Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.63 Billion |

| Market Size (2026) | USD 1.68 Billion |

| Market Size (2031) | USD 1.97 Billion |

| Growth Rate (2026 - 2031) | 3.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Floor Covering Market Analysis by Mordor Intelligence

The Netherlands floor covering market size is expected to grow from USD 1.63 billion in 2025 to USD 1.68 billion in 2026 and is forecast to reach USD 1.97 billion by 2031 at 3.22% CAGR over 2026-2031. Renovation activity anchored by government sustainability codes, post-COVID residential upgrades, and steadily rising commercial refurbishments continues to propel demand even as construction cost inflation and labor shortages curb new-build volumes [1]Volkshuisvesting Nederland, “Woningbouw: 90.000 tot 100.000 woningen per jaar tot en met 2030,” volkshuisvestingnederland.nl. Vinyl flooring retains the largest product position, luxury vinyl tile (LVT) logs the swiftest compound growth, and e-commerce channels accelerate as digital-first purchasing reshapes consumer journeys. Commercial refurbishments emphasize wellness, acoustic performance, and low-emission certification, expanding opportunities beyond the dominant residential segment. Suppliers differentiate through circular-economy programs, sensor-ready constructions, and documented environmental performance that collectively offset margin pressure caused by raw-material volatility. Regulatory alignment with EU green-building targets magnifies premium demand, while government subsidies reinforce the adoption of recycled-content products.

Key Report Takeaways

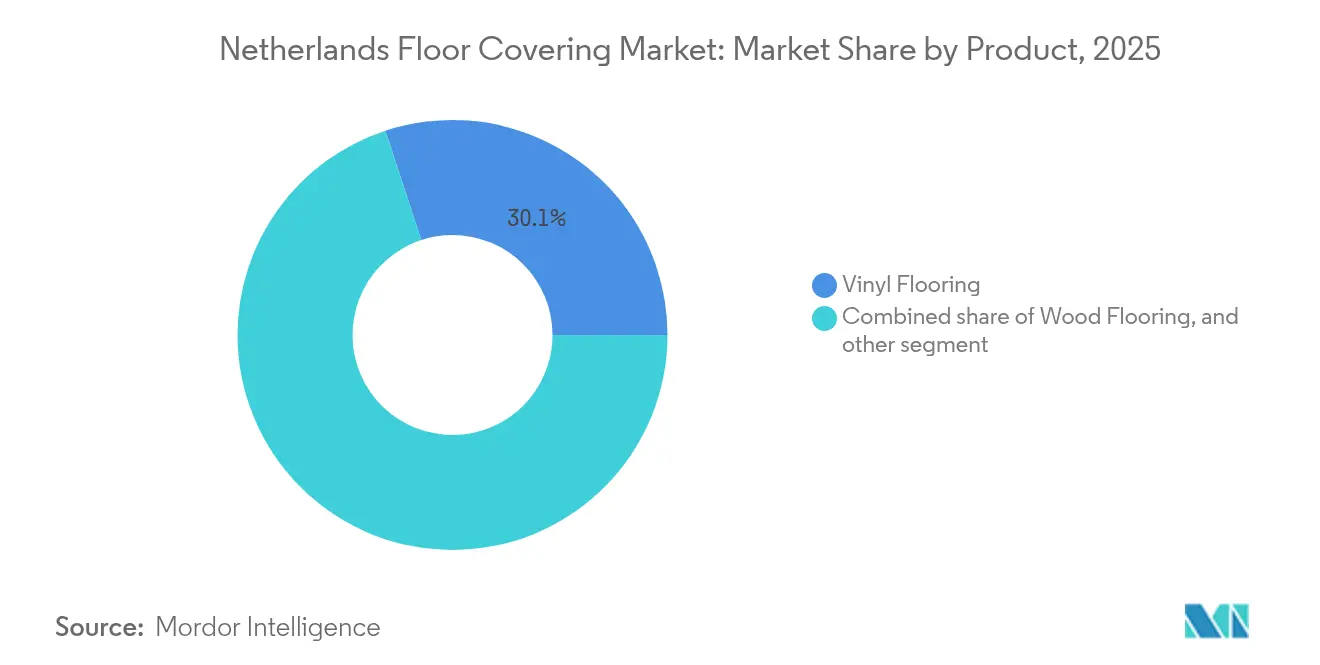

- By product category, vinyl flooring led with 30.05% of the Netherlands floor covering market share in 2025; luxury vinyl tile is projected to expand at a 6.78% CAGR through 2031.

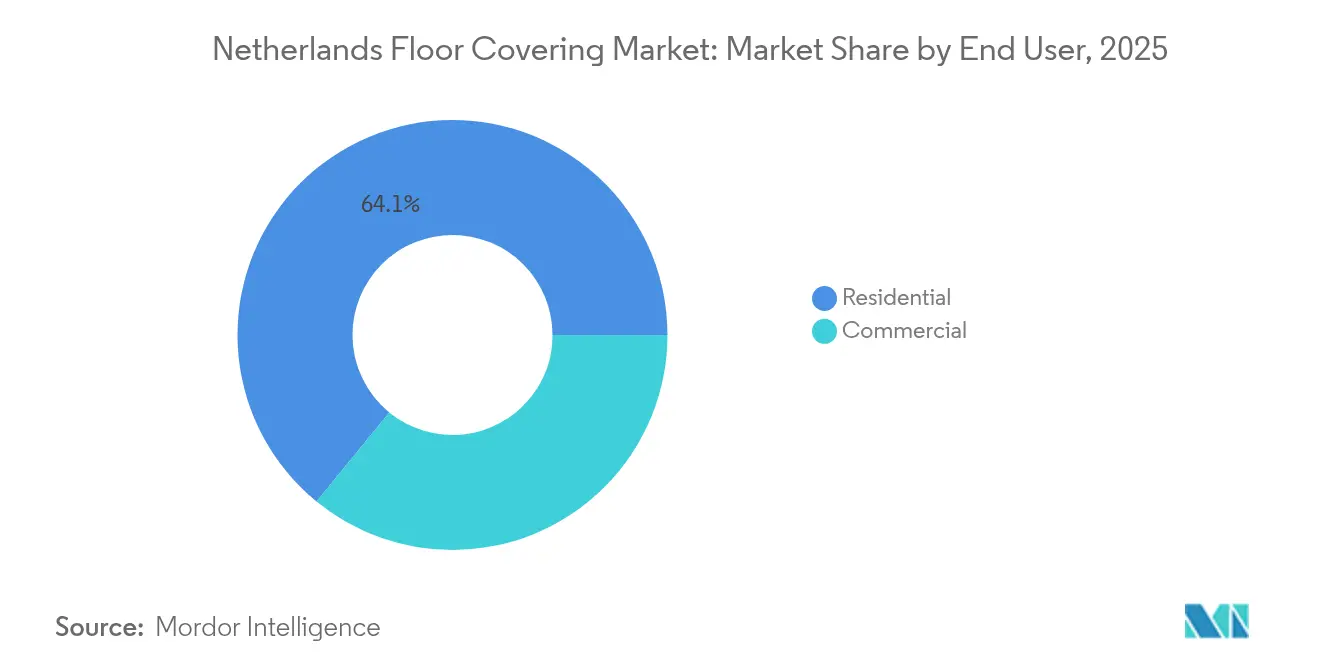

- By end user, the residential segment held 64.10% of the Netherlands floor covering market share in 2025, while commercial applications record the highest projected CAGR at 5.07% through 2031.

- By distribution channel, specialty stores accounted for a 36.45% share of the Netherlands floor covering market size in 2025; online channels are advancing at a 9.35% CAGR to 2031.

- By geography, Western Netherlands captured 37.60% of the Netherlands floor covering market size in 2025; Northern Netherlands is forecast to be the fastest-growing region with a 5.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Netherlands Floor Covering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability-linked building codes accelerate floor upgrades | +0.8% | National, early gains in Western Netherlands | Medium term (2-4 years) |

| Rapid post-COVID renovation boom in residential sector | +0.6% | National, urban focus | Short term (≤ 2 years) |

| Growth in commercial refurbishments (retail & offices) | +0.5% | Western and Southern Netherlands | Medium term (2-4 years) |

| Government subsidies for circular construction materials | +0.4% | National | Long term (≥ 4 years) |

| Smart-home integration driving sensor-ready flooring | +0.3% | Western Netherlands, expanding nationally | Long term (≥ 4 years) |

| Rising adoption of modular flooring systems | +0.2% | National, commercial focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sustainability-Linked Building Codes Accelerate Floor Upgrades

The MilieuPrestatie Gebouwen (MPG) thresholds tightened in 2025, making flooring a focal point for lifecycle impact reductions. Developers prioritize certified low-emission and high-recycled-content products to sidestep permitting delays. EU Taxonomy limits on formaldehyde push manufacturers toward clean-chemistry binders [2]European Commission, “EU Ecolabel for wood-, cork- and bamboo-based floor coverings,” ec.europa.eu. BREEAM-NL and GPR credits reward documented environmental performance, establishing a premium tier for fully traceable materials. Retrofit projects accelerate as building owners race to meet 2026 compliance dates, generating near-term replacement demand. The combined regulatory momentum extends product lifecycles into circular take-back schemes that further strengthen suppliers with closed-loop capabilities.

Rapid Post-COVID Renovation Boom in Residential Sector

ISDE subsidies, expanded in 2025, subsidize energy-saving measures that often include floor upgrades, especially underfloor-heating-compatible surfaces. Limited housing inventory and high mortgage rates keep families in place and willing to invest in comfort enhancements. LVT, waterproof laminate, and engineered wood with acoustic underlays top shopping lists. Consumers request recycled content and end-of-life take-back options, aligning home improvements with personal sustainability values. Aging housing stock in cities like Amsterdam and Rotterdam amplifies demand for easy-install systems that minimize disruption. This trend fuels steady volume for specialty retailers and e-commerce alike as homeowners increasingly research and order products online.

Growth in Commercial Refurbishments (Retail & Offices)

Office occupancy stabilizes, and retailers reinvent physical stores, triggering renovation that emphasizes acoustics, indoor-air quality, and biophilic design. Flexible work patterns require modular carpet tiles and loose-lay LVT that can shift with changing layouts. Healthcare and education facilities refresh surfaces to meet stringent hygiene protocols, widening commercial demand. A construction outlook of 1.6% growth in 2025 supports financing for interior investments [3]Atradius, “Nederlandse bouwsector groeit naar verwachting met 1,6 procent in 2025,” atradius.nl. Longer commercial replacement cycles favor suppliers able to document durability and provide post-installation maintenance guidance. International brands with Dutch distribution hubs benefit from shorter lead times when project schedules tighten.

Government Subsidies for Circular Construction Materials

The National Circular Economy Programme 2023-2030 earmarks flooring for extended producer‐responsibility pilots and funds material innovation through DUMAVA grants totaling EUR 405 million (USD 422.58 million). Revised MIA/Vamil tax lists now exclude many legacy surfaces, steering buyers toward products with verifiable recycled content. Suppliers expand take-back logistics, integrate recycled fillers, and develop disassembly-friendly click systems to secure public-sector and ESG-driven private contracts. Circular credentials increasingly serve as pre-qualification criteria, aligning market incentives with regulatory goals. Early adopters gain export potential as EU states emulate Dutch circular guidelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw-material prices (wood, PVC, stone) | -0.7% | National, supply-chain impacts | Short term (≤ 2 years) |

| Stricter VOC-emission limits increase compliance costs | -0.4% | National, EU aligned | Medium term (2-4 years) |

| Trade-talent shortage lengthens installation lead-times | -0.5% | National, acute in urban areas | Medium term (2-4 years) |

| Intense competition pressures margins | -0.3% | National, commodity segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Material Prices (Wood, PVC, Stone)

Energy shocks, shipping congestion through the Red Sea, and climate-related supply disruptions caused sharp price swings in 2024. Mohawk Industries cited persistent headwinds that forced selective price increases during Q1 2025. Potential tariffs on Chinese PVC threaten additional cost layers for LVT and SPC imports, prompting European sourcing shifts. Contractors struggle to finalize bids, leading to postponed tenders and renegotiated budgets. Manufacturers focus on value-added ranges where pricing flexibility is higher and on recycled-PVC compounds that hedge virgin-material volatility. Raw-material risk also accelerates R&D into bio-based alternatives, diversifying supply chains.

Trade-Talent Shortage Lengthens Installation Lead-Times

Dutch construction continues to report more vacancies than qualified installers [4]Centraal Bureau voor de Statistiek, “Labour shortage in construction industry remains high,” cbs.nl. Stricter employment contracts raise costs, while specialized smart-floor and radiant-heating installations demand new skills. Project timelines extend, encouraging developers to pre-fabricate components and favor user-friendly click systems. Suppliers respond with training academies and digital installation guides, building loyalty among contractors. The labor gap also spurs uptake of adhesive-free solutions that cut on-site steps, improving overall project economics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Vinyl Dominance Drives Market Evolution

Vinyl flooring commanded 30.05% of the Netherlands floor covering market share in 2025; ongoing water-resistance and design flexibility keep the category pivotal to both residential and commercial upgrades. Luxury vinyl tile leads growth at a 6.78% CAGR through 2031, driven by high-definition printing, rigid cores that resist telegraphing, and embossed-in-register textures that mimic hardwood and stone. The Netherlands floor covering market size benefits from PVC-free flexible tiles and bio-attributed resins, scale, demonstrating lower embodied carbon without sacrificing performance. Wood flooring retains premium cachet—particularly engineered planks designed for underfloor heating—yet forestry constraints and price volatility moderate expansion. Ceramic tiles capitalize on commercial renovations and energy-efficient radiant systems, while waterproof laminates challenge entry-level LVT by offering scratch resistance and improved acoustics.

Hybrid innovations such as cork-backed rigid vinyl, carbon-negative linoleum, and fully recyclable polypropylene composites reflect regulatory pressure and consumer eco-awareness. Carpet faces declining residential uptake post-pandemic, yet holds in hospitality and offices where modular tiles deliver design flexibility and circular take-back simplicity. Stone and terrazzo remain niche but command attention in luxury multi-family lobbies and heritage restorations. Continuous product R&D around antimicrobial coatings, click installations, and cradle-to-grave certification ensures the Netherlands floor covering market remains dynamic even as overall adoption patterns mature.

By End User: Commercial Acceleration Reshapes Demand

The residential domain held 64.10% of the Netherlands' floor covering market share in 2025 as households leveraged energy-efficiency subsidies and prioritized home comfort during housing shortages. LVT, waterproof laminate, and engineered oaks compatible with heat pumps remain favored, while sensor-ready underlays gain early traction among tech-savvy buyers. Homeowners increasingly evaluate Environmental Product Declarations and participate in retailer take-back schemes, showcasing a value shift toward long-term sustainability. Specialist retailers and online influencers guide product selection, reinforcing premiumization trends within the Netherlands floor covering industry.

Commercial applications outpace overall growth at a 5.07% CAGR to 2031 as offices, retail, and mixed-use facilities upgrade interiors to attract talent and foot traffic. Productivity and acoustic well-being goals drive the specification of low-VOC, modular surfaces. Healthcare and education segments adopt seamless safety vinyl and carbon-negative linoleum to satisfy strict hygiene and lifecycle cost benchmarks. Facility managers increasingly require documentation of circular practices—turnkey recycling, repair warranties, and replacement guarantees—that prioritize suppliers with established end-of-life solutions. This alignment of wellness, durability, and sustainability multiplies cross-segment appeal for brands delivering integrated, certifiable portfolios.

By Distribution Channel: Digital Disruption Accelerates

Specialty stores retained a 36.45% share of the Netherlands floor covering market size in 2025 by offering design advisory, installer coordination, and exclusive collections that safeguard margins. Showrooms deploy AR visualization and color-matching tools, enhancing the in-store experience. Online channels post a 9.35% CAGR as consumers embrace click-to-deliver convenience, detailed product data sheets, and virtual room renderings. DIY enthusiasts and small contractors rely on digital marketplaces for rapid pricing and logistical visibility, compelling manufacturers to hone drop-ship capabilities.

Home centers still move large volumes of entry-price laminate and sheet vinyl, yet face margin squeeze from warehouse-style retailers with integrated logistics platforms. Direct-to-consumer models, subscription-based floor-maintenance kits, and manufacturer flagship webshops broaden the “Other Distribution” category, trimming middle-layer costs. Cross-channel buying journeys—research online, pick up in-store—blur channel distinctions, pushing every distributor to invest in omnichannel support and last-mile tracking.

Geography Analysis

The Netherlands floor covering market demonstrates pronounced regional contrasts linked to population density, construction pipelines, and infrastructure constraints. Western Netherlands dominated with 37.60% of the Netherlands' floor covering market size in 2025. Dense urban fabric in Amsterdam, Rotterdam, and The Hague supports a constant renovation baseline as property owners refresh interiors to preserve asset value. Port proximity lowers import logistics costs, facilitating a broad assortment of international brands. Grid-congestion challenges hamper some new builds, yet retrofit activity offsets volume gaps by targeting building-services upgrades that typically include flooring replacement. Multinational headquarters and government ministries amplify commercial demand for low-VOC, circular-ready surfaces compliant with corporate ESG frameworks.

Northern Netherlands posts the fastest 5.12% CAGR through 2031, buoyed by infrastructure expansion, renewable-energy projects, and affordable land that attract remote workers. Residential starts rise in provinces like Groningen and Friesland, driving uptake of modular LVT and click-laminate suitable for self-installers. Provincial grants incentivize bio-based building materials, positioning circular linoleum and cork composites favorably. Nitrogen-emission litigation threatens a share of planned housing, yet policymakers remain intent on redirecting national targets northward to relieve pressure on densely populated Randstad municipalities.

Eastern and Southern Netherlands together deliver steady, mid-single-digit growth. Industrial clusters in Gelderland and Brabant specify heavy-duty epoxy and antistatic vinyl for manufacturing environments, diversifying product mix. Mid-rise apartment refurbishments in Arnhem, Nijmegen, and Eindhoven favor waterproof laminate and hybrid cork-vinyl planks that balance cost and comfort. Cross-border e-commerce with Germany and Belgium expands distributor catchment areas, prompting regional warehouses to stock wider assortments. Universities and hospitals in Twente and Limburg upgrade to low-emission resilient floors, echoing national healthcare investment patterns. Balanced residential and commercial pipelines protect these regions from sharper cyclical swings seen in concentrated urban cores.

Competitive Landscape

The Netherlands floor covering market remains moderately fragmented. Global leaders—Tarkett, Mohawk Industries (Unilin), and Forbo—capitalize on expansive assortments, recycling networks, and advanced design technologies to win high-specification tenders. Domestic retailers such as Kwantum and Leen Bakker maintain strong brand recognition and leverage omnichannel capabilities to engage price-sensitive consumers. Sustainability credentials represent a decisive differentiator: Tarkett’s Waalwijk facility processes post-consumer carpet and vinyl, Forbo markets carbon-negative linoleum, and Interface pursues “Mission Zero” targets that resonate with institutional buyers.

Technology investments intensify rivalry; digital printing enables custom visuals at smaller minimums, while PVC-free backings address regulatory concerns. Warehouse-style outlets and direct-to-consumer startups erode traditional distributor margins, spurring incumbents to streamline supply chains and offer value-added services such as on-site moisture testing and acoustic modeling. Heightened VOC thresholds and looming extended-producer-responsibility rules raise compliance costs, encouraging alliances among mid-tier suppliers to share testing labs and recycling logistics. Continuous product and service differentiation counterbalances pricing pressure and ensures dynamic competition within the Netherlands floor covering industry.

Netherlands Floor Covering Industry Leaders

Tarkett S.A.

Forbo Flooring Systems

Interface, Inc.

Unilin (Quick-Step

Mohawk Industries (Pergo / IVC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Tarkett published its 2024 Universal Registration Document, reporting a 47% reduction in Scope 1 & 2 emissions versus 2019 and an expanded ReStart take-back program in 29 countries, underlining its strategic commitment to circularity. The document highlights the Waalwijk recycling hub, which processes both carpet tiles and vinyl waste streams for reintroduction into new products, positioning the facility as a model for EU circular-economy targets.

- January 2025: The parent company of Dutch retailers Kwantum and Leen Bakker returned to profitability with a EUR 19.5 million (USD 20.35 million) net result for 2023, reversing the prior year’s loss. Management credited cost optimization, online-channel growth, and stable post-pandemic home-furnishing demand for the turnaround, signaling renewed investment capacity in store refurbishments and digital infrastructure.

- November 2024: Forbo Holding announced leadership changes with Bernhard Merki proposed as new Chairman, reiterating its focus on carbon-negative linoleum and phthalate-free vinyl. The governance update aligns with a broader sustainability roadmap that includes increased renewable energy use across European factories and expanded digital-service offerings for architects.

- May 2024: Mohawk Industries detailed persistent raw-material inflation and competitive pricing pressure in its Q1 2025 results, noting selective price adjustments to offset costs. The company emphasized continued investment in SPC rigid-core capacity and water-resistant laminates aimed at European consumers, prioritizing durability and affordability.

Netherlands Floor Covering Market Report Scope

The report provides a detailed study of the variations in the floor covering market's growth trends. The report also provides a competitive landscape covering market shares, with detailed profiling of major revenue-contributing companies. The market is segmented by product, end user, and distribution channel.

Segmentation by Product

| Carpet and Area Rugs |

| Wood Flooring |

| Ceramic Tiles Flooring |

| Laminate Flooring |

| Vinyl Flooring |

| Stone Flooring |

| Other Products |

Segmentation by End User

| Commercial |

| Residential |

Segmentation by Distribution Channel

| Home Centers |

| Flagship Stores |

| Specialty Stores |

| Online Stores |

| Other Distribution Channels |

Segmentation by Geography

| Western Netherlands |

| Eastern Netherlands |

| Northern Netherlands |

| Southern Netherlands |

| Segmentation by Product | Carpet and Area Rugs |

| Wood Flooring | |

| Ceramic Tiles Flooring | |

| Laminate Flooring | |

| Vinyl Flooring | |

| Stone Flooring | |

| Other Products | |

| Segmentation by End User | Commercial |

| Residential | |

| Segmentation by Distribution Channel | Home Centers |

| Flagship Stores | |

| Specialty Stores | |

| Online Stores | |

| Other Distribution Channels | |

| Segmentation by Geography | Western Netherlands |

| Eastern Netherlands | |

| Northern Netherlands | |

| Southern Netherlands |

Key Questions Answered in the Report

How large is the Netherlands floor covering market in 2026?

The Netherlands floor covering market size reached USD 1.68 billion in 2026.

What growth rate is projected for Dutch flooring demand?

The market is forecast to grow at a 3.22% CAGR, reaching USD 1.97 billion by 2031.

Which product category leads sales in the Netherlands?

Vinyl flooring is the largest segment, while luxury vinyl tile shows the swiftest growth momentum.

Why are online channels expanding so quickly?

Improved visualization tools, rapid delivery, and digital-first buying habits support a 9.35% CAGR for online distribution through 2031.

Which region is expected to grow the fastest?

Northern Netherlands is projected to post a 5.12% CAGR owing to infrastructure investment and new housing developments.

How are sustainability regulations influencing supplier strategy?

Tightened MPG thresholds and circular-economy subsidies push manufacturers to adopt recycled content, low-VOC formulations, and take-back programs to remain specification-eligible.

Page last updated on: