shop owners increasingly use voice-enabled ordering interfaces offered in local languages. Financial-service partners underwrite inventory loans based on real-time sales data, reducing default risk. Over the forecast horizon, scale economics, coupled with deeper monetisation of data, should sustain double-digit growth and progressively rebalance overall revenue composition within the Nigeria e-commerce market.

By Device Type: Mobile Prevails, Multiscreen Matures

Smartphones generated 82% of orders in 2024 and are projected to grow at a 13.2% CAGR. The Nigeria e-commerce market size for mobile reached USD 7.66 billion in 2025 and is set to exceed USD 12.5 billion by 2030. High-speed 4G and impending 5G roll-outs further reinforce mobile’s primacy. Desktop traffic, while shrinking as a share, remains important for research-intensive or high-value purchases such as appliances.

Short-form video, live commerce and in-app messaging are optimised for handheld devices, obliging merchants to prioritise responsive design, compressed imagery and concise copy. Voice search and vernacular chat-bots improve accessibility for first-time shoppers. Concurrently, connected-TV commerce and smart-speaker ordering are emerging in affluent homes, indicating a gradual pivot toward omnichannel engagement. Platforms that maintain design parity across screens are positioned to capture incremental wallet share as device ecosystems proliferate.

By Payment Method: BNPL Widens Affordability Spectrum

Cards led value throughput with 33% share in 2024, yet BNPL volume is climbing rapidly. The Nigeria e-commerce market size for BNPL solutions is expected to surpass USD 1.62 billion in 2025, reflecting mounting preference among millennials seeking frictionless credit. Pay-in-four instalments spread discretionary spending without incurring traditional loan interest, driving up conversion rates for electronics and fashion.

Digital wallets are on track to capture 22% of transaction value by 2027. Telecommunications operators anchor this trend by bundling wallets with data plans and loyalty rewards. Payment orchestration platforms route transactions dynamically to optimise approval rates and lower fees. Cash-on-delivery still appeals in trust-deficit clusters, but its share will erode as agent networks and regulatory safeguards improve perception of digital channels in the Nigeria e-commerce market.

Note: Segment shares of all individual segments available upon report purchase

By B2C Product Category: Beauty and Personal Care Outpaces Core Electronics

Consumer electronics retained the revenue crown with 28% of sales in 2024, buoyed by demand for smartphones, accessories and home entertainment. However, beauty and personal care generated the fastest trajectory with a 16.8% CAGR outlook. Rising disposable income and social-media-driven aesthetics fuel online discovery of skincare, haircare and cosmetics. Local indie brands leverage home-grown ingredients and inclusive shades to differentiate.

Average basket values in beauty remain lower than electronics but frequency is higher, promoting recurring revenue. Subscription models for essential items and influencer-led bundles encourage loyalty. Meanwhile, fashion, grocery and home goods continue to expand as logistics and cold-chain capacity strengthen. Augmented-reality try-on tools for furniture and apparel reduce return rates, enhancing profitability across verticals in the Nigeria e-commerce market.

Geography Analysis

Greater Lagos accounted for nearly 40% of online orders in 2024, supported by 60% broadband penetration and a dense courier network. Abuja and Port Harcourt complete the top urban triad, contributing a further quarter of trade. Collectively, these hubs dominate basket sizes and host the highest concentration of same-day fulfilment services. Smart lockers and bike couriers offset traffic congestion, yet address verification remains a work in progress.

Expansion to secondary cities such as Ibadan, Kano and Enugu is accelerating. Telecom roll-outs, affordable smartphones and agent-enabled cash digitisation lower entry barriers for first-time shoppers. The Nigeria e-commerce market size attributable to northern states is projected to record a 15.3% CAGR to 2030, aided by government and donor programmes that promote female agent participation and vernacular literacy tools. Regional platform variants with lighter apps and USSD ordering further bridge digital divides.

Cross-border commerce layers another dimension on geography. Import-dependent segments rely on coastal ports and Lagos airport logistics hubs to feed inventory. The African Continental Free Trade Area promises smoother customs corridors, potentially expanding addressable demand to diaspora markets and neighbouring economies. However, currency risks and nascent digital tax enforcement make cross-border volume sensitive to macro shifts. Operators that hedge currency exposure and adopt compliant invoicing stand to capture incremental share within the Nigeria e-commerce market.

Competitive Landscape

Nigeria’s digital retail arena remains moderately concentrated. Jumia leads on brand awareness, logistics reach and vendor onboarding, processing 21.3 million orders in 2023. Konga defends share through private-label electronics and marketplace diversification. Temu’s late-2024 entry injected aggressive price competition backed by global sourcing efficiencies. The trio commanded an estimated 54% of gross merchandise value in 2024.

Competitive advantage now hinges on control of fulfilment nodes and payment rails. Jumia invests in proprietary delivery vehicles and pick-up stations, while Temu partners with international couriers to compress lead times for imports. BNPL alliances with fintechs such as CredPal deepen consumer stickiness, whereas embedded wallet ecosystems from telcos create closed-loop funnels for repeat purchase. Data analytics, AI-driven recommendations and real-time inventory sync differentiate user experience and lift conversion across the Nigeria e-commerce market.

Niche challengers carve defensible positions in grocery, pharmaceuticals and B2B trade. OmniRetail leverages embedded credit to lock in informal shopkeepers, whereas GoLemon deploys dark stores for perishable goods. Logistics startups like Shipbubble and Kobo360 monetise route intelligence through software-as-a-service. Strategic partnerships, selective M&A and targeted geographic focus are the dominant manoeuvres as firms pursue scale without overextending capital.

Nigeria E-commerce Industry Leaders

-

Chrisvicmall

-

Zikel Cosmetics International Limited

-

Soso Games Limited

-

BonAmour Nigeria Limited

-

Ajebomarket Limited

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: OmniRetail secured USD 20 million in Series A funding to deepen coverage across West Africa, signalling investor confidence in B2B model scalability.

- April 2025: The Central Bank of Nigeria approved open banking, due to launch on 1 August 2025, enabling secure data sharing that will foster innovative checkout and credit products.

- April 2025: L’Oréal appointed a dedicated head of e-commerce for Nigeria to fast-track online penetration of Garnier and Maybelline, highlighting global brand prioritisation of the channel.

- April 2025: Nigeria formed the National Broadband Alliance to mobilise capital toward its 70% penetration goal, directly uplifting future addressable demand for the Nigeria e-commerce market.

Nigeria E-commerce Market Report Scope

E-commerce, commonly known as electronic commerce, involves any online transaction, including purchasing and selling products and services. Among other advantages, e-commerce provides convenience, borderless transactions, and scalability.

The Nigerian e-commerce market is segmented into B2C e-commerce (beauty and personal care, consumer electronics, fashion and apparel, food and beverages, and furniture and home) and B2B e-commerce. The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| By Business Model | B2C |

| B2B | |

| By Device Type | Smartphone / Mobile |

| Desktop and Laptop | |

| Other Device Types | |

| By Payment Method | Credit / Debit Cards |

| Digital Wallets | |

| BNPL | |

| Other Payment Method | |

| By B2C Product Category | Beauty and Personal Care |

| Consumer Electronics | |

| Fashion and Apparel | |

| Food and Beverages | |

| Furniture and Home | |

| Toys, DIY and Media | |

| Other Product Categories |

By Business Model

| B2C |

| B2B |

By Device Type

| Smartphone / Mobile |

| Desktop and Laptop |

| Other Device Types |

By Payment Method

| Credit / Debit Cards |

| Digital Wallets |

| BNPL |

| Other Payment Method |

By B2C Product Category

| Beauty and Personal Care |

| Consumer Electronics |

| Fashion and Apparel |

| Food and Beverages |

| Furniture and Home |

| Toys, DIY and Media |

| Other Product Categories |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Nigeria e-commerce market?

The Nigeria e-commerce market size reached USD 9.35 billion in 2025 and is forecast to rise to USD 16.83 billion by 2030.

Which business model is growing fastest within Nigerian e-commerce?

The B2B segment is expanding at an 18.5% CAGR as digital platforms streamline wholesale procurement for informal retailers.

How important is mobile commerce in Nigeria?

Smartphones contributed 82% of online orders in 2024, reflecting Nigeria’s mobile-first shopping behaviour.

Why is BNPL gaining traction among Nigerian consumers?

BNPL boosts affordability by splitting payments into instalments, raising average order values by up to 40% and supporting a projected 29.4% CAGR between 2025 and 2030.

What challenges affect last-mile delivery in Nigeria?

Urban congestion, informal addressing and traffic delays inflate delivery costs by up to 30%, prompting investment in address verification and micro-fulfilment hubs.

Who are the leading e-commerce players in Nigeria?

Jumia, Konga and Temu lead in terms of gross merchandise value, jointly accounting for about 54% of the market in 2024.

Page last updated on: July 4, 2025