Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 21.63 Billion |

| Market Size (2031) | USD 28.68 Billion |

| Growth Rate (2026 - 2031) | 5.81% CAGR |

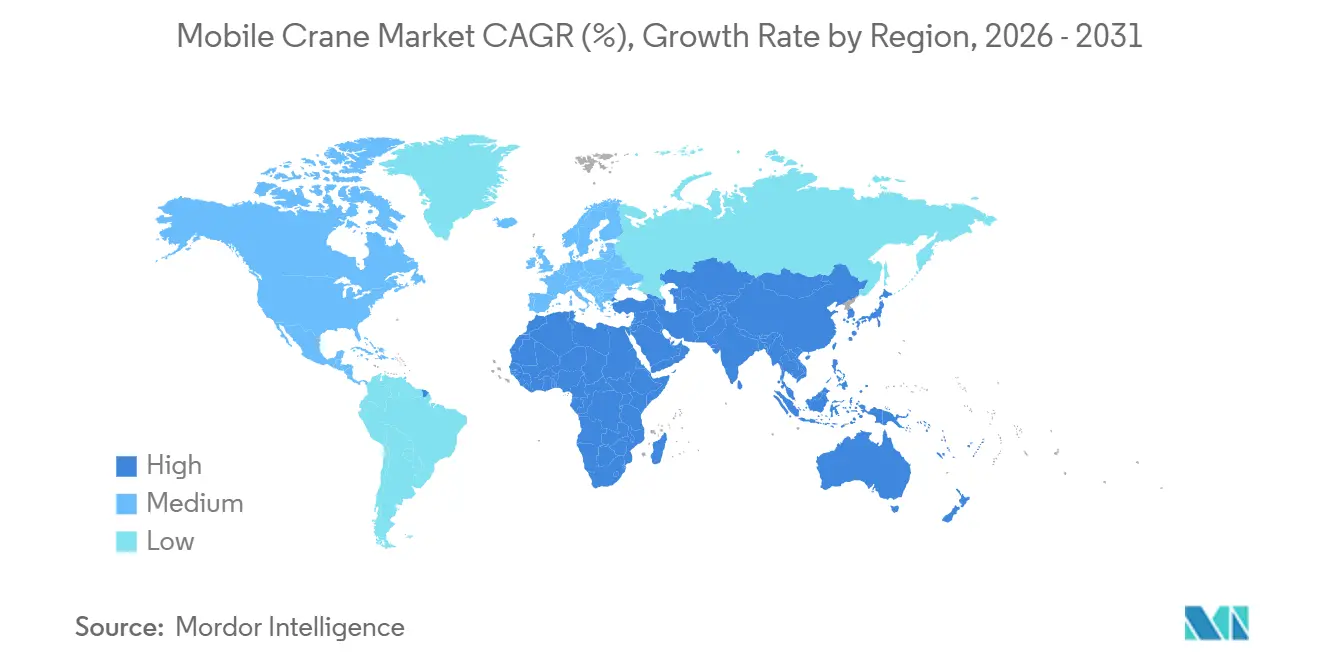

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

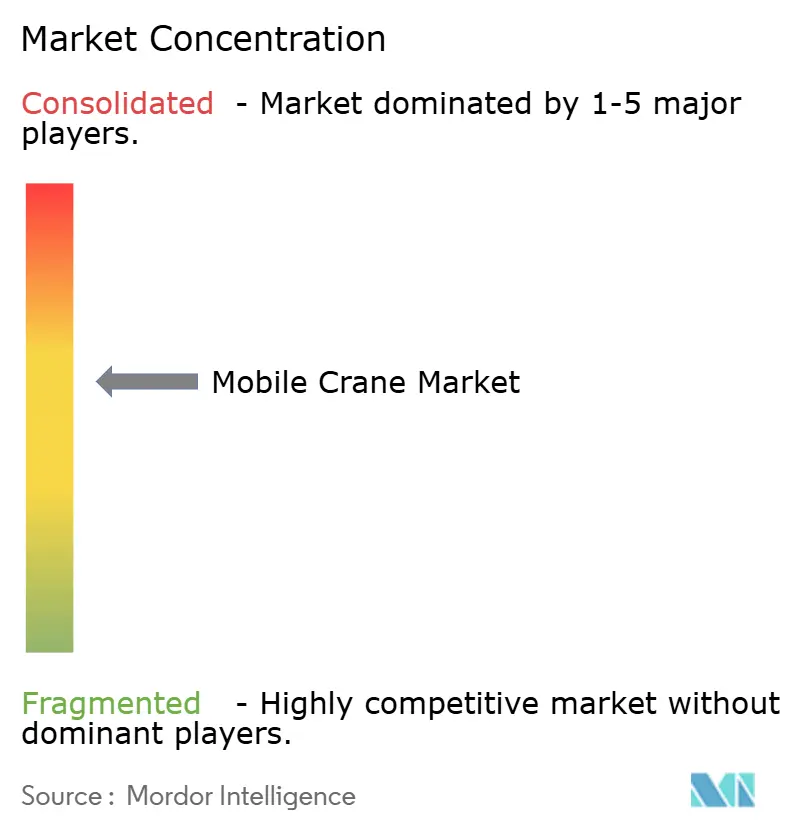

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Crane Market Analysis by Mordor Intelligence

The Mobile Crane Market size is estimated at USD 21.63 billion in 2026, and is expected to reach USD 28.68 billion by 2031, at a CAGR of 5.81% during the forecast period (2026-2031). This growth aligns with sustained public-private infrastructure commitments in OECD countries, a broad construction surge in emerging Asia anchored by China and India, and accelerated fleet-renewal cycles tied to Stage V and Tier 4-Final emission rules. Truck-mounted units still dominate day-to-day lifting, yet all-terrain models are posting the quickest revenue gains as contractors seek one-crane mobility across urban streets, gravel haul roads, and offshore lay-down yards. Asia-Pacific retains the largest regional footprint, while the Middle East & Africa corridor is rising quickest due to Saudi Vision 2030 giga-projects and the UAE’s port-and-airport build-out. Operators and rental fleets that integrate modular boom designs, telematics, and hybrid or battery-electric drivetrains are positioned to capture share as financing headwinds begin to ease and input-cost volatility stabilizes.

Key Report Takeaways

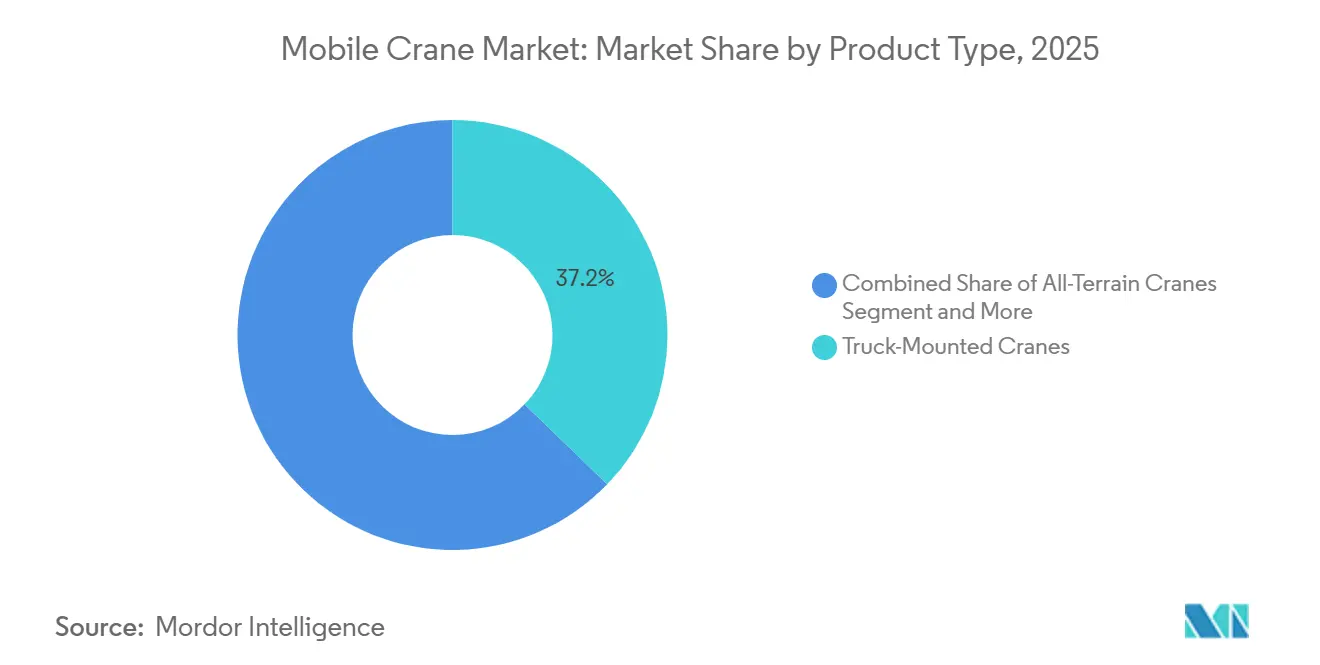

- By product type, truck-mounted cranes led with 37.17% revenue share in 2025; all-terrain cranes are forecast to expand at a 5.83% CAGR through 2031.

- By application, construction accounted for 53.41% of the mobile crane market share in 2025, while marine and offshore work is advancing at a 5.88% CAGR to 2031.

- By end user, rental companies held 43.45% of the 2025 base, yet government procurement is growing at a 5.85% CAGR through 2031.

- By lifting capacity, the 50-150 ton class commanded 38.73% share in 2025, whereas above-300-ton heavy-lift units are projected to grow at a 5.91% CAGR to 2031.

- By geography, Asia-Pacific captured 38.86% of 2025 demand; the Middle East & Africa corridor is set to log the fastest 5.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mobile Crane Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction Boom in Emerging Asia | +1.8% | Asia-Pacific core (China, India), spill-over to Southeast Asia | Medium term (2-4 years) |

| Rapid Public-Private Spending on 5G & Green-Energy Infrastructure (OECD Nations) | +1.4% | North America, Europe, advanced Asia-Pacific (Japan, South Korea) | Medium term (2-4 years) |

| Fleet Renewal Driven by Stage V / Tier 4-Final Emission Mandates (EU & NA) | +1.2% | Europe, North America | Short term (≤ 2 years) |

| Modular Boom Designs Slashing Transport/Setup Time | +0.7% | Global, with early gains in Europe, North America | Medium term (2-4 years) |

| Accelerating De-Risking of Offshore Wind Installation Through "Feeder" Jack-Ups | +0.5% | Europe (North Sea), Asia-Pacific (Taiwan, Japan), emerging in North America | Long term (≥ 4 years) |

| Growing Demand for Small-Footprint Cranes on Urban Infill Sites | +0.3% | Global urban centers, concentrated in Asia-Pacific, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Construction Boom in Emerging Asia

China and India continue to allocate record capital toward highways, metros, and water projects, ensuring multi-year visibility for the mobile crane market [1]“Union Budget FY 2024–25,” Government of India, indiabudget.gov.in . In India, the government has announced a substantial increase in capital outlays for infrastructure development, reflecting its commitment to enhancing the country’s connectivity and urban infrastructure. Similarly, China has reported consistent growth in its fixed-asset infrastructure spending, demonstrating its focus on expanding and modernizing its infrastructure network. The Asian Infrastructure Investment Bank has played a pivotal role by committing substantial funding across numerous projects, driving demand for truck-mounted and all-terrain cranes. These cranes are crucial for efficiently operating in both densely populated urban areas and remote, less accessible regions. Despite challenges such as a shortage of skilled operators and delays in the availability of components, the strong financial commitments and ongoing infrastructure initiatives are effectively mitigating supply-chain disruptions over the medium term.

Rapid Public-Private Spending on 5G & Green-Energy Infrastructure

OECD nations are expanding the mobile crane market's horizons by layering digital and energy-transition projects atop traditional civil works. GSMA forecasts that operator capital expenditures will remain substantial in the coming years, primarily driven by the need for 5G densification, which is expected to significantly increase demand for tower and rooftop lifts [2]“Global 5G Capex Outlook 2025,” GSMA, gsma.com. Currently, the expansion of hyperscale data centers is gaining momentum, with electricity consumption projected to grow considerably. This trend highlights the critical need for precise placement of heavy prefabricated modules to support these facilities [3]“Data Centres and Energy,” International Energy Agency, iea.org . The UK’s National Infrastructure Strategy has allocated significant funding for grid upgrades, aiming to accommodate a substantial increase in offshore wind capacity over the next decade. This initiative compels contractors to prioritize cranes that offer both high capacity and efficient rig-down cycles. Furthermore, the rise of modular construction methods is intensifying the demand for repeated high-accuracy lifts, all within increasingly compressed project schedules.

Fleet Renewal Driven by Stage V / Tier 4-Final Emission Mandates

In Europe and North America, stringent limits on particulates and NOx are driving the swift replacement of older, non-compliant fleets. Compared to earlier engine standards, the latest regulations significantly reduce particulate matter emissions to minimal levels. Similarly, the United States' advanced regulations achieve comparable reductions. According to industry estimates, this compliance push has moderately increased OEM build costs. However, rental companies are compelled to modernize their fleets, not only to obtain necessary permits but also to align with contractor sustainability goals. Highlighting the industry's shift, Liebherr’s LTM 1110-5.1 and Tadano’s ATF 70G-4 are leading the way with innovative single-engine designs that substantially reduce fuel consumption and simplify maintenance. These advancements underscore the industry's pivot towards more technologically sophisticated models, driven by regulatory pressures.

Modular Boom Designs Slashing Transport Time

OEMs are re-engineering boom sections so they fit into standard containers and bolt together on site, shrinking mobilization windows by up to two-fifths. Liebherr’s TCC 78000 and Manitowoc’s Grove family integrate configurable inserts that allow a single crane model to tackle multiple lift classes. The Port of NEOM pre-assembled ten mobile harbor cranes in modular form, cutting commissioning to six weeks and validating the cost-down thesis for far-flung projects. While upfront engineering costs rise, the payoff in reduced trucking, permitting, and idle time is reshaping procurement criteria for fleet owners.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steel Price Volatility Squeezing OEM Margins | -0.9% | Global, with acute pressure in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Skilled-Operator Shortages in OECD | -0.6% | North America, Europe, advanced Asia-Pacific (Japan, South Korea) | Medium term (2-4 years) |

| Grid-Carbon-Intensity Rules Delaying Diesel Crane Permits | -0.4% | Europe, California & select US states, advanced Asia-Pacific | Short term (≤ 2 years) |

| Financing Hurdles for Rental Fleets Amid Rising Interest Rates | -0.3% | Global, with acute pressure in OECD nations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Steel Price Volatility Squeezing OEM Margins

In recent years, the Producer Price Index for U.S. steel mill products experienced significant fluctuations, with a sharp increase followed by a notable decline before stabilizing. Since a substantial portion of structural steel is embedded in all-terrain cranes, original equipment manufacturers (OEMs) that entered into contracts during the period of elevated prices are now facing considerable pressure on their profit margins. A leading manufacturer highlighted the impact of rising costs, emphasizing the importance of strategies such as price surcharges and productivity improvements to mitigate the effects of volatile material costs. Smaller brands, however, often lack the ability to hedge against such fluctuations, forcing them to pass on costs to customers, which can undermine their competitiveness in the market. Additionally, rental fleets are encountering difficulties in forecasting residual values due to the unpredictable nature of commodity price trends.

Skilled-Operator Shortages in OECD

In 2024, a significant majority of U.S. firms faced challenges in filling equipment-operator roles, as reported by the Associated General Contractors of America. The workforce in this field is aging, with operators now predominantly in their late forties or older, while the rate of new certifications has remained stagnant over recent years. Europe is experiencing a comparable issue, with an aging labor force and declining enrollment in vocational schools, which is slowing the replacement of skilled workers. Wage inflation has been consistently high, creating additional pressure on rental margins and operational costs. Efforts to address these challenges include investments in advanced technologies such as telematics-enabled load-moment indicators and remote-assist systems, which aim to maximize the efficiency of the existing workforce. However, despite these measures, the gap between supply and demand for skilled operators is expected to persist throughout the forecast period.

Segment Analysis

By Product Type: All-Terrain Momentum Widens

The mobile crane market size attributed to product types shows truck-mounted units capturing 37.17% of 2025 revenue, while all-terrain cranes are projected to grow at a 5.83% CAGR through 2031. Liebherr’s LTM 1650-8.1 and Manitowoc’s Grove GMK6400-1 demonstrate how Stage V-compliant single-engine layouts cut fuel use by minimal and simplify maintenance. Operators in Europe and North America value the highway-legal configuration paired with off-road flexibility, a combination that encourages fleet rationalization. Emerging markets retain a preference for truck-mounted cranes because of lower acquisition cost and simpler service networks, yet stricter emission rules are slowly nudging buyers toward modern designs.

OEM differentiation is focusing on modular booms, telematics, and hybrid drivetrains. XCMG’s XCA400L8 integrates load-moment monitoring and automated outrigger deployment to reduce setup time, a feature set aimed at regions facing skilled-operator shortfalls. Crawler cranes maintain relevance for petrochemical and offshore projects, but their lower utilization rates in diverse civil work limit share gains. Rough-terrain and trailer-mounted models target mining, utility maintenance, and industrial plant shut-downs, yet incremental demand rests on commodity cycles rather than steady infrastructure spending. Taken together, the all-terrain segment’s rising share underscores a pivot toward versatile, emission-compliant equipment in the mobile crane market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Offshore Wind Lifts Marine Demand

Construction retained 53.41% of the 2025 mobile crane market share due to housing, commercial, and public works activity. Marine and offshore projects, however, are forecast to post a 5.88% CAGR to 2031 as 50 GW of U.K. offshore wind, Taiwanese multi-gigawatt rounds, and early U.S. Atlantic leases come online. Installation vessels such as Cadeler’s Wind Peak with a 2,500-tonne crane enable rapid turbine stacking, cutting cycle times, and raising demand for feeder cranes at marshaling ports. Industrial modules at data centers and semiconductor fabs also require precise heavy lifts, feeding higher utilization rates for telematics-equipped all-terrain units.

Mining and excavation remain cyclical, with dragline replacements tied to commodity price trends. Utility applications benefit from grid-reinforcement budgets and the roll-out of electric bucket trucks, reflecting broader electrification policies. Shipping and port infrastructure are buoyant in Saudi Arabia and the UAE, where the Port of NEOM deployed ten Liebherr mobile harbor cranes, signaling long-term lift demand as logistics hubs scale up. Collectively, the widening scope of non-building work sustains a diversified demand base within the mobile crane market.

By End User: Public Procurement Gains Traction

Rental companies represented 43.45% of 2025 end-user revenue, cementing their role as the default channel for contractors managing volatile project schedules. Yet government and municipal agencies are estimated to expand purchases at a 5.85% CAGR as national stimulus plans lock in multi-year infrastructure pipelines. Brazil’s Novo PAC allocates a vast amount, while the United Kingdom’s ten-year strategy earmarks a significant amount, translating into predictable tender volumes and framework agreements. Contractors continue to offload ownership risk onto rental firms, but rising sustainability, prevailing-wage, and domestic-content clauses are steering some agencies toward direct fleet acquisitions.

Refinery and power plant owners maintain a baseline of crawler and heavy-lift units for maintenance. However, as predictive analytics extends service intervals, the capital expenditure cycle is becoming more stable. Financing plays a crucial role: While high interest rates in the United States have limited lease affordability, Brazil's national development bank has provided significant financial support, offering a much-needed boost to the market. This shift towards public-sector involvement bolsters the mobile crane market, countering the cyclical nature of private construction.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Lifting Capacity: Heavy-Lift Outpaces the Mid-Range

Capacity mix data show the 50-150 ton class accounting for 38.73% of 2025 revenue, yet cranes above 300 tons are expected to rise at a 5.91% CAGR through 2031 on the back of modular nuclear, offshore wind, and hyperscale data center projects. Mammoet’s SK6000 ring crane, now in assembly with a 6,000-tonne maximum capacity, underscores the escalation path for ultra-heavy lifts. Sarens’ SGC-250 offers 5,000 tonnes, allowing single-piece lifts that compress on-site integration schedules.

Below 50 tons, compact all-terrain and city-class units thrive in dense urban cores, aided by zero-emission or hybrid propulsion that keeps them compliant in low-emission zones. The 151-300 ton bracket remains versatile, servicing bridge girders, billboard-sized HVAC modules, and 8-MW wind-turbine nacelles. California’s ACE list already includes Liebherr’s LR 1250.1 unplugged, indicating regulatory momentum toward electric heavy-lift solutions. The evolving capacity spectrum ensures that each project scale finds fit-for-purpose equipment within the mobile crane market.

Geography Analysis

Asia-Pacific captured 38.86% of the 2025 mobile crane market share, driven by steady growth in infrastructure spending in China and a substantial capital expenditure plan in India. Japan's robust construction activities, including major events like the Osaka Expo and advancements in transportation infrastructure such as maglev routes, continue to sustain demand. Meanwhile, South Korea's strong performance in construction-equipment exports highlights the region's manufacturing capabilities. Although challenges such as labor shortages and supply-chain disruptions persist, they have not significantly hindered the ongoing fleet-renewal cycles.

North America benefits from substantial investments in construction activities, with a notable focus on nonbuilding structures and a growing number of data-center projects fueled by advancements in artificial intelligence. Despite the impact of higher interest rates on leasing markets, operators are effectively leveraging federal tax incentives and state-level infrastructure grants to modernize equipment and adopt newer technologies. In Canada, while the scope of projects is narrower, key initiatives remain centered on energy infrastructure and transit system expansions. Europe, recovering from a recent downturn, is witnessing a resurgence in construction activities. The United Kingdom is experiencing steady growth, supported by a long-term infrastructure roadmap, while Germany's energy transition efforts are driving the repowering of onshore turbines. Across the European Union, ambitious infrastructure goals over the coming decades are expected to sustain demand for heavy-lift equipment in large-scale transport and grid projects.

South America is progressing at a slower pace, with Brazil's construction sector showing gradual growth, supported by government funding directed toward numerous concession and public-private partnership initiatives. BNDES credit approvals underscore selective liquidity pockets even as Argentina wrestles with macro instability. The Middle East & Africa corridor holds the fastest 5.87% CAGR, fueled by Saudi Arabia’s project slate and UAE logistics upgrades. NEOM’s deployment of ten Liebherr harbor cranes exemplifies the heavy civil tempo, while South Africa pushes to stabilize power supply before scaling infrastructure outlays.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Global giants like Liebherr, XCMG, SANY, Zoomlion, Tadano, Manitowoc, and Terex collectively dominate a significant portion of the mobile crane market, indicating a moderate level of market concentration. Their strategic priorities are centered on achieving compliance with emission regulations, advancing electrification, and integrating digital technologies. Liebherr’s electric crawler cranes, designed to meet stringent zero-emission mandates in regions such as California and Europe, exemplify this focus. Similarly, Zoomlion’s concept for battery-electric truck cranes highlights the efforts of Chinese OEMs to cater to cost-sensitive markets with innovative solutions.

Rental-fleet consolidators are increasingly adopting advanced telematics systems, such as Tadano’s Hello-Net and Manitowoc’s Crane Control System, to enhance operational efficiency, minimize downtime, and document environmental, social, and governance (ESG) metrics. The volatility in steel prices has intensified the need for cost management, shifting the competitive focus from initial purchase price to the overall cost of ownership. Heavy-lift specialists, including Mammoet and Sarens, are investing in cutting-edge super-ring cranes capable of handling extremely heavy loads. These cranes are being deployed for complex projects such as offshore wind farm staging and the construction of small modular reactors, allowing these companies to establish a premium niche within the broader mobile crane market.

Emerging opportunities are concentrated in areas such as urban infill lifting, upgrades for feeder jack-up vessels, and the production of modular nuclear components. Chinese manufacturers are leveraging their domestic production scale to offer competitively priced solutions, enabling them to outpace Western competitors in regions like Asia, Latin America, and Africa. On the other hand, established players are relying on their extensive service networks and advanced engineering capabilities to maintain their market positions. Although challenges such as fluctuating input costs and a shortage of skilled operators add complexity to operations, the sustained demand for infrastructure development provides original equipment manufacturers (OEMs) and rental firms with a strong foundation to continue investing in technological advancements throughout the forecast period.

Mobile Crane Industry Leaders

Cargotec Corporation

Terex Corporation

TADANO Ltd

Konecranes Plc

Zoomlion Heavy Industry Science & Technology Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: ZF Friedrichshafen AG launched series production of steer-by-wire systems for NIO’s ET9, signaling progress toward fully electronic steering on heavy mobile platforms.

- December 2024: Robert Bosch GmbH began manufacturing electric steering systems in Hungary to meet surging European demand, strengthening regional supply chains that include crane-component vendors.

Global Mobile Crane Market Report Scope

The scope of the report includes Product Type (Truck-Mounted and More), Application (Construction, Mining & Excavation, and More), End User (Rental Companies, Contractors, and More), Lifting Capacity (Below 50 Tons and More), and Geography.

By Product Type

| Truck-Mounted Cranes |

| Trailer-Mounted Cranes |

| Crawler Cranes |

| All-Terrain Cranes |

| Rough Terrain Cranes |

| Others |

By Application

| Construction |

| Mining & Excavation |

| Industrial Applications |

| Marine & Offshore |

| Utility |

| Shipping & Port Building |

By End User

| Rental Companies |

| Construction Contractors |

| Government & Municipalities |

| Industrial Operators |

By Lifting Capacity

| Below 50 Tons |

| 50–150 Tons |

| 151–300 Tons |

| Above 300 Tons |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Truck-Mounted Cranes | |

| Trailer-Mounted Cranes | ||

| Crawler Cranes | ||

| All-Terrain Cranes | ||

| Rough Terrain Cranes | ||

| Others | ||

| By Application | Construction | |

| Mining & Excavation | ||

| Industrial Applications | ||

| Marine & Offshore | ||

| Utility | ||

| Shipping & Port Building | ||

| By End User | Rental Companies | |

| Construction Contractors | ||

| Government & Municipalities | ||

| Industrial Operators | ||

| By Lifting Capacity | Below 50 Tons | |

| 50–150 Tons | ||

| 151–300 Tons | ||

| Above 300 Tons | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the mobile crane market by 2031?

The market is forecast to reach USD 28.68 billion by 2031, growing at a 5.81% CAGR.

Which product type is expanding fastest in mobile lifting?

All-terrain cranes are projected to post the highest 5.83% CAGR through 2031, due to emission compliance and multi-terrain agility.

How large is Asia-Pacific’s share of global demand?

Asia-Pacific accounted for 38.86% of 2025 revenue and continues to anchor growth through large-scale infrastructure spending.

Why are heavy-lift cranes above 300 tons in demand?

Ultra-large wind turbines, modular nuclear components, and hyperscale data center modules require single-piece lifts that only heavy-lift models can handle.

What regulatory trend is accelerating fleet renewal?

Stage V and Tier 4-Final emission mandates push fleet owners to replace older diesel units with compliant, fuel-efficient models.

How are operator shortages being addressed?

Rental firms and OEMs deploy telematics, load-moment indicators, and remote-assist systems to boost safety and productivity while training programs scale up new talent.