Naval Vessel MRO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 63.27 Billion |

| Market Size (2031) | USD 73.66 Billion |

| Growth Rate (2026 - 2031) | 3.09% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Naval Vessel MRO Market Analysis by Mordor Intelligence

The naval vessel MRO market size stands at USD 61.38 billion in 2025. The naval vessel MRO market size in 2026 is estimated at USD 63.27 billion, growing from 2025 value of USD 61.38 billion with 2031 projections showing USD 73.66 billion, growing at 3.09% CAGR over 2026-2031. Sustained modernization programs, higher operational tempos in contested waters, and shifting toward performance-based logistics (PBL) contracts continue to anchor demand. Nuclear-powered vessel upkeep and dry-dock overhauls remain the most lucrative niches as they require specialized infrastructure and deep technical expertise, locking in premium pricing. Asia-Pacific accounts for the largest regional spend, propelled by China’s rapid fleet expansion and allied counter-responses, while Europe is accelerating fastest on the back of renewed NATO commitments. Supply-chain fragility and skilled-labor shortages pose measurable headwinds, yet digital twin analytics and additive manufacturing mitigate downtime and unlock incremental savings.

Key Report Takeaways

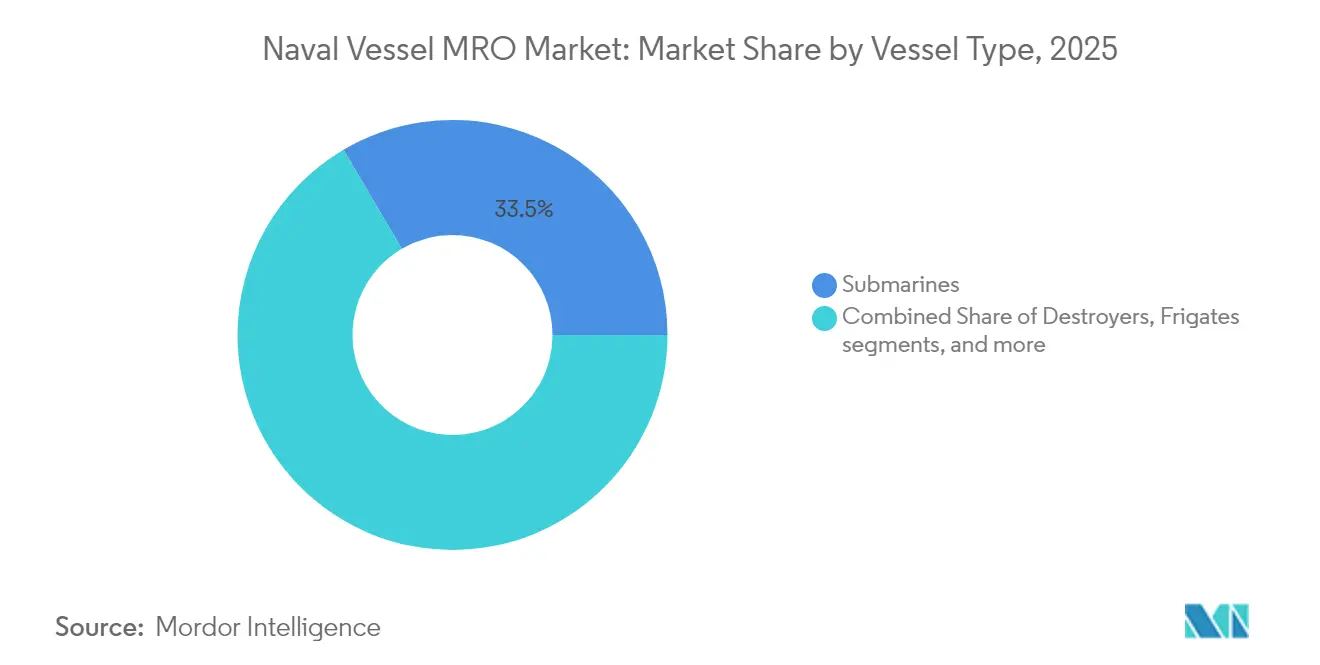

- By vessel type, submarines led the naval vessel MRO market share with 33.46% in 2025; frigates are forecasted to expand at a 5.05% CAGR through 2031.

- By propulsion type, nuclear-powered vessels captured 53.21% of the naval vessel MRO market size in 2025 and are projected to grow at a 4.12% CAGR through 2031.

- By MRO type, dry-dock services accounted for 38.57% of the naval vessel MRO market size in 2025; modification and upgrade services are advancing at a 3.60% CAGR to 2031.

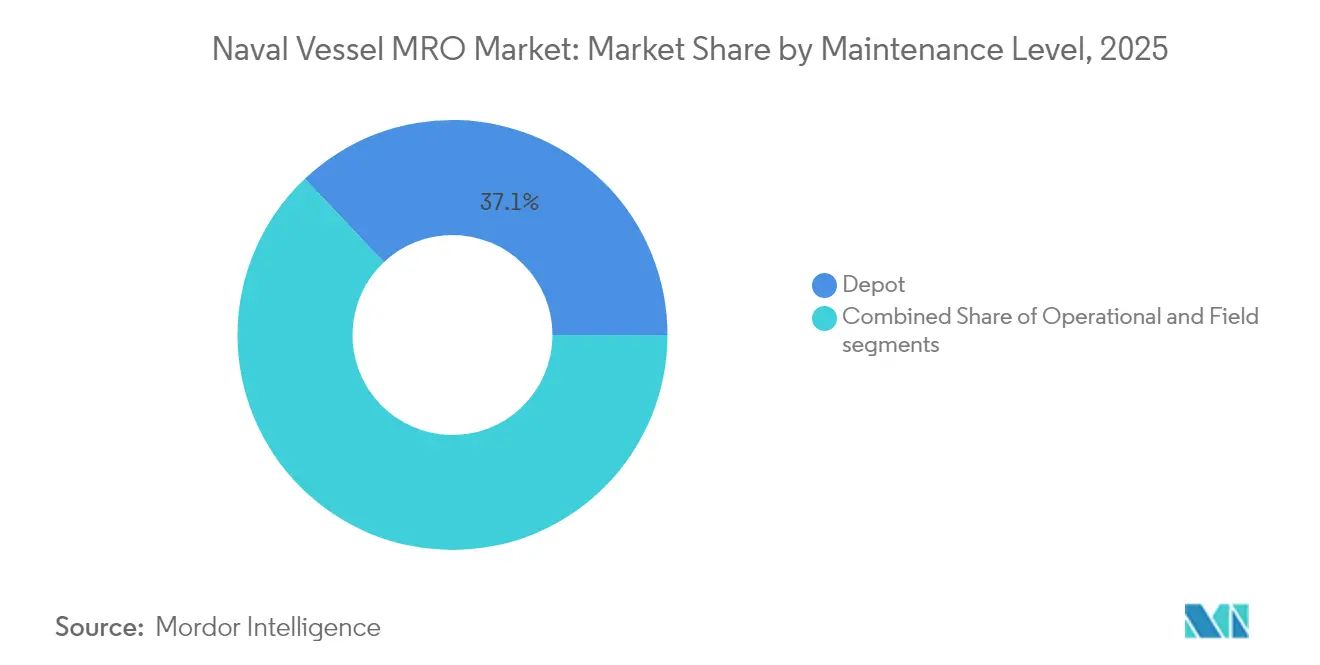

- By maintenance level, depot-level work controlled 37.05% of the naval vessel MRO market size in 2025, rising at a 4.66% CAGR through 2031.

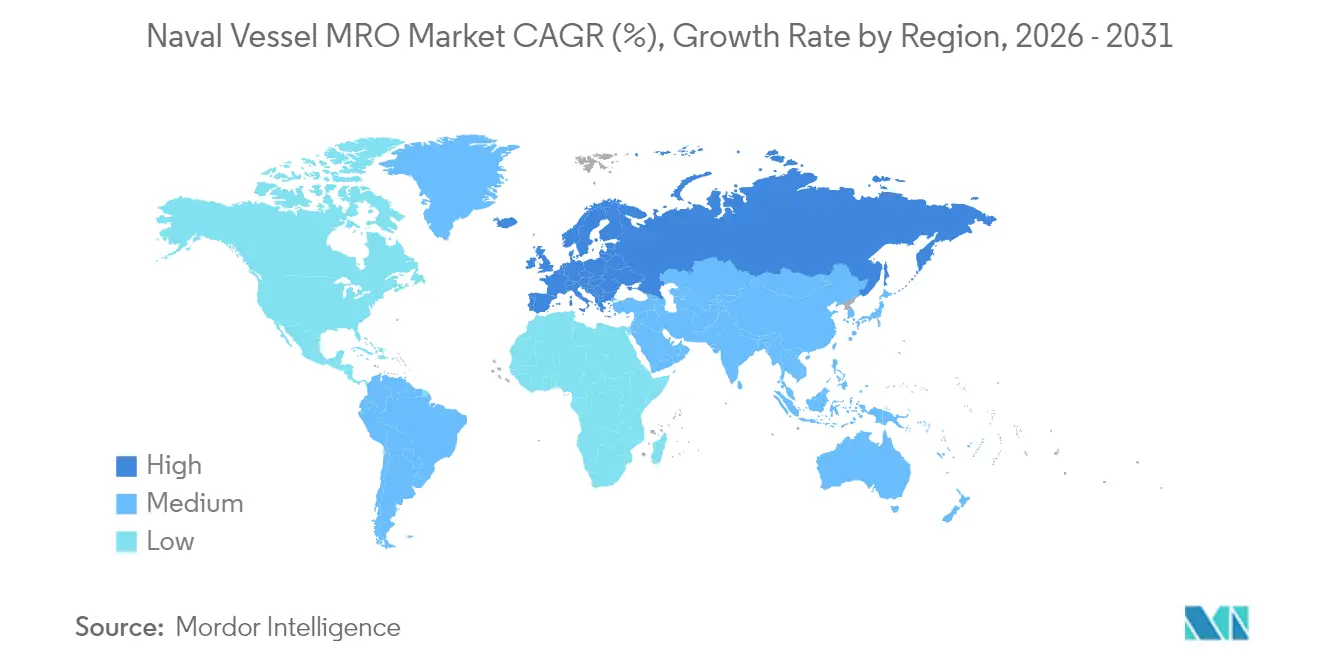

- By geography, Asia-Pacific held a 37.14% share of the naval vessel MRO market in 2025, while Europe registered the highest regional CAGR at 3.88% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Naval Vessel MRO Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet-modernization programs | +0.80% | Global; highest in Asia-Pacific and Europe | Medium term (2-4 years) |

| Life-extension of legacy fleets | +0.60% | North America and Europe; spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Rising maritime-security tensions | +0.50% | Global; focus on Indo-Pacific and Middle East | Short term (≤ 2 years) |

| Adoption of PBL contracts | +0.40% | North America and Europe; expanding to Asia-Pacific | Medium term (2-4 years) |

| Digital-twin based predictive MRO | +0.30% | North America and Europe; emerging in Asia-Pacific | Medium term (2-4 years) |

| Additive-manufactured spares | +0.20% | North America and Europe; pilot projects in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fleet-Modernization Programs

Nationwide upgrade plans are reshaping the naval vessel MRO market demand as governments aim to stretch capability rather than merely expand fleet count. The Philippines’ USD 35 billion modernization drive and Turkey’s three-year fleet enhancement initiative earmark sizable shares for maintenance infrastructure and platform upgrades rather than for acquisition only. Similar strategies in Denmark and Australia show that mid-tier navies can secure disproportionate capability gains by funding refits, overhauls, and modular upgrades. Submarine hull-life extensions add 10-15 years of service at near one-quarter of new-build cost, generating durable MRO revenue. Predictability improves because phased work packages allow contractors to plan labor and inventory well in advance, narrowing schedule slippage.

Life-Extension of Legacy Fleets

Keeping older ships battle-ready has moved from thrift to necessity as next-generation hulls arrive late. The US Navy cruiser overhaul program and the Royal Navy Type 23 frigate life-extension effort illustrate how navies capture 70-80% of modern capability for only 15-25% of replacement cost. Enhanced coatings, structural health monitoring, and mid-life combat-system swaps tackle fatigue and obsolescence while predictive analytics tighten inspection intervals. Growing reliance on legacy vessels stabilizes demand for depot-level refits that independent yards cannot easily replicate, bolstering premium pricing for incumbent contractors.

Rising Maritime-Security Tensions

Heightened friction in the Red, South China, and Eastern Mediterranean keeps task groups at sea longer. The USS Dwight D. Eisenhower flew over 13,000 sorties during a seven-month deployment that typically lasts six, sharply compressing overhaul windows and spiking spare-part consumption.[1]US Naval Institute, “IKE Carrier Strike Group and the Red Sea Crisis,” usni.org Allied responses—from Japan’s destroyer-escort transfers to the Philippines to Australia’s fleet-doubling plan—multiply regional demand for propulsion overhauls, combat-system checks, and electronic-warfare calibrations. The result is that workload lifts utilization across dry-dock slots and component-repair lines, sustaining the naval vessel MRO market even when new-build cycles flatten.

Adoption of PBL Contracts

Performance-based logistics models redistribute availability risk to contractors in return for steadier revenue and freedom to innovate. The US Navy’s USD 1.2 billion P-8A Poseidon support deal and StandardAero’s USD 315 million T56 engine agreement show how navies now pay for predetermined readiness levels rather than individual work orders. Contractors respond by embedding digital twins, additive manufacturing, and condition-based maintenance into service delivery, driving down lifecycle cost while meeting uptime metrics. PBL penetration exceeds 60% in new US programs and is spreading through European procurement frameworks.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dry-dock slot overruns and costs | −0.4% | Global; most acute in North America and Europe | Medium term (2-4 years) |

| Skilled-labor shortages | −0.3% | North America and Europe; emerging in Asia-Pacific | Long term (≥ 4 years) |

| Cyber-risk to connected shipyards | −0.2% | Global; higher in digitally advanced regions | Short term (≤ 2 years) |

| Green-compliance waste-disposal cost | −0.1% | Europe and North America; expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Dry-Dock Slot Overruns and Costs

Aging facilities and project creep push overhaul budgets well above plan. Pearl Harbor’s dry-dock modernization ballooned from USD 6.1 billion to USD 16 billion, while Portsmouth Naval Shipyard costs quadrupled, blocking capacity for other urgent work. The Shipyard Infrastructure Optimization Program injects USD 21 billion, yet it cannot eliminate near-term gaps that delay submarine refits by 12-18 months. Commercial yards often refuse naval contracts because overruns jeopardize profitability, further tightening the bottleneck.

Skilled-Labor Shortages

Demographics and high attrition shrink the talent pool for welding, pipe-fitting, and nuclear maintenance. Hampton Roads alone faces a 10,000-person shortfall that may quadruple by 2030, while European yards wrestle with limited cross-border mobility post-Brexit. Recruitment pipelines produce fewer than 15,000 qualified hands annually against a requirement for 174,000 over the decade. Labor scarcity inflates wage bills, stretches delivery dates, and curtails expansion plans, moderating naval vessel MRO market growth despite ample funding.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vessel Type: Submarines Drive Strategic Deterrence

Submarines accounted for 33.46% of the 2025 naval vessel MRO market, reflecting their nuclear-propulsion complexity and deterrence value that anchor multi-year service contracts. High regulatory barriers restrict competition and support premium rates. Frigates represent the fastest-growing slice at 5.05% CAGR thanks to their role in distributed surface operations and relatively quicker build cycles that soon enter sustainment phases. Destroyers and corvettes sit mid-pack; the former benefit from Aegis-system maintenance, while the latter attract emerging littoral navies seeking budget-friendly patrol craft.

Subsurface platforms require extensive reactor refueling, acoustic signature checks, hull pressure tests, and lock-in depot-level workloads. Frigate programs leverage modular combat-system blocks, simplifying mid-life upgrades and enticing navies to invest in incremental capability paths instead of fresh hulls. Digital twin pilots under Spain’s ISOPRENE project have demonstrated 15-20% cuts in unscheduled downtime for both vessel classes, pointing toward broader adoption over the forecast period.

By MRO Type: Dry-Dock Services Dominate Complex Maintenance

Dry-dock work held 38.57% of the naval vessel MRO market in 2025 due to statutory hull inspections, shaft-line replacements, and propulsion-system overhauls that mandate docking. The segment enjoys steady visibility because mandatory periodicity supports multi-year master schedules. Modification and upgrade services are growing 3.60% annually as navies retrofit sensors, weapons, and electronic-warfare suites rather than wait for new builds.

Additive manufacturing is reshaping component repair economics. Metal 3D printers on the USS Bataan already produce certified spares at sea, cutting logistics lag and freeing dock space for heavier tasks. PBL frameworks incentivize suppliers to invest further in this capability, as faster part turnarounds boost contract performance metrics.

By Maintenance Level: Depot-Level Services Command Premium Pricing

Depot-level work comprised 37.05% of the 2025 naval vessel MRO market and is rising at 4.66% CAGR, the fastest among maintenance levels, because advanced combat systems exceed organic ship-crew skill sets. Nuclear-qualified trades require years of clearance and schooling, tightening supply and elevating hourly rates. Digital-twin analytics refine yard schedules by predicting wear patterns, which lowers idle time and maximizes capital-intensive dock usage.

Intermediate maintenance fills the capability gap between crews and depots, especially for emergent repairs during extended deployments. Organizational maintenance remains essential yet budget-capped; navies prefer to reallocate complex work to contractors who guarantee uptime under PBL arrangements.

By Propulsion Type: Nuclear-Powered Vessels Drive Premium Demand

Nuclear platforms captured 53.21% of the 2025 naval vessel MRO market and are projected to grow at a 4.12% CAGR, outpacing conventional propulsion due to their strategic priority and stringent safety standards. Only a handful of firms possess the requisite clearances, facilities, and tooling, which creates high entry barriers and durable margins. Diesel and gas-turbine vessels fill coastal patrol and rapid-response roles, benefiting from broader supplier bases but lacking the pricing power of nuclear-powered programs.

Supply-chain fragility remains acute for nuclear segments. General Dynamics Electric Boat pushed delivery schedules out by up to 16 months after critical component delays, illustrating dependency on specialized vendors. Nuclear maintenance budgets remain resilient despite these challenges because strategic imperatives rarely face cuts.

Geography Analysis

Asia-Pacific held 37.14% of the 2025 naval vessel MRO market spending, anchored by China’s fleet growth toward 435 ships by 2030 and allied counter-moves such as Australia’s plan to double its surface force. Shipbuilding powerhouses South Korea and Japan offer overflow dock capacity; Hanwha Ocean became the first Korean yard to win US Navy repair work, underscoring deeper allied collaboration.

Europe is the fastest-growing region at 3.88% CAGR as NATO members lift defense outlays to at least 2% of GDP. Denmark’s large-scale fleet expansion, France’s Tourville submarine commissioning, and Greece’s USD 27 billion rearmament funnel fresh hulls into sustainment pipelines. Turkey’s EUR 350 million Aksaz Naval Base upgrade further broadens regional maintenance options and reflects wider Mediterranean security concerns.

North America sustains robust but stable demand as the US Navy balances modernization with aging-yard constraints. Emergency supplements of USD 5.7 billion for submarine labor and a USD 40.1 billion annual shipbuilding budget highlight fiscal commitment, yet projected force levels drop to 283 ships by 2027 before rebuilding toward 381 by 2054. South America and the Middle East/Africa remain smaller contributors, though programs like ZAR 1.4 billion (USD 78.90 million) submarine refit point to gradual upticks.

Competitive Landscape

The naval vessel MRO market is concentrated in a handful of defense primes that control nuclear-qualified facilities, security clearances, and specialized labor. Huntington Ingalls Industries (HII) tops the field with a USD 47.1 billion order backlog and the recent W International acquisition that expands Newport News Shipbuilding's capacity for AUKUS submarines.[3]Robert W. Brauchle, “HII to Strengthen Nuclear-Powered Submarine Supply Chain,” HII, hii.com General Dynamics Electric Boat remains pivotal but has eased production cadence due to component shortages, spotlighting supplier dependencies.

Strategic partnerships widen capacity and share risk. HII's 2025 memorandum with Hyundai Heavy Industries seeks to blend US nuclear expertise with South Korean throughput, potentially doubling Aegis destroyer output. Contractors differentiate through technology: the Spanish SOPRENE digital-twin project cut unscheduled downtime 15–20%, while US Navy additive-manufacturing pilots aim for USD 250 million annual savings.

Naval Vessel MRO Industry Leaders

General Dynamics Corporation

Lockheed Martin Corporation

BAE Systems plc

Huntington Ingalls Industries, Inc.

Naval Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The US Navy’s FY 2025 shipbuilding plan sought 381 battle-force ships and 134 unmanned vessels by 2054, backed by a USD 40.1 billion annual budget.

- March 2025: Huntington Ingalls Industries clinched a USD 147 million deal to provide the Navy with combat training services, both shipboard and shore-based. The Mission Technologies division has entered a five-year task order with the Navy. The division will deliver engineering support for training systems at the Naval Surface Warfare Center's Dahlgren Division.

- February 2025: Abu Dhabi Ship Building (ADSB), part of the EDGE Group and a regional frontrunner in designing, constructing, and maintaining naval and commercial vessels, inked a Memorandum of Understanding (MoU) with Intermarine (IMMSI Industrial Group—IMS.MI). Intermarine is a global authority that crafts minehunter vessels for mine warfare, seabed surveillance, survey ships, patrol boats, and fast ferries. The two entities aim to explore collaborative avenues and bolster mutual business growth.

- November 2024: General Dynamics NASSCO–Norfolk secured a contract for the maintenance, modernization, and repair of the USS Porter (DDG 78). This acquisition encompasses all necessary labor, supervision, equipment, production, testing, facilities, and quality assurance to prepare for and execute the Chief of Naval Operations (CNO) Availability, focusing on essential modernization and maintenance programs.

- November 2024: BAE Systems plc clinched a USD 212 million contract to maintain, modernize, and repair the Navy's San Antonio-class amphibious transport dock, the USS Green Bay (LPD 20), based in San Diego. BAE Systems will deliver labor, supervision, equipment, production, testing, facilities, and quality assurance to back the Chief of Naval Operations' critical modernization and maintenance programs. The project is slated for completion by October 2026.

- October 2024: BAE Systems plc clinched two contracts from the US Navy, totaling approximately USD 222.6 million, to deliver maintenance, repair, and modernization services for an Arleigh Burke-class guided-missile destroyer and a multipurpose amphibious assault ship. The contracts encompass all necessary labor, equipment, production, supervision, testing, quality assurance, and facilities to support essential maintenance, repair, and modernization initiatives.

Global Naval Vessel MRO Market Report Scope

The maintenance, repair, and overhaul operations conducted periodically on naval vessels are crucial for sustaining and extending the life of a ship. It involves all the functions related to the maintenance, overhaul, routine checks, inspection, repair, and modification of the vessel and its components. Performing MRO services helps ensure the safety and worthiness of naval vessels.

The market for naval vessel maintenance, repair, and overhaul (MRO) is segmented based on vessel type into submarines, frigates, corvettes, aircraft carriers, destroyers, and other vessel types. The other vessel types segment includes amphibious warfare ships, littoral combat ships, cruisers, mine countermeasure ships, and patrol ships. The market is segmented by MRO type into engine MRO, dry dock MRO, component MRO, and modification. The report also covers the market sizes and forecasts for the naval vessel MRO market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Aircraft Carriers |

| Destroyers |

| Frigates |

| Corvettes |

| Submarines |

| Other Vessel Types (Support and Auxiliary Vessels, Unmanned Surface, and Underwater Vessels) |

| Engine MRO |

| Dry-Dock MRO |

| Component MRO |

| Modification and Upgrade |

| Organizational/Operational |

| Intermediate/Field |

| Depot |

| Nuclear-Powered Vessels |

| Conventional (Diesel/Gas Turbine) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | Egypt | |

| South Africa | ||

| Rest of Africa | ||

| By Vessel Type | Aircraft Carriers | ||

| Destroyers | |||

| Frigates | |||

| Corvettes | |||

| Submarines | |||

| Other Vessel Types (Support and Auxiliary Vessels, Unmanned Surface, and Underwater Vessels) | |||

| By MRO Type | Engine MRO | ||

| Dry-Dock MRO | |||

| Component MRO | |||

| Modification and Upgrade | |||

| By Maintenance Level | Organizational/Operational | ||

| Intermediate/Field | |||

| Depot | |||

| By Propulsion Type | Nuclear-Powered Vessels | ||

| Conventional (Diesel/Gas Turbine) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | Egypt | ||

| South Africa | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the expected value of global naval vessel MRO activity by 2031?

The naval vessel MRO market is projected to reach USD 73.66 billion by 2031 at a 3.09% CAGR.

Which region currently spends the most on naval maintenance and overhaul?

Asia-Pacific leads with 37.14% of 2025 spending, reflecting China’s fleet expansion and allied response programs.

Why are performance-based logistics contracts gaining favor?

PBL contracts shift availability risk to contractors while guaranteeing readiness, enabling navies to control costs and improve uptime, as seen in the USD 1.2 billion P-8A Poseidon deal.

How large is the nuclear-powered segment within naval vessel MRO?

Nuclear-powered vessels account for 53.21% of 2025 spending and are forecasted to grow 4.12% annually through 2031.

What is the main bottleneck limiting naval vessel MRO growth?

Shortage of dry-dock slots and escalating overhaul costs delay major programs by up to 18 months, constraining near-term capacity.

Which maintenance level shows the fastest growth?

Depot-level services are expanding at 4.66% CAGR because increasingly complex systems require specialized facilities and skills beyond ship-crew capability.

Page last updated on: