Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.07 Billion |

| Market Size (2026) | USD 1.16 Billion |

| Market Size (2031) | USD 1.77 Billion |

| Growth Rate (2026 - 2031) | 8.79% CAGR |

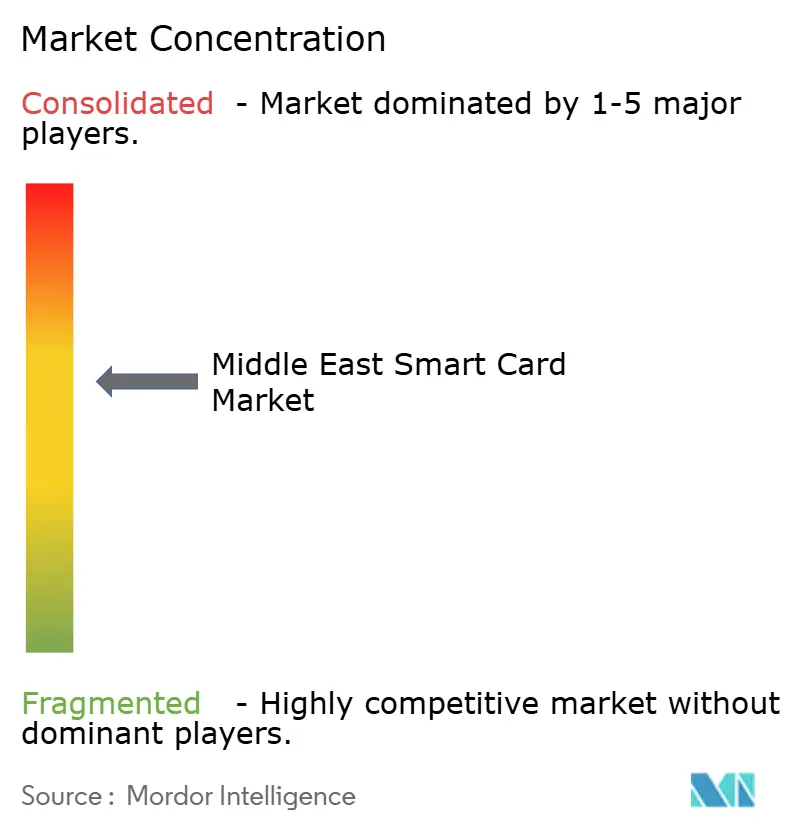

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East Smart Card Market Analysis by Mordor Intelligence

The Middle East smart card market size is expected to grow from USD 1.07 billion in 2025 to USD 1.16 billion in 2026 and is forecast to reach USD 1.77 billion by 2031 at 8.79% CAGR over 2026-2031. Robust public-sector digitization programs in Saudi Arabia and the UAE, cashless payment mandates, and mega-infrastructure projects such as Riyadh Metro are accelerating card issuance across identity, transit, payment, and telecommunication domains.[1]Saudi Vision, “Pilgrim Experience Program,” Saudi Vision 2030, vision2030.gov.saSupply-side momentum stems from European technology leaders deepening local partnerships, while rising 5G roll-outs spur high-end SIM replacements and stimulate demand for secure microcontroller chips. Governments are prioritizing biometric e-ID schemes that embed multiple applications on a single credential, ensuring multi-year volume visibility for suppliers. However, standardization gaps among GCC and Levant schemes, chip shortages, and the surge of mobile wallets introduce implementation risk and margin pressure.

Key Report Takeaways

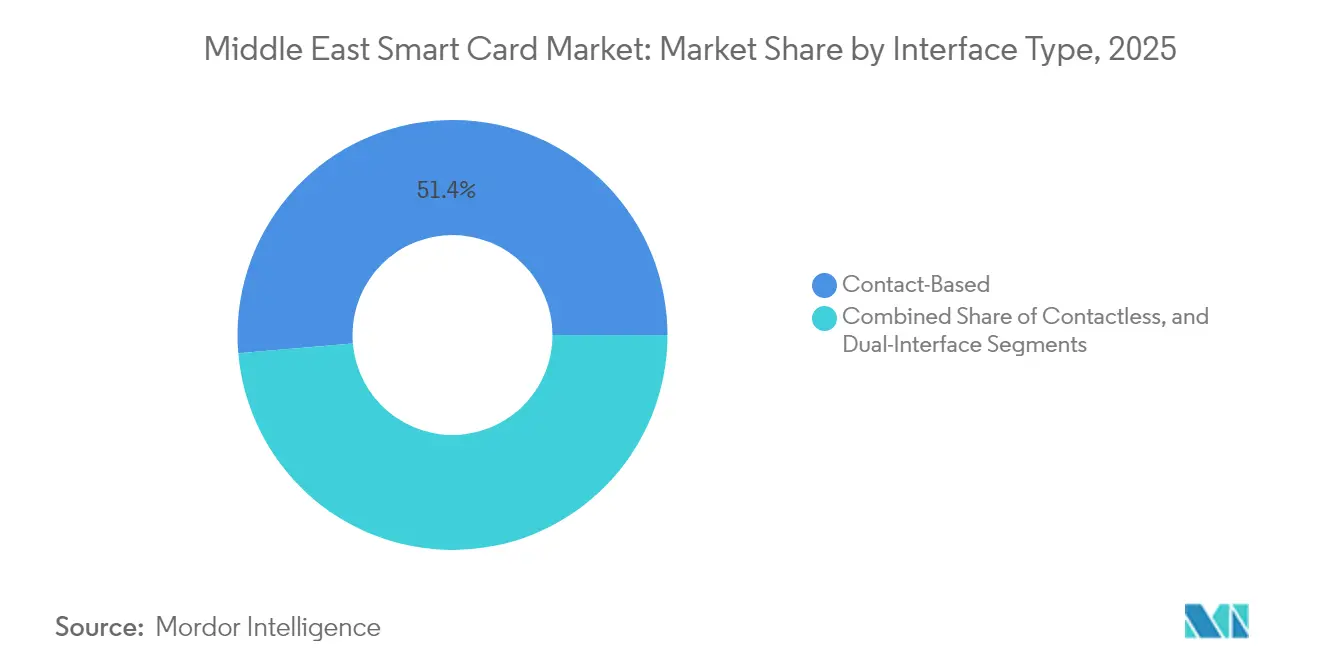

- By interface type, contact-based cards led with 51.36% revenue share in 2025; contactless is projected to expand at a 9.41% CAGR through 2031.

- By chip type, micro-controller smart cards accounted for 65.28% of the Middle-east smart card market size in 2025, while system-on-chip devices are forecast to grow at 11.06% CAGR to 2031.

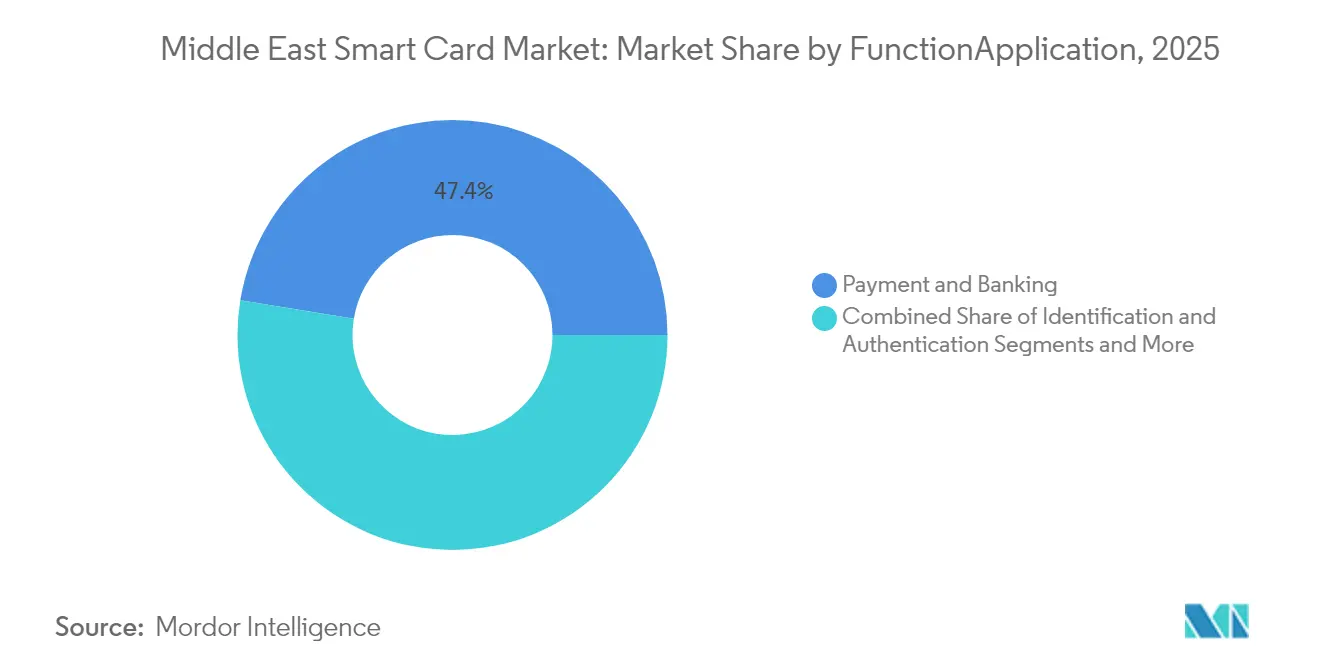

- By function, payment & banking captured 47.42% share of the Middle-east smart card market size in 2025; IoT & emerging uses will rise at 10.74% CAGR over 2026-2031.

- By end-user vertical, BFSI held 41.33% of Middle-east smart card market share in 2025; government & public ID applications show the highest 10.93% CAGR outlook.

- By country, Saudi Arabia dominated with 38.12% revenue share in 2025, while the UAE is poised for the fastest 10.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Smart Card Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National e-ID & e-Passport Roll-outs across GCC | +2.1% | GCC countries with spillover to Levant | Medium term (2-4 years) |

| Vision-2030–led Cashless Payment Mandates in Saudi Arabia & UAE | +1.8% | Saudi Arabia & UAE core, expansion to Qatar, Kuwait | Long term (≥ 4 years) |

| Mass-Transit Smart-Ticketing for Mega-Projects | +1.3% | Saudi Arabia, UAE, Qatar with infrastructure focus | Short term (≤ 2 years) |

| 5G SIM Replacement Cycle Boosting High-End Micro-controller Cards | +0.9% | Global with GCC early adoption | Medium term (2-4 years) |

| Smart Hajj/Umrah ID Initiatives Driving High-Volume Issuance Peaks | +0.7% | Saudi Arabia national, regional pilgrimage impact | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

National e-ID & e-Passport Roll-outs across GCC

GCC governments have made biometric civil ID a centrepiece of digital public-service delivery. The UAE will decommission physical Emirates ID cards by late 2025, transitioning to face- and fingerprint-verified digital credentials that remain accessible through secure mobile wallets. Oman already maintains 100% population coverage with multi-application smart IDs supplied by Thales. Kuwait’s MY KUWAIT ID app embeds additional verification layers that strengthen access to more than 70 e-government services. Such programmes elevate unit volumes and drive the Middle East smart card market as ministries demand interoperable solutions capable of cross-border authentication.

Vision-2030-Led Cashless Payment Mandates in Saudi Arabia & UAE

Saudi Arabia’s Mada network expansion and Dubai’s target of 90% cashless transactions by 2026 institutionalise card-based payments across retail, transport, and government service payments.[2]Saudi Arabian Monetary Authority, "The New Identity of the Saudi Payment Network (MADA)", rulebook.sama.gov.sa Simultaneously, the Central Bank of the UAE will introduce the Digital Dirham in late 2025, embedding tokenisation and smart-contract capabilities that must interface seamlessly with advanced card hardware. Cash-on-delivery usage in MENA halved from 41% in 2020 to 20% in 2023, underscoring behavioural shifts favouring contactless card infrastructure.

Mass-Transit Smart-Ticketing for Mega-Projects

The USD 25 billion Riyadh Metro integrates physical and mobile smart-ticketing across its 176-kilometre network, creating large-volume orders for secure transit cards. Dubai’s platform now supports digital issuance via NFC smartphones, further expanding user convenience while maintaining the card backbone for tourists and residents alike. These projects embed payment, loyalty, and identity features into a single transit credential, reinforcing the strategic relevance of the Middle East smart card market.

5G SIM Replacement Cycle Boosting High-End Micro-controller Cards

GCC operators accelerate 5G coverage and plan for 6G spectrum allocation by 2028, triggering a natural SIM upgrade cycle demanding higher-capacity secure elements capable of supporting mobile broadband, eSIM, and IoT authentication. Saudi Arabia and the UAE collectively spent USD 60 billion on ICT infrastructure in 2024, driving volumes for advanced SIM cards that underpin subscriber migration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inter-operability Gaps between GCC & Levant Card Standards | -1.4% | Regional cross-border applications | Medium term (2-4 years) |

| Grey-Market Counterfeit Card Inflows Undermining Security Trust | -1.1% | Regional with focus on high-volume markets | Short term (≤ 2 years) |

| Imported IC Shortages due to Global Export Controls & Logistics | -0.9% | Global supply chain affecting regional production | Medium term (2-4 years) |

| Mobile-Wallet Cannibalisation in Affluent Gulf States | -0.8% | UAE, Qatar, Kuwait with high smartphone penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Interoperability Gaps between GCC & Levant Card Standards

While GCCNET unifies ATM clearing, card certification protocols remain fragmented across neighbouring markets, forcing issuers to carry multiple product SKUs and slowing cross-border service harmonisation.[3]Qatar Central Bank, "Electronic Payments And Settlements Systems 2", qcb.gov.qa Lebanon’s adoption of alternate biometric standards for border control exemplifies the technical divergence that elevates certification cost and complexity.

Mobile-Wallet Cannibalisation in Affluent Gulf States

High smartphone adoption rates in the UAE, Qatar, and Kuwait support rapid wallet penetration, which competes directly with physical payment cards for consumer mindshare. Palm-vein payment acceptance in the UAE and the scheduled 2025 launch of Google Wallet in Egypt illustrate the consumer gravitation toward device-native payments. Card vendors thus must reposition toward applications where device independence and multi-factor security remain indispensable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Interface Type: Contactless Surge Accelerates Transit Integration

Contact-based credentials remain dominant due to legacy bank and e-ID programmes, yet the contactless wave is unmistakable. In 2025, contactless cards represented 48.00% issuance and are advancing at 9.41% CAGR. The Middle East smart card market size for contactless platforms is forecast to add USD 258.6 million between 2026 and 2031 as transit operators and retailers retrofit NFC readers. Dual-interface cards mitigate migration risk by embedding both modes and already account for 19.00% of new volumes.

Transit agencies favour contactless because it speeds passenger flow and supports multi-modal integration. Retail chains deploy tap-to-pay because it aligns with regional social-distancing preferences adopted during the pandemic. Meanwhile, biometric overlays—such as palm-vein or facial match—are beginning to secure high-value contactless limits, reinforcing confidence in frictionless payment. These factors ensure the contactless segment will overtake contact-based share well before 2031, cementing its status as the long-term growth engine of the Middle East smart card market.

By Chip Type: System-on-Chip Innovation Drives Premium Applications

Microcontroller units currently dominate with a share of 65.28% in 2025 due to established certification pedigree and broad application across payments, telecom, and ID. Nevertheless, SoC architectures are growing fastest at 11.06% CAGR because they consolidate CPU, secure element, and wireless interface in one die, reducing BOM and footprint. The Middle East smart card market size for SoC platforms is poised to reach USD 223.4 million by 2031.

Regional sovereign investment in semiconductor design hubs—exemplified by Saudi Arabia’s SAR 1 billion (USD 266 million) National Semiconductor Hub—signals a future shift toward domestic IP and packaging capacity. European technology leaders respond by localising value chains; IDEMIA invested EUR 20 million (USD 21.6 million) in capacity that guarantees European source traceability while serving GCC data-protection mandates. Infineon’s SECORA Pay Green exemplifies the parallel sustainability imperative, cutting virgin plastic and CO₂ by 60%

By Function/Application: IoT Integration Expands Beyond Traditional Uses

Payment and Banking continue to anchor revenue with a share of 47.42% in 2025, yet IoT & Other emerging uses will grow the highest with a CAGR of 10.74% due to industrial automation, and smart-grid metering will stimulate double-digit volume growth. The Middle East smart card market adds roughly 5 million IoT credentials annually, reflecting burgeoning smart-city deployments such as NEOM that rely on secure device identity. Healthcare is another frontier: Malaffi in Abu Dhabi references 1.7 billion clinical records and aims to issue patient-centric access cards that travel across public and private facilities.

Pilgrimage management showcases cross-sector convergence: health screening, identity, payment, and feedback now reside on one token. Such multi-application adoption lifts ASPs and creates pull-through for SoC chips with larger EEPROM and crypto libraries. As sovereign CBDC projects mature, offline retail transactions will require robust card-resident smart-contract execution, further elevating the Middle East smart card market demand for compute-rich secure elements.

By End-User Vertical: Government Sector Leads Digital Transformation

BFSI retains a plurality of shipments and holds a majority share of 41.33% in 2025, driven by EMV renewal cycles and regulator-mandated contactless upgrades. Yet, government volumes grow faster with a CAGR 10.93% during forecast period.because every citizen and resident must be enrolled in e-ID schemes. Kuwait has already biometrically registered 3 million people—nearly 70% of its population—prior to the full Vision 2035 roll-out.

Enterprise access control is another high-growth niche as oil & gas majors adopt card-plus-mobile credential frameworks to harden security. Network International’s deployment of FICO fraud analytics across 180 million annual transactions underscores BFSI's emphasis on layered security, validating continuous investment in card-centric risk controls. Cross-selling opportunities emerge where one credential spans facility entry, time-and-attendance, canteen payment, and secure printing, boosting token utility and retention.

Geography Analysis

Saudi Arabia’s 38.12% share of the Middle East smart card market in 2025 stems from the Kingdom’s USD 133.3 billion infrastructure outlay and the scale of nationwide e-ID, transit, and pilgrimage programmes. The Riyadh Metro alone triggered multi-year procurement of dual-interface cards for 6 lines and 84 stations. Moreover, Alat’s USD 100 billion capital plan to localise electronics production could shorten lead times for card modules.

The UAE records the fastest 10.28% CAGR, attributable to a decisive pivot toward biometric governance and central-bank digital currency experimentation. Its agile regulatory environment lets vendors pilot biometric payments such as palm-vein matching at scale, reinforcing the nation’s position as the sandbox for regional fintech innovation.

Qatar’s post-World-Cup infrastructure legacy includes integrated e-government and transit platforms; its Digital ID app already provides e-gate access at Hamad International Airport, signalling stable card demand growth. Kuwait and Bahrain emphasise cashless agendas linked to diversified economic visions; Bahrain’s stcPay ecosystem integrates tokenised payments that still rely on card back-ends for settlement. Oman's Vision 2040 fosters mobile payment adoption yet still depends on 100% smart-ID penetration as the trust anchor.

Competitive Landscape

European incumbents dominate supply thanks to decades-deep IP portfolios and Common Criteria-certified secure elements. Thales, IDEMIA, and Giesecke+Devrient collectively control an estimated 55% of regional shipments, underpinning a moderately concentrated market. IDEMIA Secure Transactions posted EUR 1.5 billion (USD 1.6 billion) revenue in its inaugural year, funneling R&D toward quantum-safe firmware and offline CBDC functionality to pre-empt central-bank requirements. G+D’s EUR 490 million (USD 528 million) R&D spend in 2023 underscores sustained leadership in cryptographic innovation.

Component players NXP and Infineon reinforce the upstream ecosystem by supplying high-performance 40 nm and 28 nm secure MCUs; Infineon’s SECORA Pay Green answers GCC ESG imperatives by cutting plastic and adding recycled PET-G substrates. HID Global’s decision to expand engineering resources in Saudi Arabia and launch the Amico biometric reader reflects a localisation strategy calibrated against Vision 2030 public-security investments.

M&A remains an accelerant: IN Groupe’s planned acquisition of IDEMIA Smart Identity would form a EUR 1 billion (USD 1.1 billion) entity with extended Middle-east reach, potentially consolidating passport, ID, and border-control tenders. TOPPAN Security’s purchase of dzcard widens laminates and module production in Asia, ensuring supply resilience for GCC issuers. Such moves illustrate strategic vertical integration and geographic hedging aimed at protecting share in the Middle-east smart card market.

Middle East Smart Card Industry Leaders

-

Thales Group

-

IDEMIA (Advent International)

-

Infineon Technologies AG

-

HID Global Corporation

-

Eviden (Atos Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: TOPPAN Security acquires Dzcard Group to secure upstream module capacity and deepen regional smart-card penetration in anticipation of GCC volume surges.

- May 2025: Smart Payment Association reports 2.5 billion cards shipped in 2024, 92% contactless; sustainability card volumes lift 28%, signposting materials shift in Middle-east smart card market procurement.

- April 2025: UAE Federal Authority for Identity rolls out biometrics-only Emirates ID, eliminating plastic issuance and pivoting vendors toward digital secure element provisioning.

- March 2025: Central Bank of the UAE confirms late-2025 retail Digital Dirham, linking CBDC wallets to tokenised card rails for offline acceptance at POS.

Middle East Smart Card Market Report Scope

A smart card is a pocket-sized card made from plastic and embedded with integrated circuits known as microchips. The applications of smart cards are for security purposes such as authentication, identification, data storage, and application processing. Contactless smart cards are made by deploying a radio frequency between the card and any reader that requires no physical insertion. Contactless smart cards are expected to have wider applications and, on account of being user-friendly, are expected to be accepted much faster than contact-based smart cards.

The Middle East Smart Card Market is Segmented by Type (Contact-Based, Contact Less), End-User (BFSI, IT and Telecommunication, Government, Transportation), and country.

By Interface Type

| Contact-Based |

| Contactless |

| Dual-Interface |

By Chip Type

| Memory Smart Cards |

| Micro-controller Smart Cards |

| System-on-Chip and Others |

By Function / Application

| Payment and Banking |

| Identification and Authentication |

| SIM and Telecommunications |

| Transit and Ticketing |

| Healthcare |

| IoT and Other Niche Uses |

By End-User Vertical

| BFSI |

| IT and Telecommunications |

| Government and Public Sector |

| Transportation and Logistics |

| Healthcare |

| Retail and Loyalty |

| Others |

By Country

| United Arab Emirates |

| Saudi Arabia |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| Israel |

| Rest of Middle-East |

| By Interface Type | Contact-Based |

| Contactless | |

| Dual-Interface | |

| By Chip Type | Memory Smart Cards |

| Micro-controller Smart Cards | |

| System-on-Chip and Others | |

| By Function / Application | Payment and Banking |

| Identification and Authentication | |

| SIM and Telecommunications | |

| Transit and Ticketing | |

| Healthcare | |

| IoT and Other Niche Uses | |

| By End-User Vertical | BFSI |

| IT and Telecommunications | |

| Government and Public Sector | |

| Transportation and Logistics | |

| Healthcare | |

| Retail and Loyalty | |

| Others | |

| By Country | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| Israel | |

| Rest of Middle-East |

Key Questions Answered in the Report

How big is the Middle-east smart card market in 2026?

The Middle-east smart card market size stands at USD 1.16 billion in 2026.

What is the projected CAGR for the Middle-east smart card market?

The market is forecast to grow at 8.79% CAGR between 2026 and 2031.

Which country leads the Middle-east smart card market share?

Saudi Arabia dominates with 38.12% share in 2025, owing to large-scale e-ID and transit investments.

Which segment is growing fastest?

System-on-chip cards record the highest 11.06% CAGR as IoT and CBDC use cases demand higher compute.

What role do cashless mandates play in market growth?

Mandatory cashless targets under Saudi Vision 2030 and Dubai’s 90% cashless goal significantly lift demand for contactless payment cards.

How is sustainability influencing card procurement?

Vendors such as Infineon now offer recyclable card platforms that cut plastic waste by up to 100%, aligning with GCC ESG policies.

Page last updated on: